Freighter Aircraft Market Size, Share & Industry Analysis, By Freighter Type (OEM Configured and P2F Converted), By Engine (Turboprop and Turbofan), By Application (Commercial and Military), By Aircraft Type (Narrow Body, Wide Body, Regional Aircraft, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

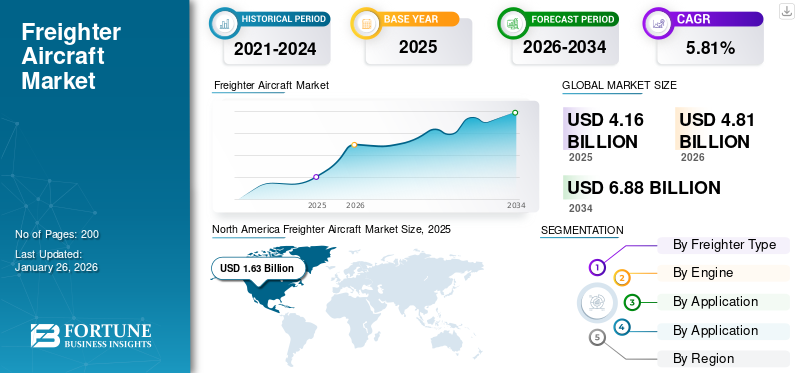

The global freighter aircraft market size was valued at USD 4.16 billion in 2025. The market is projected to grow from USD 4.81 billion in 2026 to USD 6.88 billion by 2034, exhibiting a CAGR of 5.81% during the forecast period. North America dominated the freighter aircraft market with a market share of 39.25% in 2025.

A freighter aircraft, also known as a cargo aircraft, is a specially designed or converted aircraft to carry cargo rather than people. These airplanes usually lack passenger amenities and have large doors for fast loading and offloading goods. Their characteristics include a wide body, high-swept wings for easy ground access, and strengthened floors for large cargo. It plays an important role in global logistics, especially in time-sensitive deliveries and the international air transport of goods, including raw materials and perishable items. Growing demand for air cargo is expected to lead to substantial growth in the market over the forecast period.

The global market development is driven by the growing e-commerce explosion, which aims at advanced and fast transportation. Moreover, the overall landscape for air cargo is expanding, driven by increasing levels of global trade and the urge for fast shipping. The expansion of the global economy and rising air cargo volumes are driving investments in freighter aircraft deliveries across the globe. Technological advancements in aircraft manufacturing are further amplifying these trends with the development of more efficient and capable freighters. This combination allows continued expansion in the market, as they become crucial to enabling global commerce and demand in a rapidly evolving and digitally driven world.

Download Free sample to learn more about this report.

Freighter Aircraft Market Key Takeaways

- 2025 Market Size: USD 4.16 Billion

- 2026 Market Size: USD 4.81 Billion

- 2034 Forecast Market Size: USD 6.88 Billion

- CAGR: 5.81% from 2026–2034

- North America dominated the freighter aircraft market with a 39.25% share in 2025.

- The OEM configured segment is projected to hold an 87.19% market share in 2026.

- The commercial segment is expected to account for an 88.41% market share in 2026.

North America

North America reached USD 1.63 billion and accounted for 39.25% of the global market in 2025.

Europe

Europe generated USD 1.16 billion, contributing 27.76% of global market revenue in 2025.

Asia Pacific

Asia Pacific accounted for USD 0.83 billion, representing 19.89% of the global market in 2025.

U.S.

The market is projected to reach USD 1.64 billion in 2026, supported by strong cargo and defense demand.

Japan

The freighter aircraft market is expected to reach USD 0.18 billion in 2026.

Read More

Market Dynamics

Market Drivers

Growing E-Commerce Trade and the Influence of Global Trade Contributes to Market Growth

E-commerce has transformed global trade, with tremendous growth in the air cargo industry and increased demand for freighter aircraft. The growth in online shopping demands faster and more reliable delivery services, which air cargo is well-positioned to offer. Such demand is fueled by competitive pricing, diversity of products, and the convenience of shopping from anywhere in the world.

E-commerce growth has been substantial along routes from China to Europe and the U.S. Demand for super freighter aircraft, such as the Boeing 777F and Airbus A350F, is also increasing. According to Boeing, e-commerce is fueling a surge in air cargo demand, with online platforms shipping over 10,000 tons of goods daily, which is equivalent to the capacity of 100 Boeing 777 freighters. It is, therefore, expected that express shipments will account for 1/4th of all air cargo business in 2043, with volumes increasing at 5.8% per year, compared to 3.6% for general cargo. This demand has generated significant investments in freighter fleets from the incumbent carriers and newly established ones.

Boeing's study on air cargo, as of December 2024, indicated that airfreight shipping volumes would be pushed to a 4 % annual growth, doubling air traffic in 20 years, mainly due to the global economic growth, diversification of supply chain disruptions, and increasing demand for e-commerce.

- In December 2024, Amazon amplified its tried and demonstrated coordination arrangements with businesses over India. These administrations give clear estimation and simple integration for both B2B and B2C operations for companies of all sizes in the e-commerce market.

Market Restraints

High Cost of Operations to Restrain Market Growth

Numerous factors are hampering the freighter aircraft market growth, and higher cost is the primary restraint. Purchasing and maintaining these aircraft is costly as compared to passenger aircraft, given repeated cargo loading and unloading. Environmental issues also pose a challenge since these have higher emissions than passenger aircraft, and thus, more regulatory inspection is done on their activities. Furthermore, geopolitical instability and trade disputes also restrict air cargo routes and introduce uncertainty in global trade. Shortage of skilled labor for operations and maintenance, coupled with limited conversion slots to transform passenger aircraft into freighters, adds to the operational challenges for the market. Moreover, price volatility in fuels also affects operational costs and thus further constrain the growth of this market.

Market Opportunities

Conversion From Passenger to Freighter Acts as a Major Market Opportunity

Passenger-to-freighter (P2F) conversions are a huge opportunity in the market, which is driven by the need for cost-effective and efficient cargo solutions. This process involves transforming retired or underutilized passenger aircraft into dedicated freighters, thereby allowing airlines to maximize their assets. This conversion usually includes removing passenger interiors, installing a cargo door, and reinforcing the fuselage to handle heavier loads. P2F conversions are more financially affordable compared to new freighter aircraft, priced at about USD 25 million, while a new freighter will cost the operator around USD 150 to 200 million. With such low investments, it facilitates quick ROI for operators and gets quicker revenue.

Additionally, as global air cargo demand continues to grow, driven by cross-border e-commerce growth, converted freighters offer a flexible solution to expand capacity without the long lead times associated with new aircraft production. In addition, these conversions contribute to sustainability efforts by extending the lifecycle of existing aircraft and reducing waste. With the rise of the air cargo industry, P2F conversions become crucial in increasing supply with the help of operational and financial benefits.

Market Challenges

Competition From Jet Aircraft to Challenge the Market Development

The main challenge that the market competition poses to a freighter model is the jet plane. Jets go faster, have long ranges, and may fly at far higher altitudes than Freighters, increasing efficiency over higher distances. Additionally, this is effective in traveling altitude for several hours on most long flights, and it is ideal for sipping fuel from a large oil tank. While freighters shine in short-haul operations, as they are lower in operating cost and can handle shorter runways, airlines, with a keen focus on the need for greater speed and higher capacity, jets are highly preferred in regional markets, affecting the demand for freighters.

Freighter Aircraft Market Trends

Emergence of Sustainable Aviation Fuel to Act as Major Market Trends

Sustainable Aviation Fuel (SAF) is a new substitute for the fossil jet fuel in use, intended to reduce carbon emissions by a significant percentage and make the freighter a fuel-efficient aircraft. It is derived from renewable feedstocks that include used cooking oils, animal fats, agricultural residues, and municipal waste. This biofuel reduces lifecycle greenhouse gas emissions by up to 80% as compared to traditional jet fuels. Efforts from the aviation industry must reach the net-zero target of carbon emissions by 2050. Additionally, the major benefit of SAF is its compatibility with currently available aircraft and infrastructure, as they can be added to conventional jet fuel without engine or fuel system modifications. Currently, the law allows for a maximum blend of 50%.

Download Free sample to learn more about this report.

However, it is predicted that the technology will soon advance up to 100% SAF by 2030. The manufacture of SAF also supports a circular economy by utilizing waste streams that materialize into landfill problems. As aviation becomes more sustainable, it considers SAF to be an important solution to lower environmental impacts while ensuring operational efficiency. Scaling up can be achieved only when it is supported by favorable government policies invested with satisfactory funds in infrastructure and technology.

Impact of COVID-19

The COVID-19 pandemic intensively affected the dynamics and supply chains of production and sales of freighter aircraft. It also brought traditional air travel to a standstill and increased the demand for air cargo. Passenger flights were grounded, and the belly cargo capacity plummeted as airlines relied more on dedicated freighters. This situation caused airlines to convert unutilized passenger aircraft into freighters to bridge the immediate requirement for shipping crucial goods with the growing prominence of e-commerce. Air cargo rates shot through the roof as operational and regulatory costs began to surface. Progress toward sustainability was accelerated during the pandemic, and investment in sustainable aviation fuels and aircraft designs became faster.

Segmentation Analysis

By Freighter Type

Fleet Modernization of Major Airlines Propelled OEM Configured Segment Growth

On the basis of freighter type, the market has been divided into OEM configured and P2F converted.

The OEM configured segment is anticipated to hold a dominant market share of 87.19% in 2026 and is expected to grow at the highest CAGR during the forecast period. The modernization drive for airlines involves the replacement of older, less fuel-efficient aircraft with new ones that meet environmental standards and reduce the cost of operating. It aims at reducing carbon emissions and increasing energy efficiency. Newer aircraft consume about 30% less fuel than their predecessors, thus lowering CO2 emissions by significant amounts. Fleet renewal also encompasses technical modifications of existing aircraft, such as optimizing engines and equipping them with fuel-saving technologies.

In July 2024, The Boeing Company and Emirates SkyCargo reported an arrangement for five extra 777 Tankers. The administrator picked the world's most competent twin-engine vessel to meet developing cargo requests. The modern buy takes Emirates' arranged book to 245 Boeing widebody airplanes, counting 10 777 Vessels.

The P2F segment accounted for a significant market share in 2024. The increase in demand for air cargo services is a significant growth driver for the Passenger-to-Freighter (P2F) configured aircraft. In essence, e-commerce has also been growing rapidly. With the steady trend of online shopping, there is a tremendous need for efficient and reliable transportation of goods – as a channel, airlines are converting older passenger aircraft into freighters. It is usually cheaper to purchase than a new freighter aircraft, which enables airlines to extend the life of existing aircraft while still satisfying the market demand.

By Engine

Better Fuel Efficiency of Turbofan Engines to Augment Segmental Growth

Based on the engine, the market is segmented into turboprop and turbofan.

In 2026, the turbofan segment is projected to lead the market with a 75.27% share and is expected to grow at the highest CAGR during the forecast period. Turbofan engines can be used for short domestic and long international routes. This makes them capable of handling all kinds of cargo operations. Thus, airlines are interested in turbofan engines to optimize their fleets. Turbofan engines consume less fuel compared to other engines and perform better as well. They produce thrust through a combination of jet core efflux and bypass air, offering longer flight ranges and reduced operation costs, which are critical in cargo operations.

The turboprop segment accounted for a substantial market share in 2024. This has allowed turboprop aircraft to be broadly utilized within military and cargo missions. Turboprop engines possess exceptional fuel efficiency, which reduces high operating costs for various missions, particularly in regions with limited fuel availability. Due to short takeoff and landing, operations can take place from smaller airfields and unpaved runways, though crucial for military logistics as well as humanitarian missions. Turboprops are highly versatile, as they can be used for transporting personnel and cargo, reconnaissance, and surveillance. For example, the Beechcraft King Air is used for intelligence and cargo movements, proving their versatility.

By Application

Growing Focus on the Speedy and Efficient Movement of Commodities Boosted Commercial Segment Expansion

Based on application, the market is segmented into commercial and military.

The commercial segment accounted for the largest market share and is expected to grow at the highest CAGR in the forecast period. The commercial segment is projected to dominate the market with a share of 88.41% in 2026. Freighter airplanes are highly important in commercial usage as they offer speedy and efficient movement of commodities to any sector of the world. For the delivery of raw materials as well as the finished products, manufacturing, automobile, and e-commerce rely on these airplanes. For instance, the cargo airplane Boeing 747-8F is designed to carry oversized cargo, while the Airbus A330-200F is designed to carry temperature-sensitive cargo. They help to move perishable cargo and pharmaceuticals, among others, that have a higher value. Thus, the products shall be able to reach consumers even under the required conditions. At large, the growing e-commerce sector produces air freight in this particular aspect since the air freighter airplane represents one of the currently highly priceless tools for logistics.

The military segment accounted for a significant market share in 2024. The segment is expected to record a CAGR of 4.59% during the forecast period. Logistics for a particular mission is enhanced by rapid and efficient transportation of sensitive freight into difficult or severe locations. Two of the most typical types used are the Lockheed C-130 Hercules and Boeing KC-135 Stratotanker, which are versatile for landing from any short-runway base. Military freighters are also significant in humanitarian missions and disaster relief, where resources must be readily available for rapid deployment. Their ability to carry heavy payloads and operate over a variety of environments allows them to be an incredible asset to military operations in any continent.

By Aircraft Type

Rise In Long-Haul Cargo Transportation to Augment Wide Body Segment Growth

Based on aircraft type, the market is divided into narrow body, wide body, regional aircraft, and others.

The wide body segment is expected to lead the market, contributing 63.38% globally in 2026 and is expected to grow at the highest CAGR in the forthcoming years. The segment is likely to capture 62% of the market share in 2025. The growing need to achieve efficient long-haul cargo transportation acts as the main driver for segmental growth. Expansion of global trade, especially in high-growth markets such as Asia, increases the need for larger aircraft to carry significant volumes of cargo over the long term. Large wide body freighters, such as the Boeing 777F and Airbus A350F, are effective in carrying high-value products and e-commerce shipments due to their increased payload capabilities and improved operational efficiencies. Advances in turbofan engine technology have brought improved fuel efficiency, reduced emissions and making them an indispensable part of this changing logistics map.

The regional aircraft segment is expected to record a high CAGR of 5.55% over the forecast period. Regional freighter aircraft is on the rise as it creates an opportunity to link smaller airports and underserved markets. The demand for regional freighters rises with the growing economies of e-commerce and will result in quick deliveries. Short-haul routes are inexpensive for regional freighters, and this enables the operators to optimize the logistic services and reach remote places that are inaccessible by larger aircraft. In addition, performance and reliability with turboprop technology have brought regional freighters to the forefront of dedicated cargo operations and passenger-to-freighter conversions. This growing attention to regional connectivity supports the expansion of the overall air cargo market.

To know how our report can help streamline your business, Speak to Analyst

Freighter Aircraft Market Regional Outlook

The global market is divided into North America, Europe, Asia Pacific, and the rest of the world, according to the regions.

North America

North America Freighter Aircraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Passenger-to-Freighter Conversions Boosted Market Growth in North America

North America maintained a strong presence in the global market, reaching USD 1.63 billion in 2025, accounting for 39.25% share, and is expected to reach USD 1.88 billion in 2026. Another notable trend is passenger-to-freighter conversions as airlines seek to optimize their cargo fleets while meeting the growing capacities. Major companies such as FedEx are investing in more advanced freighter aircraft to improve their operational efficiency. In addition, the development of a fully-fledged aviation industry and development in airports also promote the growth of this market, further establishing North America as an aerospace air cargo transport leader.

In 2024, the U.S. market accounted for a dominating market share. The U.S. market size is estimated to hit USD 1.64 billion in 2026. There is an increasing need for cost-effective regional air transportation, especially to distant areas. Travel over short distances is ideally served by turboprop aircraft, which is an affordable means of connecting smaller cities and towns in the U.S. The military sector accounts for a significant proportion of market development, and whenever defense expenditures increase, turboprop aircraft orders to support training, transport, and intelligence operations soar. New plane orders such as the AT-802U Sky Warden are an indicator of this trend in the U.S.

Europe

In 2025, Europe generated USD 1.16 billion, contributing 27.76% to global market revenue, and is projected to grow to USD 1.34 billion in 2026. The European market is forecast to achieve a higher growth rate in the coming years. Europe is anticipated to account for the second-highest market size of USD 1.16 billion in 2025, exhibiting the second-fastest growing CAGR of 6.04% during the forecast period. The European market will experience immense growth by 2032, owing to its huge demand for air cargo service due to expansion in e-commerce and its strong requirement for appropriate logistics solutions. Recent developments include Lufthansa Cargo taking its orders toward the Boeing freighter fleet to upgrade further its capability and potential for its cargo carrier business operations. Advances in airline-to-freighter conversion and supportive regulations for new aircraft type certification sets the stage for Europe to play a significant role in global air cargo. The market value in U.K. is expected to be USD 0.26 billion in 2026.

On the other hand, Germany is projecting to hit USD 0.52 billion in 2026 and France is likely to hold USD 0.13 billion in 2025.

Asia Pacific

The Asia Pacific market accounted for USD 0.83 billion in 2025, representing 19.89% of the global industry, and is expected to reach USD 0.97 billion in 2026. The Asia Pacific market is forecast to achieve the highest growth rate in the coming years. This region is to be anticipated as the third-largest market with USD 0.83 billion in 2025. This is due to the high demand for air cargo services with a rapidly growing e-commerce industry and strengthening regional trade ties. It is further compounded by the movement of transportation to air from marines owing to disruption caused in shipping logistics. However, with passenger aircraft being converted to freighters, capacity constraints are being eased. Aircraft technology has improved the operational efficiency of aircraft. All these factors position the Asia Pacific region as one of the leaders in the market. The market value in China is expected to be USD 0.37 billion in 2025.

On the other hand, India is projecting to hit USD 0.23 billion and Japan is likely to hold USD 0.18 billion in 2026.

Rest of the World

Rest of the World accounted for USD 0.54 billion in 2025, representing 12.96% of the global market share, and is projected to reach USD 0.62 billion in 2026. The rest of the world market is forecast to achieve a higher growth rate in the coming years. The availability of natural resources in different regions and the need for efficient logistics solutions further support this dominance. The Rest of the World is anticipating to be the fourth-largest market with a size of USD 0.54 billion in 2025. On the other hand, passenger-to-freighter conversion leads to an enhancement of capacities and flexibility. Latin America is now profiled as a critical player in global air cargo networks. The geographical position of this region as a passage between continents further facilitates huge volumes of air cargo traffic. The company is investing in fleet renewal and increasing cargo capacity through freighter additions and conversions, which improve operational effectiveness in order to meet emerging market requirements.

Competitive Landscape

Key Industry Players

New Initiatives, Partnerships, and Aircraft Deliveries by Key Market Players are Expected to Boost the Competition in the Market

The competitive landscape of the global freighter aircraft market offers insights into various competitors. This includes an overview of each company, its financial performance, revenue generation, and market potential. Key players emphasize investments in research and development, new initiatives, strengths and weaknesses, product and brand portfolios, product launches, mergers and acquisitions, and their applications. The data provided focuses specifically on the companies' engagement within the market.

List of Key Freighter Aircraft Companies Profiled

- Airbus SE (Netherlands)

- The Boeing Company (U.S.)

- Embraer S.A. (Brazil)

- Bombardier Inc. (Canada)

- Textron Aviation Inc. (U.S.)

- Antonov (Ukraine)

- Lockheed Martin Corporation (U.S.)

- Ilyushin Aviation Complex (Russia)

- ST Engineering Inc. (Singapore)

- ATR Aircraft (France)

Key Industry Developments

- December 2024 – The U.S.-based cargo charter airline startup- Global Crossing Airlines partnered with a private equity group to establish a segment of their business in Australia. The new venture is expected to provide both cargo and passenger transportation.

- November 2024- Elbe Flugzeugwerke GmbH (EFW) and MRO Japan (MJP) announced a partnership in P2F transformations. This association sets up MJP as Japan's, to begin with the change location for the next-generation Airbus narrow-body P2F airplane. The contract was marked at the inaugural Airbus and EFW P2F Symposium Japan. Beneath the terms of the contract, MJP will act as a subcontractor for EFW, advertising third-party transformation administrations for EFW's Airbus A320P2F/A321P2F programs.

- October 2024- A new plant was launched in Vadodara city, India, by the prime minister of India and Spain to produce Airbus C297. This military aircraft is set to boost India’s defense and manufacturing capabilities.

- September 2024 – Brazil-based aircraft manufacturer- Embraer unveiled a proposal for India-based conglomerate- Mahindra Group to build an assembly line for C-390, a military transport aircraft in India. The partnership was proposed to meet the Indian Air Force’s transport aircraft program.

- August 2024- My freighter airlines and American Airlines concurred on an interline association that will permit both carriers to get to each other's cargo systems by means of North America, Europe, and Central Asia. The partnership is said to serve as a benchmark to cargo carriers around the world, displaying the conceivable outcomes that can be accomplished through common participation.

Report Coverage

The report analyzes the market in-depth and highlights crucial aspects, such as prominent companies, market segmentation, competitive landscape, aircraft types, and technology adoption. Besides this, it provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market's growth over the years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.81% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Freighter Type

By Engine

By Application

By Aircraft Type

By Region

|

Frequently Asked Questions

The market was valued at USD 4.81 billion in 2026 and is projected to reach USD 6.88 billion by 2034.

The market is projected to record a CAGR of 5.81% during the 2026-2034 forecast period.

The commercial application segment led the market in 2026.

E-commerce boom and global trade dynamics lead to substantial market growth.

Airbus SE, The Boeing Company, and Embraer are some of the leading players in the market.

The U.S. dominated the global market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us