Fuel Cell Commercial Vehicle Market Size, Share & Industry Analysis, By Vehicle Type (Bus and Truck), By Application (Urban Transit, Urban delivery/last-mile, and Others), By Power output (<200kW, 201-300kW, and >300kW), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

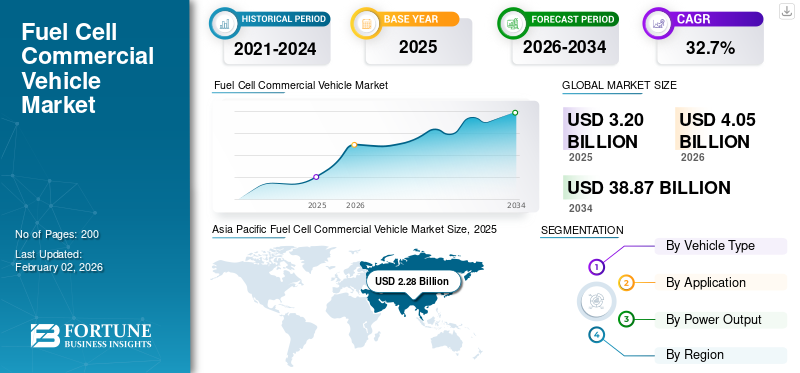

The global fuel cell commercial vehicle market size was valued at USD 3.20 billion in 2025. The market is projected to grow from USD 4.05 billion in 2026 to USD 38.87 billion by 2034, exhibiting a CAGR of 32.7% during the forecast period. Asia Pacific dominated the global market with a market share of 71.25% in 2025.

The market refers to road-legal commercial vehicles powered by hydrogen fuel cell electric powertrains, including buses and trucks used for passenger and freight transportation. These vehicles generate electricity onboard through a fuel cell, primarily Proton Exchange Membrane Fuel Cells (PEMFCs), and use electric motors for propulsion, typically supported by a battery system. The market covers vehicle sales and deployments across key regions such as North America, Europe, Asia Pacific, and the rest of the world.

The market is primarily driven by decarbonization targets for medium- and heavy-duty transport, where fuel cells offer advantages over battery-electric solutions, especially for long-range, high-payload, and fast-refueling requirements. Governments across major economies are implementing Zero-Emission Vehicle (ZEV) mandates, hydrogen strategies, and freight corridor programs, which directly support the adoption of fuel cell commercial vehicles. Urban air-quality regulations are accelerating the deployment of fuel cell buses in public transit fleets, while hydrogen-powered trucks are gaining attention for long-haul and regional freight, where downtime and vehicle utilization are critical. Continuous improvements in fuel cell durability, reductions in system costs through scale, and the expansion of hydrogen refueling infrastructure further support market growth.

Major players include Hyundai Motor Company, Toyota Motor Corporation, Daimler Truck, Volvo Group, Nikola Corporation, and leading Chinese OEMs such as Foton, FAW, and Sinotruk, which are actively developing fuel cell buses and heavy-duty trucks. Technology suppliers such as Ballard Power Systems play a critical role by providing fuel cell modules integrated into vehicles produced by bus and truck OEMs.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Government Policy Support and Hydrogen Strategies Drive Market Growth

A primary driver of the market is expanding government policy support and national hydrogen strategies, which are accelerating the adoption of hydrogen fuel cell buses and trucks by shaping regulation, infrastructure investment, and financial incentives. In the U.S., the National Zero-Emission Freight Corridor Strategy outlines a phased approach to deploying hydrogen refueling infrastructure along major freight routes, targeting at least 30% zero-emission medium- and heavy-duty vehicle sales by 2030. This provides strategic clarity for fleets and manufacturers considering fuel cell technology. Similarly, Japan’s Ministry of Economy, Trade, and Industry has designated priority regions and introduced subsidies for hydrogen refueling and the deployment of commercial vehicles to narrow the cost gap with diesel, aiming to scale up the adoption of hydrogen trucks and buses. In Europe, public funding under programs such as the IPCEI framework supports innovation in hydrogen mobility across multiple transport sectors. This development drives the fuel cell commercial vehicle market growth.

MARKET RESTRAINTS

Limited Hydrogen Refueling Infrastructure Availability May Limit Market Growth

Limited availability of hydrogen refueling infrastructure remains a significant restraint for the market. Unlike conventional fuels and electric charging networks, hydrogen refueling stations are sparse, unevenly distributed, and often concentrated in pilot regions or specific corridors. This lack of widespread infrastructure restricts operational flexibility for fleet operators, particularly in long-haul and multi-route commercial applications, where reliable access to refueling is crucial. Transit agencies and long haul logistics companies are often required to invest in dedicated or depot-based hydrogen stations, which substantially increase upfront project costs and slows large-scale adoption. Additionally, many existing hydrogen stations are designed for passenger vehicles and lack the capacity or dispensing speed required for heavy-duty buses and trucks. Infrastructure permitting timelines, high capital expenditure, and coordination challenges between vehicle deployment and station rollout further compound the issue. Until hydrogen refueling networks achieve broader geographic coverage and readiness for heavy-duty vehicles, fuel cell commercial vehicles will face adoption barriers compared to more established diesel and battery-electric alternatives.

MARKET OPPORTUNITIES

Growing Adoption in Public Transit and Municipal Fleets to Create Lucrative Growth Opportunities

Growing adoption of fuel cell technology in public transit and municipal fleets represents a significant opportunity for the global fuel cell commercial vehicle market. Transit authorities and local governments are under increasing pressure to reduce emissions, improve urban air quality, and meet climate targets, making zero-emission buses a strategic priority. Fuel cell buses are particularly attractive for public transport systems that operate high daily mileage, have fixed routes, and demanding duty cycles, where fast refueling and consistent range offer operational advantages over battery-electric alternatives. Municipal fleets, including those for waste collection, street maintenance, and utility vehicles, are also exploring hydrogen solutions to decarbonize their operations without compromising vehicle availability. Many governments support these deployments through public procurement programs, subsidies, and pilot funding, lowering adoption risks for fleet operators. As cities expand their clean transport initiatives and replace aging diesel fleets, fuel cell commercial vehicles are well-positioned to secure long-term contracts, stable demand, and repeat orders, creating sustained growth opportunities across both developed and emerging urban markets.

FUEL CELL COMMERCIAL VEHICLE MARKET TRENDS

Increasing Focus on Heavy-Duty and Long-Haul Applications is a Significant Market Trend

A significant trend shaping the fuel cell commercial vehicle market is the growing emphasis on heavy-duty and long-haul transportation applications. As fleet operators evaluate zero-emission technologies, fuel cell electric vehicles are gaining attention for use cases that require long driving range, high payload capacity, and minimal downtime. Battery-electric solutions often face challenges in long-haul operations due to extended charging times and the requirement for large, heavy battery packs. In contrast, hydrogen fuel cell trucks offer fast refueling and consistent performance over long distances. This makes fuel cell technology particularly attractive for regional haul, port drayage, and long-haul freight corridors. OEMs are increasingly prioritizing the development of high-power fuel cell systems and scalable platforms designed for heavy-duty trucks. At the same time, infrastructure planning is increasingly aligned with freight corridors, supporting hydrogen availability where demand is highest. As a result, fuel cell adoption is gradually shifting from transit-focused deployments toward freight-dominated applications.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Limited Availability of Green and Low-Cost Hydrogen is a Challenging Factor for the Market

Limited availability of green and cost-competitive hydrogen remains a major challenge for the global Market. While hydrogen fuel cell vehicles offer zero tailpipe emissions, their overall environmental and economic benefits depend heavily on access to low-carbon hydrogen produced from renewable or low-emission sources. Currently, most hydrogen is derived from fossil fuels, and green hydrogen production remains limited in scale and expensive due to high electricity costs, high investment in electrolyzers, and the requirements for infrastructure. This constrains the fuel supply for commercial fleets, resulting in hydrogen prices that are often higher and less stable than those of conventional fuels. Until green hydrogen production scales significantly and achieves cost reductions, the adoption of fuel cell commercial vehicles will face economic and sustainability-related challenges.

Segmentation Analysis

By Vehicle Type

Bus Segment Leads Owing to Strong Public Transit Adoption and Government Support for Zero-Emission Fleets

Based on vehicle type, the market is classified into bus and truck.

The bus segment represents the dominant fuel cell commercial vehicle market share driven primarily by strong adoption in public transit systems. Fuel cell buses are particularly well-suited for urban transit due to their ability to support high daily mileage, fast refueling, and predictable route operations. Governments and municipal authorities are increasingly prioritizing zero emission buses to meet air quality regulations and climate targets, making fuel cell technology a viable alternative to diesel fleets. Public procurement programs, subsidies, and pilot funding have significantly reduced adoption risk, accelerating fleet replacement cycles. Additionally, fuel cell buses offer operational advantages in cold climates and high-duty-cycle environments, where battery-electric buses may face range or charging limitations. As transit agencies continue to modernize fleets and expand clean transportation initiatives, the bus segment is expected to maintain a leading position in the market.

The truck segment is poised to grow at a CAGR of 33.2%, showcasing the fastest growth over the analysis period.

By Application

Urban Transit Leads Due to Large-Scale Deployment of Fuel Cell Buses in City Transport Systems

Based on application, the market is classified into urban transit, urban delivery/last-mile, and others.

Urban transit dominates the application segment owing to the large-scale replacement of diesel buses in city transport systems. Public transit authorities are under increasing regulatory and social pressure to reduce emissions, noise, and air pollution in densely populated urban areas. Fuel cell buses are well-suited for fixed-route, high-frequency operations, offering fast refueling and consistent range without the downtime associated with battery charging. Government support, in the form of subsidies, public procurement programs, and pilot funding, has played a crucial role in accelerating adoption. As urbanization increases and cities expand, clean mobility initiatives are expected to support the segment’s largest share during the forecast period.

The others segment is poised to grow at a CAGR of 33.8%, showcasing the fastest growth over the analysis period.

To know how our report can help streamline your business, Speak to Analyst

By Power Output

<200 kW Power Output is Highly Preferred Driven by Widespread Adoption of Fuel Cell Buses and Urban Transit Fleets

Based on power output, the market is segmented into <200kW, 201-300kW and >300kW.

The <200 kW power output segment accounts for the largest market share driven by the widespread deployment of fuel cell buses and light- to medium-duty commercial vehicles. Most urban transit buses operate with fuel cell systems in this power range, as it provides sufficient energy for stop-and-go operations while optimizing system efficiency and cost. This segment benefits from early commercialization, standardized fuel cell modules, and extensive use in public transit fleets supported by government procurement programs. Additionally, vehicles in this power class typically require smaller hydrogen storage systems, reducing overall vehicle cost and complexity. As urban transit continues to lead fuel cell adoption globally, the <200 kW segment is expected to maintain a strong market position, particularly in regions with established bus deployment programs.

The segment exceeding 300kW is poised to grow at a CAGR of 34.2%, showcasing the fastest growth over the analysis period.

Fuel Cell Commercial Vehicle Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Fuel Cell Commercial Vehicle Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the largest and fastest-growing region driven by strong government support, large-scale manufacturing capabilities, and early commercialization. The region is characterized by a diversified application mix, with fuel cell buses and trucks both playing significant roles. China and South Korea have actively promoted hydrogen mobility through subsidies, fleet mandates, and infrastructure investments, thereby accelerating its adoption in public transit and heavy-duty freight. Asia Pacific is particularly advanced in fuel cell truck deployment, supported by growing demand for zero-emission logistics and industrial transport.

North America

North America represents an emerging yet strategically important market for fuel cell commercial vehicles, driven primarily by policy-led decarbonization efforts in public transit and freight transport. In the near term, market adoption has been dominated by fuel cell buses, supported by public transit funding, pilot programs, and zero-emission mandates at the state and municipal levels. However, the regional growth is increasingly shaped by medium and heavy-duty trucking applications. Government initiatives focused on zero-emission freight corridors and hydrogen infrastructure development are creating favorable conditions for the adoption of fuel cell trucks, particularly for long-haul and regional freight.

Europe

Europe is one of the most advanced regions in terms of fuel cell commercial vehicle deployment, with strong adoption in public transit systems. The market is currently dominated by fuel cell buses, driven by stringent emission regulations, urban air-quality goals, and large-scale public procurement programs. Several European countries have integrated hydrogen buses into their public transport networks as part of broader zero-emission mobility strategies.

Rest of the World

The rest of the world’s market is in its early stages of development, with fuel cell commercial vehicle adoption largely limited to pilot projects and initial demonstrations. Deployment has primarily focused on fuel cell buses in public transit systems, as governments and municipalities explore zero-emission transport solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

OEMs, Fuel Cell Technology Providers, and Fleet Integrators Strengthen Competition via Ecosystem Development and Early-mover Advantages

The fuel cell commercial vehicle market is shaped by a combination of global commercial vehicle OEMs, hydrogen-focused vehicle manufacturers, and fuel cell technology suppliers that are actively advancing fuel cell buses and trucks. Key players include Hyundai Motor Company, Toyota Motor Corporation, Daimler Truck, Volvo Group, Nikola Corporation, and major Chinese OEMs such as Foton, FAW Group, and Sinotruk. These companies are leveraging established manufacturing capabilities, strong balance sheets, and early-mover advantages to commercialize fuel cell vehicles across public transit and freight applications.

Market participants are increasingly strengthening competitiveness through strategic partnerships, pilot fleet deployments, and ecosystem development, rather than standalone vehicle sales. Collaborations between OEMs, hydrogen infrastructure developers, and fleet operators are enabling integrated solutions that combine vehicles, refueling access, maintenance, and performance monitoring. Companies are also investing in high-power fuel cell platforms, modular architectures, and digital fleet monitoring tools to improve vehicle reliability and total cost of ownership.

LIST OF KEY FUEL CELL COMMERCIAL VEHICLE COMPANIES PROFILED

- Hyundai Motor Company (South Korea)

- Toyota Motor Corporation (Japan)

- Ballard Power Systems Inc. (Canada)

- Nikola Corporation (S.)

- Beiqi Foton Motor Co., Ltd. (China)

- Hyzon Motors (U.S.)

- SAIC Iveco Hongyan (South)

- Sinotruk (China National Heavy Duty Truck Group) (China)

- FAW Group Corp., Ltd. (China)

- Dongfeng Motor Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Rutgers University's CAIT research center received a grant to test heavy-duty hydrogen fuel-cell trucks from Hyundai Motor Group. A USD 13 million grant will fund testing of six hydrogen fuel-cell-powered trucks at Port Newark starting in early 2026.

- October 2025: Yutong announced a deal to sell 500 hydrogen trucks to Zhengzhou Transportation Construction Investment (ZTCI), a state-owned entity in central China's Henan province, marking a significant move for hydrogen transport adoption in the region.

- May 2025: Hyundai Motor and Plus introduced autonomous hydrogen freight ecosystem concept. The collaboration aims to accelerate the development of a hydrogen-powered freight network in the U.S. and was unveiled in a concept film at the Advanced Clean Transportation (ACT) Expo 2025 in Anaheim, California.

- November 2023: Daimler AG delivered the first three of 48 fully electric eCitaro articulated buses with a 60 kW fuel cell as a range extender to Rhein-Neckar-Verkehr GmbH. It consists of NMC3 high-performance batteries and fuel cells that increase the range to 400 kilometers on one charge.

- August 2022: Nikkiso signed a contract for Hydrogen stations in South Korea and California. The stations will provide fuel for light-duty, heavy-duty, and transit fuel cell vehicles that need H35 and H70 dispensing.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 32.7% from 2025-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Application, Power Output, and Region |

|

By Vehicle Type |

· Bus · Trucks |

|

By Application |

· Urban Transit · Urban delivery / last-mile · Others |

|

By Power output |

· <200kW · 201-300kW · >300kW |

|

By Geography |

· North America (By Vehicle Type, By Application, By Power Output, and by Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Vehicle Type, By Application, By Power Output, and by Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o Netherlands (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Vehicle Type, By Application, By Power Output, and by Country) o China (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Vehicle Type, By Application, By Power Output, and by Country ) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.20 billion in 2025 and is projected to reach USD 38.87 billion by 2034.

In 2025, Asia Pacifics market value stood at USD 2.28 billion.

The market is expected to exhibit a CAGR of 32.7% during the forecast period.

The bus segment led the market based on vehicle type.

Government policy support and hydrogen strategies are key factors driving market growth.

Asia Pacific dominated the market by holding the largest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us