Healthcare ERP Market Size, Share & Industry Analysis, By Component (Software/Platforms and Services), By Deployment (Cloud-Based, On-Premise, and Hybrid), By Application (Financial Management, Procurement & Supplier Management, Inventory & Warehouse Management, Human Capital Management, Planning, Forecasting & Analytics, and Others), By End User (Hospitals & ASCs, Specialty Clinics, Diagnostic & Imaging Centers, Long-Term Care Facilities, and Others), and Regional Forecast, 2026-2034

Healthcare ERP Market Size and Future Outlook

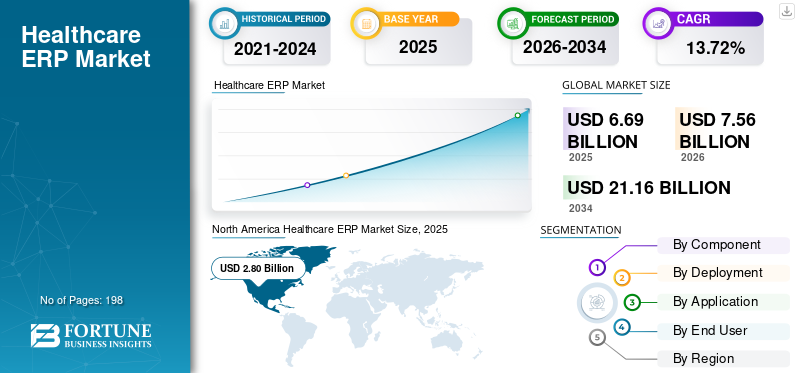

The global healthcare ERP market size was valued at USD 6.69 billion in 2025. The market is projected to grow from USD 7.56 billion in 2026 to USD 21.16 billion by 2034, exhibiting a CAGR of 13.72% during the forecast period. North America dominated the healthcare ERP market with a market share of 41.85% in 2025.

The global market includes enterprise software solutions utilized by hospitals, healthcare systems, specialty clinics, diagnostic facilities, and other provider entities to oversee finance, procurement, supply chain, inventory, human resources, and planning processes in a cohesive setting. The market is influenced by increasing demand for cloud-based ERP implementation, heightened emphasis on cost management and operational efficiency, a greater necessity for workforce and payroll oversight, and the ongoing modernization of procurement, inventory, and analytical operations. Market growth is further aided by the transition from disparate back-office solutions to unified platforms that link financial, administrative, and operational functions across multi-location healthcare systems.

Key players operating in the global market include Oracle, Infor, SAP SE, and Microsoft. These companies are focusing on cloud-based ERP suites, connected finance and supply chain workflows, embedded analytics, workforce management, and automation capabilities that help healthcare organizations improve visibility, strengthen compliance, reduce manual burden, and support enterprise-wide decision-making.

Download Free sample to learn more about this report.

Healthcare ERP Market Key Takeaways

- 2025 Market Size: USD 6.69 billion

- 2026 Market Size: USD 7.56 billion

- 2034 Forecast Market Size: USD 21.16 billion

- CAGR: 13.72% from 2026-2034

- North America dominated the healthcare ERP market with a 41.85% share in 2025.

- The services segment is projected to grow at a CAGR of 14.89% during the forecast period.

- The hybrid segment is anticipated to register a CAGR of 14.65% over the forecast period.

North America

North America maintained its leading position in 2025 with a market value of USD 2.80 billion.

Europe

Europe is expected to expand at a CAGR of 12.32% during the forecast period.

Asia Pacific

Asia Pacific is projected to reach USD 1.73 billion by 2026, making it the fastest-growing regional market.

U.S.

The market is projected to reach USD 2.72 billion by 2026, accounting for approximately 36.0% of global sales.

Japan

The market is estimated to reach around USD 0.35 billion by 2026, representing roughly 4.7% of global revenues.

Read More

HEALTHCARE ERP MARKET TRENDS

Growing Integration of Artificial Intelligence in Healthcare ERP is a Significant Market Trend Observed

The growing incorporation of artificial intelligence in healthcare ERP is a significant market trend, as providers are progressively leveraging AI to enhance the efficiency, precision, and decision-making in finance, procurement, inventory, and workforce processes. AI assists healthcare organizations in automating routine tasks, forecasting supply requirements, minimizing manual errors, identifying spending discrepancies, and enhancing oversight across multiple sites. This is particularly crucial in healthcare since hospitals and provider organizations face pressure to manage expenses, address labor shortages, and prevent supply interruptions while ensuring service quality. With ERP platforms increasingly shifting to cloud environments and accumulating abundant data, vendors are integrating AI directly into enterprise processes rather than providing it as an independent tool. This enhances the product’s worth as an operational intelligence platform, transcending mere record-keeping, and promotes quicker adoption of next-generation solutions, thereby supporting the overall global healthcare ERP market growth.

- For instance, in September 2025, Oracle introduced AI-powered capabilities within Oracle Fusion Cloud Applications for healthcare organizations to strengthen supply chain operations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Digital Transformation in Healthcare Systems is Driving Market Growth

The surge in digital transformation within healthcare systems is a key market catalyst, as hospitals and provider networks face increasing pressure to enhance operational efficiency, diminish administrative workload, manage costs, and link fragmented processes. As healthcare organizations upgrade their finance, procurement, supply chain, workforce, and analytics operations, they are increasingly requiring integrated ERP systems rather than separate legacy tools. Digital transformation enhances enterprise-wide visibility, accelerates decision-making, and enables scalable management across multi-site healthcare systems. This capability is particularly crucial as providers encounter workforce shortages, squeezed margins, and increasing need for immediate operational data. Consequently, adoption of healthcare ERP is increasing, as these platforms convert wider digital transformation objectives into quantifiable enhancements in operational efficiency and back-office performance.

- For instance, in January 2025, Johns Hopkins selected Workday as part of its Sightline business modernization program. The implementation includes Workday Human Capital Management, Workday Financial Management, Workday Supply Chain Management for Healthcare, and Workday Grants Management, aimed at modernizing HR and financial processes across the Johns Hopkins Health System and University.

MARKET RESTRAINTS

High Cost of Implementation to Limit Market Growth

Significant implementation expenses remain a major limitation in the healthcare ERP market, as installations typically entail far more than just acquiring software. Hospitals frequently require system integration, data migration, workflow redesign, staff training, testing, compliance validation, and the decommissioning of legacy systems, all of which can greatly increase overall project expenses. This complexity is particularly pronounced in healthcare environments, where organizations function across various departments, locations, and very sensitive data settings. Smaller hospitals, specialized providers, and financially limited public systems might postpone or reduce the scope of ERP projects when initial costs are excessively high. Extended deployment timelines also elevate financial risk, as organizations need to finance consulting, internal project teams, and change management efforts before realizing complete value. Consequently, substantial implementation expenses can hamper adoption, particularly in less developed or budget-conscious markets.

MARKET OPPORTUNITIES

Rising Demand for Unified Data Management Solutions to Offer Several Growth Opportunities

Growing demand for unified data management solutions presents a significant market opportunity, as healthcare providers increasingly seek a single platform that integrates financial, supply chain, workforce, and operational data rather than depending on disjointed legacy tools. When data resides in isolated systems, hospitals encounter delayed reporting, poor visibility among departments, redundant records, and increased manual reconciliation. Integrated data management enables providers to develop a cohesive perspective of business operations, enhancing decision-making, bolstering regulatory compliance, and assisting across multi-site networks. This chance is growing as healthcare ERP providers enhance cloud-based systems that integrate finance, staffing, procurement, inventory, and analytics into a single framework. For instance, Infor highlights that its healthcare cloud suite consolidates clinical, financial, supply chain, and operational data, reflecting a broader market shift toward integrated data systems.

For instance, in December 2025, Oracle announced that healthcare organizations, including Regency Integrated Health Services, are using Oracle Fusion Cloud Applications to replace disparate business systems with an integrated suite of applications.

MARKET CHALLENGES

Resistance to Digital Transformation Among Healthcare Staff Poses a Prominent Challenge to Market Growth

Healthcare staff resistance to digital transformation poses a significant market challenge, as ERP modernization alters daily workflows for finance teams, supply personnel, HR teams, and operational managers, who frequently face staffing shortages and high workloads. When new systems necessitate retraining, process overhaul, and alterations in approvals, reporting, or scheduling, employees may be concerned about short-term disruptions, productivity declines, or increased complexity. This resistance can slow deployment timelines, raise change management expenses, and postpone the complete achievement of ERP benefits. According to the American Hospital Association 2025 Health Care Workforce Scan, swift technological change is a significant force influencing the healthcare workforce, indicating how the digital shift itself can become a challenge for providers from the staff side. In healthcare settings, successful adoption relies on IT teams and on widespread acceptance among administrative and operational users. Consequently, staff reluctance and adjustment fatigue may diminish implementation momentum, particularly in large, multi-site healthcare systems, thereby affecting market growth.

Segmentation Analysis

By Component

Software/Platforms Segment Dominated the Market Owing to Its Central Role in Managing Core Enterprise Workflows

In terms of component, the market is divided into software/platforms and services.

The software/platforms segment captured the dominant global healthcare ERP market share in 2025, as the platform layer forms the core of every deployment and captures the largest share of enterprise spending across finance, procurement, inventory, workforce, and planning functions. Healthcare providers usually invest first in the main ERP system as it serves as the system of record for operational and administrative workflows across multiple departments and sites. The segment also benefits from rising migration toward cloud-based integrated suites, which help providers replace fragmented legacy tools with a unified environment. In addition, software platforms support automation, analytics, AI-enabled workflows, and real-time visibility, making them more central to long-term digital transformation initiatives than standalone services.

- For instance, in December 2025, Oracle announced that healthcare organizations, including Billings Clinic-Logan Health, Children’s Hospital Los Angeles, and Regency Integrated Health Services, are implementing Oracle Fusion Cloud Applications to streamline finance, HR, supply chain, and customer experience processes in the cloud.

The services segment is anticipated to rise with a CAGR of 14.89% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Cloud-Based Segment Dominated the Market Due to Its Ability to Provide Real-Time Data Access

Based on deployment, the market is classified into on-premise, cloud-based, and hybrid.

The cloud-based segment captured the leading position in the global market in 2025, driven by the growing preference among healthcare providers for systems that are easier to deploy, scale, and update across multiple facilities. Cloud-based ERP systems reduce dependence on heavy in-house infrastructure and help hospitals standardize finance, HR, procurement, and supply chain workflows more efficiently. These systems also provide real-time data access, easier system upgrades, and better visibility across distributed provider networks. This is especially important as healthcare organizations try to replace fragmented legacy tools with more connected enterprise platforms while controlling IT costs. Furthermore, the segment is set to hold 51.5% share by 2026.

- For instance, in September 2025, NYC Health + Hospitals announced plans to upgrade to Oracle Fusion Cloud Applications to consolidate finance, supply chain, and HR processes across its system.

The hybrid segment is anticipated to rise with a CAGR of 14.65% over the forecast period.

By Application

Financial Management Segment Dominated the Market Due to Its Core Operational Importance

On the basis of application, the market is divided into financial management, procurement & supplier management, inventory & warehouse management, human capital management, planning, forecasting & analytics, and others.

In 2025, the financial management segment led the market, as finance is typically the primary and most crucial area that providers aim to optimize through ERP adoption. Hospitals and healthcare organizations require improved management of budgeting, reporting, accounts payable, cash flow, and overall expenditures, particularly amid ongoing cost pressures and margin constraints. Financial management tools assist organizations in minimizing manual tasks, enhancing reporting precision, and providing leaders with a clearer perspective on performance across various departments and locations. As these functions are crucial for day-to-day activities and future planning, providers frequently implement finance modules prior to branching out into additional ERP applications. Furthermore, the segment is set to hold 27.7% share by 2026.

- For instance, in February 2024, Apollo Health & Lifestyle Limited selected Oracle Fusion Cloud ERP to optimize financial operations, improve reporting speed and accuracy, align financial and operational planning, and strengthen decision-making.

The human capital management segment is anticipated to rise with a CAGR of 15.43% over the forecast period.

By End User

Hospitals & ASCs Segment Dominated the Market Due to High Operational Complexity

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, diagnostic & imaging centers, long-term care facilities, and others.

The hospitals & ASCs segment dominated the market in 2025, as these organizations handle the highest volume of financial, workforce, procurement, and inventory operations. Hospitals and outpatient surgical centers manage intricate daily operations across various departments, locations, vendors, and staff teams, requiring more robust enterprise systems than smaller healthcare providers. They are under ongoing pressure to enhance cost management, standardize processes, and improve transparency across finance, HR, and supply chain operations. As a result, hospitals and ASCs typically emerge as the primary and largest purchasers of healthcare ERP systems. Furthermore, the segment is set to hold 57.5% share by 2026.

- For instance, in March 2026, Monash Health, Victoria’s largest health service, announced that it is using Oracle Fusion Cloud Applications to move finance and supply chain operations to the cloud, improving efficiency, strengthening controls, and supporting patient care.

The diagnostic & imaging centers segment is expected to grow at a CAGR of 15.22% during the forecast period.

Healthcare ERP Market Regional Outlook

By geography, the market is divided into Latin America, Asia Pacific, Europe, North America, and the Middle East & Africa.

North America

North America Healthcare ERP Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global market, with a value of USD 2.48 billion in 2024 and maintained its leading position in 2025, with USD 2.80 billion. The region is expanding due to a continued increase in digital and IT budgets, a strong focus on operational efficiency, cost control, workforce management, and modernization of legacy enterprise systems. Additionally, the region benefits from high ERP awareness, strong cloud readiness, and the presence of major vendors and implementation partners.

U.S. Healthcare ERP Market

The U.S. market led the North American region and is projected to be approximately USD 2.72 billion by 2026, representing about 36.0% of the global sales.

Europe

Europe is poised to grow at a CAGR of 12.32% during the forecast period. The region is experiencing a significant digital health transformation across healthcare systems, propelled by strong policy support, modernization of the public sector, and an increasing adoption of eHealth services. Growth is further supported by the need to enhance interoperability, fortify financial and workforce management, and modernize disjointed administrative systems across nations.

U.K Healthcare ERP Market

The U.K. market is estimated to reach around USD 0.36 billion by 2026, representing roughly 4.8% of global revenues.

Germany Healthcare ERP Market

Germany’s market size is projected to reach approximately USD 0.42 billion by 2026, equivalent to around 5.6% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 1.73 billion by 2026 and is expected to be the fastest-growing region. Growth is driven by large-scale genomics expansion, growing biotech investment, and rising adoption of AI and precision medicine.

Japan Healthcare ERP Market

The Japanese market is estimated to reach around USD 0.35 billion by 2026, accounting for roughly 4.7% of global revenues.

China Healthcare ERP Market

China’s market is projected to reach around USD 0.50 billion by 2026, representing roughly 6.7% of global sales.

India Healthcare ERP Market

The Indian market is estimated to touch around USD 0.24 billion by 2026, accounting for roughly 3.1% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa markets are anticipated to grow at a slower pace over the forecast period. Growth in these regions is supported by increasing investment in digital infrastructure, ongoing modernization of healthcare provider operations, and rising demand for more efficient health systems. The Latin American market is estimated to reach around USD 0.37 billion by 2026.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.11 billion by 2026, representing about 1.4% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Focus on Technological Advancements to Strengthen Their Market Position

The global market represents a moderately concentrated structure, with large enterprise software vendors holding a strong competitive position. Oracle, Infor, Workday, Inc., SAP SE, and Microsoft are some of the prominent participants in the market, supported by broad product portfolios across finance, procurement, supply chain, workforce, and planning functions. These companies benefit from established relationships with large hospitals and health systems, strong cloud capabilities, and the ability to deliver integrated platforms instead of fragmented back-office tools.

- For instance, in May 2025, Kuwait Hospital announced a collaboration with SAP to enhance innovation in the healthcare sector, including the use of SAP SuccessFactors to improve HR and digital workforce capabilities.

Other significant market players include Acumatica, Inc., Epicor Software Corporation, Unit4, and Aptean. These firms are anticipated to focus on product improvement, workflow automation, and technological advancements to strengthen their market position throughout the forecast period.

LIST OF KEY HEALTHCARE ERP COMPANIES PROFILED

- Oracle (U.S.)

- Infor (U.S.)

- SAP SE (Germany)

- Microsoft (U.S.)

- Sage Group plc (U.K.)

- Acumatica, Inc. (U.S.)

- Epicor Software Corporation (U.S.)

- Unit4 (Netherlands)

- Aptean (U.S.)

- Workday, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Workday announced that Fairview Health Services selected Workday’s full suite of HR, finance, and supply chain solutions to replace aging business systems and create a more modern operating platform.

- January 2026: Oracle announced that Alrajhi Medicine in Saudi Arabia is implementing Oracle Fusion Cloud Applications alongside Oracle Health tools to modernize healthcare operations.

- November 2025: Workday announced that Advocate Health, the third-largest U.S. not-for-profit health system, is unifying HR, finance, and supply chain on Workday’s AI-powered platform.

- April 2025: Sage announced new software innovations for healthcare in partnership with Wipfli, extending Sage Intacct’s healthcare capabilities.

- October 2024: Oracle introduced RFID for Replenishment in Oracle Fusion Cloud Inventory Management to help healthcare customers automate stock capture, track locations, and trigger restocking.

REPORT COVERAGE

The global healthcare ERP market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. It provides an understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, and key dhevelopments in the industry within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.72% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 6.69 billion in 2025 and is projected to reach USD 21.16 billion by 2034.

In 2025, the market value stood at USD 2.80 billion.

The market is expected to exhibit a CAGR of 13.72% during the forecast period.

By component, the software/platforms segment is expected to lead the market.

Increasing digital transformation in healthcare systems, along with rising demand for integrated data management solutions, are primarily driving market expansion.

Oracle, Infor, SAP SE, and Microsoft are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us