Aircraft APU Market Size, Share & Industry Analysis, By End-User (OEM and Aftermarket), By Aircraft Type (Fixed Wing [Narrow Body, Wide body, Business Jets and Regional Jets], Rotary Wing, and UAVs), By Power Source (Conventional Fuel Combustion, Hydraulic Accumulator, Electric Powered and Others), By Platform (Commercial and Military), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

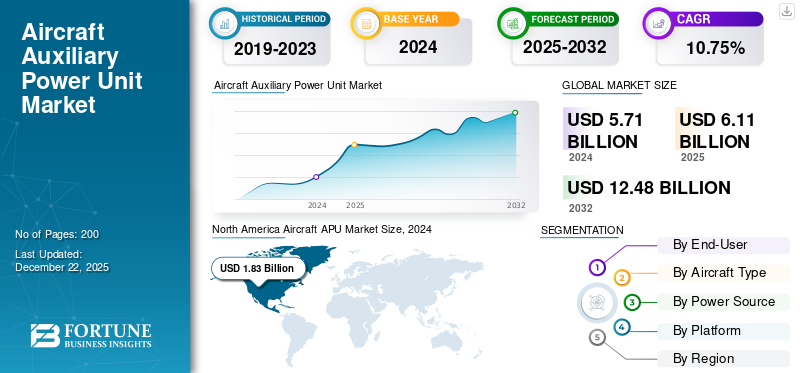

The global aircraft APU market size was valued at USD 6.11 billion in 2025. The market is projected to grow from USD 6.62 billion in 2026 to USD 14.85 billion by 2034, exhibiting a CAGR of 10.61% during the forecast period. North America dominated the global aircraft APU market with a market share of 31.91% in 2025.

The Auxiliary Power Unit (APU) is a compact gas turbine engine, usually installed in the tail of an airplane. It provides independent electrical power, compressed air and air conditioning when the main engines are not running. It also offers ground independence in flight, driving such systems as air conditioning, cockpit equipment and engine starters, and acts as a standby power source in case of emergency. The majority of market share is driven by top players such as Honeywell International Inc., Safran Group, Pratt & Whitney, PBS Velka Bites and Lufthansa Technik.

Increased utilization of APUs is triggered by growing demand for fuel efficiency and environmental controls. This compels manufacturers to develop even more environmentally friendly technology, such as electric APUs and biofuels. The push toward electric and hybrid aircraft goes even further and speeds up the process using electric APUs, leading to reduced emissions and maintenance. Advanced materials such as light composites increase reliability and simplicity of maintenance and reduce operating expenses. Integration with IoT based predictive maintenance reduces downtime and regulation compliance allows noise and emissions conformity. The global spread of aviation further demands safe handling on the ground, with APUs reducing the need for external power units and increasing efficiency and independence.

Download Free sample to learn more about this report.

Aircraft APU Market KEY TAKEAWAYS

- 2025 Market Size: USD 6.11 Billion

- 2026 Market Size: USD 6.62 Billion

- 2034 Forecast Market Size: USD 14.85 Billion

- CAGR: 10.61% from 2026–2034

- North America dominated the aircraft APU market with a 31.91% share in 2025.

- The aftermarket segment is projected to hold a 65.61% share in 2026.

- The fixed wing segment is projected to account for an 82.52% share in 2026.

Asia Pacific

Asia Pacific reached USD 1.56 billion in 2025, driven by rapid fleet expansion and increasing air travel demand.

North America

North America accounted for USD 1.95 billion in 2025, supported by strong aerospace manufacturing and advanced MRO infrastructure.

Europe

Europe reached USD 1.72 billion in 2025, driven by sustainable aviation initiatives and next-generation aircraft adoption.

U.S.

The U.S. market is projected to reach USD 1.53 billion in 2026, supported by commercial fleet expansion and military aircraft modernization.

Japan

Japan is projected to reach USD 0.31 billion in 2026, driven by fleet renewal and demand for high-reliability aircraft systems.

Read More

AIRCRAFT APU MARKET TRENDS

3D Printing, Modular and Lightweight Design, Enhanced Integration and Focus on Sustainability are Major Market Trends

Air transport operators are adopting 3D printing, lightweight and modular design, more integration, and a high concentration on sustainability as leading trends within the aircraft APU industry. Manufacturers are using 3D printing to make intricate and lightweight components more precisely and with less material wastage, yielding effective and low-maintenance APUs. Modular construction is becoming increasingly popular, allowing faster installation, simpler upgrades and maintenance, thus decreasing aircraft downtime and lifecycle costs.

The use of advanced materials and clever engineering leads to less heavy APUs, significantly increasing fuel consumption efficiency and payload capacity, both of which are required in modern aviation. Integration with aircraft systems, such as avionics, power management systems, and predictive maintenance platforms, further boosts operational reliability and efficiency, moving toward more electric airplanes.

The common thread is sustainability, with manufacturers selecting green materials, low-energy technologies as well as lower-emission and reduced-noise designs. Regulatory pressures, airline cost-cutting burden and the industry’s desire to reduce its environmental footprint are few other drivers behind these trends, setting the stage for long-term growth and technological development in the market in the next few years.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Surge in Global Air Travel and Expansion of Air Transport Networks to Result in Substantial Market Growth

Growing global air travel and aviation network expansion are primary forces behind global aircraft APU market growth. More people are flying, allowing airlines to expand their fleets and accelerate plane deliveries to meet the augmented demand driven by emerging nations with growing middle classes. This expansion demands efficient APUs, which can power aircraft ground systems such as air conditioning, lighting and engine starting, thus increasing operational flexibility and decreasing dependency on external power.

Besides, expanding low-cost carriers and new routes also contribute to the demand for high-efficiency APUs to allow greater aircraft utilization and passenger comfort. As carriers upgrade to newer fleets with more efficient and technologically advanced APUs, the market continues to grow with a focus on efficiency, sustainability and improvements in ground operations.

Market Restraints

High Development and Integration Costs to Restrain Market Growth

There are various reasons behind the slow demand for aircraft APU. APUs' outlandish development and integration expenses, especially sophisticated or specialty ones, are formidable barriers for makers and operators alike, particularly small companies or new operators. Strict green laws on emissions and noise pollution also constrain market growth, as traditional APUs are noisy and emit pollutants, and APU manufacturers and airlines look for alternatives. Market consolidation and more competition also constrain growth, and new entrants struggle to get in or remain viable.

Market Opportunities

Emergence of Electric and Hybrid APUs Act as a Major Market Opportunity

Hybrid and electric APUs present significant potential in aircraft design as the aviation sector moves toward greater sustainability, fuel efficiency and regulatory compliance. These electric and hybrid APUs achieve enhanced fuel efficiency and emissions reduction compared to traditional gas turbine units, aligning with the global push for environmentally friendly practices and adherence to stringent regulations. Hybrid-electric APUs can reduce fuel consumption by up to 5% in large commercial aircraft and 30% in regional commuter aircraft. Additionally, they can lower maintenance costs due to fewer moving parts and reduced reliance on fossil fuels.

Shifting to More Electric Aircraft (MEA) configurations and increasing utilization of electric propulsion systems also generate the need for electric and hybrid APUs, which enable efficient, reliable ground and auxiliary power without necessitating main engine operation. With manufacturers and airlines increasingly investing in next-generation aircraft, the application of electric and hybrid APUs is also anticipated to gain momentum, generating new market expansion and innovation opportunities.

Market Challenges

Regulatory Pressure to Challenge Market Growth and Restrict Development

Regulatory pressure is a significant force witnessed by aircraft APU sector, driven by governments such as the International Civil Aviation Organization (ICAO) and the Federal Aviation Administration (FAA), raising the bar on fuel efficiency, noise and emissions. Such backstopping takes manufacturers' massive investment in R&D to create friendlier and more efficient APU units, increasing development and manufacturing expenses.

Compliance also demands sophisticated engineering for multi-varying operating conditions and local noise regulations, particularly for city airports. Therefore, compliance with regulations creates entry barriers, affects the market's competitiveness, and reduces the innovation rate and emergence of new APU technology.

Segmentation Analysis

By End-User

Aging Fleets and Rising MRO Requirements to Drive Aftermarket Segment Growth

On the basis of end-user, the market has been divided into OEM and aftermarket.

The aftermarket segment is anticipated to hold a dominant market share of 65.61% in 2026. due to aging aircraft fleets and rising MRO needs. Increased air traffic has accelerated aircraft utilization, requiring frequent support, repairs and replacements. Carriers prioritize cost-effective retrofits and upgrades to expand operational lifespans, especially for older models, such as the Airbus A320ceo. The expansion of MRO facilities in Asia Pacific and the Middle East bolsters this development, with service providers offering predictive maintenance and IoT-enabled solutions to diminish downtime. Additionally, stricter administrative standards for emissions and noise are pushing carriers to replace outdated APUs with newer, compliant models, supporting aftermarket momentum.

The OEM segment is anticipated to rise with a CAGR of 12.16% over the forecast period.

By Aircraft Type

Rising APU Demand for Commercial Aviation Expansion and Fleet Modernization to Boost Fixed Wing Segment Growth

Based on aircraft type, the market is segmented into fixed wing, rotary wing, and UAVs. Fixed wing is further divided into narrow body, wide body, business jets, and regional jets.

The fixed wing segment is anticipated to hold a dominant market share of 82.52% in 2026. The surge in air travel post-pandemic has accelerated aircraft orders, especially for narrow-body planes, such as the Airbus A320 and Boeing 737, which rely on APUs for ground control and cabin systems. Carriers prioritize fuel-efficient, low-emission APUs to comply with stricter regulations, whereas progressions in lightweight composites and modular designs upgrade operational proficiency and decrease maintenance costs. Fixed wing APUs benefit from military modernization programs, with new transport and fighter aircraft requiring advanced auxiliary power for mission-critical systems. The Asia Pacific region, driven by China's C919 orders and India's aviation development, is a key segment growth driver.

The UAVs segment is anticipated to rise with a CAGR of 17.83% over the forecast period.

By Power Source

Growth in Military Application of Gas Turbine Engines to Augment Conventional Fuel Combustion Segment Growth

Based on power source, the market is segmented into conventional fuel combustion, hydraulic accumulator, electric powered, and others.

The conventional fuel combustion segment is anticipated to hold a dominant market share of 40.58% in 2026. Fueled by conventional fuel combustion, these units are essential for providing pneumatic and electrical power during ground operations and emergencies. Their broad selection of aircraft, such as the Airbus A380 (utilizing Pratt & Whitney's PW980) and Boeing 787 (electrical-only, but gas turbine-based), underscores their critical part. Innovations focus on progressing fuel proficiency, such as progressed compressor plans and reducing emissions to comply with stricter regulations. Gas turbine APUs are too integral to military aircraft and marine applications, where high power demand and operational flexibility are vital.

The electric powered APU segment is anticipated to rise with a CAGR of 13.73% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Rising Air Travel Requests to Drive Commercial Segmental Growth

Based on the platform, the market is segmented into commercial and military.

The commercial segment is anticipated to hold a dominant market share of 66.82% in 2026. The commercial segment is driven by rising air travel requests, particularly in developing markets such as Asia Pacific, where expanding fleets and new aircraft deliveries require advanced APUs. Sustainability orders are accelerating the adoption of electric APUs and hybrid frameworks, which reduce emissions and noise while improving fuel efficiency. Advancements such as 3D-printed components and lightweight composites enhance execution, with market players such as Honeywell integrating predictive maintenance to minimize downtime.

The military segment is anticipated to rise with a CAGR of 9.98% over the forecast period.

Aircraft APU Market Regional Outlook

By region, the market is studied across North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Aircraft APU Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 1.95 billion, representing 31.92% of global demand, and is projected to grow to USD 2.11 billion in 2026. North America dominates the market, driven by strong aerospace manufacturing by Boeing, Airbus U.S. operations, advanced MRO infrastructure, and military modernization, with strict FAA regulations. This ensures high-quality APUs for commercial fleets such as the A320neo and 737 MAX with a growing number of military contracts and business aviation powered by Gulfstream, Bombardier. These factors are driving the regional market growth. Post-pandemic air travel recovery and investments in electric and hybrid APUs, such as Honeywell’s 131- 9A, sustain growth efficiency upgrades, highly supported by research and development hubs and a focus on low-emission technologies. The U.S. market is valued at USD 1.53 billion by 2026.

U.S Aircraft APU Market

The U.S. market can be analytically approximated at around USD 1,593.9 million in 2026, accounting for roughly 10.80% of CAGR. The U.S. holds the largest APU market share globally, driven by commercial fleet expansions (United Airlines, Delta) and military procurement such as F-35 and P-8 Poseidon. Regulatory leadership, such as emission constraints, accelerates the adoption of advanced APUs. OEMs such as Honeywell and Pratt & Whitney also leads in electric APUs. Additionally, aging fleets such as the A320ceo retrofits boost the demand, with IoT integration optimizing MRO efficiency.

Europe

The Europe region captured 28.11% of the global market in 2025, generating USD 1.72 billion in revenue, and is projected to reach USD 1.87 billion in 2026. Europe’s market thrives on sustainability mandates primarily driven by EU Flight Path 2050 and airline partnerships such as the Lufthansa-Air France MRO collaboration. The region prioritizes low-emission APUs for next-gen aircraft such as the A350 and A220, with OEMs investing in hybrid-electric systems. Military modernization and general aviation growth by Dassault, Airbus Corporate Jet, and others lead to high product demand. Europe’s advanced infrastructure and focus on circular economy practices in MRO further drive market demand in the region. The UK market is valued at USD 0.51 billion by 2026, while the Germany market is valued at USD 0.45 billion by 2026.

U.K Aircraft APU Market

The U.K. market growth in 2026 is estimated at around USD 337.8 million, representing roughly 11.43% CAGR. U.K. aircraft APU demand is driven mainly by high aircraft movements, tight turnaround expectations and strong MRO connectivity with Europe. OEM demand is limited as compared to major assembly hubs, but aftermarket demand is solid due to heavy utilization, exchange/pooling reliance and a focus on quick troubleshooting and fast spares access.

Germany Aircraft APU Market

Germany’s market is projected to reach approximately USD 256.2 million in 2026. This is supported by a large European airline footprint and strong MRO/logistics capability. OEM-linked demand follows European production cadence, while aftermarket demand stays high due to cycle-heavy operations and winter conditions. Operators are disciplined buyers, prioritizing reliability upgrades, predictive maintenance and predictable turnaround to protect punctuality.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 1.56 billion in 2025, accounting for 25.48% share, and is expected to reach USD 1.71 billion in 2026. The Asia Pacific market is projected to achieve highest growth rate in the coming years, fueled by air travel surges and fleet expansions (China’s COMAC C919, IndiGo’s 500+ A320neo orders). Local manufacturing (Hindustan Aeronautics) and government initiatives (China’s aviation self-reliance policy) reduce import dependency. Low-cost carriers (AirAsia, SpiceJet) and military UAV programs (India’s Rustom-II) drive demand for compact, fuel-efficient APUs. MRO hubs in Singapore and Malaysia support the market growth, while investments in green APUs align with net-zero targets. The Japan market is valued at USD 0.31 billion by 2026, the China market is valued at USD 0.47 billion by 2026, and the India market is valued at USD 0.41 billion by 2026.

Japan Aircraft APU Market

The Japan market share in 2026 is estimated at around USD 233.5 million, accounting for roughly 11.73% of CAGR during the forecast period. Japan’s product demand is steady and quality-driven. Fleet renewal supports OEM-linked demand, while aftermarket demand is shaped by high dispatch standards and preventive maintenance culture. Strong airport infrastructure can reduce routine gate APU runtime, but APUs remain essential for irregular operations, cold weather starts and reliable autonomous capability across the network.

China Aircraft APU Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 531.3 million. China’s APU demand is expanding with fleet growth and dense domestic networks. OEM demand is delivery-led, while aftermarket demand accelerates as the installed base matures. High cycle intensity and regional weather extremes increase removals and spares pull, though parts access and shop capacity can create uneven execution and turnaround variability.

India Aircraft APU Market

The India market in 2026 is estimated at around USD 275.0 million. India’s market is among the fastest-growing due to aggressive fleet expansion and high utilization on short-haul routes. OEM demand tracks aircraft deliveries, while aftermarket demand rises sharply with cycles, heat, and dust exposure. Operators are cost-sensitive but invest in pooling, exchange units and reliability fixes to protect dispatch.

Rest of the World

The Rest of the World market generated USD 0.89 billion in 2025, representing 14.49% of the global market landscape, and is expected to reach USD 0.94 billion in 2026. The rest of the world include Middle East & Africa and Latin America. These regions are expected to witness moderate growth in this market space during the forecast period. The market in Latin America is witnessing moderate growth, driven by low-cost carrier expansions and fleet upgrades. Economic constraints and infrastructure gaps limit growth compared to other regions, but tourism growth in Mexico & Brazil and military modernization offer niche opportunities. Aftermarket services dominate due to aging regional jets, with partnerships such as Embraer-Honeywell supporting APU lifecycle management. The Middle East & Africa market is growing, owing to airline expansions and military UAV adoption. Airport modernization, such as Saudi Arabia’s Red Sea projects and MRO investments, further boosts aircraft APU demand in the region.

Competitive Landscape

Key Industry Players

Continuous Technological Innovations by Key Companies and Growing Demand for APUs Resulted in Their Dominating Positions in Market

The competitive landscape of the market offers insights into various competitors. Honeywell and Pratt & Whitney Canada anchor aircraft APU volumes, driven mainly by high-rate single-aisle programs where line-fit demand stays strong. Safran builds momentum in business jets, helicopters, and military platforms where autonomy and rugged reliability are key buying factors. Collins Aerospace supports growth through exchange and repair-chain models that improve availability, while Lufthansa Technik expands the market by adding MRO capacity and faster turnaround. PBS Aerospace grows through niche defense and special-mission wins, and Rolls-Royce influences longer-term direction via electrification roadmaps. Overall growth depends increasingly on production quality, parts availability, and repair throughput.

List of Key Aircraft APU Companies Profiled

- Honeywell International Inc. (U.S.)

- Pratt & Whitney (U.S.)

- Safran Group (France)

- Collins Aerospace (RTX Corporation) (U.S.)

- Rolls-Royce Plc (K.)

- Lufthansa Technik (Germany)

- PBS AEROSPACE (U.S.)

- Turkish Technic Inc. (Turkey)

- StandardAero (U.S.)

- MTU Aero Engines AG (Germany)

Key Industry Developments

- March 2025- Finnair, Finland's lead carrier, declared the re-establishment of its contract with EPCOR B.V. by an extra five years to support its A330 fleet's Auxiliary Power Units (APUs). EPCOR, the Air France Industries KLM Engineering & Maintenance (AFI KLM E&M), responsible for the repair of APU and pneumatic components, will proceed to supply the airline with maintenance for the GTCP331-350 model APUs.

- December 2024- Philippines Airlines unveiled a partnership with Air France KLM to maintain and repair the aircraft APUs of the A320 fleet of PAL. The partnership is specifically for APU131-9A.

- November 2024- Qatar Airways unveiled the selection of Honeywell International Inc. as the airline’s official maintenance and overhaul partner for aircraft APUs. The first license issued in the Middle East & Africa region marks a significant achievement by Qatar Airways.

- September 2024 – Airbus partnered with Honeywell International Inc. for Honeywell to provide Airbus with a major mechanical system for aircraft APUs for the company’s long-range, wide-body aircraft- A350.

- November 2023 – Pratt & Whitney partnered with Emirates to maintain their aircraft APU for the Airbus 380 Aircraft fleet. The contract is expected to be 10 years long and specifically would deal with maintaining and supporting the airline's 116 PW980 Auxiliary Power Units (APUs) on its Airbus A380 aircraft.

Report Coverage

The report analyzes the market in-depth and highlights crucial aspects, such as prominent companies, market segmentation, competitive landscape, APU types, and technology adoption. Besides this, it provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, it encompasses several factors contributing to the market's growth over the years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.61% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By End-User · OEM · Aftermarket By Aircraft Type · Fixed Wing o Narrow Body o Wide Body o Business Jets o Regional Jets · Rotary Wing · UAVs By Power Source · Conventional Fuel Combustion · Hydraulic Accumulator · Electric Powered

By Platform · Commercial

By Region North America (By End-User, Aircraft Type, Power Source, Platform and Country) · U.S. (By End-User) · Canada (By End-User) Europe (By End-User, Aircraft Type, Power Source, Platform and Country) · U.K. (By End-User) · Germany (By End-User) · France (By End-User) · Russia (By End-User) · Rest of Europe (By End-User) Asia Pacific (By End-User, Aircraft Type, Power Source, Platform and Country) · China (By End-User) · India (By End-User) · Japan (By End-User) · Australia (By End-User) · Singapore (By End-User) · Rest of Asia Pacific (By End-User) Rest of the World (By End-User, Aircraft Type, Power Source Platform and Country) · Latin America (By End-User) · Middle East & Africa (By End-User) |

Frequently Asked Questions

The market was valued at USD 6.11 billion in 2025 and is projected to record a valuation of USD 14.85 billion by 2034.

The market is projected to record a CAGR of 10.61% during the forecast period of 2026-2034.

By platform, the commercial segment accounted for a majority of the market share in 2025.

The surge in global air travel and expanding air transport networks resulted in substantial market growth.

Honeywell International Inc., Pratt & Whitney, Safran Group, Collins Aerospace (RTX Corporation), Rolls-Royce Plc, Lufthansa Technik, and others are some of the leading players in the market.

North America dominated the global market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us