HDPE Pipes Market Size, Share & Industry Analysis, By Grade (PE 100, PE 80, and PE 63), By End-Use Industry (Municipal/Public Utilities, Agriculture, Oil & Gas, Industrial, Construction, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

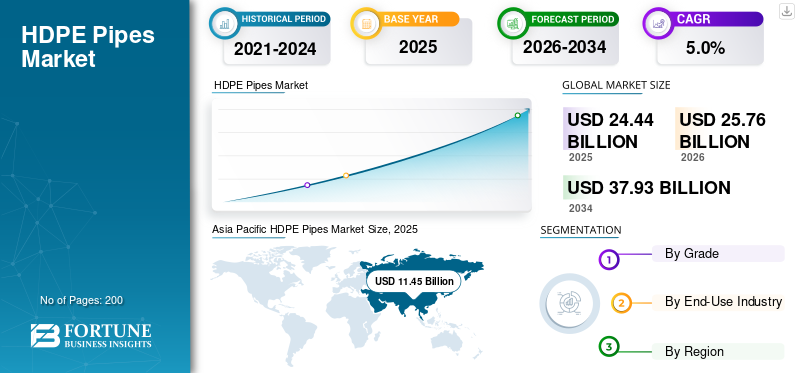

The global HDPE pipes market size was valued at USD 24.44 billion in 2025. The market is projected to grow from USD 25.76 billion in 2026 to USD 37.93 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the global HDPE pipes market with a market share of 46.84% in 2025.

HDPE pipes are plastic pipes made from high-density polyethylene, a tough, flexible polymer used to transport water, wastewater, gas, and industrial fluids. They are valued as they are lightweight, resist corrosion and many chemicals, and can better withstand ground movement than many rigid pipe materials. High-density polyethylene pipes are widely used in municipal water supply, drainage and sewer networks, irrigation systems, gas distribution, and industrial piping, where long service life and low maintenance are important. Growth is also encouraged by the shift toward durable, leak-resistant piping solutions and the need to reduce water losses through better network performance.

The market is largely led by a relatively small set of well-established producers with strong manufacturing scale and long-standing operating experience. Key players such as JM EAGLE, INC., Advanced Drainage Systems, Chevron Phillips Chemical Company LLC., WL Plastics, and Supreme compete through high-capacity production, efficient operations, and consistent supply reliability to serve large infrastructure and utility projects.

Download Free sample to learn more about this report.

HDPE PIPES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 24.44 billion

- 2026 Market Size: USD 25.76 billion

- 2034 Forecast Market Size: USD 37.93 billion

- CAGR: 5.0% from 2026–2034

- Asia Pacific dominated the global HDPE pipes market with a market share of 46.84% in 2025.

- The PE 80 segment is expected to grow at a CAGR of 4.3% over the forecast period.

- The agriculture segment is expected to grow at a CAGR of 4.3% over the forecast period.

North America

North America remains an important regional market for HDPE pipes, with the market valued at USD 4.56 billion in 2025.

Europe

The Europe region is projected to record moderate growth in the market, valued at USD 5.40 billion in 2025.

Asia Pacific

Asia Pacific held the dominant position in the global market in 2025, valued at USD 11.45 billion, and is expected to maintain its leading role in 2026, reaching USD 12.10 billion.

U.S.

The U.S. market in 2025 was valued at USD 3.80 billion, accounting for 83.3% of regional revenues.

Japan

Consumption is supported by a strong municipal infrastructure base, high standards for utility reliability, and consistent investment in pipeline replacement and rehabilitation.

Read More

HDPE PIPES MARKET TRENDS

Growing Shift Toward Leak-Resistant and Long-Life Pipeline Systems to be a New Market Trend

A notable trend in the market is the increasing preference for long-life, leak-resistant piping solutions in municipal and utility networks. Project owners are placing greater emphasis on sustainable, lower-maintenance costs and on improving network reliability throughout the pipeline's full life. This supports higher adoption of HDPE pipes as they are corrosion-resistant and can deliver strong joint integrity when properly installed. As a result, suppliers and contractors are focusing more on quality consistency, installation performance, and standardized practices that improve long-term pipeline reliability.

- According to an International Water Association (IWA) study, global non-revenue water is estimated at 126 billion m³ per year, highlighting the large scale of water losses that is pushing utilities toward leak-reducing, long-life pipe networks, including HDPE.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Infrastructure and Utility Networks Drive HDPE Pipes Demand

Demand for HDPE pipes is strongly driven by ongoing investment in water supply, sewerage, and drainage systems, as well as gas distribution networks. High-density polyethylene pipes are widely used in these applications as they are lightweight, corrosion-resistant, and offer a long service life, helping reduce maintenance and replacement needs. As cities expand and governments focus on upgrading aging pipelines, HDPE adoption increases for both new installation and replacement projects. Growth in agriculture also supports demand, as high-density polyethylene pipes are commonly used in irrigation systems that require durable and leak-resistant performance.

- According to the U.S. EPA’s 7th Drinking Water Infrastructure Needs Survey and Assessment (DWINSA), drinking-water systems have an estimated USD 629.1 billion in DWSRF-eligible infrastructure needs for 2021–2040, supporting sustained demand for pipe replacement and network expansion, including HDPE.

MARKET RESTRAINTS

Dependence on Construction Spending and Project Delays Restrains Market Growth

The market faces restraint due to its high dependence on construction activity and the timing of large infrastructure projects. Demand is closely linked to municipal budgets, public tender cycles, and private construction spending, so delays in approvals, funding, or project execution can quickly slow the pace of pipe purchases. In many regions, water and drainage upgrades take longer than planned due to permitting, land access issues, and coordination with other utilities, which pushes demand out rather than eliminating it.

- According to the OECD, infrastructure project permitting and approval periods can easily reach or exceed 10 years, delaying the start of utility and construction projects and pushing out near-term demand for high-density polyethylene pipes.

MARKET OPPORTUNITIES

Accelerating Water Management and Irrigation Investments Creates New Opportunities

There are strong HDPE pipes market growth opportunities as countries increase investment in water security, irrigation efficiency, and climate-resilient infrastructure. High-density polyethylene pipes are well-suited for large-scale water transfer, rural and urban distribution lines, and modern irrigation systems as they are corrosion-resistant, flexible, and easier to install across difficult terrain. As agriculture shifts toward drip and micro-irrigation to reduce water losses, demand for reliable HDPE lateral lines and distribution networks increases.

- According to FAO, more than 60% of global irrigated cropland is under high water stress, strengthening the push for more efficient irrigation and water-delivery infrastructure where high-density polyethylene pipes are widely used.

MARKET CHALLENGES

Raw Material Price Volatility Creates Market Challenges

HDPE pipe manufacturers face persistent challenges from polyethylene (PE) resin price volatility, since pipe costs are directly linked to PE input pricing. As a result, fluctuations in oil and gas feedstock markets and changing resin supply conditions can quickly translate into unstable pipe pricing and margin pressure across the value chain.

- According to the U.S. Energy Information Administration (EIA), polyethylene is produced from oil- and gas-based feedstocks such as ethane, price changes in energy market conditions can directly influence PE resin costs and create pricing and margin volatility for HDPE pipe manufacturers.

Segmentation Analysis

By Grade

Higher Strength and Wider Use in Pressure Networks Support Dominance of PE 100 Demand

Based on grade, the market is segmented into PE 100, PE 80, and PE 63.

To know how our report can help streamline your business, Speak to Analyst

The PE 100 grade holds the largest share in the market as it offers higher strength and more dependable long-term performance for demanding pressure applications. Compared with older grades, PE 100 is commonly selected for municipal water supply, gas distribution, and industrial pipelines as it can handle higher operating pressures and, in many cases, achieve the same performance with a thinner wall, which helps reduce material use and installation load.

- According to the PE100+ Association, PE100 pipe material is classified with a Minimum Required Strength (MRS) of 10.0 MPa (vs 8.0 MPa for PE80), supporting its wider use in higher-pressure water and gas pipe applications.

The PE 80 segment is expected to grow at a CAGR of 4.3% over the forecast period.

By End-Use Industry

Large-Scale Water and Sewer Networks Support Biggest Market Share of Municipal/Public Utilities Segment

In terms of end-use industry, the market is categorized into municipal/public utilities, agriculture, oil & gas, industrial, construction, and others.

The municipal/public utilities segment holds the largest HDPE pipes market share, as cities and utilities require large volumes of pipe for water supply, sewer lines, stormwater drainage, and network expansion. HDPE is widely used in these systems due to its corrosion resistance, leak-tight jointing, and long service life, which helps reduce maintenance and replacement needs in buried infrastructure. Demand in this segment is strongly driven by function and scale, as utility networks span long distances and must operate reliably under continuous service conditions, making durable pipe performance a priority for public agencies and contractors.

- According to the Government of India’s AMRUT/AMRUT 2.0 document (PIB), targets for the next 5 years include 1.25 lakh km of water network and 35,866 km of sewer network, showing the scale of municipal pipeline build-out that supports steady HDPE pipe demand.

The agriculture segment is expected to grow at a CAGR of 4.3% over the forecast period.

HDPE Pipes Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

ASIA PACIFIC

Asia Pacific HDPE Pipes Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in the global market in 2025, valued at USD 11.45 billion, and is expected to maintain its leading role in 2026, reaching USD 12.10 billion. The region’s leadership is supported by large-scale urbanization, high infrastructure spending, and sustained investment in municipal water supply, sewerage, stormwater drainage, and irrigation networks. Strong construction activity and ongoing expansion of utility connectivity across fast-growing cities keep demand steady across both pressure and non-pressure pipe applications.

China HDPE Pipes Market

Based on Asia Pacific’s strong contribution and China’s extensive infrastructure footprint, the China market was valued at USD 4.47 billion in 2025, accounting for 39.0% of regional revenues. Demand is supported by large municipal pipeline programs, ongoing urban redevelopment, and continuous expansion of industrial parks and utility corridors. China also has a strong domestic resin-to-pipe manufacturing ecosystem, which supports large-scale supply for drainage, water transmission, and gas distribution projects.

India HDPE Pipes Market

The Indian market in 2025 was valued at around USD 2.79 billion. Demand is driven by expanding water supply coverage, sanitation infrastructure development, and rising adoption of modern irrigation systems across agricultural states. Public investment in municipal water networks and sewerage systems, combined with robust housing and road development, supports steady demand for HDPE pipes across both urban and semi-urban areas.

NORTH AMERICA

North America remains an important regional market for HDPE pipes, with the market valued at USD 4.56 billion in 2025. Demand is supported by steady spending on water infrastructure upgrades, water management systems, drainage systems, and ongoing replacement of aging pipelines across cities and counties. The region also benefits from a well-established base of pipe manufacturers and resin supply chains, which helps maintain reliable availability for municipal, industrial, and construction projects.

U.S. HDPE Pipes Market

The U.S. market in 2025 was valued at USD 3.80 billion, accounting for 83.3% of regional revenues. Demand is driven by large-scale municipal water and sewer rehabilitation, widespread use of HDPE corrugated drainage pipe in transportation and site development, and ongoing utility network expansion.

EUROPE

The Europe region is projected to record moderate growth in the market, valued at USD 5.40 billion in 2025. The region is shaped by strict building standards, strong sustainability expectations, and a steady shift toward long-life infrastructure materials that reduce maintenance and leakage risk. Demand is supported by the continuous renewal of aging water and wastewater networks, upgrades to drainage and flood management systems, and ongoing residential and commercial construction activity.

Germany HDPE Pipes Market

Germany’s market reached a valuation of approximately USD 1.01 billion in 2025, accounting for 18.8% of regional demand. Consumption is supported by a strong municipal infrastructure base, high standards for utility reliability, and consistent investment in pipeline replacement and rehabilitation.

Italy HDPE Pipes Market

The Italy’s market in 2025 was valued at USD 0.36 billion, representing roughly 6.6% of regional revenues. Demand is driven by ongoing upgrades to municipal water and wastewater networks, drainage requirements linked to transport and urban development projects, and rehabilitation needs in older cities where pipeline replacement is a recurring requirement.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa regions are expected to experience moderate market growth during the forecast period. The Latin America market reached a valuation of USD 1.03 billion in 2025, supported by water supply upgrades, sanitation expansion, irrigation networks, and drainage needs tied to housing and transport projects. The Middle East & Africa market reached a valuation of USD 2.01 billion in 2025, supported by urban expansion, desalination-linked water transmission, and large utility and industrial corridor projects that require long-life, corrosion-resistant piping.

Brazil HDPE Pipes Market

The Brazilian market in 2025 was valued at USD 0.42 billion, accounting for 41.2% of Latin America revenues. Demand is driven by municipal water distribution improvements, sanitation infrastructure build-out, and strong use of HDPE in drainage and stormwater systems. Irrigation and water-transfer needs in agriculture also support steady consumption.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management to Shape Competition in Market

The market is relatively consolidated and capital-intensive, as large-scale production requires high-capacity extrusion lines, robust quality control systems, and compliance with stringent product and safety standards. The need for significant upfront investment, along with qualification requirements for municipal and utility projects, limits new entrants.

JM EAGLE, INC., Advanced Drainage Systems, Chevron Phillips Chemical Company LLC., WL Plastics, and Supreme mainly concentrate on improving operational efficiency, upgrading product performance, and strengthening upstream integration rather than aggressively expanding capacity.

LIST OF KEY HDPE PIPES COMPANIES PROFILED IN REPORT

- JM EAGLE, INC. (U.S.)

- WL Plastics (U.S.)

- Chevron Phillips Chemical Company LLC. (U.S.)

- Advanced Drainage Systems. (U.S.)

- Prinsco, Inc. (U.S.)

- Lane Enterprises, LLC. (U.S.)

- AGRU (Austria)

- Deriplast Group. (Italy)

- Jain Irrigation Systems Ltd. (India)

- Supreme (India)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Advanced Drainage Systems. signed an agreement to acquire NDS (National Diversified Sales) from NORMA Group, expanding its stormwater and water-management portfolio that closely complements ADS’s core plastic pipe and drainage business where corrugated HDPE pipe is a key material.

- August 2025: Supreme completed the acquisition of Orbia Building & Infrastructure (Wavin) pipes & fittings business in India, adding a larger pipes/fittings footprint that supports its plastic pipe leadership, including HDPE ranges used across water and infrastructure.

- May 2025: Advanced Drainage Systems. acquired River Valley Pipe, adding pipe manufacturing capacity in the U.S. Midwest, a direct adjacency to ADS’s plastic drainage/pipe platform, including HDPE pipe products.

- October 2024: Lane Enterprises, LLC. opened a new plastic pipe production facility in Longview, Washington, with lines producing corrugated HDPE pipe and plans to add more capacity.

- February 2024: Chevron Phillips Chemical Company LLC. (U.S.) and QatarEnergy began construction of a Ras Laffan integrated polymers complex that includes HDPE units. This upstream expansion supports long-term polyethylene supply used in pipe-grade resins and PE pipe systems.

- October 2023: Prinsco, Inc. moved forward with a new Valdosta, Georgia, manufacturing center designed to run multiple lines for the expansion of the corrugated HDPE pipe stormwater market.

REPORT COVERAGE

The global HDPE pipes market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.0% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Grade, End-Use Industry, and Region |

|

By Grade |

· PE 100 · PE 80 · PE 63 |

|

By End-Use Industry |

· Municipal/Public Utilities · Agriculture · Oil & Gas · Industrial · Construction · Others |

|

By Region |

· North America (By Grade, End-Use Industry, and Country) o U.S. (By End-Use Industry) o Canada (By End-Use Industry) · Europe (By Grade, End-Use Industry, and Country) o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o Italy (By End-Use Industry) o France (By End-Use Industry) o Rest of Europe (By End-Use Industry) · Asia Pacific (By Grade, End-Use Industry, and Country) o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry) · Latin America (By Grade, End-Use Industry, and Country) o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America(By End-Use Industry) · Middle East & Africa (By Grade, End-Use Industry, and Country) o Saudi Arabia (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of the Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 24.44 billion in 2025 and is projected to reach USD 37.93 billion by 2034.

Recording a CAGR of 5.0%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The municipal/public utilities end-use industry segment led in 2025.

Asia Pacific held the highest market share in 2025.

Rising investment in municipal water, sewer, drainage, and gas distribution infrastructure, which increasingly uses HDPE pipes for durable, corrosion-resistant pipeline networks, is the key driver of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us