Glass Ceramics Market Size, Share & Industry Analysis, By Material Type (Lithium Aluminosilicate (LAS), Zinc Aluminosilicate (ZAS), Magnesium Aluminosilicate (MAS), and Others), By Application (Household Appliances, Building & Construction, Electrical & Electronics, Healthcare & Medical, Industrial Equipment, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

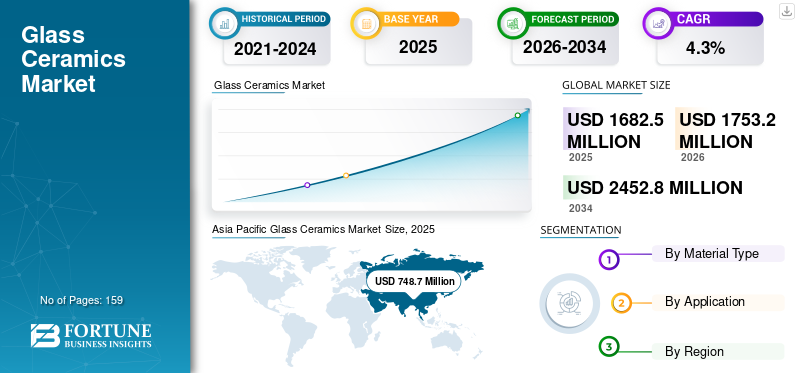

The global glass ceramics market size was valued at USD 1,682.5 million in 2025. The market is projected to grow from USD 1,753.2 million in 2026 to USD 2,452.8 million by 2034, exhibiting a CAGR of 4.3% during the forecast period. Asia Pacific dominated the glass ceramics market with a market share of 44.5% in 2025.

Glass ceramics are engineered materials produced by controlled crystallization of a parent glass, resulting in a microstructure that combines glass-like formability with ceramic-like performance. They are valued for near-zero or low thermal expansion, high thermal shock resistance, mechanical durability, and application-specific optical and electrical properties. Glass ceramics are generally employed across end-uses including household appliances (cooktops and oven components), building and construction (fireplace panels and heat-resistant glazing), electrical and electronics (substrates and protective housings), healthcare and dental (CAD/CAM restorations), and industrial and aerospace systems requiring high-temperature stability.

The growth of the glass ceramics market is driven by steady replacement demand for cooktops and heat-resistant panels, rising adoption of precision electronic packaging and protective components, and sustained demand from healthcare and dental restoration workflows. In parallel, product innovation focused on thinner, tougher, and more functional glass-ceramic panels is improving design flexibility for appliance and electronics OEMs.

The market comprises several major players, including SCHOTT, Corning Incorporated, Nippon Electric Glass Co., Ltd., EuroKera, and Ohara Inc. A broad portfolio, continuous material innovation, and multi-region manufacturing footprints support competitive positioning in this market.

Download Free sample to learn more about this report.

GLASS CERAMICS MARKET TRENDS:

Advances in Electronics and Semiconductor Packaging Boost Market Trends

Glass-ceramic demand continues to be anchored by the electrification of cooking and the premiumization of kitchen appliances, where low thermal expansion and high thermal shock resistance enable durable, flat, and aesthetically consistent cooking surfaces. At the same time, advances in electronics and semiconductor packaging are increasing interest in glass-ceramic substrates and core materials that support larger panel formats and improved dimensional stability under thermal cycling conditions. Sustainability considerations are also shaping procurement decisions, as manufacturers prioritize lower-emission production processes, improved recyclability that extends service life, reduce breakage, and improve energy efficiency in use.

- For instance, in March 2025, Corning introduced Corning Gorilla Glass Ceramic, positioned as a tough, transparent, and strengthenable glass-ceramic cover material for mobile devices to improve drop performance on rough surfaces.

- In January 2025, Nippon Electric Glass announced the development of a large-panel glass-ceramic core substrate (GC Core) for next-generation semiconductor packages requiring a larger substrate size and structural stability.

MARKET DYNAMICS

MARKET DRIVERS:

Thermal Shock Performance Properties are Supporting Glass-Ceramics Adoption

Glass-ceramics remain one of the most proven material solutions for applications requiring a combination of low thermal expansion, heat resistance, and mechanical robustness. In household appliances, this translates into reliable performance for cooktop panels, where repeated heating and cooling cycles demand thermal shock tolerance and long-term dimensional stability. In construction and industrial systems, heat-resistant viewing panels and fireplace applications contribute to stable base demand. In electronics, tougher glass-ceramic cover and protection solutions are expanding use-cases in devices that require improved durability without sacrificing optical clarity.

- For instance, SCHOTT’s CERAN portfolio highlights continuous innovation in glass-ceramic cooktop panels and global production footprints to serve appliance OEM requirements effectively and at scale.

MARKET RESTRAINTS:

Limiting Rapid Supplier Switching to Restrict Market Expansion

Glass-ceramic manufacturing requires precise melting, forming, and controlled ceramization steps, all of which require tight temperature control, making production energy-intensive and capital-demanding. End users often enforce strict tolerance requirements for optical properties, surface quality, and thermal expansion, increasing product qualification requirements and limiting rapid supplier switching. In certain applications, alternative engineered materials (advanced ceramics, tempered specialty glass, or coated glass systems) can compete effectively on cost, lead time, or performance fit, particularly within midrange product segments.

MARKET OPPORTUNITIES:

Rising Demand For Premium Glass-Ceramic Panels to Create Lucrative Growth Opportunities

Increasing adoption of induction and electric cooktops continues to support ongoing demand for premium glass-ceramic panels, especially as appliance OEMs pursue thinner designs, integrated displays, and differentiated aesthetics. In advanced packaging, glass-ceramic core substrates offer potential benefits in panel-size scalability and dimensional stability, creating opportunities for suppliers serving semiconductor ecosystem roadmaps. In healthcare applications, glass-ceramic dental blocks and restorative materials benefit from predictable machining workflows and increasing uptake of digital dentistry, supporting steady, higher-margin growth within specialized segments.

- For example, NEG’s GC Core development illustrates industry movement toward glass-ceramic substrates designed to accommodate larger, next-generation semiconductor package formats.

MARKET CHALLENGES:

Cost Pressure in Consumer Appliances to Hamper Market Growth

While baseline demand is stable, volumes can fluctuate in response to macro conditions affecting consumer appliance spending and construction cycles. In the cooktops segment, OEMs facing cost pressures during economic downturns may shift product mixes toward lower-cost alternatives, thereby constraining premium panel growth. In electronics and medical uses, qualification and reliability testing can be extensive, increasing time-to-revenue for new materials and creating execution risk for capacity additions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material Type

Lithium Aluminosilicate (LAS) Segment Dominated due to itsNear-Zero Thermal Expansion

Based on material type, the market is segmented into lithium aluminosilicate (LAS), zinc aluminosilicate (ZAS), magnesium aluminosilicate (MAS), and others.

The lithium aluminosilicate (LAS) segment accounted for the largest glass ceramics market share in 2025. The segment is driven by its near-zero thermal expansion and high thermal shock resistance, which are critical in household appliances and heat-resistant building applications. Furthermore, the segment held a 61.1% share in 2025.

The growth of the zinc aluminosilicate (ZAS) segment is supported by electronics and specialty technical components, where mechanical strength and tailored properties are valued. The zinc aluminosilicate (ZAS) segment is projected to grow at a 4.2% CAGR during the study period.

The magnesium aluminosilicate (MAS) segment is expected to grow favorably throughout the forecast period, driven by industrial components requiring durability and moderate-to-high temperature stability.

By Application

Household Appliances Segment Dominates the Market Due to the Extensive Use of the Product

By application, the market is categorized into household appliances, building & construction, electrical & electronics, healthcare & medical, industrial equipment, aerospace & defense, and others.

The household appliances segment accounted for the largest share in 2025, due to large-scale use of glass-ceramic panels in induction and radiant cooktops, and stable replacement demand in mature markets. Furthermore, the segment held a 32.8% share in 2025.

The building & construction segment is expected to grow at a CAGR of 4.5% over the forecast period. The segment's growth is supported by fireplace panels and heat-resistant glazing.

The electrical & electronics segment is expected to experience favorable growth throughout the forecast period, driven by protective covers and substrate applications in high-value electronics and packaging.

To know how our report can help streamline your business, Speak to Analyst

Glass Ceramics Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Glass Ceramics Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 748.7 million, and is expected to maintain the leading share in 2026, with USD 784.7 million. The region benefits from strong appliance manufacturing ecosystems, expanding electronics and semiconductor supply chains, and increasing adoption of premium cooking solutions in urban markets. China remains the largest consumer base, while Japan and South Korea contribute significantly through specialty materials and high-precision electronics applications.

China Glass Ceramics Market

In 2025, the China market reached USD 357.9 million, supported by high appliance manufacturing throughput and rising domestic consumption of induction cooktops and premium kitchen products.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 323.9 million by 2026. The market’s growth is supported by stable appliance replacement demand, industrial high-temperature applications, and specialty materials innovation. The U.S. accounts for the majority of regional consumption through consumer appliance demand and electronics-related end uses.

U.S. Glass Ceramics Market

In 2025, the U.S. market is estimated to reach USD 267.6 million. The market is driven by replacement and upgrade demand for induction/electric cooktops and other premium appliances that rely on low-thermal-expansion, thermal-shock-resistant glass-ceramic panels.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the region is projected to grow at a CAGR of 4.4% and reach a valuation of USD 475.6 million in 2026. The glass ceramics market growth is driven by established specialty glass and glass-ceramic manufacturing capabilities, strong demand for fireplace and heat-resistant architectural applications, and continued innovation in appliance design. Germany remains a key manufacturing and technology hub.

U.K. Glass Ceramics Market

The U.K. market in 2025 reached around USD 43.3 million, representing approximately 3.7% of global market revenue.

Germany Glass Ceramics Market

Germany’s market reached approximately USD 140.0 million in 2025, equivalent to around 4.6% of global sales.

Latin America

Latin America is experiencing steady growth and is expected to reach a valuation of USD 88.1 million in 2026. The demand in the region is tied to appliance penetration, renovation activity, and selective industrial uses.

The Middle East & Africa

The Middle East and Africa region is gradually expanding, with sales recorded at USD 27.9 million in 2025. The growth of the market is driven by construction-led demand for heat-resistant panels and increasing adoption of premium appliances in the GCC. Limited local manufacturing capacity in several countries increases reliance on imports and regional distribution networks.

GCC Glass Ceramics Market

GCC reached USD 34.3 million in 2025, accounting for approximately 2.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players:

Key Players are Focusing on Sustainability Efforts to Maintain Their Position in the Market

Competition is shaped by material science capabilities, tight process control across melting and ceramization, surface finishing know-how, and long-term OEM qualifications. Leading suppliers differentiate through proprietary formulations (low expansion, improved toughness, optical tuning), multi-region manufacturing footprints, and technical support for appliance and electronics design-in cycles. Some of the key market players include SCHOTT, Corning Incorporated, Nippon Electric Glass Co., Ltd., EuroKera , and Ohara Inc. Sustainability efforts, including energy efficiency and lower-emission manufacturing pathways, are increasingly influencing procurement and supplier selection.

LIST OF KEY GLASS CERAMICS COMPANIES PROFILED:

- SCHOTT (Germany)

- Corning Incorporated (U.S.)

- Nippon Electric Glass Co., Ltd. (Japan)

- EuroKera (France)

- Ohara Inc. (Japan)

- AGC Inc. (Japan)

- Precision Ceramics Limited (U.K.)

- Ortech, inc. (U.S.)

- Morgan Advanced Materials (U.K.)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: SCHOTT announced serial production of the CERAN matte line for glass-ceramic cooktops, signalling commercial scale-up of matte “design trend” surfaces with functional benefits such as reduced visible scratches/fingerprints.

- March 2025: Corning launched Corning Gorilla Glass Ceramic as a transparent, strengthenable glass-ceramic cover material for mobile devices, signalling new growth headroom for glass-ceramics beyond cooktops into consumer electronics durability applications.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.3% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Material Type, Application, and Region |

|

By Material Type |

· Lithium Aluminosilicate (LAS) · Zinc Aluminosilicate (ZAS) · Magnesium Aluminosilicate (MAS) · Others |

|

By Application |

· Household Appliances · Building & Construction · Electrical & Electronics · Healthcare & Medical · Industrial Equipment · Aerospace & Defense · Others |

|

By Geography |

· North America (By Material Type, Application, and Country) o U.S. (By Application) o Canada (By Application) · Europe (By Material Type, Application, and Country/Sub-region) o Germany (By Application) o France (By Application) o Italy (By Application) o U.K. (By Application) o Rest of Europe (By Application) · Asia Pacific (By Material Type, Application, and Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Material Type, Application, and Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Material Type, Application, and Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 1,682.5 million in 2025 and is projected to reach USD 2,452.8 million by 2034.

Recording a CAGR of 4.3%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

The household appliances segment led the market in 2025 by application.

Asia Pacific held the highest market share in 2025.

SCHOTT, Corning Incorporated, Nippon Electric Glass Co., Ltd., EuroKera, and Ohara Inc. are some of the top players in the market.

The key factor driving the market is the rising adoption of glass-ceramic panels in household appliances, especially induction and electric cooktops.

- 2021-2034

- 2025

- 2021-2024

- 159

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us