Aircraft Battery Market Size, Share & Industry Analysis, By Aircraft Type (Fixed-Wing, (Narrow Body, Wide Body, Regional Jets, Business Jets, and Military Aircraft) Rotary-wing, (Military helicopters and Commercial Helicopters) and UAVs (Commercial UAV and Military UAV)), By Battery Type (Solid Battery, Lithium-ion, Nickel-Cadmium, and Lead-acid), By Application (Propulsion, Start & Backup, Avionics and Cabin, and Others), By End-Users (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

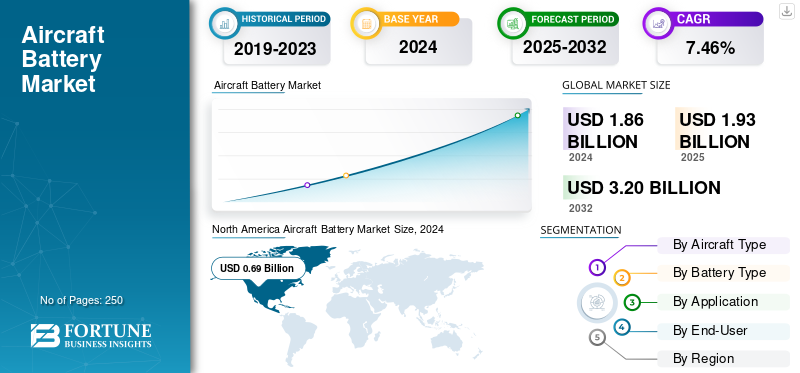

The global aircraft battery market size was valued at USD 1.86 billion in 2024. The market is projected to grow from USD 1.93 billion in 2025 to USD 3.20 billion by 2032, exhibiting a CAGR (compound annual growth rate) of 7.46% during the forecast period. North America dominated the aircraft battery market with a market share of 37.09% in 2024.

Aircraft batteries are onboard power sources that help start engines and APUs, keep avionics and lights running, and provide emergency power if generators fail. They come in four main types: solid-state (emerging), lithium-ion, nickel-cadmium, and lead-acid. New electric aircraft also use large battery cell packs for propulsion as they meet strict safety standards.

More-electric aircraft (MEA) architectures increase battery counts and capacity per tail (including electro-hydraulic brakes, distributed actuators, and power electronics). AAM/eVTOL and defense–commercial UAV fleets shift batteries from auxiliary to mission-critical, driving higher energy and power requirements. Li-ion retrofits improve weight, maintenance, and dispatch reliability while enabling health-monitoring and eTechLog integration. Clearer certification (e.g., DO-311A thermal-runaway containment and DO-160 environmental testing) plus better BMS and thermal design have de-risked adoption after early incidents. Replacement cycles create recurring spend, while growth of the Asia Pacific fleet and missionization in the defense sector contribute to increased volume. Sustainability targets, recycling mandates, and airport electrification further reinforce investment in advanced chemistries and safer pack architectures.

Leaders include Saft, GS Yuasa, Concorde, Teledyne Gill, MarathonNorco, EnerSys/Hawker, True Blue Power, Safran Electrical & Power, Parker Meggitt/Securaplane, Collins, EaglePicher, and electrification specialists EPS, H55, Amprius, Molicel, CUSTOMCELLS, Denchi. They pair certification with BMS/thermal safety, cycle life, field support and tight alignment to eVTOL/Unmanned Aerial Vehicles (UAV) and retrofit roadmaps.

Download Free sample to learn more about this report.

Aircraft Battery Market KEY TAKEAWAYS

- 2024 Market Size: USD 1.86 Billion

- 2025 Market Size: USD 1.93 Billion

- 2032 Forecast Market Size: USD 3.20 Billion

- CAGR: 7.46% from 2025–2032

- North America dominated the aircraft battery market with a 37.09% share in 2024.

- The lithium-ion batteries segment holds the largest market share.

- The OEM segment accounts for a significant market share.

North America

North America generated USD 0.69 billion in 2024, driven by aviation fleet expansion and electrification adoption.

Europe

Europe is growing strongly, driven by aircraft battery investments and lithium-ion adoption.

Asia Pacific

Asia Pacific is expected to grow fastest, driven by air travel growth, fleet expansion, and eVTOL development.

U.S.

Electric aircraft adoption, eVTOL programs, UAV deployment, and battery advancements are driving market growth.

Japan

Aviation expansion, fleet modernization, and electrification investments are supporting aircraft battery demand.

Read More

MARKET DYNAMICS

MARKET DRIVERS

More-Electric Aircraft, AAM Ramp, and Higher Battery Content per Tail to Drive Market Growth

Airframers are switching from hydraulics power to electric power (for brakes, actuators, and power electronics), and this shift increases both the number and capacity of batteries per aircraft. At the same time, advanced air mobility (eVTOL/eCTOL) moves batteries from “auxiliary” to “propulsion-critical,” multiplying value per tail and accelerating investment in high-voltage packs, robust BMS, and thermal containment. As regulatory paths clarify, airline and airport pilots integrate certified solutions into the mainstream, while OEM roadmaps standardize interfaces and health-monitoring hooks. The feedback loop for airframes is powerful due to more electric loads, which leads to larger and more complex batteries and propulsion systems, ultimately resulting in stricter safety specifications that cater to business aviation, regional, and rotorcraft operations, thereby driving overall market development.

- January 2025: The FAA finalized rules to integrate powered-lift into operations and pilot certification—an enabling step for eVTOL entry-into-service.

MARKET RESTRAINTS

Tighter Thermal Safety, Handling, and Ops Burden to Constrain the Market for Aircraft Batteries

Lithium-ion’s energy density is compelling but aviation demands impeccable design: cell selection, propagation-resistant structures, controlled vent paths, heaters, and fault-tolerant BMS logic. Operators also carry procedural loads, including carriage limits for spares, cabin crew training, and standardized fire-containment gear, as well as the documentation to display compliance with abuse tests. Mixed fleets and extreme-temperature ops magnify the burden, stretching qualification timelines and adding cost. Even with safer chemistries, airlines still factor in containment hardware and ground-handling controls, slowing adoption in segments where weight savings are marginal. Real-world events keep risk in focus and drive conservative engineering margins.

- October 2025: An Air China A321 diverted after a carry-on lithium battery ignited mid-flight, underscoring persistent thermal-runaway risks and the need for containment and procedures.

MARKET OPPORTUNITIES

Growth Opportunities through UAV Proliferation and Defense Missionization

Unscrewed systems are scaling in number, mission diversity, and sortie rates. This creates the demand for hot-swappable, rapid-charge packs that handle high C-rates, wide temperatures, and repeated abuse while remaining signature-quiet. Defense programs, in particular, are funding the development of ruggedized enclosures, advanced state-of-health analytics, and standardized interfaces across various families. These are the features that lift battery ASPs. Commercial inspection, logistics, and mapping fleets pull similar capabilities but with tighter cost-per-flight-hour targets, creating volume for cell makers and integrators. Furthermore, UAV learning curves in thermal management and BMS propagate quickly into manned retrofits, shortening the time-to-certification for next-gen packs.

- October 2025: A Washington Post investigation documented the surging Chinese exports of lithium-ion batteries and other components feeding Russia’s battlefield drones, highlighting how the UAV demand is expanding battery volumes and tech deployment.

AIRCRAFT BATTERY MARKET TRENDS

High-Voltage Modular Packs to Act as a Major Technological Trend

Across manned and unmanned platforms, architectures are marching to higher voltages with tighter thermal envelopes and BMS that fuse cell diagnostics with flight data to predict remaining useful life. Suppliers are hardening packs against propagation using mechanical isolation, gas management, and materials that tolerate abuse without catastrophic failure. In parallel, IP is consolidating around HV systems, BMS, and electric-propulsion system integration, speeding certification by reusing proven design blocks.

- October 2025: Archer acquired ~300 patents from Lilium covering high-voltage systems, BMS, and ducted-fan e-propulsion, signaling continued consolidation of battery-adjacent IP in aviation.

MARKET CHALLENGES

Fragmented Certification Present Threats to the Market Growth

Only a subset of chemistries, formats, and vendors meet flight-critical reliability along with temperature/abuse requirements. Qualifying alternates is a slow process. Pack integrators must reconcile evolving FAA/EASA expectations, aircraft-specific installation nuances, and evidence for containment and fault tolerance, each of which adds test cycles, documentation, and cost. Downstream operators seek closed-loop recycling and traceability, which complicates procurement but improves lifecycle outcomes. Geopolitics and export controls can pinch separators, electrolytes, heaters, and sensors, stretching lead times. Winners pre-qualify multiple cell sources, design for manufacturability, and standardize interfaces to de-risk change.

July 2025: EASA issued new Acceptable Means of Compliance/Guidance Material for Innovative Air Mobility (Part-IAM), raising clarity but also increasing the evidentiary bar for operations with VTOL-capable aircraft.

Download Free sample to learn more about this report.

Segmentation Analysis

By Battery Type

Dominance of Lithium-ion Batteries Driven by Energy Density and Efficiency

On the basis of battery type, the market is classified into solid batteries, lithium-ion, nickel-cadmium, and lead-acid.

The lithium ion batteries segment holds the largest aircraft battery market share, owing to their superior energy density, lightweight design, and faster recharge cycles. Their adaptability across propulsion, backup, and auxiliary systems has made them the preferred choice for modern electric and hybrid aircraft. Continuous advancements in thermal management and power-to-weight ratio further strengthen their use in next-generation platforms. Additionally, OEMs are phasing out legacy chemistries due to maintenance and weight limitations.

- August 2025: Airbus announced the successful flight testing of lithium-ion-powered hybrid aircraft demonstrators under its ZEROe program, reinforcing the technology’s leadership in aerospace electrification.

The solid batteries segment is likely to register a significant CAGR of 8.49% during the forecast period.

By End-User

OEM Segment Leads with Integration of Advanced Power Systems

In terms of end-user, the market is categorized into OEM and aftermarket.

The OEM segment accounts for a significant market share, due to the increasing installation of advanced battery systems in new-generation aircraft during the production process. Manufacturers are integrating batteries with intelligent power management units and condition monitoring systems to enhance operational safety and lifecycle efficiency. The rising demand for electric and hybrid propulsion aircraft has driven OEMs to collaborate with specialized energy system suppliers. The aftermarket segment, although growing, remains secondary due to replacement cycles and certification complexity.

- In 2024, Lufthansa Technik expanded trials of UV-C cabin disinfection systems, highlighting the aircraft battery industry toward advanced cleaning technologies. This evolution underscores how regulatory pressure, sustainability, and passenger expectations are reshaping the cleaning process segmentation.

The aftermarket segment is projected to depict a considerable CAGR of 7.35% during the forecast period.

By Application

Mandatory Need in Certification Catering to Aircraft Leads to High Demand for Start & Backup Segment

Based on application, the market is segmented into propulsion, start & backup, avionics and cabin, and others.

The start & backup segment held a dominating position in 2024, with a share of over 45%. The segment is expanding due to increased electrification of c and the need for onboard power redundancy. Modern aircraft are utilizing more-electric architectures, relying on lithium-ion and nickel-cadmium batteries for engine starting and auxiliary power, offering higher energy density and quicker recharge times. The rise in business jet production, and combined with regulatory demands for safety and fail-safe systems, further drives the need for compact, high-performance batteries in this sector.

- October 2025: Saft’s AirLion cleared a key DO-311A thermal-runaway containment test for 28-V start/backup use.

To know how our report can help streamline your business, Speak to Analyst

The others segment is expected to grow at the highest CAGR of 8.97% from 2025-2032.

By Aircraft Type

Increasing Air Travel Demand Fuels Growth in the Fixed-Wing Segment

Based on aircraft type, the market is segmented into fixed-wing, rotary wing, and UAVs.

The fixed-wing segment held the dominating position in 2024 with more than 60% share. Narrow-bodies (A320/737 families) dominate fixed-wing battery demand due to their large in-service fleets and high utilization, which accelerates the replacement cadence. Weight-saving Li-ion retrofits appeal to carriers on short-haul cycles, while newer airframes expand electric loads (including brakes and actuators), nudging them toward higher capacity. Wide-body aircraft are fewer in number and require slower replacement cycles compared to other fixed-wing aircraft types, such as regional and business jets. These other types of aircraft require faster replacement, thereby fueling demand due to their higher capacity.

- October 2025: Airbus opened a second A320neo line in Tianjin, targeting 75 aircraft per month by 2027, an evidence of sustained narrow-body growth.

The UAVs segment is expected to grow with the highest CAGR of 9.96% from 2025-2032.

Aircraft Battery Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Aircraft Battery Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2023, valued at USD 0.65 billion, and it maintained the top position in 2024 with USD 0.69 billion. The region dominates the global aircraft battery market. North America’s lead rests on a deep airline/bizav fleet, strong MRO networks, and clearer regulatory pathways that accelerate electrification and AAM pilots. Li-ion retrofits are common in bizav/rotorcraft, while eVTOL programs pull high-voltage pack capability and safety cases into the mainstream. Helicopter EMS and public safety also contribute to steady replacement demand.

The U.S. aircraft battery demand is rising as airlines add more electric systems, OEMs advance hybrid-electric and eVTOL programs, and UAV fleets expand. Higher onboard power needs, stricter reliability standards, and rapid-charging/solid-state advances are accelerating adoption. Defense modernization and federal incentives for domestic energy storage manufacturing further boost production and replacements nationwide.

- January 2025: FAA finalized the powered-lift (eVTOL) pilot certification and operations rule, opening the door to commercial services and related battery cert activity.

Europe

Europe is witnessing fast-tracked investments in aircraft battery capabilities. The region’s battery demand benefits from structured certification and a large parapublic helicopter market. Li-ion upgrades focus on weight and maintenance savings, while OEMs emphasize DO-311A alignment and containment. Airports and OEM partners test more-electric subsystems, and rotorcraft orders in EMS/offshore support steady aftermarket pull. In July 2025, EASA issued AMC/GM for Innovative Air Mobility (Part-IAM), clarifying operations for manned VTOL and reinforcing electrification pathways that depend on robust battery compliance.

Asia Pacific

The Asia Pacific aircraft battery industry experiences rapid growth and is expected to grow at the highest CAGR over 2025-2032, driven by expanding air travel, increased domestic and international flights, and fleet expansions in countries such as China, India, and Southeast Asia. Asia Pacific combines scale (China, India, and Japan) with policy-backed low-altitude economies and domestic OEM footprints. China’s commercial eVTOL operations and UAV production lift high-voltage packs and certified backup systems, while regional airlines and bizav fleets expand. Supply-chain proximity for cells also lowers upgrade barriers. For instance, in March 2025, China’s CAAC granted the world’s first eVTOL Air Operator Certificates for EHang EH216-S commercial passenger flights, signaling operational demand for certified battery systems.

Middle East & Africa

The Middle East & Africa region is expected to witness a moderate aircraft battery market growth. The regional market in 2025 is set to record USD 0.19 billion as its valuation. The Middle East & Africa’s battery demand concentrates in rotorcraft for energy, EMS, and government missions, with upgrades favoring reliability in heat and sand. Urban-air-mobility initiatives in the Gulf are catalyzing high-voltage pack readiness, ground handling, and maintenance capabilities. As corridors and vertiports are mapped and certified, battery requirements are locked into procurement.

Latin America

Latin America is a small market, but it remains strategically important as helicopters cover vast geographies for EMS/public service. Brazil anchors eVTOL manufacturing and regulation efforts, which will require certified packs and robust recycling logistics. As city-pair UAM use cases firm up, suppliers co-locate for final assembly and service. For instance, in October 2024, Embraer’s Eve secured a USD 88 million BNDES loan to build its first eVTOL plant in Taubaté, Brazil—cementing the region’s role in future battery demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Product Portfolio and Extensive Distribution Network Drive Market Leadership for Key Players

The market has two types of competitors. Incumbent aerospace suppliers, Saft, Concorde, Teledyne Gill, MarathonNorco, EnerSys/Hawker, GS Yuasa, Safran Electrical & Power, Parker Meggitt/Securaplane, Collins, and EaglePicher anchor the installed base with proven DO-311A/DO-160 compliance, airframer approvals, and global MRO coverage. Their advantages include reliability across hot/cold operations, known maintenance intervals, and established spares logistics. Electrification specialists such as Electric Power Systems (EPiC), H55, and cell providers Amprius, Molicel, and CUSTOMCELLS, as well as UAV-focused Denchi compete on high-voltage architectures, energy density, cycle life, and rapid iteration, typically through OEM partnerships in eVTOL/eCTOL and UAV programs. Customer selection criteria emphasize BMS diagnostics and APIs, thermal-propagation containment, form-factor modularity, and recycling/traceability programs.

- October 2025: Archer purchased ~300 Lilium patents spanning high-voltage systems and battery management, underscoring ongoing consolidation in electrified aviation.

LIST OF KEY AIRCRAFT BATTERY COMPANIES PROFILED

- Saft (TotalEnergies) (France)

- GS Yuasa (Japan)

- Concorde Battery Corporation (U.S.)

- Teledyne Gill Batteries (U.S.)

- MarathonNorco Aerospace (U.S.)

- EnerSys (Hawker) (U.S.)

- True Blue Power (Mid-Continent) (U.S.)

- Safran Electrical & Power (France)

- Parker Meggitt (U.K.)

- EaglePicher Technologies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025 — Archer Aviation acquired ~300 Lilium patents for USD 21 million, covering high-voltage systems, battery management, and e-propulsion, consolidating AAM’s IP and strengthening Archer’s battery technology position for commercialization.

- October 2025 — Saft’s AirLion™ battery passed the DO-311A thermal-runaway containment test, a key hurdle for certification of 28-V lithium-ion start/backup systems. This de-risks the adoption of airline and rotorcraft, and supports broader OEM selection.

- October 2025 — True Blue Power partnered with 101 Aviation to finalize STCs for Gen5 TB50/TB20 lithium-ion main-ship batteries on Bombardier and Gulfstream jets, with approvals targeted from early 2026. The program unlocks lighter, lower-maintenance retrofits across business aviation.

- April 2025 — Amprius launched its 450 Wh/kg SiCore™ high-energy cell for aviation, moving toward near-term mass production through its partners. The step targets longer range/endurance and higher payloads for AAM and UAS platforms.

- February 2025 — Safran Electrical & Power sought a lithium-metal cell partner to develop its GENeUSPACK for electric/hybrid propulsion, combining Safran’s packaging/thermal expertise with advanced chemistries. The alliance strategy is aimed at faster, certification ready high-voltage systems.

- October 2024 — Saft launched a new 28V lithium-ion aviation battery at NBAA-BACE for backup and engine start on bizjets and helicopters to cut weight and maintenance. The product targets lead-acid/Ni-Cd replacements, positioning Saft for broader linefit and retrofit opportunities.

- January 2024 — H55 advanced certification after EASA accepted its battery-pack Compliance Check List, enabling completion of tests for CS-23 propulsion packs. The move streamlines the route to type-certified electric trainers and hybrid demonstrators and should accelerate OEM integrations.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 7.46% from 2025-2032 |

|

Unit |

Value (USD Billion) |

|

By Aircraft Type |

|

|

By Battery Type |

|

|

By Application |

|

|

By End-User |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.86 billion in 2024 and is projected to reach USD 3.20 billion by 2032.

In 2024, the market value stood at USD 0.69 billion.

The market is expected to exhibit a CAGR of 7.46% during the forecast period of 2025-2032.

The fixed-wing aircraft segment led the market by aircraft type in 2024.

More-electric aircraft, AAM ramp, and higher battery content per tail are the key factors driving the market.

Safran Electrical & Power (France) and Parker Meggitt (U.K.) are some of the prominent players in the market.

North America dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us