Hazmat Suits Market Size, Share, and COVID-19 Impact Analysis, By Protection Standard (Level A, Level B, Level C, and Level D), By Application (Firefighting, Chemical Protection, Radioactive Protection, Biohazard Protection, and Others), By End-User (Healthcare, Oil & Gas, Mining & Metallurgy, Construction, Manufacturing, and Others), and Regional Forecast, 2026-2034

Hazmat Suits Market Size and Future Outlook

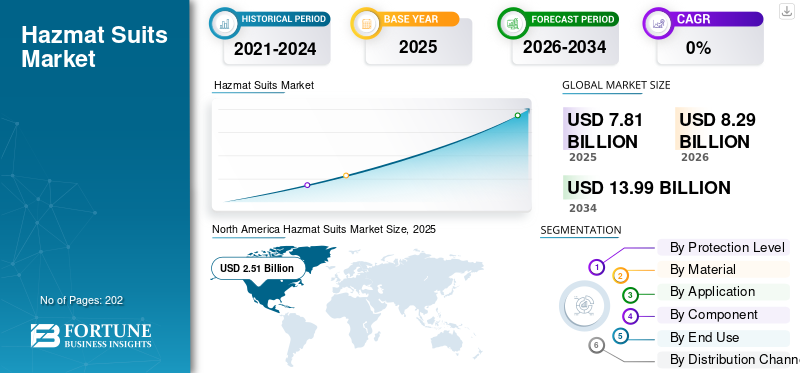

The global hazmat suits market size was valued at USD 7.81 billion in 2025. The market is projected to grow from USD 8.29 billion in 2026 to USD 13.99 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period. North America dominated the global hazmat suits market with a market share of 32.14% in 2025.

A hazmat suit is a whole-body garment designed to protect individuals from contact with hazardous materials such as chemicals, biological agents, or radioactive substances. These suits are a form of Personal Protective Equipment (PPE) and create a barrier against toxic environments. The level of protection provided by hazmat suits varies and is classified from Level A (most protective, fully encapsulating) to Level D (least protective, standard work clothing), according to the Environmental Protection Agency (EPA) and Occupational Safety and Health Administration (OSHA) standards.

Major players in the market include 3M Company, Ansell Limited, Drägerwerk AG & Co. KGaA, DuPont de Nemours Inc., Kappler Inc., Lakeland Industries Inc., Respirex International, and others. These companies dominate the market by offering a range of protective suits that

are required for various industrial, healthcare, and emergency response needs.

3M Company provides advanced protective garments, including chemical-resistant suits with integrated respiratory protection, used widely in industrial and healthcare sectors. Ansell Limited offers multi-layer chemical barrier suits designed for high-level protection in hazardous environments.

Download Free sample to learn more about this report.

Hazmat Suits Market Key Takeaways

- 2025 Market Size: USD 7.81 billion

- 2026 Market Size: USD 8.29 billion

- 2034 Forecast Market Size: USD 13.99 billion

- CAGR: 6.8% from 2026-2034

- North America dominated the hazmat suits market with a 32.14% share in 2025.

- The Level C segment held the largest share of the market in 2025.

- The polypropylene (PP) segment accounted for the largest market share in 2025.

North America

North America generated USD 2.51 billion in 2025, supported by stringent workplace safety standards and strong industrial demand

Europe

Europe is witnessing steady growth due to stringent PPE regulations under Regulation (EU) 2016/425 and a substantial hazardous industrial sector.

Asia Pacific

Asia Pacific is experiencing rapid growth driven by expanding chemical, electronics, battery, and pharmaceutical manufacturing industries.

U.S.

Strong demand from healthcare, chemical, and emergency response sectors continues to support market expansion.

Japan

Increasing focus on industrial safety and preparedness for chemical hazards is driving demand for advanced protective clothing.

Read More

Key Insights:

Shift Toward Lightweight, System-Integrated Advanced Hazmat Suits

The market is increasingly driven by the need for lightweight, durable, and system-integrated CBRN ensembles that reduce physiological stress while maintaining full protective performance. Traditional CBRN suits are often heavy, restrictive, and poorly integrated with masks, boots, and gloves, which limits mobility and operational duration in real-world missions. End-users such as military CBRN units, Special Forces, and hazmat response teams push the suppliers to deliver full protective systems rather than standalone suits, with a focus on comfort, agility, and seamless equipment interfaces.

- For instance, in February 2024, Avon Protection launched its EXOSKIN-S1 CBRN protective suit, explicitly marketed as a low-burden, high-performance suit that seamlessly integrates with respirators, boots, and gloves to form a full-body CBRN protective system.

Impact of Russia-Ukraine War

Russia-Ukraine War Triggers Heightened Defense Spending and Protective Gear Demand

The Russia-Ukraine war has significantly impacted the market owing to rising geopolitical tensions across the globe. This is pushing the military and defense sectors of various countries to increase their spending on protective gear, including advanced hazmat suits for chemical, biological, and nuclear threat preparedness.

Moreover, the war has also encouraged government investments in emergency response readiness and the stockpiling of protective equipment globally, further boosting demand. In addition, the surge in the awareness of chemical and biological warfare risks during the conflict has also accelerated technological innovations and adoption of multi-threat protective suits in defense and civilian sectors, driving market growth.

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Safety Concerns and Rising Incidence of CBRN Industrial Accidents to Drive Market Growth

The market is strongly driven by increasing safety concerns and a rising number of chemical industrial accidents across the globe.

- For instance, a report by a coalition of community and health organizations in 2023 identified 825 hazardous chemical incidents in the U.S. since January 2021, significantly more than previously recognized by government bodies.

These industrial accidents increase the need for protective measures to safeguard workers and local communities, which drives the demand for the product. Therefore, the industries are investing in these suits to ensure compliance, reduce liability risks, and protect individuals handling hazardous materials, further driving market growth. In addition, the expansion of chemical, oil and gas, pharmaceutical, and nuclear sectors continue to fuel the need for advanced protective suits to ensure safety compliance and reduce accident risks.

MARKET RESTRAINTS:

High Cost Associated with Advanced Protective Suits to Limit Market Expansion

A significant restraint for the hazmat suits industry is the high cost associated with advanced protective suits. Numerous small businesses and industries with limited safety budgets find it difficult to invest in high-quality products, which restricts the product adoption. Although stringent safety regulations drive overall demand, the expense of specialized materials, sealed seams, and integrated respiratory devices makes these suits less accessible for organizations with constrained resources, which hampers market growth.

MARKET OPPORTUNITIES:

Stringent Regulations and Safety Standards to Present Growth Opportunities for the Market

Stringent regulations and safety standards imposed by governments and regulatory bodies globally present a significant growth opportunity for the market. Regulations, such as those from OSHA in the U.S. and similar agencies globally, make the use of certified protective equipment compulsory to safeguard workers from chemical, biological, radiological, and nuclear hazards.

- For instance, in October 2024, the European Commission adopted Implementing Decision (EU) 2024/2599, which includes adopting stricter harmonized standards for protective gear such as powered filtering respiratory devices, electrically insulating helmets, footwear, and fall-protection equipment.

This regulatory environment compels industrial establishments in chemical manufacturing, pharmaceuticals, oil and gas, and emergency response to invest heavily in hazmat suits to ensure compliance and minimize legal liabilities.

HAZMAT SUITS MARKET TRENDS:

Development and Adoption of Lightweight and Eco-Friendly Materials is a Significant Market Trend

The advancement of lightweight, breathable, and eco-friendly materials for protective clothing is a substantial opportunity for the market. Traditional hazmat suits tend to be bulky and uncomfortable, which limits their usability and compliance. Therefore, manufacturers focus on creating innovation in the material of suits to enhance the protection, comfort, and mobility of suits. In addition, defense forces are enhancing the protection of military personnel with investment in advanced materials against various chemical, biological, radiological, and nuclear threats.

- For instance, in February 2024, Tetramer Technologies was awarded a USD 12.5 million five-year contract by the Pentagon to develop advanced protective fabrics for soldiers. The project will incorporate the metal-organic framework bead technology designed to neutralize hazardous threats.

MARKET CHALLENGES:

Lack of Awareness and Safety Culture in Emerging Economies Acts a Challenge for the Market

A significant challenge constraining the market growth is the lack of awareness and an underdeveloped safety culture in many emerging economies. In developing regions, there is an insufficient regulatory framework and a limited understanding of the health risks associated with hazardous materials. This decreases the demand for protective gear such as hazmat suits. There is a lack of educational initiatives, stricter enforcement of safety regulations, and partnerships among governments, industries, and NGOs to promote protective suit usage, which pose a challenge to the hazmat suits market growth during the forecast period.

Download Free sample to learn more about this report.

Segmentation Analysis

By Protection Level

Respiratory Protection Needs and Expansion of Industries Drives Level C Segment Growth

On the protection level, the market is classified into level A (full body, highest protection), level B (high respiratory, moderate skin protection), level C (moderate skin, air-purifying protection), and level D (basic protection).

The level C (moderate skin, air-purifying protection) segment held the largest hazmat suits market share in 2025. The growth of this segment is driven by the suitability of these types of suits for scenarios where respiratory protection is essential and vapor and liquid exposure risk is lower. The need for level C suits is increasing in pharmaceutical manufacturing, environmental cleanup, and decontamination activities. The expanding pharmaceutical and electronics manufacturing sectors and stricter regulatory requirements stimulate segmental growth.

The level A (full body, highest protection) segment is expected to grow at a steady rate of 6.8% over the forecast period. This growth is driven by their use in environments requiring the highest level of protection against vapors, gases, and liquids, such as chemical spills and hazardous material response. Moreover, the increasing incidence of industrial chemical accidents and defense partnerships with OEMS for manufacturing advanced high protection CBRN suits is expected to drive the demand for Level A suits.

- For instance, in September 2023, Avon Protection and OPEC CBRNe announced a strategic partnership aimed at innovating CBRN protective suit technologies for international military, special forces, and first responder markets.

By Material

Cost-Effectiveness, Disposable Use, and Wide Application Boosts Demand for Polypropylene Segment

Based on material, the market is segmented into Polypropylene (PP), Polyethylene (PE), Tyvek, PVC (Polyvinyl Chloride), neoprene, and others.

The Polypropylene (PP) segment acquires the largest share in the market, owing to its cost-effectiveness and wide application in disposable, light-duty protective clothing for industrial and healthcare settings. Its application is expanding in sectors such as pharmaceuticals, food processing, and general manufacturing. In addition, emerging economies are increasingly preferring PP-based PPE, due to affordability and ease of disposal, boosting segment growth.

The Tyvek segment is experiencing the fastest growth, driven by its superior chemical resistance, durability, and lightweight nature. Tyvek suits provide effective barrier protection against fine particles, aerosols, and light liquid splashes. The suits made from Tyvek material are increasingly being used in moderate to high-risk applications in chemical, pharmaceutical, and hazardous material handling industries. Manufacturers are constantly involved in the design of Personal Protective Equipment (PPE), which provides high protection and safety across diverse industries. The segment is expected to record the highest CAGR of 8.0% during the forecast period.

- For instance, in December 2024, DuPont officially launched the Tychem 6000 AL ventilated coverall. It is designed to provide enhanced protection and comfort for workers exposed to hazardous chemicals in industries such as pharmaceuticals and chemical manufacturing.

By Application

Increase in Hazardous Chemical Handling and Advanced Material Innovation Support Chemical Protection Segment Growth

Based on application, the market is segmented into chemical protection, biohazard & infection control, radioactive & nuclear protection, firefighting, and others.

The chemical protection segment leads the market as there is an increase in handling hazardous chemicals in industries such as chemical manufacturing, oil & gas, and pharmaceuticals, and others. Stringent safety regulations and rising awareness of chemical hazards encourage companies to adopt specialized suits with advanced materials for effective protection. In addition, there is a surge in research and development of protection suits designed from lighter and durable materials.

- For instance, researchers at the German Institutes of Textile and Fiber Research Denkendorf (DITF) announced the development of a lighter, more flexible chemical protective suit (AgiCSA) with integrated sensors.

The biohazard & infection control segment grows with fastest growth rate fueled by global health concerns, particularly the spread of infectious diseases and pandemics. Healthcare facilities, research labs, and emergency responders increasingly require high-quality suits that offer fluid resistance, and bioaerosol protection, which accelerates the market demand for increased biohazard protection. This segment is estimated to display a CAGR of 7.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Component

Advancement in Fabric Technology and Demand for Durable & Disposable Suits Drive Outer Shell Segment Growth

Based on component, the market is segmented into outer shell, visor/face shield, gloves & boots, respirator/face mask, and others.

The outer shell segment dominates the market as there is a rise in innovation and research in the design of advanced fabric technologies to create lighter, stronger, and more chemically resistant suits. In addition, the demand for durable yet disposable suits in industries such as nuclear power, oil & gas, and chemical manufacturing boosts the adoption of advanced outer shells.

The respirator/face mask segment is expected to grow at the fastest CAGR of 8.2% during the forecast period. This growth is driven by factors such as the increasing cases of airborne and respiratory hazards in healthcare, industrial, and emergency response settings. The COVID-19 pandemic and ongoing concerns about infectious diseases have increased the demand for respirators integrated into hazmat suits. Moreover, the manufacturers aim to evolve the suit structure by integrating advanced masks with high filtration efficiency and comfort to enhance protection.

- For instance, at DSEI 2023, Avon Protection showcased its first CBRN protective suit concept, developed with OPEC CBRNe and designed as a full-body garment integrating with Avon’s CBRN respiratory masks and EXOSKIN boots and gloves.

By End Use

Rising Chemical Use and Stricter Safety Regulation Compliance Propel Industrial & Manufacturing Segment Growth

Based on end use, the market is segmented into industrial & manufacturing, defense & military, healthcare & emergency medical services, public safety agencies, oil & gas, laboratories & research institutions, and others.

The industrial & manufacturing segment holds the largest market share due to the rising use of hazardous chemicals, solvents, and particulates in sectors such as chemicals, pharmaceuticals, mining, and oil & gas. This is pushing companies to upgrade from basic workwear to certified hazmat ensembles for routine operations and shutdowns. In addition, stricter enforcement of OSHA/EN/NFPA norms, and launch & availability of advanced standardized hazmat suits drive the segment growth.

- For instance, in January 2025, E.I. du Pont de Nemours, Inc. launched the DuPont™ Tychem 6000 SFR, a lightweight hooded chemical protective coverall engineered for industrial workers exposed to both chemical splash and flash-fire hazards.

The healthcare & emergency medical services segment is the fastest growing segment as post‑COVID infection-control protocols and pandemic and other infectious disease preparedness plans has pushed the demand for hazmat suits for high‑risk procedures, isolation wards, and ambulance decontamination. Moreover, the expansion of high-containment labs andblood-borne pathogen handling has increased use of biohazard-rated suits in hospitals and research facilities. The segment is likely to grow at the highest CAGR of 9.0% during the forecast period.

By Distribution Channel

Established Supply Chains, Value-Added Services, and Strong Manufacturer Relations Stimulate Distributor Segment Growth

Based on distribution channel, the market is segmented into direct sales, distributors, and online.

The distributor segment holds the largest market share due to established supply chain networks serving industrial, healthcare, and government clients with trusted, personalized service. The segment is growing as distributors add value by providing bulk procurement, discounts, and helping customers understand their suit needs and meet complex protection standards. In addition, their strong relationships with manufacturers and end-users enable tailored product offerings and timely replenishment.

- For instance, in October 2023, Lakeland Industries, Inc. announced that its senior management team participated in the A+A 2023 Trade Fair in Düsseldorf to highlight the company’s comprehensive portfolio of industrial protective apparel and strengthen engagement with buyers and its network of more than 1,600 global safety and industrial supply distributors.

The online segment grows at the fastest rate in the industry as these online e-commerce platforms help customers to access information about hazmat suits in the fastest and transparent manner. Online sales channels boost market reach through detailed product information, customer reviews, and easy comparison. Customers are interested in procuring suits by online channels as it helps with flexibility and competitive pricing. Thus, the factors such as convenience of direct ordering, rapid delivery, and digital payment integration propel the segment growth in the market. The segment is poised to expand with a substantial CAGR of 8.4% during the forecast period.

Hazmat Suits Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Hazmat Suits Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

The North America dominated the market with the largest share, valued at USD 2.51 billion in 2025. It is expected to grow at a significant CAGR during the forecast period, due to stringent safety standards in the industries, NFPA and OSHA requirements, and the presence of a large number of chemical, pharmaceutical, and semiconductor factories and facilities in countries such as the U.S.

- For instance, in October 2025, the U.S. drug maker Merck announced its plans to invest over USD 70 billion in expanding its U.S. manufacturing and research operations in 2025, including a USD 3 billion new pharmaceutical facility in Elkton, Virginia.

Such expansion developments push industries such as healthcare, oil & gas, and chemicals to adopt biohazard suits to ensure worker safety and health. Furthermore, frequent industrial accidents and continuous technological advancements in protective materials are driving strong demand in the U.S. market.

Europe

The Europe market is expected to grow due to the substantial hazardous industrial sector, combined with stringent Personal Protective Equipment (PPE) regulations under Regulation (EU) 2016/425. Moreover, continuous updates to harmonized PPE standards, including powered filtering respiratory devices and face or eye protection, are encouraging buyers to transition to certified, higher-performance CBRN and hazmat suits over legacy equipment. In addition, the OEMs are focused on creating innovation in the design of suits and protective equipment to ensure the reliability and safety of workers, driving market growth in the region.

- For instance, in November 2025, Sioen, a protective clothing company in Belgium, launched Sioen PRO, a new brand focused on multinorm protective clothing that offers certified protection against hazards such as heat, flame, electric arc, chemicals, and cold.

Asia Pacific

The Asia Pacific market is experiencing rapid growth driven by the expansion of chemical, electronics, battery, and pharmaceutical manufacturing sectors that demand certified protective clothing. Therefore, India’s expanding chemical industry and regulatory focus on workplace safety drive product demand during the forecast period. Moreover, manufacturers conduct strategic partnerships to support the growth of the market by enhancing the availability of stringent safety-certified products.

- For instance, in May 2022, Kappler and Lakeland Industries, Inc. partnered to expand high-level chemical worker protection in India by combining Kappler’s NFPA-certified hazmat suits with Lakeland’s established local manufacturing and distribution network.

Latin America

The demand for hazmat suits in Latin America is primarily driven by exposure to high-risk industries such as petrochemicals, oil & gas, mining, fertilizers, and industrial chemicals, coupled with the steady adoption of labor and safety regulations. Key markets such as Brazil, Mexico, and Argentina are increasingly enforcing PPE compliance in hazardous environments, which drives market growth.

Middle East & Africa

In the Middle East & Africa, the market growth is closely linked to oil & gas, petrochemicals, large industrial projects, and expanding CBRN defense capabilities. Gulf states are investing heavily in civil defense and military CBRN protection, while national oil companies and contractors require robust chemical protective clothing for refinery, propelling the market growth.

- For instance, in March 2024, Abu Dhabi’s Tawazun Council announced defence contracts worth USD 2.77 billion, including a USD 33.03 million agreement with local company Trust to supply CBRN protective suits.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Innovation, Adoption of Advanced Materials and Protective Technologies Drive Competitive Dynamics in the Market

The market is moderately consolidated with leading global manufacturers such as DuPont, Lakeland Industries, Inc., Ansell, Kappler, Dräger, Avon Protection, Honeywell International Inc., Respirex, and others. These companies provide strong product portfolios in chemical, biological, radiological, and industrial protective equipment. Such companies use regulatory expertise, extensive distribution networks, and a broad product range to serve the protective apparel or equipment needs of diverse industries.

To increase market share, key players are heavily investing in advanced technologies, breathable and lightweight and strong materials, integrated CBRN systems, and designs to improve user comfort and operational endurance. Strategic partnerships with defense, fire, healthcare, and industrial organizations are being formed to validate innovations and secure long-term contracts. Moreover, the manufacturers expand global production, enhance certification capabilities, and strengthen digital sales channels to meet growing demand for products from various industries and organizations.

LIST OF KEY HAZMAT SUITS COMPANIES PROFILED:

- DuPont (U.S.)

- Lakeland Industries, Inc. (U.S.)

- Ansell Limited (Australia)

- Kappler, Inc. (U.S.)

- Respirex International Ltd. (U.K.)

- Drägerwerk AG & Co. KGaA (Germany)

- Avon Protection plc (U.K.)

- Honeywell International Inc. (U.S.)

- OPEC CBRNe Ltd. (U.K.)

- Uvex Arbeitsschutz GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS:

- March 2025: Merseyside Fire & Rescue Service in the U.K. awarded a supply contract for CBRN chemical protective suits, covering one-piece gas-tight suits with integrated gloves, boots, and visors for hazmat and CBRN incidents.

- January 2025: DuPont announced the launch of Tychem 6000 SFR lightweight hooded coverall, designed to provide chemical protection against >250 chemicals plus secondary flame resistance.

- July 2024: Ansell announced its acquisition of Kimberly-Clark’s Personal Protective Equipment (KCPPE) business to expand the portfolio of protective clothing and PPE for industrial and scientific users.

- April 2024: Ansell announced a binding agreement to acquire 100% of Kimberly-Clark’s PPE business for USD 640 million, explicitly covering hand and body protection used in cleanroom, healthcare, and industrial environments.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.8% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Protection Level, By Material, By Application, By Component, By End Use, and Region |

|

By Protection Level |

· Level A (Full Body, Highest Protection) · Level B (High Respiratory, Moderate Skin Protection) · Level C (Moderate Skin, Air -Purifying Protection) · Level D (Basic Protection) |

|

By Material |

· Polypropylene (PP) · Polyethylene (PE) · Tyvek · PVC (Polyvinyl Chloride) · Neoprene · Others |

|

By Application |

· Chemical Protection · Biohazard & Infection Control · Radioactive & Nuclear Protection · Firefighting · Others |

|

By Component |

· Outer Shell · Visor/Face Shield · Gloves & Boots · Respirator/Face Mask · Others |

|

By End Use |

· Industrial & Manufacturing · Defense & Military · Healthcare & Emergency Medical Services · Public Safety Agencies · Oil & Gas · Laboratories & Research Institutions · Others |

|

By Distribution Channel |

· Direct Sales · Distributors · Online |

|

By Geography |

· North America (By Protection Level, By Material, By Application, By Component, By End Use, and Country) o U.S. (By End User) o Canada (By End User) · Europe (By Protection Level, By Material, By Application, By Component, By End Use, and Country) o U.K. (By End User) o Germany (By End User) o France (By End User) o Russia (By End User) o Rest of Europe (By End User) · Asia Pacific (By Protection Level, By Material, By Application, By Component, By End Use, and Country) o China (By End User) o Japan (By End User) o India (By End User) o South Korea (By End User) o Rest of Asia Pacific (By End User) · Latin America (By Protection Level, By Material, By Application, By Component, By End Use, and Country) o Brazil (By End User) o Mexico (By End User) o Argentina (By End User) o Rest of Latin America (By Platform) · Middle East & Africa (By Protection Level, By Material, By Application, By Component, By End Use, and Country) o UAE (By End User) o Saudi Arabia (By End User) o South Africa (By End User) o Rest of the Middle East & Africa (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.81 billion in 2025 and is projected to reach USD 13.99 billion by 2034.

In 2025, the market value stood at USD 2.51 billion.

The market is growing at a CAGR of 6.8% during the forecast period of 2026-2034.

The Level C segment led the market by protection level in 2025.

The key factors driving the market are increasing safety concerns and rising incidence of CBRN industrial accidents.

DuPont (U.S.), Lakeland Industries, Inc. (U.S.), Ansell Limited (Australia), and Kappler, Inc. (U.S.), among others are some of the prominent players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us