Flight Data Monitoring Market Size, Share & Industry Analysis, Aircraft Type (Fixed Wing (Narrow-Body, Wide Body, Business Jets, and Regional jets), Rotary Wing, and UAVs), By Component (Hardware, Software & analytics, and Services), By End-User (Commercial passenger airlines, Cargo airlines & logistics operators, Business aviation operators, Helicopter operators, & Others), By Application (Safety & risk management, Regulatory compliance & reporting, Operational efficiency, & Others), By Deployment (On-premise, Cloud, and Hybrid), and Regional Forecast, 2026-2034

Flight Data Monitoring Market Size and Future Outlook

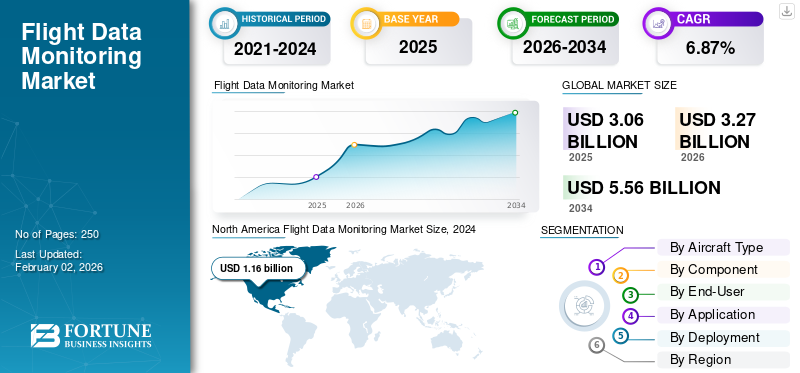

The global flight data monitoring market size was valued at USD 3.06 billion in 2025. The market is projected to grow from USD 3.27 billion in 2026 to USD 5.56 billion by 2034, exhibiting a compound annual growth rate CAGR of 6.78% during the forecast period. North America dominated the global flight data monitoring market with a market share of 39.54% in 2025.

The flight data monitoring (FDM) market centers on systems and services that capture, transmit, and analyze detailed digital flight data from aircraft to improve safety, efficiency, and maintenance. Often branded as FDM, FOQA, or FDAP, these programs were formalized under ICAO Annex 6, which recommends that operators of large aircraft and helicopters implement structured flight-data analysis as part of their accident-prevention and safety-management systems. Market growth is being driven by tighter regulatory expectations, airlines’ push to reduce incidents and fuel burn, and the broader digitalization of flight operations.

EASA’s EOFDM initiative shows how regulators now expect FDM outputs to feed directly into safety risk management, crew training, not just exceedance statistics. At the same time, leading carriers are deploying cloud-based analytics platforms and pilot-facing mobile apps that put de-identified flight-data insights across flight crews and operations teams. GE Aerospace, for instance, offers the Safety Insight FDM platform and the Flight Pulse pilot app; SITA provides OptiFlight and eWAS for fuel and weather optimization; Airbus’s NAVBLUE, Honeywell, Collins Aerospace, Safran, and Teledyne Controls all supply integrated FDM and flight-operations analytics solutions.

Recent contracts such as Korean Air’s group-wide adoption of GE’s Safety Insight and the Air India Group’s rollout of SITA’s OptiFlight/eWAS illustrate how Tier-1 airlines in Asia are investing heavily in FDM-centered digital stacks to reduce operational risk, fuel burn, and emissions.

GE reports that its Flight Pulse app has grown from 40,000 to more than 60,000 pilot users across 42 airlines, signaling a strong global appetite for pilot-level analytics derived from FDM datasets. This growth underlines the market’s shift from a compliance tool to an everyday operational platform.

Major players in the global flight data monitoring (FDM) market include Teledyne (Teledyne Controls), Curtiss‑Wright, Safran (Safran Electronics & Defense), and L3Harris, which supply integrated FDM hardware, software, and avionics-linked systems to airlines and OEMs.

Download Free sample to learn more about this report.

Flight Data Monitoring Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.06 billion

- 2026 Market Size: USD 3.27 billion

- 2034 Forecast Market Size: USD 5.56 billion

- CAGR: 6.78% from 2026–2034

- North America dominated the market with a 39.54% share in 2025.

- Software & Analytics accounted for the largest market share.

- UAVs segment is expected to grow at the highest CAGR of 9.17% from 2026–2034.

North America

Valued at USD 1.21 billion in 2025, supported by mature FDM programs, strong airline adoption, and FAA-backed safety initiatives.

Europe

Second-largest market, driven by stringent aviation safety regulations and strong industry collaboration on flight data monitoring.

Asia Pacific

Expected to witness the fastest growth, driven by rising air traffic, fleet expansion, and increasing adoption of advanced FDM analytics.

U.S.

Expected to witness steady growth, supported by widespread adoption of pilot analytics and long-established FDM programs.

Japan

Expected to witness steady growth, driven by increasing focus on aviation safety, operational efficiency, and advanced flight data analytics.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Regulatory Pressure and Rising Need for Maintaining Formal Flight Data Analysis to Fuel Market Growth

The primary growth driver in the flight data monitoring (FDM) market is the convergence of regulatory requirements with airline safety strategies. ICAO, EASA, and many national authorities now expect operators of larger aircraft and helicopters to maintain formal flight data analysis or FDM programs as part of their safety management systems, rather than treating them as optional add-ons. Large carriers are extending these programs beyond simple exceedance counting into continuous risk monitoring, fuel efficiency, and flight-crew training, which lifts both per-aircraft spend and analytics complexity. Regional CAAs in emerging markets are also issuing their own FDAP/FDM guidance, bringing smaller fleets into scope over the forecast period.

- In March 2024, EASA published NPA 2024-02, proposing enhancements to EU air-operations rules on FDM programs, with the explicit aim of improving implementation quality and embedding lessons learned from safety recommendations, thereby reinforcing regulatory demand for robust FDM.

MARKET RESTRAINTS:

Lack of Budget and IT Infrastructure to Act As A Restraint For Growth

The main restraint is that a high-quality FDM program remains resource-intensive and organizationally sensitive. Smaller airlines, regional operators, and helicopter fleets often lack the budget, IT infrastructure, and specialist analysts needed to ingest, clean, and interpret large volumes of flight parameters data. Guidance from ICAO and several CAAs emphasizes that FDM/FDAP must be non-punitive; however, in practice, some pilots and union aviation personnel remain cautious about how data might be used, which hinders cultural adoption. At the same time, debates over data ownership and data-sharing rights have compelled operators, OEMs, and regulators to address contractual and privacy concerns before scaling new use cases.

- In October 2024, IATA, along with Airbus, Embraer, and Rolls-Royce, agreed on five principles governing access to and use of aircraft operational data, directly addressing ownership, consent, and governance concerns that have been a barrier to broader data-driven programs.

MARKET OPPORTUNITIES:

Growing Regulatory and OEM Pressure for Continuous FDM Presents a Major Market Opportunity

The biggest opportunity for the market is the shift from viewing FDM as a core driver of operational performance and reliability. OEMs and safety bodies increasingly emphasize that routine flight data analysis can identify operational risks, unstable-approach trends, fuel-burn inefficiencies, and earlier technical issues long before they escalate into incidents or unplanned maintenance. Airlines that integrate FDM outputs into engineering, network operations, and training functions demonstrate a strong business case: fewer safety events, lower fuel consumption, and more predictable maintenance planning. The opportunity is widening beyond major carriers into low-cost carriers, regional fleets, and high-end business aviation operators that are starting to adopt airline-style FDM capabilities to improve safety and efficiency.

- In July 2024, Korean Air signed a major contract to deploy GE Aerospace’s Safety Insight FDM system across its mainline and low-cost subsidiary, Jin Air. This explicitly links advanced flight data analytics to future safety, efficiency, and predictive maintenance gains, signaling how Tier-1 airlines are monetizing FDM beyond compliance.

Flight Data Monitoring MARKET TREND:

Adoption of Cloud Analytics and Pilot-facing Apps is a Major Market Trend

Technology is reshaping how FDM is delivered and consumed. Cloud-based platforms, big data tooling, and automation now enable airlines to process far more parameters per flight and generate near-real-time insights for safety and engineering teams. Vendors are also moving “downstream” toward the cockpit with pilot-facing apps that return de-identified FDM data back to crews for self-improvement, closing the loop between analysis and behavior change, thereby driving flight data monitoring market growth. At the same time, new platforms such as eVTOL and advanced air mobility are designing OEM-level FDM/FOQA into their aircraft architectures from the outset rather than adding them as retrofit compliance tools.

- In October 2025, Reuters reported that GE Aerospace’s FlightPulse flight-data app grew from 40,000 to over 60,000 commercial pilot users within a year, with airlines paying on a per-pilot basis for access. This demonstrates the strong demand for pilot-level analytics built on FDM data and validates the market’s accelerating shift toward real-time, operationally embedded digital safety tools.

MARKET OPPORTUNITY:

Shift Toward GNSS-Based and Automated Inspection Systems to Fuel Industry Growth

The most prominent technological trend in the flight data monitoring market is the migration toward GNSS-based navigation validation and automated flight profiles. These systems enable higher accuracy in navigation-aid calibration while minimizing human error and mission duration. Advanced data logging, AI-assisted route planning, and real-time signal integrity assessment tools are further enhancing the efficiency of flight data monitoring. The adoption of dual-use inspection aircraft capable of handling both conventional and satellite-based systems is increasing among ANSPs and defense operators. Automation is also extending into mission management, improving repeatability and operational safety.

In August 2025, Germany’s Aerodata AG unveiled an upgraded automated flight data monitoring system integrating GNSS signal mapping and AI-driven mission planning, designed for both civil and defense calibration fleets.

MARKET CHALLENGES:

Limited Integration of FDM Outputs into Safety to Present Threats in the Market

The key challenges are no longer about collecting data but about effectively using it. Many operators still treat FDM as an isolated safety project, with limited integration into safety risk management, training, or engineering processes. EASA’s EOFDM forum and associated best-practice documents exist precisely as operators struggle to design KPIs, standardize analysis methods, and embed outputs into their safety management systems. There is also a talent shortage: experienced FDM analysts who understand both data science and line operations are in short supply, particularly outside large network carriers. In emerging markets, operators are building FDM capabilities from a low base, guided by ICAO and regional CAA documents on establishing FDAP/FDM programs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Aircraft Type

Aircraft Type Segment Dominates due to the Increase in InvestmentsinAdvanced FDMSystems

Based on aircraft type, the market is classified into fixed wing, rotary wing, and UAVs.

Fixed wing aircraft, particularly the A320 and 737 families, account for the largest flight data monitoring market share. These aircraft operate the highest flight cycles, form the backbone of most airline networks, and are the primary focus of ICAO and national regulations that mandate robust flight data analysis for large transport aircraft. Safety incidents, fuel burn, and turnaround-time gains have the most significant impact on these fleets, making airlines more willing to invest in advanced FDM systems and pilot analytics for narrow-body aircraft first, with wide-body fleets and regional jets typically following.

- In July 2024, Korean Air signed a fleet-wide agreement with GE Aerospace to deploy the Safety Insight FDM system across its fleet, including Korean Air and Jin Air, utilizing data from both narrow-body and wide-body aircraft to enhance safety and efficiency.

The UAVs segment is expected to grow at the highest CAGR of 9.17% from 2026-2034.

By Component

Software & Analytics Segment Is Growing Due To Increasing Requirement To Transform Raw Data Into Actionable Insights

In terms of component, the market is categorized into hardware, software & analytics, and services.

Software & analytics holds the largest share in the FDM market as the true value of flight data lies in transforming raw data into actionable insights. Airlines pay recurring fees for FDM platforms, cloud storage, dashboards, pilot apps, and data-science tools that support safety, fuel, and maintenance actions.

Hardware, such as QARs or modems, is purchased infrequently and tends to be commoditized, whereas analytics capabilities are continuously upgraded and scaled across fleets and crews. As more use cases, such as fuel optimization, predictive maintenance, and turbulence analytics, are layered on the same data streams, spending naturally concentrates on software.

- In October 2025, GE Aerospace confirmed its FlightPulse analytics app exceeded 60,000 commercial pilot users, with 42 airlines paying per-pilot subscriptions for data-driven safety and fuel-efficiency insights.

By End-User

Commercial Passenger Airlines Segment Dominates Due To Rising Customer Trust Pressures

Based on end-user, the market is segmented into commercial passenger airlines, cargo airlines & logistics operators, business aviation operators, helicopter operators, military and government operators, and UAV/drone operators.

Commercial passenger airlines are the largest end-user segment in the market, as they operate under the largest safety, regulatory, and customer trust pressures. FDM is embedded into their safety management systems and linked to key performance indicators for fuel efficiency, scheduling, and maintenance, KPIs, leading airlines to dedicate teams and budgets specifically to these programs. Cargo, business aviation, helicopter, and UAV operators are increasingly adopting FDM; the scale and intensity of operations remain concentrated with passenger carriers, especially network airlines and large LCCs. As these airlines digitize operations, FDM becomes a key input to broader operations-control and performance-management programs.

- In September 2025, the Air India Group deployed SITA’s OptiFlight and eWAS solutions across its fleet to optimize climb profiles and manage weather risk, explicitly positioning flight-data-driven analytics at the heart of its airline transformation.

To know how our report can help streamline your business, Speak to Analyst

By Application

Safety & Risk Management Segment Dominates Due To Early Detection of Unstable Approaches

Based on application, the market is segmented into safety & risk management, regulatory compliance & reporting, operational efficiency, maintenance & reliability analytics, and training & crew performance.

The safety & risk management segment captures the largest share of the FDM market. Regulators, IATA, and safety bodies regard systematic analysis of flight data as one of the most effective tools to reduce accidents, so airlines continue to justify FDM investments primarily on safety grounds with operational benefits layered on top. FDM supports the early detection of unstable approaches, runway excursions, turbulence exposure, and SOP drift, providing targeted interventions that inform training and procedures. With accident rates still closely scrutinized, particularly at the regional level, airline boards are unlikely to reduce funding for data-driven safety, even during economic downturns.

- In February 2025, IATA’s 2024 Annual Safety Report highlighted that industry safety remains strong, but uneven by region, emphasizing the continued importance of structured safety data and analysis to address issues such as runway events and turbulence.

By Deployment

Cloud Segment Is Growing Due To Growing Technological Innovations In The Flight Data Monitoring Market

Based on deployment, the market is segmented into on-premise, cloud, and hybrid.

The cloud segment accounted for a dominating market share in 2025 and has become the most prevalent deployment model for FDM as airlines shift away from bespoke, on-premises infrastructures. Cloud and SaaS platforms lower upfront cost, easier scaling across fleets and stations, and faster access to new analytics features. They also simplify collaboration between safety, operations, and fuel-efficiency teams by ensuring everyone can access the same dashboards and APIs. While some sensitive or defense-related operations still prefer hybrid or on-premise setups, most new civilian projects, and the majority of contract renewals, are now cloud-first, especially where pilot-facing apps are part of the solution.

- In September 2024, Emirates reported that pilots on all 470 daily flights now use GE’s cloud-delivered FlightPulse app to access safety and fuel-efficiency insights, citing “remarkable improvements” in key KPIs.

Flight Data Monitoring Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America held the dominant share in 2024, valued at USD 1.16 billion, and also took the leading share in 2025 with USD 1.21 billion. The region remains the global leader, anchored by the U.S. airline system. Major carriers have run FOQA and FDM programs for decades under FAA guidance and actively participate in voluntary data-sharing initiatives. FDM data is deeply embedded across safety, training, and fuel-saving programs, with particularly strong adoption of pilot-level analytics.

- In October 2025, Reuters reported that GE’s FlightPulse app had grown to over 60,000 pilot users across 42 airlines, including Qantas, Delta, and NetJets. GE targeted 100,000 pilots by 2026, underscoring strong traction in North America and other mature markets.

North America Flight Data Monitoring Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe is the second-largest FDM region, distinguished by strong regulatory expectations and a strong culture of safety collaborations. EASA and the European Operators Flight Data Monitoring (EOFDM) Forum promote FDM as a core part of safety management and publish guidance on analysis techniques and integration with training and risk management. European airlines run mature, multi-use FDM programs that combine safety, fuel, and maintenance analytics, reinforced by active cross-industry collaboration through EOFDM working groups.

The Asia Pacific region is experiencing rapid growth and is expected to grow at the highest CAGR by 2032 in the flight data monitoring market. Rapid traffic growth in air traffic, large narrow-body orders, and several high-visibility safety incidents have increased regulatory scrutiny, prompting airlines to accelerate FDM adoption and upgrade to more advanced analytics. Flag carriers and large LCCs are now investing in group-wide platforms that cover safety, fuel, and predictive maintenance for mixed fleets. Emerging markets in the region view FDM as a key enabler of improved safety culture and IOSA standards.

The Middle East and Africa are characterized by a small number of hub carriers that account for a significant portion of FDM spending. Their long-haul networks, high aircraft utilization, and premium brand positioning make data-driven safety and fuel efficiency, operational efficiency, central to their strategic priorities.

Latin America represents a smaller but steadily growing FDM market. Airlines in the region operate under tight cost constraints, volatile currencies, and challenging operational environments, prompting them to adopt FDM solutions for safety assurance and operational-efficiency gains.

COMPETITIVE LANDSCAPE

Key Players:

Key Players are Adopting Cloud-Based Analytics to Support Airlines' Integration Capabilities

The flight data monitoring market is moderately concentrated, comprising a mix of large avionics/OEM players and specialized analytics providers. Major vendors include GE Aerospace (Safety Insight, FlightPulse), Honeywell, L3Harris, Safran, Teledyne Controls, Collins Aerospace, SITA, NAVBLUE/Airbus, along with niche specialists such as Scaled Analytics and various regional HFDM providers. Competition is shifting from pure data acquisition to cloud-based analytics, pilot apps, and integrated safety, fuel, and maintenance platforms, favoring players with strong software roadmaps and airline integration capabilities.

Partnerships between airlines, OEMs, and IT firms are becoming common, as carriers want end-to-end solutions rather than point tools. In 2024–2025, high-profile wins, such as Korean Air choosing GE’s Safety Insight and the Air India Group selecting SITA’s OptiFlight/eWAS suite, underscore how Tier-1 airlines are consolidating around a small set of strategic FDM analytics partners, raising the bar for smaller competitors.

LIST OF KEY Flight Data Monitoring COMPANIES PROFILED:

- GE Aerospace (U.S.)

- Honeywell Aerospace (U.S.)

- Collins Aerospace (U.S.)

- Safran Electronics & Defense (France)

- L3Harris Technologies (U.S.)

- Teledyne Controls (U.S.)

- SITA (Switzerland)

- NAVBLUE (an Airbus company) (France)

- Boeing Global Services (U.S.)

- Scaled Analytics (Canada)

KEY INDUSTRY DEVELOPMENTS:

- March 2024: The EASA launched NPA 2024-02 to amend EU air operations rules and strengthen flight data monitoring requirements, aiming to improve FDM implementation and integration with safety risk management. This regulatory push is expected to drive additional FDM investments across European airlines and operators.

- July 2024: Korean Air partnered with GE Aerospace to deploy the Safety Insight flight data monitoring system across Korean Air and Jin Air. The deal would modernize group-wide FDM, boost safety analytics, and support predictive maintenance, and is expected to become a flagship Asian reference.

- July 2024: Riyadh Air signed a five-year agreement with GE Aerospace to launch Safety Insight, Fuel Insight, and FlightPulse as its core digital flight operations stack, positioning the start-up carrier as a “digital native” airline. The program would shape its safety and fuel efficiency performance from day one.

- September 2024: Emirates deepened its collaboration with GE by rolling out the FlightPulse pilot app on all ~470 daily flights, providing every pilot with personalized safety and fuel-efficiency data. The initiative aims to reduce fuel burn and emissions while improving key safety KPIs.

- September 2025: Air India Group partnered with SITA to deploy OptiFlight and eWAS across Air India and Air India Express fleets, using advanced climb and weather analytics on flight data to reduce around 11,100 tons of fuel and 35,000 tons of CO₂ annually.

- November 2025: Ethiopian Airlines partnered with Safran Electronics & Defense to roll out the Cassiopée Alpha flight-data analysis platform across its 147-aircraft fleet, including A350, 787, and 737 MAX; the project will centralise safety and operational analytics for Africa’s largest carrier.

- In December 2025, SKYTRAC announced a new partnership with Embraer’s Services & Support division to integrate SKYTRAC’s next-generation flight data monitoring suite into Embraer’s aftermarket digital ecosystem. The collaboration will provide regional jet and turboprop operators with real-time safety alerts, automated FOQA reporting, and cloud-based analytics, accelerating the adoption of proactive safety management across global fleets.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Attribute |

Details |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.87% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Aircraft Type, Component, End-User, Application, Deployment, and Region |

|

By Aircraft Type |

Fixed Wing

|

|

By Component |

|

|

By End-User |

|

|

By Application |

|

|

By Deployment |

|

|

By Geography |

North America (By Aircraft Type, Component, End-User, Application, Deployment, and Country)

Europe (By Aircraft Type, Component, Aircraft Type, Application, Deployment, and Country)

Asia Pacific (By Aircraft Type, Component, Aircraft Type, Application, Deployment, and Country)

Rest of the World (By Aircraft Type, Component, Aircraft Type, Application, Deployment, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.06 billion in 2025 and is projected to reach USD 5.56 billion by 2034.

In 2025, the market value stood at USD 1.21 billion.

The market is expected to exhibit a CAGR of 6.87% during the forecast period (2025-2032).

The fixed wing segment leads the market in terms of aircraft type.

Regulatory pressure and the rising need for maintaining formal flight data analysis are the key factors driving market growth.

GE Aerospace (U.S.), Honeywell Aerospace (U.S.), and Collins Aerospace (U.S.) are prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us