Flight Inspection Market Size, Share & Industry Analysis, By Aircraft Type (Fixed Wing Aircraft (Narrow-Body, Wide Body, Business Jets, Regional Jets, and Military Jets) and Rotary Wing Aircraft (Military Helicopters and Commercial Helicopters)), By Solution Type(System and Service), By Application (Civil & Commercial and Military), By Inspection Type (Routine Inspection, Commissioning Inspection, and Special Inspection), By End User (Airport Operators, Air Navigation Service Providers (ANSPs), Defense Authorities, and Flight Inspection Service Providers), and Regional Forecast, 2025-2032

KEY MARKET INSIGHTS

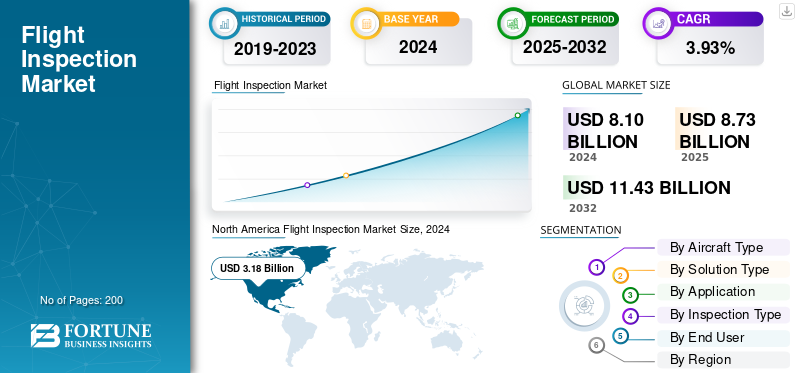

The global flight inspection market size was valued at USD 8.10 billion in 2024. The market is projected to grow from USD 8.73 billion in 2025 to USD 11.43 billion by 2032, exhibiting a CAGR of 3.93% during the forecast period. North America dominated the flight inspection market with a market share of 39.26% in 2024.

The flight inspection market refers to the specialized segment of aviation services and systems dedicated to ensuring the accuracy, reliability, and safety of air navigation aids and procedures. These operations involve the calibration and validation of ground-based navigation systems such as ILS, VOR, DME, and satellite-based aids including GNSS, guaranteeing compliance with ICAO and national aviation industry authority standards. Flight inspection industry is a critical pillar in airspace management, as even minor deviations in navigational signals can affect approach precision and overall flight safety.

The industry is highly specialized, with a handful of key players serving as the backbone of both equipment supply and inspection services. Leading system manufacturers include Safran Electronics & Defense (France), Textron Aviation (U.S.), Cobham Limited (U.K.), and MST Group GmbH (Germany), which develop integrated flight inspection systems and aircraft. On the service front, major providers such as Flight Calibration Services Ltd. (U.K.), Bombardier Specialized Aircraft (Canada), Aerodata AG (Germany), and ENAV (Italy) perform inspection operations across multiple countries under regulatory contracts. The competitive focus is increasingly shifting toward data-driven calibration analytics, autonomous inspection platforms, and multi-mission aircraft integration, positioning the market for sustained growth as global aviation infrastructure becomes more technologically intensive and regulated.

Download Free sample to learn more about this report.

Global Flight Inspection Market Key Takeaways

Market Size & Forecast:

- 2024 Market Size: USD 8.10 billion

- 2025 Market Size: USD 8.73 billion

- 2032 Forecast Market Size: USD 11.43 billion

- CAGR: 3.93% from 2025–2032

Market Share:

- Europe has strengthened its position in the global flight inspection market following the Russia–Ukraine conflict, driven by airspace reconfiguration, increased inspection frequency along alternative flight corridors, and heightened defense–civil aviation coordination across NATO-aligned countries.

- North America continues to hold a significant share, supported by FAA-led modernization programs and defense-backed GNSS validation initiatives. Asia Pacific is expected to grow at the fastest pace, fueled by rapid airport expansion, GNSS adoption, and rising air traffic in China, India, and Southeast Asia.

- By solution type, the service segment dominates the market, as aviation authorities increasingly outsource inspection operations to specialized providers to manage high operational costs, regulatory complexity, and dynamic airspace conditions intensified by geopolitical instability.

Key Country Highlights:

- United States: The FAA’s NextGen program and defense-driven airspace resilience initiatives are accelerating demand for advanced GNSS-based and automated flight inspection systems, particularly for transatlantic and rerouted air corridors.

- Europe: Growth is supported by EASA-led standardization under the Single European Sky (SESAR) initiative and increased inspection activity near Eastern European borders following the Russia–Ukraine conflict, ensuring navigation reliability and airspace security.

- Russia: The market has become more domestically oriented due to sanctions and restricted cross-border operations, with reliance on state-controlled inspection fleets and locally supported navigation systems.

- China: Continued airport expansion, airspace modernization, and investment in GNSS infrastructure are sustaining strong demand for flight inspection services, positioning China as a key growth driver in Asia Pacific.

MARKET DYNAMICS

MARKET DRIVERS

Airspace Modernization and Airport Expansion Leading to Market Growth

The primary driver of the flight inspection market growth is the continuous modernization of global airspace and the commissioning of new airports. Aviation authorities are transitioning from conventional navigation aids to satellite-based and performance-based navigation (PBN) systems, which require regular flight inspection to ensure signal precision and safety ensure compliance. The proliferation of commercial air traffic and investments in next-generation navigation systems have significantly increased demand for both commissioning and routine inspection services. Emerging economies, particularly across Asia Pacific and the Middle East, are witnessing rapid airport construction, necessitating extensive calibration and validation cycles.

- In April 2025, India’s Airports Authority (AAI) commissioned new GNSS-based flight inspection systems across six regional airports, enhancing precision navigation and compliance with ICAO standards for next-generation operations.

MARKET RESTRAINTS

High Operational Cost and Limited Skilled Workforce to Act as a Restraint for Growth

One of the major restraints in the flight inspection market is the high operational and maintenance cost of specialized aircraft, onboard systems, and calibration equipment. Flight inspection operations demand highly skilled pilots, engineers, and technicians certified by aviation regulators, which significantly increases cost barriers for new service entrants. Additionally, the aging fleet of inspection aircraft in several countries limits operational flexibility and incurs high lifecycle expenses. Developing nations often rely on outsourced inspection services due to the financial and technical burden of maintaining in-house capabilities.

In February 2025, Nigeria’s Civil Aviation Authority announced a temporary delay in routine flight inspections at regional airports due to shortages of certified inspection aircraft and qualified calibration specialists.

MARKET OPPORTUNITIES

Integration of UAVs and Digital Inspection Technologies Posing As Major Market Opportunity

The integration of unmanned aerial vehicles (UAVs), AI-based analytics, and digital calibration tools presents a strong opportunity for market expansion. UAV-based inspection can drastically reduce operational costs, turnaround time, and airspace disruption while enabling precise real time data collection at lower altitudes. With the ongoing digital transformation of aviation infrastructure, combining autonomous systems with real-time analytics and cloud platforms is enhancing efficiency and predictability in calibration processes. Several countries are exploring hybrid models where UAVs complement conventional aircraft for localized navigation checks, offering scalability and cost benefits.

- In June 2025, Japan’s Civil Aviation Bureau successfully tested UAV-based flight inspection for short-range navigation aids, marking one of the first operational validations of autonomous calibration technology in the Asia Pacific region.

FLIGHT INSPECTION MARKET TRENDS

Shift Toward GNSS-Based and Automated Inspection Systems Pose As a Technological Trend

The most prominent technological trend in the flight inspection market is the transition toward GNSS-based navigation validation and automated flight profiles. These systems enable higher accuracy in navigation aid calibration while minimizing human error and mission duration. Advanced data logging, AI-assisted route planning, and real-time signal integrity assessment tools are transforming flight inspection efficiency. The adoption of dual-use inspection aircraft capable of handling both conventional and satellite-based systems is increasing among ANSPs and defense operators. Automation is also extending into mission management, improving repeatability and operational safety.

In August 2025, Germany’s Aerodata AG unveiled an upgraded automated flight inspection system integrating GNSS signal mapping and AI-driven mission planning, designed for both civil and defense calibration fleets.

MARKET CHALLENGES

Regulatory Complexity and Airspace Access Restrictions Present Threats to Market Growth

Regulatory hurdles and restricted airspace access remain key challenges for the global flight inspection market. Conducting inspection flights often requires multi-agency coordination, special flight permits, and adherence to stringent national aviation authority protocols. Differences in calibration standards between ICAO-compliant and region-specific regulations complicate cross-border operations. Additionally, defense-controlled or congested airspaces limit flight inspection scheduling, particularly in emerging regions where procedural harmonization is still evolving. Addressing these challenges demands close collaboration between regulatory bodies, service providers, and manufacturers to ensure interoperability and safety.

- In March 2025, The European Union Aviation Safety Agency (EASA) introduced new guidelines harmonizing flight inspection requirements across member states to streamline cross-border calibration operations and reduce mission delays.

Download Free sample to learn more about this report.

Segmentation Analysis

By Solution Type

Service Segment is Growing Due to Expanding Outsourced Inspection Contracts

On the basis of solution type, the market is classified into system and service.

The service segment dominates and continues to expand due to the rising number of outsourced inspection programs managed by civil and defense aviation authorities. Airports and ANSPs increasingly rely on specialized service providers for routine, commissioning, and calibration missions rather than maintaining costly in-house fleets. Growth is supported by aviation modernization projects, digital data management, and multi-year contracts that ensure operational continuity. Emerging economies are also adopting service-based inspection models to align with ICAO compliance standards without heavy capital investment in aircraft and systems.

- In April 2025, The UAE’s General Civil Aviation Authority awarded Safran Electronics & Defense a USD 70 Billion, five-year service contract to manage nationwide calibration of navigation aids and GNSS systems across 12 airports. The agreement includes provisions for automated data analysis and remote mission management, strengthening regional inspection capability.

By End User

Air Navigation Service Providers (ANSPs) Segment Dominate Due to Regulatory Responsibility and Centralized Operations

In terms of end user, the market is categorized into airport operators, Air Navigation Service Providers (ANSPs), defense authorities, and flight inspection service providers.

The Air Navigation Service Providers (ANSPs) segment dominated the market in 2024. The ANSP segment holds the largest share as these organizations bear regulatory accountability for maintaining airspace safety and navigation integrity. With centralized command structures and national coverage, ANSPs invest heavily in inspection modernization and automation. They often collaborate with OEMs and service contractors to implement consistent calibration standards across multiple regions. The trend toward integrated digital mission planning and automated scheduling is driving efficiency, making ANSPs the backbone of global inspection activities.

- In February 2025, NAV CANADA partnered with Aerodata AG to upgrade its entire inspection fleet with next-generation AD-AFIS systems and GNSS validation software. The USD 45 Billion modernization project aims to standardize data collection and reduce calibration cycle times across over 60 airports in Canada.

To know how our report can help streamline your business, Speak to Analyst

By Aircraft Type

Fixed-Wing Aircraft Segment Dominated Due to Long-Range and Multi-Mission Capability

Based on the aircraft type, the market is segmented into fixed wing aircraft and rotary wing aircraft.

Fixed wing aircraft accounted for the largest share in 2024. The fixed wing segment dominates due to its versatility, payload capacity, and superior flight range, making it ideal for national and cross-border calibration missions. These aircraft, particularly narrow-body and regional jets, provide high stability, enabling precise route and approach inspections. Increasing adoption of hybrid configurations that combine analog and digital calibration systems is extending aircraft lifecycle utility. OEMs are now designing multi-role inspection aircraft capable of handling both civil and defense operations, further strengthening the segment’s position.

- In May 2025, Textron Aviation delivered two new Beechcraft King Air 360 CER aircraft equipped with Aerodata’s integrated flight inspection suite to support FAA and NATO missions. The USD 95 Billion deal includes advanced GNSS, ILS, and ADS-B validation systems, expanding transatlantic inspection capacity.

By Application

Civil & Commercial Segment Led Due to Airport Expansion and Navigation Upgrade

Based on the application, the market is segmented into civil & commercial and military.

Civil & commercial segment accounted for the largest share in 2024. The Civil & Commercial segment leads the market owing to large-scale airport modernization, expansion of air routes, and the global shift toward performance-based navigation (PBN). Governments and airport authorities are investing in upgrading ILS, VOR, and GNSS systems, generating sustained demand for commissioning and routine inspections. The rise in private airport management and new route authorizations in Asia and the Middle East are further fueling inspection frequency.

- In January 2025, China’s Civil Aviation Administration launched an ambitious airspace modernization plan worth USD 220 Billion to recalibrate navigation aids across 15 major airports. The initiative includes GNSS-based inspection missions operated jointly with Japan’s JCAB to enhance precision landing capability.

By Inspection Type

Routine Inspection Segment Dominated Due to Regulatory Mandates and Frequency of Operations

Based on the inspection type, the market is segmented into routine inspection, commissioning inspection, and special inspection.

Routine inspections segment accounted for the largest share in 2024. Routine inspections represent the largest share as aviation authorities mandate frequent calibration of navigation aids to maintain safety and precision. Airports with heavy traffic conduct multiple inspections yearly, creating consistent, and high-volume service demand. Automation, data logging, and predictive maintenance systems are improving inspection efficiency, encouraging continuous investment by ANSPs and service providers.

- In March 2025, France’s DGAC completed over 1,200 routine inspection missions under its 2024 national program, covering ILS, VOR, and GBAS systems across 70 airports. The agency announced a 15% increase in annual inspection frequency following EASA’s updated navigation accuracy directives.

Flight Inspection Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

NORTH AMERICA

North America Flight Inspection Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant flight inspection market share in 2023, valued at USD 2.95 billion, and also took the leading share in 2024 with USD 3.18 billion. North America leads globally owing to robust FAA and Transport Canada frameworks, extensive airport networks, and early adoption of automated inspection systems. The region’s focus on GNSS-based calibration and digital data reporting under NextGen initiatives strengthens its market presence. Investment in specialized fleets ensures consistent operational coverage across thousands of navigation aids. The U.S. market is growing due to strong aircraft production rates, expanding MRO capacity, and continuous investment in next-generation aviation coatings that meet stringent FAA and sustainability standards.

- In June 2025, The FAA awarded a USD 120 Billion modernization contract to Bombardier Specialized Aircraft for its flight inspection fleet. The project integrates digital mission control, GNSS signal validation, and automated data transfer, enabling real-time compliance monitoring across all U.S. airports.

EUROPE

Europe’s flight inspection growth is driven by EASA-led standardization under the Single European Sky (SESAR) initiative. High-density airspace, cross-border flight corridors, and technological harmonization among EU states necessitate frequent calibration missions. National service providers increasingly share data through integrated platforms to improve operational efficiency and safety consistency.

ASIA PACIFIC

The Asia Pacific region is experiencing rapid growth and is expected to grow at the highest CAGR by 2032 in Flight Inspection market. Asia Pacific is the fastest-growing region, propelled by rapid airport expansion, new route authorizations, and airspace modernization in China, India, and Southeast Asia. Governments are investing heavily in GNSS infrastructure, while domestic service providers expand fleet capability through partnerships with Western OEMs. Rising passenger volumes and regional connectivity initiatives sustain inspection frequency.

REST OF THE WORLD

The Middle East & Africa region is expanding its flight inspection capacity due to ambitious infrastructure projects and increasing air traffic. Gulf nations are commissioning new airports, while African countries modernize outdated systems with international support. Latin America’s growth is steady, supported by airport modernization and new compliance mandates from ICAO. Countries including Brazil, Mexico, and Colombia are overhauling navigation aids and expanding regional air connectivity, leading to an increase in inspection operations. Public-private collaborations are emerging to reduce dependency on foreign fleets.

COMPETITIVE LANDSCAPE

Key Industry Players

A Wide Range of Product Offerings, coupled with a Strong Distribution Network of Key Companies, Supported their Leading Position

The competitive landscape of the aircraft batteries market is characterized by a mix of established aerospace power solution providers and emerging battery technology innovators. Key players such as Saft Groupe S.A. (France), GS Yuasa Corporation (Japan), EaglePicher Technologies (U.S.), Concorde Battery Corporation (U.S.), and TELEDYNE Technologies (U.S.) dominate through extensive OEM partnerships and certified battery systems for both civil and military platforms. These companies are focusing on high-energy-density lithium-ion solutions, improved lifecycle performance, and compliance with aviation safety standards such as RTCA DO-311A and EASA CS-25. Strategic collaborations with aircraft manufacturers including Boeing, Airbus, and Embraer are driving integration of advanced energy storage systems in next-generation aircraft. Meanwhile, niche firms and startups are entering the segment with solid-state and hybrid chemistries, aiming to enhance power-to-weight ratios. Continuous innovation, safety certification, and energy management optimization remain the primary competitive differentiators shaping market leadership.

LIST OF KEY FLIGHT INSPECTION COMPANIES PROFILED

- Saft Groupe S.A. (France)

- GS Yuasa Corporation (Japan)

- EaglePicher Technologies (U.S.)

- Concorde Battery Corporation (U.S.)

- Teledyne Technologies Incorporated (U.S.)

- MarathonNorco Aerospace (U.S.)

- Enersys Inc. (U.S.)

- Kokam Co., Ltd. (South Korea)

- Sichuan Changhong Battery Co., Ltd. (China)

- Tadiran Batteries GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2025 – AkzoNobel partnered with LandLocked Aviation Services to repaint a USAF JSTAR aircraft for a local technical college, signalling increased OEM/MRO collaboration and niche military repaint demand.

- May 2025 – PPG Industries secured a multi-year contract to supply exterior and interior coatings for the Airbus A320neo family, reinforcing its role in the commercial-fleet paint supply chain.

- June 2025 – Qatar Airways signed a deal with Satys Aerospace and Barzan Holdings to establish a wide-body aircraft painting facility in the Middle East, aimed at reducing ground-time and servicing commercial, VIP and military aircraft.

- July 2025 – Ryanair extended its long-term repainting deal with MAAS Aviation for up to 500 aircraft over ten years at Maastricht and Kaunas facilities, supporting its fleet growth and brand-standard consistency.

- August 2025 – International Aerospace Coatings (IAC) announced expansion of its painting presence at Teruel, Spain, adding a new wide-body hangar adjacent to its existing facility to meet rising demand for large-aircraft paint services.

- August 2025 – Airbourne Colours revealed that its second aircraft-paint hangar at Teesside Airport is nearing completion (USD 16.45 Billion investment) to cope with Europe’s backlog in aircraft painting capacity.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 3.93% from 2025-2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Aircraft Type, Solution, Application, Inspection Type, End User, and Region |

|

By Aircraft Type |

· Fixed Wing Aircraft o Narrow-Body o Wide Body o Business Jets o Regional jets o Military Jets · Rotary Wing Aircraft o Military helicopters o Commercial Helicopters |

|

By Solution Type |

· System · Service |

|

By End User |

· Airport Operators · Air Navigation Service Providers (ANSPs) · Defense Authorities · Flight Inspection Service Providers |

|

By Application |

· Civil & Commercial · Military |

|

By Inspection Type |

· Routine Inspection · Commissioning Inspection · Special Inspection |

|

By Region |

· North America (By Aircraft Type, Solution, Application, Inspection Type, End User, and Country) o U.S. (By Aircraft Type) o Canada (By Aircraft Type) · Europe (By Aircraft Type, Solution, Application, Inspection Type, End User, and Country) o U.K. (By Aircraft Type) o Germany (By Aircraft Type) o France (By Aircraft Type) o Russia (By Aircraft Type) o Rest of Europe (By Aircraft Type) · Asia Pacific (By Aircraft Type, Solution, Application, Inspection Type, End User, and Country) o China (By Aircraft Type) o India (By Aircraft Type) o Japan (By Aircraft Type) o Australia (By Aircraft Type) o Rest of Asia Pacific (By Aircraft Type) · Rest of the World (By Aircraft Type, Solution, Application, Inspection Type, End User, and Country) o Latin America (By Aircraft Type) o Middle East & Africa (By Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.10 Billion in 2024 and is projected to reach USD 11.43 Billion by 2032.

In 2024, the market value stood at USD 3.18 Billion.

The market is expected to exhibit a CAGR of 3.93% during the forecast period of 2025-2032.

The fixed wing segment led the market in terms of aircraft type.

Airspace Modernization and Airport Expansion are leading to market growth.

Saft Groupe S.A., GS Yuasa Corporation, and Teledyne Technologies Incorporated are some of the prominent players in the market.

North America dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us