Flood Barrier Market Size, Share & Industry Analysis, By Product (Temporary Barriers, Permanent Barriers, Floodgates, and Others), By Application (Urban, River, Coastal, Transportation, Utility & Critical Infrastructure, and Others), and Regional Forecast, 2026-2034

FLOOD BARRIER MARKET SIZE AND FUTURE OUTLOOK

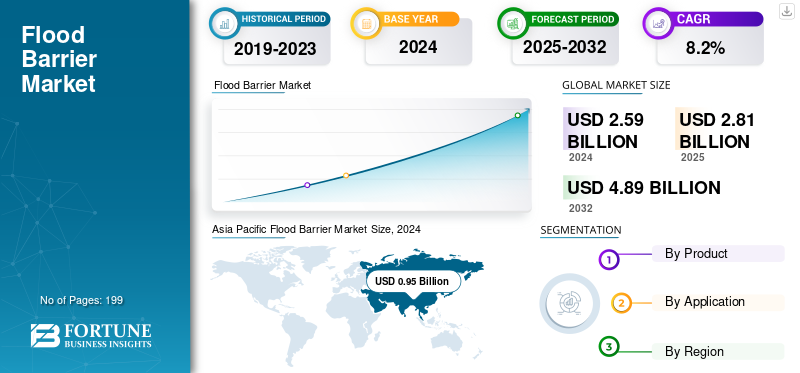

The global flood barrier market size was valued at USD 2.81 billion in 2025. The market is projected to grow from USD 3.05 billion in 2025 to USD 5.67 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period. Asia Pacific dominated the global flood barrier market with a market share of 1.15% in 2025.

A flood barrier refers to a constructed physical element or a configured system that is aimed at stopping or changing the flow of water to protect the flooded areas. Such protective devices might be installed for life, for only a short time, or may be automatically operated and serve different levels of protection, ranging from a single house up to the whole globe.

The market is expanding due to various reasons such as climate change resulting in frequent and severe floods, increasing urbanization and infrastructure development, as well as rising sea levels affecting coastal areas. Besides, stricter government regulations, increased awareness of climate risks, and technological advancements in resilient infrastructure are some of the other contributing factors.

The top firms in the industry are AquaFence, AWMA Water Control Solutions, Blobel Umwelttechnik, Denilco Environmental Technology, and Flood Control International.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Frequency and Severity of Floods Drives Market Growth

The rising number and severity of floods, mainly brought by climate change, erratic weather conditions, and high urbanization are greatly increasing the rate at which flood barrier systems are demanded. The focus is on investments in the robust flood management infrastructure by governments, municipalities and the private sector to ensure the protection of critical assets and the population. The emergence of awareness of disaster preparedness, as well as regulatory policies and climate resilient investments, is driving cities toward implementing superior flood barrier solutions to reduce economic costs and guarantee sustainable urban development.

Market Restraints

High Upfront Costs and Deployment Complexity to Hinder Market Growth

The extensive use of flood barrier systems has various obstacles associated with financial and technical problems. The huge start-up and installation costs, combined with the difficulties of implementing the systems, can frequently discourage small scale users and municipalities with limited funds. The long approval process, the need to integrate with the existing drainage systems, regular maintenance requirements, and specialized workforce requirements further complicate the implementation. Such difficulties render cost optimization, modular design innovation, and concise permitting necessary to surmount the restraints and stimulate more extensive adoption in developing and developed regions.

Market Opportunities

Urban Retrofit and Temporary Solution Demand Drive Growth, Creating Opportunities

The boost in the flood barrier suppliers in the rapidly urbanizing regions is being observed as a result of retrofit programs and the growing lack of preference for costly and flexible solutions. Short-term barriers, also known as temporary barriers or modular barriers, are becoming viable options for protecting urban places in need of scalable short-term barriers during seasonal flooding. The manufacturers have an opportunity to exploit this demand through innovation of flood protection systems, value-added services such as installation and maintenance, and collaboration models that include the participation of both the public and private stakeholders. This market trend promotes diversification of products and the availability of additional revenues from smart city/climate adaptation programmes.

FLOOD BARRIER MARKET TRENDS

Increasing Investment in Resilient Flood Infrastructure Emerges as a Major Market Trend

The increased interest in sustainable flood protection infrastructure is supported by efforts in global climate resilience. Modular and permanent flood barrier systems are becoming a priority for governments and private entities to enhance the resilience of critical infrastructure and reduce disaster recovery expenses in the long term. The tendencies are supported by incorporating smart monitoring technologies, predictive flood modeling, and maintaining maintenance programs based on the data. Additionally, investments in international climate adaptation funds are promoting cooperative projects that enable the rapid adoption of more technologies, as well as markets that are potentially broad-based due to the advanced and environmentally friendly flood mitigation initiatives around the globe.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product

Durability and Lower Maintenance Solutions of Permanent Barriers Drives Segment Growth

Based on theproduct, the market is segmented into temporary barriers, permanent barriers, floodgates, and others.

The permanent barriers segment is projecteed to dominate the market with a share of 38.36% in 2026. The growth is because governments and municipalities invest in long-term flood defense infrastructure to protect urban and critical assets. The high preference for durable, low-maintenance solutions where land-use and long planning horizons justify higher upfront capital expenditure.

Of all the segments, temporary barriers hold the highest CAGR of 8.8% in the global market. The growth is because they offer rapid deployment, flexibility, and lower initial cost for emergency response and short-term projects. Their adoption is rising among cities and event organizers that require scalable, on-demand protection without permanent structural changes.

To know how our report can help streamline your business, Speak to Analyst

By Application

Urban Segment Dominates Market Owing to Its Need to Safeguard Property and Critical Infrastructure

Based onapplication, the market is divided into urban, river, coastal, transportation, utility & critical infrastructure, and others.

The urban segment is projecteed to dominate the market with a share of 36.07% in 2026. The segment’s growth is because densely populated coastal and riverine cities prioritize flood protection to safeguard lives, property, and critical infrastructure. High economic value of urban assets and stricter building and planning regulations drive large investments in both permanent and hybrid solutions.

Urban also holds the highest CAGR of 8.8% in the global market. The segment’s growth is due to accelerating urbanization, greater exposure to extreme weather, and municipal budgets increasingly allocated to resilience. Municipal retrofits, waterfront redevelopment, and integrated city planning are creating recurring demand for innovative flood barrier systems.

FLOOD BARRIER MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America accounted for USD 0.58 Billion in 2025, representing 20.60% of the global market share, and is projected to reach USD 0.62 Billion in 2026. The region’s growth is due to increasing frequency and severity of extreme weather events, rising sea levels, and growing urbanization and infrastructure development.

The U.S. is at the forefront of the North American market, with expected revenue of USD 0.45 billion in 2026. The growth is due to increased extreme weather events, rising insurance costs, and a focus on resilient infrastructure, with demand strongest in coastal and urban areas.

Europe

The Europe market was valued at USD 0.71 Billion in 2025, capturing 25.10% of global revenue, and is estimated to reach USD 0.75 Billion in 2026. This growth is due to increasing awareness for flood control measures, driven by extreme weather events and climate change.

The U.K., Germany and Italy are some of the leading contributors to the growth in the market, with the required revenue stake of USD 0.13 billion, USD 0.18 billion by 2026 and USD 0.08 billion respectively by 2025.

Asia Pacific

In 2025, Asia Pacific held 37.10% of the global market, reaching a valuation of USD 1.04 Billion, and is projected to grow to USD 1.15 Billion in 2026. The region leads the market because of its large population in low-lying coastal zones, frequent monsoons and typhoons, and major infrastructure investments. Rapid urban expansion and rising awareness of climate risk are prompting national and local governments to fund large-scale flood defense projects.

Asia Pacific Flood Barrier Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

At the same time, Asia Pacific flood barrier market is also expected to have the highest CAGR of 9.6%, further solidifying the market as the fastest growing. The growth is due to accelerating economic development, increasing public and private spending on disaster resilience, and international funding initiatives. Countries in the region are prioritizing both permanent and temporary measures, creating a broad market for suppliers and technology innovators.

The Japan market is valued at USD 0.19 billion by 2026, the China market is valued at USD 0.43 billion by 2026, and the India market is valued at USD 0.21 billion by 2026.

Latin America

The Latin America region captured 7.10% of the global market in 2025, generating USD 0.2 Billion in revenue, and is projected to reach USD 0.22 Billion in 2026.

South America and Middle East & Africa

Middle East & Africa contributed approximately USD 0.28 Billion to the global market in 2025, accounting for 10.10% share, and is expected to reach USD 0.31 Billion in 2026. due to increasing climate change-related floods, rapid urbanization, and government initiatives for infrastructure development and disaster mitigation.

GCC countries are predicted to have a market share of USD 0.12 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus On R&D Investment to Develop Innovative and Lightweight Barriers

The key players in the industry are AquaFence, AWMA Water Control Solutions, Blobel Umwelttechnik, Denilco Environmental Technology, and Flood Control International. The players are focusing on several strategies, including R&D investment to develop innovative, lightweight, and rapidly deployable barriers. Companies are also expanding on manufacturing, leveraging integration opportunities, and expanding their customer base through geographic expansion and customization. Additionally, they are emphasizing factors such as barrier effectiveness, durability, and cost-efficiency, while also increasingly considering environmental impact and aesthetic concerns in urban areas.

LIST OF KEY FLOOD BARRIER COMPANIES PROFILED

- AquaFence (Norway)

- AWMA Water Control Solutions (Australia)

- Blobel Umwelttechnik (Germany)

- Denilco Environmental Technology (China)

- Flood Control International (U.K.)

- FloodBreak LLC (U.S.)

- IBS Technics GmbH (Germany)

- Muscle Wall (U.S.)

- NoFloods (Denmark)

- PS Industries (U.S.)

- The Flood Company (U.S.)

- US Flood Control Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025- Flood Risk America, a leader in flood protection solutions across North America, announced the release of its newest innovation, the Passive Automatic Flood Gate. This barrier activates automatically when floodwaters rise, providing dependable, self-activated flood protection.

- February 2025- BrightShore Insurance Company “BrightShore” announced its launch in New Jersey, offering a solution to coastal homeowners' insurance needs. Addressing the common issue of inadequate flood coverage, BrightShore provides a single policy that combines comprehensive traditional homeowners’ insurance with full flood protection.

- January 2023- The Flex Seal® Family of Products launched its revolutionary new line: Flex Seal Flood Protection. This line consists of four Flex Seal products, specially formulated to help defend homes and businesses from floodwaters, all while being completely removable after waters recede.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the flood barrier market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 8.00% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, and Region |

| By Product |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 3.05 billion in 2026 and is projected to reach USD 5.67 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 8.0% during the forecast period.

Rising frequency and severity of floods is speeding up the market growth.

AquaFence, AWMA Water Control Solutions, Blobel Umwelttechnik, Denilco Environmental Technology, and Flood Control International are some of the top players in the market.

The Asia Pacific region held the largest market share.

Asia Pacific was valued at USD 1.04 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 199

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us