Greenhouse Gas Monitoring Market Size, Share & Industry Analysis, By Technology (Non-Dispersive Infrared (NDIR), Fourier Transform Infrared (FTIR), Gas Chromatography (GC), Laser-Based Spectroscopy, and Electrochemical Sensors), By Monitoring Type (Continuous Emmission Monitoring Systems, Ambient Air Monitoring, and Leak Detection and Repair (LDAR) Monitoring), By End-Use Industry (Oil and Gas Industry, Power Generation, Industrial Manufactuirng, Waste Management, Agriculture, and Government and Environmental Agencies), and Regional Forecast, 2026-2034

Greenhouse Gas Monitoring Market Size and Future Outlook

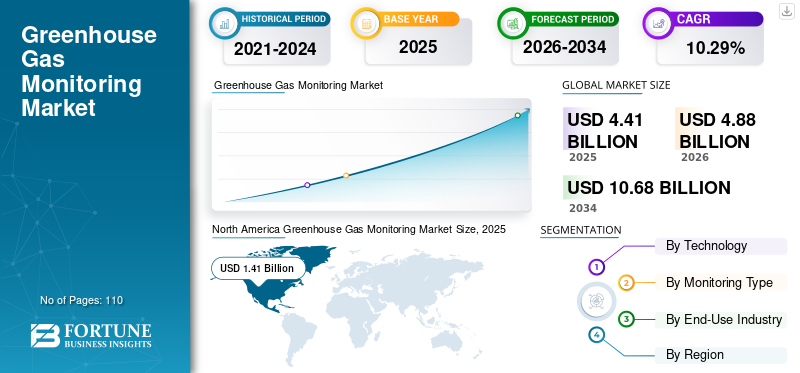

The global greenhouse gas monitoring market size was valued at USD 4.41 billion in 2025. The market is projected to grow from USD 4.88 billion in 2026 to USD 10.68 billion by 2034, with a CAGR of 10.29% over the forecast period. North America dominated the greenhouse gas monitoring market with a market share of 31.97% in 2025.

Greenhouse gas monitoring (GHG) involves the use of advanced instruments, sensors, and data management systems to continuously or periodically measure GHG concentrations and emissions across industrial facilities, energy systems, transportation networks, and environmental settings. These systems help organizations quantify emissions, meet environmental regulations, and support climate change mitigation strategies. The greenhouse gas (GHG) monitoring market is experiencing strong growth, supported by increasing investments from governments, private organizations, and financial institutions aimed at achieving climate targets and enhancing environmental accountability. I

The market is primarily driven by the increasing stringency of environmental regulations and global climate commitments, compelling industries to accurately measure and report emissions. Governments and regulatory bodies across regions are implementing mandates such as carbon reporting frameworks, emissions trading systems, and net-zero targets, which are significantly boosting the adoption of continuous emissions monitoring systems (CEMS) and advanced gas analyzers. Additionally, the growing focus on sustainability and ESG (Environmental, Social, and Governance) initiatives among corporations is accelerating demand for real-time GHG monitoring solutions to enhance transparency and accountability. Advancements in sensor technologies are significantly driving the growth of the greenhouse gas (GHG) monitoring market by enabling more accurate, reliable, and real-time detection of emission. The integration of air quality monitoring with GHG systems is driving market growth, as both are increasingly being addressed together under environmental and regulatory frameworks. The greenhouse gas (GHG) monitoring market is increasingly being shaped by the integration of advanced data analytics, which enhances the accuracy, efficiency, and real-time capabilities of emission tracking systems. With the growing adoption of technologies such as IoT-enabled sensors, satellite monitoring, and continuous emissions monitoring systems (CEMS), vast volumes of environmental data are being generated. The adoption of real time data in greenhouse gas (GHG) monitoring is also rapidly growing due to the increasing need for immediate, accurate, and actionable insights to meet stringent environmental regulations and climate targets.

ABB, Siemens, and SICK AG are the dominant players in the market due to their strong technological expertise, comprehensive product portfolios, and global presence in industrial automation and emissions monitoring systems. These companies offer advanced continuous emissions monitoring systems (CEMS), gas analyzers, and integrated digital solutions that are widely adopted across key industries such as power generation, oil & gas, and manufacturing, where regulatory compliance is critical.

Download Free sample to learn more about this report.

GREENHOUSE GAS MONITORING MARKET TRENDS

Increasing Demand for Continuous Emissions Monitoring Systems (CEMS) to Drive Market Growth

The increasing demand for CEMS is a major driver of the market, as industries are required to continuously track and report emission levels in real time to comply with stringent environmental regulations. Sectors such as power generation, oil & gas, and industrial manufacturing are increasingly adopting CEMS to ensure accurate measurement of pollutants such as CO₂, NOₓ, and SO₂, thereby avoiding penalties and maintaining operational transparency. Thus, increasing adoption of cutting edge GHG technologies including continuous emissions monitoring systems (CEMS), advanced sensors, and real-time ambient air monitoring networks, is significantly driving the growth of the greenhouse gas monitoring market by enhancing accuracy, compliance, and real-time emissions tracking capabilities.

For instance, in June 2025, Kongsberg Maritime unveiled its new CEMS. This sophisticated system enables shipowners and operators to monitor and manage vessel emissions efficiently, improving fuel efficiency and ensuring compliance with ever more stringent environmental requirements.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Industrial Activities and Stricter Emission Regulations to Drive Market Growth

The expansion of industrial activities is a key driver of the market, as industries such as oil & gas, power generation, chemicals, and manufacturing are among the largest contributors to global emissions. Rapid industrialization, particularly in emerging economies such as China, India, and Southeast Asia, has led to a significant increase in energy consumption and fossil fuel use, resulting in higher emissions of CO₂, methane, and other greenhouse gases. To address this, governments and regulatory bodies are enforcing stricter emission norms and mandating continuous monitoring and reporting, compelling industries to adopt advanced GHG monitoring systems. The implementation of stringent air quality standards is driving the greenhouse gas monitoring market growth, as governments and regulatory bodies worldwide are setting limits on emissions to protect environmental and public health.

For instance, in January 2026, the Central Pollution Control Board (CPCB) mandated the closure of 248 manufacturing facilities across Delhi-NCR region for failing to transition to the Online Continuous Emission Monitoring System (OCEMS). The directive ordered state pollution control boards and committees in NCR states to close down air-polluting factories that repeatedly failed to meet compliance deadlines. Such regulatory enforecement actions highlight the increasing focus on CEM, reinforcing demand for GHG technologies across industrial sectors.

MARKET RESTRAINTS

High Initial Investment and Implementation Costs to Restrain Market Growth

The high initial investment costs associated with GHG systems represents a significant restraint on market growth, as industries are required to allocate substantial capital for the procurement and installation of advanced monitoring equipment such as continuous emissions monitoring systems (CEMS), gas analyzers, sensors, and data management software. In addition to hardware costs, companies are required to invest in system integration, calibration, infrastructure upgrades, and compliance-related certifications, further increasing overall expenditures. This financial burden is particularly challenging for small and medium-sized enterprises (SMEs) and industries operating in cost-sensitive regions, leading to delayed or limited adoption of advanced monitoring technologies.

MARKET OPPORTUNITIES

Rising Awareness in Emerging Economies to Drive Market Growth

The rising awareness across emerging economies is significantly driving the growth of the market, as countries such as India, China, Brazil, and Southeast Asian nations are increasingly recognizing the environmental and economic impacts of uncontrolled emissions. Governments in these regions are strengthening environmental regulations, implementing national clean air programs, and introducing emission-reporting frameworks, compelling industries to adopt GHG monitoring systems. Additionally, growing public awareness, international pressure, and participation in global climate agreements are pushing both public and private sectors to enhance transparency in emissions data.

For instance, in October 2025, the California Air Resources Board (CARB) stated that it intends to complete the necessary legislative requirements to implement SB 253 during the first quarter of 2026. This announcement followed CARB's failure to meet the legal deadline imposed under SB 253 to finalize implementation rule by July 1, 2025, and subsequent delays that pushed expected finalization to December 2025. Despite occasional regulatory delays in developed regions, the rising awareness in emerging economies such as India, China, and Brazil is accelerating the global momentum for greenhouse gas monitoring, as governments in these regions are increasingly implementing stricter emission frameworks, promoting transparency, and encouraging industries to adopt advanced monitoring systems to address growing environmental concerns.

MARKET CHALLENGES

Cybersecurity and Data Privacy Concerns to Hamper Market Growth

Cybersecurity and data privacy concerns are emerging as significant restraints in the GHG monitoring market, particularly as the adoption of digital, cloud-based, and IoT-enabled monitoring systems increases. These systems collect and transmit sensitive operational and emissions data from industrial facilities, making them potential targets for cyberattacks, data breaches, or unauthorized access. Any compromise in data integrity can lead to regulatory non-compliance, financial penalties, and reputational damage for organizations. Additionally, concerns about data ownership, cross-border data transfer regulations, and the confidentiality of industrial information make companies hesitant to adopt connected monitoring solutions fully. As a result, the need for robust cybersecurity infrastructure and compliance with data protection standards adds complexity and cost, thereby slowing down the widespread adoption of advanced GHG monitoring technologies.

Segmentation Analysis

By Technology

Non-Dispersive Infrared (NDIR) Segment Led due to its High Accuracy

Based on technology, the market is classified into Non-Dispersive Infrared (NDIR), Fourier Transform Infrared (FTIR), Gas Chromatography (GC), laser-based spectroscopy, and electrochemical sensors.

Non-Dispersive Infrared (NDIR) dominated the market, with a 37.23% share in 2025. The segment’s growth due to its high accuracy, reliability, and cost-effectiveness in measuring key gases such as carbon dioxide (CO₂), methane (CH₄), and carbon monoxide (CO). NDIR sensors operate based on the principle of infrared light absorption, allowing for precise and continuous detection of gas concentrations, making them ideal for applications such as continuous emissions monitoring systems (CEMS) and industrial process monitoring.

For instance, in March 2026, Honeywell unveiled a new gas sensor that uses optical non-dispersive infrared (NDIR) technology to detect combustible gases in industrial environments, including methane, propane, and butane. In sectors such as mining, oil and gas, petrochemicals, and plastics manufacturing, the NDIR Hydrocarbon Gas Sensor helps protect people and infrastructure.

Gas Chromatography (GC) is the fastest-growing segment and is projected to grow at a 11.28% CAGR during the forecast period. The segment dominates due to its high precision, sensitivity, and ability to accurately separate and analyze complex gas mixtures, making it highly suitable for detecting trace levels of greenhouse gases such as methane (CH₄), carbon dioxide (CO₂), and nitrous oxide (N₂O). This technology is widely used in laboratories, environmental monitoring stations, and industrial applications where detailed compositional analysis and regulatory compliance are critical.

By Monitoring Type

Critical Role of Continuous Emission Monitoring Systems in Monitoring Pollutants Boosted Segment Growth

By monitoring type, the market is categorized into continuous emission monitoring systems, ambient air monitoring, and leak detection and repair (LDAR) monitoring.

The continuous emission monitoring systems segment dominated the market, accounting for a 67.88% share in 2025. The growth of the segment is driven by its critical role in providing real-time, accurate, and continuous emissions measurements, which are essential for regulatory compliance across industries such as power generation, oil & gas, and manufacturing. Governments and environmental agencies worldwide have made CEMS mandatory for large industrial facilities, driving widespread adoption. These systems enable organizations to continuously monitor pollutants such as CO₂, NOₓ, and SO₂, ensuring transparency, reducing the risk of penalties, and supporting sustainability goals.

For instance, in August 2024, ABB announced that it has signed an agreement to acquire the Födisch Group, a leading developer of advanced measurement and analysis solutions for the energy and industrial sectors. The acquisition would strengthen ABB's continuous emissions monitoring systems (CEMS) offering, enhancing its capabilities in real-time emissions measurement and regulatory compliance. It would also improve ABB's competitiveness in technology and innovation, while enabling the company to broaden its portfolio of continuous emissions monitoring solutions to meet customers' need

The ambient air monitoring is growing with a CAGR of 11.03% during the forecast period. The growth of the segment is due to the growing need to assess and manage air quality at broader environmental and urban levels. Rising concerns over climate change, urban pollution, and public health are driving governments and environmental agencies to deploy large-scale ambient monitoring networks to track atmospheric concentrations of greenhouse gases such as CO₂ and methane.

By End-User Industry

To know how our report can help streamline your business, Speak to Analyst

Oil and Gas Industry Segment Led due to its Significant Contribution to Global Emissions

By end-user industry, the market is categorized into oil and gas industry, power generation, industrial manufacturing, waste management, agriculture, and government and environmental agencies.

The oil and gas industry segment captured the dominant greenhouse gas monitoring market share, holding a 25.60% share in 2025. The segment is growing due to its significant contribution to global emissions, particularly methane (CH₄) and carbon dioxide (CO₂), across upstream, midstream, and downstream operations. Increasing regulatory pressure to detect, monitor, and reduce emissions especially methane leaks from pipelines, refineries, and production sites is driving the adoption of advanced monitoring technologies such as continuous emissions monitoring systems (CEMS), infrared sensors, and satellite-based solutions.

For instance, in August 2025, Teledyne Gas & Flame Detection (Teledyne GFD) launched the PS DUO, a portable dual-gas detector set, intended to enhance personal safety in gas monitoring applications, especially in the oil and gas business, where employees are routinely exposed to dangerous gases. The device uses passive diffusion detection to continuously monitor hazardous gases in hazardous settings and deliver prompt warnings when gas concentrations exceed acceptable levels. The PS DUO is well-suited for safety monitoring throughout upstream, midstream, and downstream oil and gas activities since it can simultaneously monitor two gases, including carbon monoxide (CO), hydrogen sulfide (H2S), sulfur dioxide (SO2), ammonia (NH3), oxygen (O2), hydrogen (H2), nitrogen dioxide (NO2), and ozone (O3).

The agriculture segment is growing at a CAGR of 12.74% during the forecast period due to its significant contribution to global greenhouse gas emissions, particularly methane (CH₄) from livestock and nitrous oxide (N₂O) from fertilizers and soil management practices. Increasing global focus on reducing agricultural emissions, improving sustainable farming practices, and meeting climate targets is driving the adoption of monitoring solutions in this sector.

GREENHOUSE GAS MONITORING MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

North America Greenhouse Gas Monitoring Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific region was valued at USD 1.13 billion in 2025 and is expected to reach USD 1.26 billion by 2026. Rapid industrialization, urbanization, and rising environmental concerns in major economies such as China, India, and Southeast Asia are driving the market in Asia Pacific. Increased emissions from industries such as power generation, oil & gas, and manufacturing have led governments to establish tighter emission controls, national clean air initiatives, and carbon-reduction goals.

CHINA GREENHOUSE GAS MONITORING MARKET

In 2025, the China market reached USD 0.44 billion. The market is growing rapidly due to the country’s strong regulatory push and its large-scale emission footprint across key industrial sectors. As the world’s largest emitter of greenhouse gases, the country is implementing strict carbon reduction policies, national emissions trading systems, and mandatory monitoring frameworks for industries such as power generation, steel, and chemicals.

For industries, in September 2025, the Chinese governments declared plans to reduce its emissions by 7 to 10% from peal levels by 2035. This announcement marked a significant policy shift, as China prioritized lowering emissions intensity, which is the amount of emissions produced per unit of GDP.

INDIA GREENHOUSE GAS MONITORING MARKET

The Indian market reached around USD 0.17 billion in 2025, accounting for roughly 15.50% of the global market. The market is growing due to a unique combination of policy development, infrastructure expansion, and the strengthening of environmental governance frameworks, which differs the country’s regulatory environment from that of many other regions.

India is witnessing a transition from pollution control toward structured emissions accountability, driven by initiatives such as the Perform, Achieve and Trade (PAT) scheme, National Action Plan on Climate Change (NAPCC), and the gradual rollout of carbon market mechanisms. Unlike developed markets, where monitoring infrastructure is already mature, India’s market growth is fueled by the formalization of monitoring practices. This includes the increasing deployment of online continuous emissions monitoring systems (OCEMS) across industries such as cement, power, and steel.

North America

North America is the dominating region in the market. The region was valued at roughly USD 1.30 billion in 2024 and touched USD 1.41 billion by 2025. The market is well-established and expanding at a consistent pace, driven by mature regulatory systems, the integration of innovative technologies, and a significant commitment to corporate sustainability.

Regulatory agencies such as the EPA and Environment and Climate Change Canada enforce stringent environmental rules in the region, requiring accurate emissions monitoring and reporting across sectors such as power generation, oil and gas, and manufacturing.

U.S. GREENHOUSE GAS MONITORING MARKET

The U.S. market stood at around USD 1.13 billion in 2025. Market growth is driven by a strong mix of regulatory enforcement, technological leadership, and expanding corporate sustainability commitments across industrial sectors. A key driver of market expansion is the regulatory framework established by the U.S. Environmental Protection Agency (EPA), which requires thousands of extensive industrial sites to monitor, record, and report emissions accurately, significantly increasing demand for sophisticated monitoring technologies. The installation of continuous emissions monitoring systems (CEMS), infrared sensors, and satellite-based technologies is also being accelerated by a greater emphasis on lowering methane emissions, particularly in the oil and gas industry.

Europe

The Europe greenhouse gas monitoring market in 2025 was valued at USD 1.23 billion and is expected to reach USD 1.36 billion by 2026. The market is growing witin a framework of sustainability integration and compliance-driven regulation, where emission monitoring serves as a vital element of the region's climate governance and energy transition plans, rather than merely a fulfilling regulatory necessity. The central driver of regional market growth is the EU Emissions Trading System (EU ETS), which establishes a direct financial link between emissions and costs. Under this system, industries are required to use high-precision monitoring, reporting, and verification (MRV) systems to properly meet their carbon compliance obligations. In contrast to other regions, where monitoring is frequently compliance-led, Europe places greater emphasis on measurement accuracy, as emissions reporting is closely tied to financial exposure and carbon markets. The greenhouse gas (GHG) monitoring market in Europe is witnessing significant growth, largely driven by the European Green Deal, which aims to make the region climate-neutral by 2050. This policy framework mandates strict emission reduction targets and enhances the need for accurate, real-time monitoring and reporting of greenhouse gas emissions across industries.

U.K. GREENHOUSE GAS MONITORING MARKET

The U.K. market in 2025 stood at around USD 0.18 billion, representing roughly 15.00% of the global market. The market is expanding under a transparency-driven, data-centric paradigm, with strong emphasis on institutional accountability, digital emssions reporting, and high-quality emissions data, rather than regulatory compliance.

The key driver of market growth is the U.K.’s independent carbon budgeting system in the U.K., which is run by the Climate Change Committee (CCC). This system mandates accurate and regular monitoring of emissions across industries to ensure compliance with legally binding carbon reduction targets. As a result, there is a consistent demand for monitoring systems that are precise and auditable. In contrast to the EU's broader mechanisms, the U.K. places greater emphasis on detailed, industry-specific emissions monitoring, especially in sectors such as buildings, transportation, and decentralized energy systems.

Germany GREENHOUSE GAS MONITORING MARKET

The German market in 2025 stood at around USD 0.24 billion, accounting for roughly 19.20% of the global market. The market is expanding within a precision-engineering and industrial decarbonization framework, with strong focus on energy transition, high-efficiency production, and cutting-edge measurement accuracy.

Germany's expansion is closely linked to its leadership in industrial transformation under the Energiewende Intiative. Under this framework, industries such as steel, chemicals, and automobiles are undergoing significant decarbonization. Meeting stringent emission-reduction goals, lowering energy use, and improving operational efficiency require the deployment of highly accurate, ongoing emissions monitoring systems. Unlike markets where monitoring is compliance-driven, Germany concentrates on process optimization and operational efficiency, placing GHG monitoring at the center of industrial performance improvement.

Latin America & Middle East Africa

Latin America and the Middle East & Africa (MEA) stood at USD 0.30 billion and USD 0.35 billion, respectively, in 2025. The market is growing within a resource-management and international alignment framework, with a focus on managing natural resources, improving environmental governance, and aligning with global climate commitments. A key driver is the region’s strong dependence on natural resource-based industries such as mining, oil & gas, and agriculture, which are major contributors to emissions.

The Middle East & Africa (MEA) market is growing under an energy transition and resource optimization framework, where the focus is on balancing hydrocarbon dependency with sustainability goals and improving operational efficiency.

GCC GREENHOUSE GAS MONITORING MARKET

The GCC market in 2025 stood at around USD 0.17 billion, representing roughly 49.00% of the global market. The market is growing as the region’s focus on energy sector optimization and sustainability-driven diversification intensifies. As GCC countries such as Saudi Arabia, UAE, and Qatar are heavily dependent on oil & gas, there is a strong push to monitor and reduce emissions, particularly methane, across upstream and downstream operations to improve efficiency and align with global climate commitments.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry players are Focusing on Forming Strategic Partnerships to Improve their Market Position

Key players in the greenhouse gas monitoring industry are placing strong emphasis on technological innovation, portfolio diversification, and strategic partnerships to improve their market position. To deliver real-time, high-accuracy emissions data, companies such as ABB, Siemens, Emerson, and SICK AG are investing in cutting-edge gas analyzers, continuous emissions monitoring systems (CEMS), and IoT-enabled solutions. They are also integrating digital analytics, cloud platforms, and artificial intelligence in their systems to improve predictive monitoring and automated reporting.

For instance, in September 2025, The International Organization for Standardization (ISO) and the Greenhouse Gas Protocol (GHG Protocol) a collaborative effort between the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) revealed a historic alliance. The partnership aims to align their current GHG standards portfolios and work together to create new norms for GHG emissions accounting and reporting.

LIST OF KEY GREENHOUSE GAS MONITORING COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Yokogawa Electric Corporation (Japan)

- Horiba Ltd. (Japan)

- SICK AG (Germany)

- Teledyne Technologies Incorporated (U.S.)

- AMETEK Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: The Trans-Anatolian Natural Gas Pipeline (TANAP) introduced a new in-house software platform to track greenhouse gas (GHG) emissions and aid sustainability reporting. The system prioritizes cybersecurity and compliance with international reporting frameworks, enabling safe, open, and standards-compliant management of large-scale data.

- March 2026: Siemens, Atmen, and TURN2X developed the first complete model for RED III-ready renewable gas generation at Turn2X's commercial e-methane facility in Miajadas, Spain. The operational facility demonstrates commercial scale production of green gas, supported by greenhouse gas monitoring systems that enable accurate emissions tracking and regulatory compliance.

- October 2025: Honeywell unveiled a cutting-edge technology that transforms forestry and agricultural waste into usable renewable fuels for difficult-to-abate sectors such as the maritime industry. The technology utilizes low-cost, plentiful biomass sources such as wood chips and crop residues to make gasoline, sustainable aviation fuel (SAF), and lower-carbon marine fuel. These ready-to-use, "drop-in" fuels offer ship operators a more economical and environmentally friendly option compared to conventional fuels. This sustainable marine fuel has a higher energy density than many biofuels now available, allowing a ship to travel farther without requiring expensive engine modifications.

- October 2025: As part of Airbus's program to lower its operational environmental impact, Siemens announced plans to decarbonize four Airbus industrial sites in the U.S. and the U.K. The initiative seeks to reduce energy usage by 20% and stationary Scope 1 and 2 emissions by 85% by 2030, using solutions such as renewable energy integration, intelligent energy management, and low-carbon heat systems, along with greenhouse gas monitoring systems developed in partnership with Capgemini.

- January 2025: Endress+Hauser's whole instrument portfolio now includes SICK's cutting-edge flow measurement and gas analysis technology. The goal of the partnership is to give customers in the process industry better assistance in improving plant efficiency, protecting the environment, and lowering carbon emissions.

REPORT COVERAGE

The global greenhouse gas monitoring market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 10.29% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Technology, By Monitoring Type, By End-Use Industry, and Region |

| By Technology |

|

| By Monitoring Type |

|

| By End-Use Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.41 billion in 2025 and is projected to reach USD 10.68 billion by 2034.

The market is expected to exhibit a CAGR of 10.29% during the forecast period (2026-2034).

The oil and gas industry segment led the market by end-use industry.

Expansion of industrial activities is the key factor driving the market.

Siemens, ABB, and Horiba are among the top players in the market.

North America dominates the market.

Rising awareness in emerging economies is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us