Golf Simulator Market Size, Share & Industry Analysis, By Offering (Simulator Hardware, Simulator Software, and Simulator Services), By Product Type (Portable and Built-in), By Simulator Type (Full Swing Simulators and Virtual Reality (VR) Golf), By Business Model (Built-in and Subscription-based), By End-user (Commercial, Residential/Amateur, and Educational Institutes), and Regional Forecast Report, 2026-2034

KEY MARKET INSIGHTS

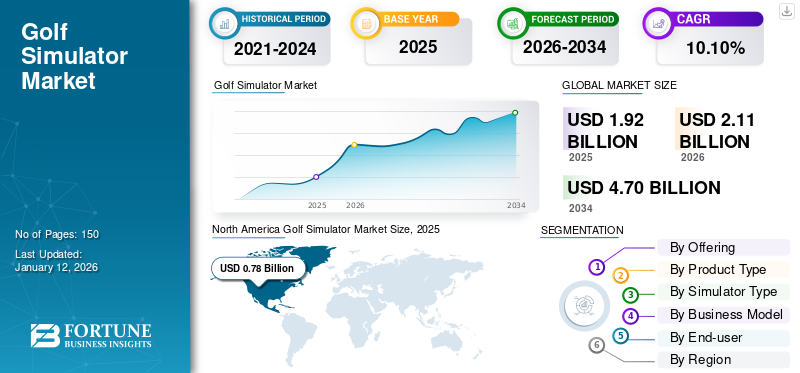

The global golf simulator market size was valued at USD 1.92 billion in 2025 and is projected to grow from USD 2.11 billion in 2026 to USD 4.7 billion by 2034, exhibiting a CAGR of 10.10% during the forecast period. North America dominated the golf simulator market with a share of 40.70% in 2025.

- The global golf simulator market is projected to grow rapidly from about $1.92 billion in 2025 to around $4.7 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 10.10% over the forecast period.

- Growth is driven by rising demand for indoor golf experiences, technological enhancements such as VR/AR and AI integration, and increasing usage across commercial, residential, and training settings.

- North America currently dominates the market, holding the largest regional share (40.70% in 2025), supported by strong recreational participation and established simulation providers, while the Asia Pacific region is expected to grow fastest due to rising urban leisure spending and technology adoption.

- Hardware systems, portable simulators, and built-in commercial installations are key segments leading market revenue, with portable systems gaining traction due to affordability and ease of setup.

The global golf simulator market has transitioned from niche recreational technology into a structured performance training and commercial entertainment ecosystem. Growth is driven by increasing demand for year-round playability, data-driven swing analytics, and premium experiential venues. While historically concentrated in high-income markets, geographic expansion and declining hardware costs are broadening addressable demand. The golf simulator market size continues to expand as commercial operators, training academies, and residential buyers adopt integrated digital golf platforms.

The industry ecosystem includes hardware manufacturers (launch monitors, impact screens, projectors), software developers (simulation engines, analytics platforms), installation service providers, and subscription-based content operators. Value capture is increasingly shifting toward recurring software and service revenue rather than one-time equipment sales. This evolution is influencing long-term golf simulator market share distribution among integrated platform providers.

Golf simulator market trends indicate increasing integration of high-speed cameras, radar tracking, and artificial intelligence-based swing analysis. Enterprises are investing in immersive experiences to enhance customer dwell time and monetization efficiency. The commercial segment, particularly indoor golf lounges and hospitality venues, is reshaping revenue concentration patterns.

Golf simulator market growth will depend on continued sensor accuracy improvement, content expansion, and affordability optimization. Competitive advantage will increasingly favor firms capable of combining hardware precision, software scalability, and recurring service models within a consolidated digital ecosystem.

A golf simulator is an advanced system that replicates real-world golf environments through a combination of hardware and software technologies, enabling users to play and practice golf indoors. These systems use high-speed cameras, radar, and sensors integrated with interactive software to mimic the experience of playing on actual golf courses. They cater to a wide range of users, from amateurs to professionals across residential, commercial, and institutional settings.

The market comprises major companies, including Panasonic Corporation, E6 Connect (TrueGolf), Foresight Sport, Full Swing Golf, Golfzon, SKYTRAK, TruGolf, OptiShot Golf, Vgolf, and TrackMan, among others.

Download Free sample to learn more about this report.

Golf Simulator Market Key Takeaways

- 2025 Market Size: USD 1.92 billion

- 2026 Market Size: USD 2.11 billion

- 2034 Forecast Market Size: USD 4.70 billion

- CAGR: 10.10% from 2026–2034

- North America dominated the market with a 40.70% share in 2025.

- The Simulator Hardware segment is projected to lead the market with a 52.07% share in 2026.

- The Portable Simulators segment is expected to dominate with a 64.37% share in 2026.

Asia Pacific

Asia Pacific recorded USD 0.37 billion in 2025 and is expected to grow to USD 0.41 billion in 2026.

North America

North America reached USD 0.78 billion in 2025 and is projected to grow to USD 0.85 billion in 2026.

Europe

Europe generated USD 0.56 billion in 2025 and is projected to reach USD 0.61 billion in 2026.

U.S.

U.S. market is projected to reach USD 0.50 billion by 2026.

Japan

Japan market is projected to reach USD 0.10 billion by 2026.

Read More

IMPACT OF ARTIFICIAL INTELLIGENCE (AI)

Artificial Intelligence (AI) is transforming the market by enhancing the precision and personalization of gameplay. AI-powered swing analysis systems use machine learning algorithms to evaluate player performance in real time and provide personalized feedback. This allows users to improve their skills more efficiently, making simulated golf more engaging to amateurs and professionals. For instance,

- In May 2025, IdeasLab launched XView AI, a markerless app that provides real-time, offline analysis of the full golf swing by tracking body, shaft, and club movement. This app is available on the iPhone App Store.

AI integration is streamlining the software experience by automating course recommendations, adapting difficulty levels, and personalizing virtual environments based on users' skill levels. These intelligent features increase user engagement and extend session durations, boosting the overall usage of simulators. Therefore, simulator manufacturers are increasingly adopting AI-driven interfaces to differentiate their offerings in a competitive market. For instance,

- In April 2025, TruGolf and Digital Legends announced a partnership to launch an advanced golf simulator experience. It is built on TruGolf's Apex platform, featuring AI-driven recreations of legendary players such as Ben Hogan. The simulator will enable users to compete with historic golf figures, receive AI-powered coaching, and engage in golf tournaments on modern courses.

Market Trends:

Growing Adoption of Virtual Reality and Augmented Reality to Propel Market Growth

In the dynamic landscape of golf simulation, the convergence of innovative technologies is opening new borders for gaming enthusiasts. One such groundbreaking trend is the integration of Augmented Reality (AR) and Virtual Reality (VR) with golf simulators, offering an unequaled experience.

One of the transformative parts of AR in golf simulators is its capability to visualize difficult data in real time. With AR and VR technology, users can view immediate feedback on clubhead speed and swing mechanics seamlessly within the user’s field of view. AR technology improves the visualization of performance data, providing a detailed analysis of every swing.

Companies in the market are integrating AR and VR technology in their product line to enhance gamers' experience. For instance,

- In February 2025, Golfjoy Limited announced the integration of the launch monitor and simulator with Virtual Reality (VR) and Augmented Reality (AR) technology. By wearing a virtual reality headset, players can effectively transport themselves to some of the greatest courses in the world.

Thus, the growing adoption of AR and VR can offer numerous advancements that will contribute to the growth of the golf simulator market.

Golf simulator market trends indicate a transition from hardware-centric differentiation toward integrated ecosystem strategies. Vendors are increasingly bundling launch monitors, simulation engines, cloud analytics, and subscription content into unified platforms. This approach enhances customer retention and recurring revenue stability. Immersive realism remains a central innovation theme. Advances in photorealistic rendering, 4K projection systems, and real-time ball flight modeling have narrowed the experiential gap between indoor and outdoor play. Improved haptic feedback surfaces and impact screen durability further enhance engagement.

Artificial intelligence-driven swing diagnostics is emerging as a competitive differentiator. Systems now offer automated club path analysis, shot dispersion mapping, and skill progression tracking. These features strengthen value propositions for coaching academies and serious amateur players. Commercial venue models are also evolving. Operators increasingly combine golf simulation with food and beverage service, event hosting, and corporate entertainment packages. This hybrid entertainment format enhances revenue per square foot and stabilizes utilization rates.

Download Free sample to learn more about this report.

Key Market Dynamics

Market Drivers

Rising Number of Golf Courses to Drive the Growth of Golf Simulators

People are progressively seeking more practical training methods, including golf simulation. The major growth in the expansion of new golf courses is one of the main factors that motivates the popularity of golf simulation processes. Owing to the increase in the participation of individuals, the number of planning and construction projects will increase. This scenario is helping to improve the golf simulator market share. For instance,

As per the Global Golf Participation 2024 Survey,

- 0.0082 billion registered golfers are officially part of the sport.

- An additional 0.03 billion unregistered 9 & 18-hole golfers actively engage in casual play.

- A total of 0.062 billion adults worldwide are engaged with golf in some capacity.

- There has been a 10% rise in registered golfers since 2020, showing growth and increasing interest in the sport.

- There are currently 21,507 golf courses in R&A-affiliated nations worldwide.

The primary driver of the golf simulator market growth is the demand for year-round accessibility independent of weather or course availability. Traditional golf participation is constrained by climate seasonality and land availability. Indoor simulation removes these barriers, expanding playable hours and geographic reach. Performance analytics is another structural catalyst. Advanced launch monitors, high-speed cameras, and radar-based tracking systems provide measurable swing data. Amateur and professional players increasingly rely on data-driven training tools. This shift toward quantified performance strengthens premium hardware and software adoption.

Commercial venue expansion also fuels the growth of the golf simulator market. Indoor golf lounges, hospitality venues, and entertainment complexes are integrating simulators to increase customer dwell time and per-visit revenue. These venues operate on high utilization models, justifying capital expenditure through diversified income streams including food, beverage, and event hosting. Urbanization supports demand where access to traditional courses is limited. Simulators allow compact footprint installations in metropolitan locations. Corporate entertainment and team-building use cases further enhance commercial viability.

Additionally, as the number of golf courses increases, more individuals are being exposed to the sport, which leads to greater participation in golf-related products. Golf simulators are becoming crucial tools for both recreation and training as golfers seek ways to enhance their game in urban areas or during the off-season when outdoor space is limited.

The growing number of golf courses and golf engagement by individuals drives the growth of the golf simulator market.

Market Restraints

High Initial Investment in Golf Restricts Market Growth

The high initial investment needed to set up a golf simulation system is still one of the main challenges that limit the application of common golf simulation processes, especially in some market segments. While golf simulation provides role-based experience to help golf players improve their skills, equipment, software, and installation costs may be prohibitively high for some potential users, limiting market growth in some regions and fields. Thus, the high initial cost of such systems limits adoption in high-tech golf clubs, commercial training centers, and luxury home installations, restricting the broader growth of the market.

Despite positive growth momentum, capital intensity remains a primary constraint within the golf simulator market. High-accuracy launch monitors, impact screens, and projection systems require meaningful upfront investment. Commercial buyers typically allocate significant budgets for build-out, limiting participation to financially stable operators.

Space requirements also restrict adoption. Built-in systems demand ceiling height, swing clearance, and dedicated room dimensions. Residential buyers in dense urban markets often face physical limitations that constrain installation feasibility. Technology obsolescence risk presents another restraint. Rapid sensor innovation may shorten hardware replacement cycles. Enterprises evaluating return-on-investment models must consider depreciation and upgrade frequency.

Market Opportunities

Portable Golf Simulators Gaining Traction among Younger Audiences, Leading to Lucrative Market Opportunities

Portable simulators are generally more affordable and require less space compared to traditional setups. This makes them an attractive option for younger individuals, including students and young professionals, who may have limited space or budget for a full-scale golf setup. Portable simulators are becoming more appealing to younger generations who may not have the time or inclination to visit a traditional golf course. This demographic is particularly interested in technology-driven leisure and fitness activities.

Younger generations are increasingly adopting golf as a sport, and portable simulators are an appealing option for these tech-savvy, budget-conscious, and space-limited individuals. For instance,

- In Australia, venues such as X-Golf and Big Swing Golf have reported that a major portion of their clientele is aged between 25 and 40, highlighting the appeal of simulators to younger players.

- According to the National Golf Foundation, nearly 6 million individuals in the 18-34 age group are actively participating in golf.

Thus, the growing adoption of these portable simulators among younger demographics is creating significant opportunities in the golf industry.

Significant golf simulator market growth opportunities exist within commercial hospitality and leisure segments. Urban indoor golf lounges are expanding in high-income metropolitan markets, driven by experiential entertainment demand. Operators targeting corporate events and group bookings benefit from predictable revenue streams. Franchise models represent an emerging expansion pathway. Standardized simulator installations combined with centralized software management enable scalable replication across regions. This structure supports accelerated golf simulator market size expansion while maintaining operational consistency.

Educational institutions also present opportunities. Universities and sports academies increasingly integrate simulators for structured training programs. Data analytics capabilities strengthen recruitment and athlete development frameworks. Emerging markets offer long-term upside potential. Rising middle-class participation in golf and limited access to traditional courses create favorable conditions for indoor alternatives. As hardware costs decline, price accessibility will improve.

Subscription-based business models provide recurring revenue potential. Content updates, performance analytics packages, and virtual tournament access encourage ongoing engagement beyond initial hardware purchase. Corporate wellness programs may represent another growth channel. Enterprises investing in employee engagement amenities are exploring simulator installations within office campuses.

SEGMENTATION ANALYSIS

By Offering

Increasing adoption Among Commercial Facilities and Professional Users to drive the Simulator Hardware Segment

Based on offering, the market is divided into simulator hardware, simulator software, and simulator services.

Simulator Hardware

Simulator hardware segment will account for 52.07% market share in 2026, due to its fundamental role in enabling realistic gameplay through high-end sensors, screens, and launch monitors. The increasing adoption of advanced hardware among commercial facilities and professional users further supports its market dominance. For instance,

- Major hardware providers such as TrackMan, Foresight Sports, and Golfzon dominate the global market, supplying high-precision launch monitors and sensors used in commercial and residential simulators.

Simulator hardware represents the foundational revenue layer within the golf simulator market. Core components include launch monitors, radar or photometric tracking systems, impact screens, projectors, hitting mats, enclosures, and computing units. Hardware currently accounts for the largest share of the total golf simulator market size, particularly in commercial installations where system precision directly affects pricing power and customer retention.

Launch monitor technology is the most critical hardware determinant. Radar-based systems and high-speed camera arrays measure ball speed, launch angle, spin rate, and club path. Accuracy variance materially influences enterprise purchasing decisions. Premium commercial venues prioritize professional-grade tracking capable of replicating outdoor play conditions with minimal deviation.

Projector resolution and screen durability also influence commercial utilization rates. High-lumen 4K projection systems improve visual realism, supporting immersive entertainment experiences. Impact screen lifespan affects operating costs, particularly in high-traffic hospitality venues.

Simulator Software

Simulator software is becoming the primary differentiation engine within the golf simulator industry. While hardware provides physical tracking capability, software determines realism, analytics depth, content diversity, and user engagement longevity. Core software functions include course simulation rendering, physics-based ball flight modeling, swing diagnostics, multiplayer connectivity, and skill tracking analytics. Premium simulation engines license real-world golf course environments, enhancing authenticity and customer appeal.

Subscription-based licensing structures are reshaping the growth dynamics of the golf simulator market. Instead of one-time software purchases, many vendors now offer recurring content updates, tournament access, and cloud-based data storage. This transition strengthens lifetime customer value and stabilizes revenue streams.

Advanced analytics modules are increasingly embedded within software platforms. Artificial intelligence algorithms evaluate swing consistency, recommend corrective drills, and track improvement metrics over time. These capabilities strengthen value propositions for coaching academies and competitive players. Interoperability also matters. Software compatibility across multiple launch monitor brands expands addressable demand. Open ecosystem platforms may capture broader golf simulator market share than closed proprietary systems.

Simulator Services

Simulator services are expected to grow at the highest CAGR owing to the increasing demand for installation, maintenance, and software upgrades. The shift toward customizable solutions and ongoing support enhances the value for service providers. Simulator services encompass installation, calibration, maintenance, training, content management, and venue consulting. Although services represent a smaller revenue component relative to hardware, they significantly influence customer retention and lifetime value. Installation complexity varies by system type. Built-in commercial systems require enclosure construction, acoustic treatment, electrical configuration, and projector alignment. Professional installation services ensure optimal sensor calibration and visual accuracy. Improper installation directly affects system credibility.

Maintenance contracts are becoming increasingly relevant. High-traffic commercial venues require periodic sensor recalibration, screen replacement, and projector servicing. Service-level agreements reduce downtime and protect revenue continuity. Consulting services are emerging within hospitality-focused segments. Vendors assist operators in space layout planning, revenue modeling, and utilization optimization. This advisory layer supports enterprise buyers unfamiliar with golf entertainment economics.

By Product Type

Portable Simulators Dominate Owing to Their Ease of Installation and Cost-Effectiveness

Based on product type, the market is separated into portable and built-in.

Portable

Portable simulators dominate the global market as they offer ease of installation, mobility, and cost-efficiency, making them highly suitable also for setups such as homes and small businesses. Their growing use among amateur players and indoor entertainment contributes to their widespread adoption. Portable simulators segment will account for 64.37% market share in 2026. For instance,

- Portable simulators such as SkyTrak, Phigolf, and Garmin Approach R10 are widely used across North America, Europe, and the Asia Pacific due to their affordability and ease of installation in homes and small businesses.

Portable systems represent an increasingly dynamic segment within the golf simulator market, driven by affordability, flexibility, and reduced spatial requirements. These configurations typically consist of compact launch monitors paired with mobile projection solutions or tablet-based visualization interfaces. Compared to permanent installations, portable systems offer lower capital expenditure and simplified setup.

Adoption within the residential and amateur segment is particularly strong. Enthusiasts seeking swing analytics without committing to structural renovation view portable platforms as an accessible entry point. Small coaching academies and driving ranges also utilize portable systems for temporary event deployments or seasonal programming.

Technology improvements have narrowed the performance gap between portable and built-in systems. Radar-based compact units now provide high-fidelity ball speed and spin measurements, sufficient for skill development purposes. However, environmental lighting sensitivity and limited immersive projection capabilities constrain realism relative to full enclosures.

Built-in

Built-in simulators are expected to grow at the highest CAGR of 12.31% during 2025-2032, due to increasing installations in commercial settings such as golf clubs, hotels, and sports complexes. The demand for immersive and permanent setups with advanced features drives this segment's growth trajectory.

Built-in systems represent the premium and commercially dominant product category within the golf simulator market. These installations involve dedicated enclosures, high-lumen projectors, professional-grade launch monitors, and integrated acoustic treatments. Built-in simulators are typically deployed in hospitality venues, training academies, corporate offices, and high-income residential environments.

The immersive realism offered by built-in configurations supports higher monetization rates. Commercial operators rely on full-enclosure installations to deliver authentic course simulations, group experiences, and event hosting capabilities. These systems justify higher pricing through enhanced user engagement and repeat visitation. Built-in platforms require significant space allocation and structural preparation. Ceiling height, swing clearance, and ventilation must be carefully engineered. As a result, this segment is capital-intensive and often associated with professional installation services.

By Simulator Type

Realistic Gameplay and Professional Demand to Drive Full Swing Simulators' Growth

Based on the simulator type, the market is distributed into full swing simulators and Virtual Reality (VR) golf.

Full Swing Simulators

Full swing simulators hold the highest share of the global market owing to their realistic gameplay experience, accuracy, and demand from commercial and professional users. Their ability to replicate complete golf swings and course conditions makes them the preferred choice. The full swing simulators are anticipated to capture 70.32% of the market share in 2026.

Full swing simulators represent the core revenue engine within the golf simulator market. These systems replicate complete ball flight trajectories using radar, photometric, or hybrid sensor tracking technologies. Accuracy in measuring club path, launch angle, spin rate, and carry distance determines user trust and enterprise adoption viability.

Commercial venues rely predominantly on full swing systems due to their ability to simulate real-world course environments at high fidelity. Hospitality operators monetize immersive gameplay experiences, tournament events, and skill-based competitions. High utilization rates justify the capital investment required for professional-grade tracking systems and projection infrastructure.

Training academies and professional coaches also prefer full swing platforms for detailed performance diagnostics. Advanced analytics modules provide shot dispersion mapping, consistency tracking, and biomechanical swing interpretation. These features reinforce the premium positioning of this segment.

Virtual Reality (VR) Golf

Virtual Reality (VR) golf is expected to grow at the highest CAGR of 12.18% during 2025-2032, due to the rising interest in immersive experiences and technological advancements in VR hardware. Increasing user-friendliness of affordable VR equipment is further expanding the user base across residential and amateur categories. For instance,

- VR golf is rapidly expanding in entertainment venues and gaming cafés, especially in the U.S., Europe, and the Asia Pacific, leveraging platforms such as Oculus Rift and HTC Vive.

Virtual Reality (VR) golf represents an emerging and innovation-driven segment within the golf simulator market. Unlike traditional full swing systems, VR golf emphasizes immersive visual engagement using head-mounted displays and motion tracking controllers. These systems often prioritize entertainment over strict swing analytics precision.

VR golf platforms appeal particularly to entertainment venues and younger demographics seeking gamified experiences. Multiplayer virtual environments, fantasy course settings, and interactive game formats differentiate this category from traditional simulation systems.

However, motion tracking precision remains comparatively lower than professional-grade radar or camera-based tracking solutions. For serious training applications, VR systems are typically supplementary rather than primary performance tools. Physical swing constraints while wearing headsets may also limit realism.

By Business Model

Rising Demand for Consistent and High-Quality Services Boosts Built-in Segment’s Growth

Based on the business model, the market is divided into built-in and subscription-based.

Built-in (Capital Purchase Model)

The built-in business model dominates the global market as many commercial establishments opt for permanent simulator setups to offer consistent, high-quality services. These installations provide long-term value and are integral to professional training and entertainment venues. The built-in segment is anticipated to capture 73.21% of the market share in 2026. For instance,

- Global leaders such as Golfzon and Full Swing Golf offer comprehensive, built-in solutions catering to large-scale installations.

The built-in capital purchase model remains the dominant business structure within the golf simulator market, particularly for commercial operators and high-end residential buyers. Under this model, customers invest upfront in complete hardware systems, including launch monitors, projection units, enclosures, and computing infrastructure. Revenue for vendors is realized primarily at the point of installation, supplemented by maintenance and optional software licensing.

Commercial venues such as indoor golf lounges and hospitality centers favor capital ownership due to long-term utilization expectations. High traffic volumes justify equipment amortization over multi-year operating cycles. Enterprise buyers evaluate the total cost of ownership, factoring in depreciation schedules, service agreements, and hardware upgrade timelines.

Subscription-based Model

The subscription-based model is expected to witness the highest CAGR of 12.47% due to its affordability and flexibility, especially among individual users and small businesses. Recurring revenue models offering regular software updates and online content are gaining popularity.

The subscription-based model is increasingly reshaping long-term golf simulator market trends. Rather than relying solely on upfront equipment sales, vendors offer recurring revenue structures tied to software access, content updates, analytics modules, and virtual tournament participation.

This model stabilizes vendor revenue streams while reducing initial capital barriers for buyers. Some providers bundle hardware leasing arrangements with monthly service fees, enabling operators to distribute costs over time. Such structures are particularly attractive for startups and smaller commercial venues seeking capital efficiency.

Subscription-based licensing strengthens customer retention by embedding users within proprietary software ecosystems. Course libraries, multiplayer competition platforms, and cloud-based performance data storage create switching costs. Over time, these recurring elements may capture a growing share of the golf simulator market relative to pure hardware transactions.

By End-user

To know how our report can help streamline your business, Speak to Analyst

High Demand for Premium Leisure Offerings Fuels Commercial Segment’s Growth

Based on end-user, the market is trifurcated into commercial, residential/amateur, and educational institutes.

Commercial

The commercial sector leads the global market, driven by demand from golf clubs, academies, entertainment centers, and hotels offering golf as a premium leisure activity. The need for high-traffic, durable systems supports market dominance. The commercial sector is anticipated to capture 51.56%% of the market share in 2025.

The commercial segment represents the primary revenue contributor within the golf simulator market. Indoor golf lounges, sports entertainment venues, hospitality chains, country clubs, and corporate recreation facilities account for the largest share of system installations. These operators deploy simulators to generate diversified revenue streams, including hourly rentals, food and beverage sales, event hosting, and league tournaments.

Utilization rate is the central economic variable. Commercial buyers evaluate return on investment through projected booking volumes and average revenue per bay. High-traffic environments justify investment in premium full-swing systems with advanced analytics and immersive projection capabilities.

Urbanization and limited land availability in metropolitan regions further strengthen commercial demand. Simulators enable golf experiences without requiring access to traditional courses. Corporate team-building and client entertainment programs also contribute incremental demand. From a golf simulator market size perspective, commercial installations generate higher per-unit revenue compared to residential deployments. As experiential entertainment continues to expand globally, this segment is expected to maintain a dominant golf simulator market share.

Residential/Amateur

The residential/amateur segment is expected to grow at the highest CAGR of 12.01% during 2025-2032, due to increasing consumer interest in golf as a home-based leisure activity. The growing availability of affordable simulators and rising disposable incomes further boost segment expansion.

Residential adoption within the golf simulator market is growing steadily, driven by affluent amateur golfers and serious hobbyists. These buyers seek year-round practice capability and data-driven swing analytics without traveling to courses or driving ranges. Space availability remains a structural constraint. Built-in systems require ceiling height and dedicated room dimensions, limiting addressable demand in dense urban housing. Portable systems partially mitigate this limitation, expanding reach to suburban and mid-income segments.

Price sensitivity is higher compared to commercial buyers. As hardware costs decline and financing options expand, residential penetration is expected to increase. However, unit economics remain closely tied to discretionary income trends. From a golf simulator market growth standpoint, residential demand contributes incremental volume expansion rather than a dominant revenue share. Over time, subscription-based software and online competition platforms may increase recurring engagement among this segment.

Educational Institutes

Educational institutes, including universities, golf academies, and professional training centers, represent a specialized but strategically significant segment within the golf simulator market. Adoption is driven by structured performance development and athlete recruitment objectives.

Data analytics capabilities are central to purchasing decisions. Institutions prioritize swing diagnostics, performance tracking, and biomechanics integration. Simulators support standardized training independent of weather variability, improving athlete development consistency. University athletic programs utilize simulators for year-round practice scheduling and team evaluation. Golf academies integrate simulator technology into coaching curricula, enhancing competitive positioning.

Regional Insights

By region, the market is studied across North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America Golf Simulator Market Analysis:

North America Golf Simulator Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 0.78 billion in 2025, representing 40.70% of total market revenue, and is projected to reach USD 0.85 billion in 2026, mainly led by the U.S., where major players such as Foresight Sports, Uneekor, and SkyTrak have established strong retail and online distribution networks. Commercial adoption is expanding in urban areas through simulation-based golf bars and private club installations in metropolitan hubs such as New York, Chicago, and Los Angeles. High per capita income and strong interest in golf as a sport and a leisure activity further reinforce market leadership. The U.S. market in 2026 is expected to reach USD 0.5 billion. For instance,

- In May 2025, Golf VX, a provider of indoor golf simulators, announced the opening of its newest franchise location, Golf VX Boston. This marks the company’s second U.S. agreement after the launch of Golf VX Arlington Heights in 2024.

North America leads the global golf simulator market, driven by high golf participation rates and strong commercial venue expansion. The United States and Canada account for the majority of the regional golf simulator market size due to established indoor golf lounge networks and affluent residential buyers. Technology adoption is rapid, particularly for premium full swing systems. Stable discretionary income supports continued golf simulator market growth.

United States golf simulator market:

The United States dominates the global golf simulator market share, supported by strong consumer spending and a mature golf ecosystem. Commercial hospitality chains continue expanding simulator-based entertainment concepts. Residential adoption remains concentrated in high-income households with dedicated space. Subscription-based software penetration is rising. Ongoing innovation in launch monitor accuracy and immersive projection systems sustains long-term golf simulator market growth potential.

Asia-Pacific Golf Simulator Market Analysis:

In 2025, the Asia Pacific market stood at USD 0.37 billion, representing 19.60% of global demand, and is projected to grow to USD 0.41 billion in 2026. Asia-Pacific is emerging as a high-growth region within the golf simulator market. Urban density and limited course availability create favorable conditions for indoor alternatives. South Korea and Japan demonstrate advanced adoption, while China shows accelerating commercial investment. Rising middle-class participation in golf supports long-term golf simulator market size expansion across metropolitan centers.

This region’s golf simulator market is expected to grow at the highest CAGR, driven by rapid urbanization and the rise of compact leisure formats suitable for dense urban environments. For instance,

- According to industry specialists, the region significantly contributes to the global golfing population, supporting a total record of 66.6 million players worldwide.

Japan golf simulator market:

Japan maintains a strong historical adoption of indoor golf facilities due to urban land constraints. Advanced technology acceptance supports demand for high-precision launch monitors. Commercial entertainment venues contribute significantly to the golf simulator market share. Residential adoption remains limited by space considerations. Continued innovation in compact system design reinforces steady golf simulator market growth.

China golf simulator market:

China’s golf simulator market is expanding alongside rising interest in golf as a premium recreational activity. Commercial venues dominate current installations, particularly in tier-one cities. Domestic manufacturers are increasing hardware production capacity and improving cost competitiveness. Although participation rates remain lower than in Western markets, long-term urban entertainment trends support sustained golf simulator market growth.

China leads the region with Golfzon operating thousands of simulation-based screen golf centers nationwide, reflecting a strong cultural integration of the technology. Japan is following with increased deployment in commercial entertainment spaces and upscale residential developments. The market in China is estimated to be USD 0.10 billion in 2025. The Indian market is anticipated to be USD 0.08 billion, and Japan’s market is projected to reach USD 0.1 billion in 2026.

Europe Golf Simulator Market Analysis:

Europe contributed approximately USD 0.56 billion to the global market in 2025, accounting for 29.00% share, and is expected to reach USD 0.61 billion in 2026, supported by strong consumer interest in off-course golfing activities and structured training. The U.K. and Germany have witnessed high installation rates of simulators in golf academies and year-round training facilities. Regulatory support for indoor sports infrastructure and investments from regional sports federations further aid market expansion. Further, the presence of established golf tourism circuits also enables growth in hotel-based simulation installations. For instance,

- According to Skal Europe, the European golf tourism market generated approximately USD 8.11 billion in revenue in 2023. The market is projected to reach USD 16.23 billion by 2035, reflecting a strong annual growth rate of 7%.

Europe demonstrates steady golf simulator market growth, particularly in the United Kingdom, Germany, and Nordic countries. Seasonal weather conditions encourage indoor training solutions. Commercial installations are increasing within hospitality and sports complexes. However, capital expenditure sensitivity moderates expansion compared to North America. Growing interest in performance analytics and structured coaching supports the gradual expansion of the golf simulator market size. The French market is anticipated to be USD 0.09 billion in 2025. Germany’s market is projected to reach USD 0.14 billion in 2026.

United Kingdom golf simulator market:

The United Kingdom golf simulator market benefits from high golf participation and variable weather conditions. Indoor golf lounges and hospitality venues are expanding across major cities. Performance-focused amateur golfers drive residential demand for advanced launch monitor systems. Subscription-based content adoption is increasing steadily. Continued venue development supports moderate but sustained golf simulator market growth. The market in U.K. is estimated to be USD 0.17 billion in 2026.

Middle East & Africa (MEA) and South America

Middle East & Africa maintained a strong presence in the global market, reaching USD 0.12 billion in 2025, accounting for 6.30% share, and is expected to reach USD 0.13 billion in 2026, due to the increasing adoption of luxury indoor golfing experiences in premium hospitality venues. Countries, including the UAE and Saudi Arabia, are investing in elite leisure destinations where golf simulators are offered as part of exclusive amenities in resorts and private clubs. High-temperature climates also make indoor golf facilities a more practical and attractive option year-round.

The Middle East and Africa region shows selective adoption within luxury hospitality venues and private golf academies. Extreme climate conditions support indoor training demand. Installations are concentrated in high-income urban centers. While overall golf simulator market share remains limited, premium venue expansion may support moderate regional growth.

The GCC countries are expecting the market to hit USD 0.03 billion in 2025. For instance,

- In April 2024, Club Lab Golf, a UAE-based company, entered the premium at-home golf simulator market in response to increasing consumer demand. The company is leveraging the convergence of affordability, advanced technology, and personalized service to deliver enhanced residential golf simulation solutions.

Latin America Golf Simulator Market Analysis:

The Latin America market accounted for USD 0.09 billion in 2025, representing 4.70% of the global industry, and is expected to reach USD 0.1 billion in 2026. Latin America represents an emerging segment of the global golf simulator market. Adoption remains concentrated in upscale hospitality venues and private clubs. Economic volatility influences capital investment decisions. However, urban entertainment development and growing middle-income participation may gradually increase the golf simulator market size over the medium term. However, South America is projected to grow at an average rate due to limited regional awareness of simulation-based golf, especially outside of Brazil, Argentina, and Chile.

Golf Simulator Industry Competitive Landscape

Key Industry Players

Key Players Launch New Products to Strengthen Market Positioning

Major players launch new product portfolios to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, acquisitions, and partnerships to strengthen their product offerings. Such strategic product launches help companies maintain and grow their market share in a rapidly evolving industry.

The golf simulator market exhibits a moderately concentrated competitive structure characterized by vertically integrated platform providers, specialized hardware manufacturers, and emerging software-centric entrants. Market leadership is largely defined by sensor accuracy, simulation realism, and ecosystem integration rather than pure volume distribution.

Sensor precision remains the principal differentiation variable. High-speed camera arrays and Doppler radar technologies influence credibility within training and commercial environments. Vendors capable of delivering reliable spin-rate and club-path accuracy command premium pricing and stronger golf simulator market share.

Strategic partnerships between hardware manufacturers and simulation software developers are increasing. These alliances expand compatibility and accelerate product adoption across broader customer bases. Commercial operators favor platforms with integrated booking systems, analytics dashboards, and recurring content updates. Barriers to entry include research and development intensity, optical tracking calibration complexity, and brand trust among performance-oriented golfers. However, portable device innovation has lowered entry thresholds in the mid-tier segment.

Consolidation risk is moderate. Larger integrated players may acquire niche sensor or software startups to strengthen analytics capabilities. Over time, competitive advantage will likely concentrate among firms combining hardware precision, immersive simulation software, and scalable subscription ecosystems.

List of Key Golf Simulator Companies Profiled:

- Panasonic Corporation (Japan)

- E6 Connect (TrueGolf) (U.S.)

- Foresight Sports (U.S.)

- Full Swing Golf (U.S.)

- Golfzon (South Korea)

- SKYTRAK (U.S.)

- TruGolf (U.S.)

- OptiShot Golf (U.S.)

- Vgolf (France)

- TrackMan (Denmark)

- Phigolf (South Korea)

- Toptracer (Sweden)

- HD Golf (Canada)

- Uneekor (U.S.)

- X-Golf (U.S.)

- ProTee United (Netherlands)

- FlightScope (U.S.)

- AboutGolf (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: IdeasLab launched XView AI, a markerless app that provides real-time, offline analysis of the full golf swing by tracking body, shaft, and club movement. This app is available on the iPhone App Store.

- May 2025: Golf VX, a provider of indoor golf simulators, announced the opening of its newest franchise location, Golf VX Boston. This marks the company’s second U.S. agreement after the launch of Golf VX Arlington Heights in 2024.

- April 2025: TruGolf and Digital Legends announced a partnership to launch an advanced golf simulator experience. It is built on TruGolf's Apex platform, featuring AI-driven recreations of legendary players such as Ben Hogan. The simulator will enable users to compete with historic golf figures, receive AI-powered coaching, and engage in tournaments on modern courses.

- February 2025: Canopy, a remote monitoring and management software provider, partnered with Full Swing Golf. This collaboration allows Full Swing’s support and software teams to leverage Canopy’s platform to enhance the performance, reliability, and remote management of their global simulator fleet.

- November 2024: Smartgolf LLC launched Smartgolf AI Coach, an advanced device aimed at enhancing golf performance through precise skill improvement. The device uses AI to analyze swing metrics such as speed, distance, angle, and direction, providing instant, detailed feedback via a connected app.

REPORT COVERAGE

The market report focuses on key aspects such as leading companies, product types, and leading product end-users. Besides, it offers insights into the market trend analysis and highlights vital industry developments. In addition to the factors above, it encompasses several factors that contributed to the market's growth in recent years. The market segmentation is mentioned below:

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

|

Study Period |

2021-2034 |

|

|

Base Year |

2025 |

|

|

Forecast Period |

2026-2034 |

|

|

Historical Period |

2021-2024 |

|

|

Unit |

Value (USD Billion) |

|

|

Growth Rate |

CAGR of 10.10% from 2026 to 2034 |

|

|

Segmentation |

By Offering, Product Type, Simulator Type, Business Model, End-user, and Region |

|

|

Segmentation |

By Offering

By Product Type

By Simulator Type

By Business Model

By End-user

By Region

|

|

|

Companies Profiled in the Report |

|

|

Frequently Asked Questions

The market is projected to record a valuation of USD 4.7 billion by 2034.

In 2026, the market size stood at USD 2.11 billion.

The market is projected to grow at a CAGR of 10.10% during the forecast period of 2026-2034.

Based on end-user, the commercial sector is leading the market.

The rising number of golf courses drives the growth of the golf simulator.

Panasonic Corporation, E6 Connect (TrueGolf), Foresight Sports, and Full Swing Golf are the top players in the market.

North America dominated the golf simulator market with a share of 40.70% in 2025.

Asia Pacific is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us