Glaucoma Surgery Devices Market Size, Share & Industry Analysis, By Device Type (Glaucoma Drainage Devices, Minimally Invasive Surgery Devices, Traditional Surgery Devices & Consumables, Laser Systems, and Others), By Procedure Type (Traditional Surgery, Minimally Invasive Surgery, and Laser Surgery), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Glaucoma Surgery Devices Market Size and Future Outlook

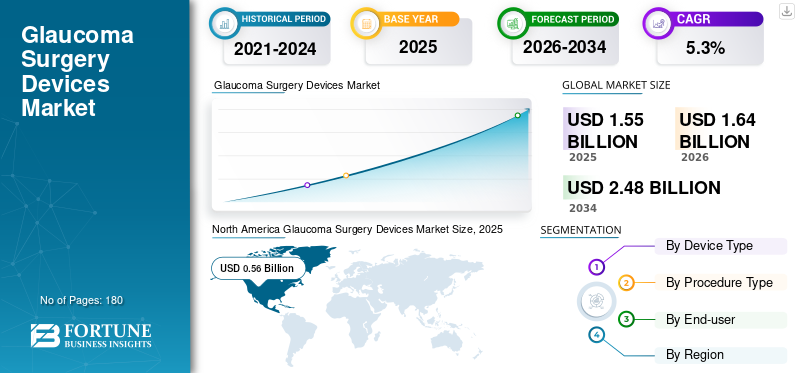

The global glaucoma surgery devices market size was valued at USD 1.55 billion in 2025. The market is projected to grow from USD 1.64 billion in 2026 to USD 2.48 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. North America dominated the global market with a market share of 36.13% in 2025.

Glaucoma surgery devices are used to lower intraocular pressure (IOP) when medicines or laser treatment are insufficient. These devices include conventional drainage implants and filtration devices, newer implants, Minimally Invasive Glaucoma Surgery (MIGS) systems, and procedure-enabling tools. The growth is supported by the rising glaucoma burden, aging populations, earlier diagnosis, and the need for safer, lower-burden interventions.

Furthermore, Glaukos Corporation, Alcon, and Iridex Corporation held the highest market share in 2025 due to their strong brand reputations and broad product portfolios.

Download Free sample to learn more about this report.

GLAUCOMA SURGERY DEVICES MARKET TRENDS

Growth of Implantable and New Laser-Based Technologies Platforms to Emerge as a Key Trend

Currently, key players are focusing on the design of sustained-release intracameral implants to reduce dependence on daily topical drops and improve adherence. Moreover, laser-based approaches are evolving beyond traditional laser trabeculoplasty, with an increasing shift toward energy-based, visualization-guided glaucoma surgery. These developments have increased the demand for glaucoma surgery in patients with primary open angle glaucoma.

- For instance, in April 2025, BVI Medical announced FDA 510(k) clearance for Leos, a laser endoscopy ophthalmic system for glaucoma surgery. The system is designed for minimally invasive ab interno endoscopic cyclophotocoagulation and combines laser treatment with endoscopic visualization.

This trend is further supported by surgeons who are increasingly using enhanced visualization to improve the precision of angle-based surgery.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Cases of Glaucoma to Fuel Market Expansion

Over the past few years, there has been an increasing number of glaucoma cases globally, of which a significant proportion require surgical intervention. This prevalence is further fueled by aging populations and diabetes prevalence, increasing demand for surgical interventions including Minimally Invasive Glaucoma Surgery (MIGS) devices. Such a scenario is anticipated to drive the global glaucoma surgery devices market growth during the forecast period.

- For instance, in May 2024, the Centers for Disease Control and Prevention (CDC) reported that over 3.0 million Americans have glaucoma, with projections showing a rise to 6.3 million cases by 2050, driven by the aging U.S. population.

MARKET RESTRAINTS

High Procedural Costs to Restrict Market Growth

Despite significant demand for glaucoma surgery and adoption of related devices, the advanced glaucoma interventions, especially Minimally Invasive Glaucoma Surgery (MIGS), which involve expensive implants, specialized surgical tools, and trained ophthalmic surgeons, significantly increase overall treatment costs compared to conventional drug therapy.

- For instance, in April 2025, NVISION Eye Centers stated that laser glaucoma procedures typically cost between USD 1,000 and USD 2,000, while incisional surgeries average around USD 11,000 in the U.S.

Additionally, follow-up care, postoperative monitoring, and the potential need for repeat procedures further increase the financial burden on patients and healthcare systems, which is anticipated to hamper the market growth.

MARKET OPPORTUNITIES

Shift Toward Safer and Less Invasive Interventional Glaucoma Care to Present Significant Growth Opportunities

In recent years, there has been an increasing adoption of minimally invasive procedures for glaucoma as these procedures offer reduced surgical trauma, shorter recovery times, and improved safety profiles compared to traditional glaucoma surgeries. This has made them highly attractive for both patients and ophthalmic surgeons. Such a scenario is expected to present significant opportunities for key companies to capitalize on this shift through continuous innovation.

- For instance, in August 2023, NVISION Eye Centers stated that MIGS offers alternative glaucoma surgical options with lower risks than traditional surgeries.

MARKET CHALLENGES

Shortage of Surgeons to Challenge Market Expansion

Despite the rising demand for glaucoma surgeries, their volume is limited by a shortage of key professionals and limited training with advanced devices. Glaucoma surgeries, especially MIGS, require specialized training, precision, and familiarity with evolving device technologies. This is further expected to delay the number of glaucoma surgeries, especially in emerging markets and rural areas. This is expected to challenge market growth in the coming years.

- For instance, a survey by AIIMS Delhi revealed that there is only one ophthalmologist available for every 65,000 people in India.

Segmentation Analysis

By Device Type

Higher Surgeon Preference for Minimally Invasive Surgery Devices to Boost Segment Growth

Based on device type, the market is segmented into glaucoma drainage devices, minimally invasive surgery devices, traditional surgery devices & consumables, laser systems, and others.

To know how our report can help streamline your business, Speak to Analyst

The minimally invasive surgery devices segment accounted for the largest glaucoma surgery devices market share in 2025. The segment’s growth is attributed to surgeons' preference for treating mild-to-moderate primary open-angle glaucoma with minimally invasive surgical devices due to better safety, faster recovery, and greater compatibility.

Additionally, the laser systems segment is projected to grow at a 4.7% CAGR during the forecast period.

By Procedure Type

Introduction of New Devices to Fuel the Minimally Invasive Surgery Segment’s Growth

By procedure type, the market is classified into traditional surgery, minimally invasive surgery, and laser surgery.

The minimally invasive surgery segment accounted for the largest market share in 2025. Minimally invasive surgery fills the gap between medication/laser therapy and traditional filtration surgery, prompting key players to introduce relatable devices, driving their penetration rates in these segments. Moreover, the segment is projected to hold a 39.5% share in 2026.

Additionally, the laser surgery segment is expected to grow at a 4.8% CAGR during the forecast period.

By End-user

Large Number of Hospitals in Developed Countries to Propel the Segment’s Growth

On the basis of end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

In 2025, hospitals & ASCs segment dominated the market. The growth is attributed to the high volume of glaucoma surgeries in these settings, driven by the availability of expertise and advanced equipment. Moreover, the large number of hospitals in the developed countries is favoring the adoption of glaucoma surgery devices, further driving the segment’s growth. This is expected to fuel the segment’s growth. Furthermore, the segment is set to hold 66.4% share in 2026.

- For instance, as of early 2026, the American Hospital Association (AHA) Fast Facts report indicated that there are 6,100 hospitals across the U.S.

In addition, the specialty clinics segment is projected to grow at a 6.7% CAGR over the forecast period.

Glaucoma Surgery Devices Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Glaucoma Surgery Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.53 billion, and also led in 2025 with a valuation of USD 0.56 billion. The growth is driven by advanced healthcare infrastructure and a large number of glaucoma procedures, supported by strong reimbursement frameworks, favorable regulatory approvals, and early commercialization of novel devices.

- For instance, according to data from the Association for Research in Vision and Ophthalmology, the total number of glaucoma surgeries surged by 176.66%, rising from 80,151 procedures in 2011 to 221,602 in 2021.

U.S. Glaucoma Surgery Devices Market

In 2026, the U.S. is anticipated to reach USD 0.51 billion, accounting for approximately 31.1% of the global market.

Europe

Europe is projected to record a 4.3% growth rate during the forecast period, the second-highest globally, reaching USD 0.48 billion by 2026. The growth is attributed to high glaucoma screening rates and a large number of ophthalmologists in Germany, the U.K., and France.

U.K. Glaucoma Surgery Devices Market

The U.K. market is projected to reach USD 0.09 billion by 2026, representing approximately 5.4% of global revenues.

Germany Glaucoma Surgery Devices Market

Germany's market is expected to reach around USD 0.10 billion by 2026, accounting for approximately 6.3% of global revenue.

Asia Pacific

By 2026, Asia Pacific’s market is projected to reach approximately USD 0.39 billion, making it the third-largest market globally. The growth is driven by a large patient pool, rising healthcare investments, and improving access to ophthalmic care, which is projected to fuel the adoption of glaucoma surgery devices.

Japan Glaucoma Surgery Devices Market

Japan is projected to generate approximately USD 0.09 billion in revenue by 2026, representing nearly 5.7% of the global market.

China Glaucoma Surgery Devices Market

China’s market is anticipated to reach around USD 0.12 billion by 2026, accounting for nearly 7.6% of global revenues.

India Glaucoma Surgery Devices Market

The Indian market is expected to reach approximately USD 0.06 billion by 2026, accounting for around 3.6% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate growth, with the Latin America market estimated to reach approximately USD 0.10 billion by 2026. The growth is attributed to rising awareness about glaucoma-related blindness and steady adoption of advanced surgical techniques in these regions.

GCC Glaucoma Surgery Devices Market

By 2026, the GCC market is estimated to reach approximately USD 0.04 billion, representing around 2.7% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Higher Focus on Product Innovation and Portfolio Expansion to Strengthen Market Foothold of Major Players

In 2025, Glaukos Corporation, Alcon, and Iridex Corporation held the largest global market share for glaucoma surgery devices. This share is attributed to a higher focus on product innovation, portfolio expansion, and strategic partnerships globally.

Moreover, other emerging players and niche manufacturers are also benefiting from broad global distribution and established surgeon relationships. Also, they are strengthening their footprint through acquisitions, which are expected to increase their market share over the forecast period.

LIST OF KEY GLAUCOMA SURGERY DEVICES COMPANIES PROFILED IN REPORT

- Glaukos Corporation (U.S.)

- Alcon (Switzerland)

- New World Medical (U.S.)

- AbbVie (U.S.)

- Iridex Corporation (U.S.)

- Lumenis Be Ltd. (Israel)

- MicroSurgical Technology (U.S.)

- LIGHTMED (U.S.)

- BVI (U.S.)

- Lumibird Medical (France)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Sight Sciences announced the debut of the OMNI Edge Surgical System at ASCRS 2025, expanding the OMNI product portfolio with higher viscoelastic capacity and TruSync technology.

- May 2024: New World Medical received 510(k) clearance for expanded indication of KDB GLIDE, including use as a standalone procedure for POAG.

- April 2024: Glaukos Corporation received a permanent CMS J-code for iDose TR, improving reimbursement clarity and supporting U.S. access.

- April 2024: Sight Sciences announced the publication of a large-scale real-world MIGS study showing OMNI’s effectiveness at lowering IOP and medication use over two years in more than 100,000 eyes.

- December 2023: Glaukos Corporation received FDA approval for iDose TR, a travoprost intracameral implant for the reduction of intraocular pressure (IOP) in patients with ocular hypertension (OHT) or open-angle glaucoma (OAG).

- April 2022: Alcon acquired Ivantis Inc., adding the Hydrus Microstent to its global surgical portfolio.

- May 2021: Glaukos Corporation expanded its PRESERFLO MicroShunt relationship with Santen through a new development and commercialization license agreement covering the U.S. and other markets.

REPORT COVERAGE

The glaucoma surgery devices market report offers an in-depth evaluation of all market segments, emphasizing key growth drivers, emerging trends, potential opportunities, and major restraints and challenges influencing overall market dynamics. It further examines advanced technological innovations, the prevalence of glaucoma, and the number of key procedures, notable industry developments, reimbursement scenarios, market share analysis, and detailed profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Device Type, Procedure Type, End-user, and Region |

| By Device Type |

|

| By Procedure Type |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.55 billion in 2025 and is projected to reach USD 2.48 billion by 2034.

In 2025, North Americas market value stood at USD 0.56 billion.

The market is expected to exhibit a CAGR of 5.3% during the forecast period of 2026-2034.

The minimally invasive surgery devices segment led the market by device type.

The key factor driving the market is the rising number of glaucoma cases globally.

Glaukos Corporation, Alcon, and Iridex Corporation are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us