Healthcare Payer Network Management Market Size, Share & Industry Analysis, By Offering (Software and Services), By Deployment (Cloud Based, On Premise, and Hybrid), By Application (Provider Credentialing Management, Provider Contracting Management, Provider Data Management, Claims Management, Provider Network Management, Reporting & Analytics, and Others), and Regional Forecast, 2026-2034

Healthcare Payer Network Management Market Size and Future Outlook

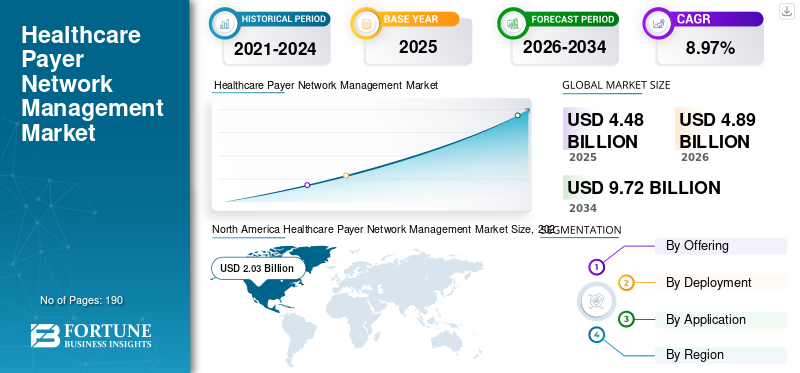

The global healthcare payer network management market size was valued at USD 4.48 billion in 2025. The market is projected to grow from USD 4.89 billion in 2026 to USD 9.72 billion by 2034, exhibiting a CAGR of 8.97% during the forecast period. North America dominated the healthcare payer network management market with a market share of 45.31% in 2025.

The global market is expected to grow steadily in the coming years, driven by the rising need among health insurers to manage complex provider networks more accurately and efficiently. As payer organizations handle large volumes of provider data, contracts, credentialing records, and compliance requirements, the demand for digital network management platforms continues to increase. These solutions help reduce administrative burden, improve provider data accuracy, strengthen regulatory compliance, and support better coordination between payers and providers. In addition, the shift toward automation, cloud-based workflows, and AI-enabled data management is further supporting market expansion across the healthcare payer ecosystem.

- For instance, in April 2025, HealthEdge announced the launch of its AI-driven Provider Data Management solution to help health plans automate the maintenance of accurate, up-to-date provider information.

Leading industry players, such as CitiusTech, Quest Analytics, Availity, and HiLabs, are expanding their offerings to boost their market position.

Download Free sample to learn more about this report.

HEALTHCARE PAYER NETWORK MANAGEMENT MARKET TRENDS

Rising Shift Toward AI-enabled Provider Data Management is Emerging as a Key Market Trend

The global healthcare payer network management market is witnessing a growing shift toward AI-enabled provider data management, as health plans face increasing pressure to maintain accurate provider records across contracting, credentialing, directory management, and compliance workflows. When payer organizations rely on fragmented, manually updated provider data, they increase the risk of inaccurate directories, delayed provider onboarding, payment errors, and regulatory issues. As a result, payers are increasingly adopting AI-driven platforms that can unify provider information, automate validation, and improve data accuracy at scale. This shift is strengthening network efficiency, improving member access, and making provider network operations more reliable, boosting market expansion.

- For instance, in October 2025, CertifyOS launched Provider Hub, a provider data management platform designed to eliminate fragmentation and reduce costs by creating a single source of truth for health plans and digital health companies. This launch highlights how vendors are increasingly focusing on AI-enabled and centralized provider data infrastructure to help payers improve network management performance.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Need to Improve Provider Data Accuracy to Drive Market Growth

The growing need to improve provider data accuracy is a major driver of the market, as health plans rely on accurate provider information to manage networks efficiently and meet compliance requirements. When provider records are outdated, incomplete, or inconsistent, it can lead to directory errors, delayed onboarding, claims issues, and a higher administrative burden. As a result, payers are increasingly adopting network management and provider data platforms that can automate updates, improve data exchange, and create a more reliable provider information system. This trend is increasing demand in the healthcare payer network management market, as accurate and up-to-date provider data helps payers improve operational efficiency, strengthen network adequacy, reduce administrative errors, and enhance member access to care.

Moreover, key companies are focusing on regulatory approvals and new product launches to strengthen their market position.

- For instance, in October 2025, CertifyOS partnered with Candor Health across all addresses through an integrated, end-to-end provider data management solution. The partnership was created to deliver a more accurate, intelligent, and scalable provider data management solution for the healthcare industry. This kind of development reflects vendors' active efforts to address payer demand for more accurate provider data, supporting the growth in the healthcare payer network management market.

MARKET RESTRAINTS

Persistent Provider Data Inaccuracy and Fragmentation Are Limiting Operational Efficiency, Restraining Market Growth

The market is constrained by persistent provider data inaccuracy and fragmentation, as payer organizations still rely on provider information that is often scattered across disconnected systems and not updated in real time. When provider data remains incomplete, duplicated, or outdated, it becomes difficult for health plans to manage provider directories, validate network participation, assess adequacy, and support smooth payer-provider workflows. This increases administrative burden, creates confusion for members, and reduces confidence in network management platforms. As a result, even though demand for these solutions is rising, fragmented and inaccurate provider data continues to slow implementation efficiency and limit the full impact of network management investments.

- For instance, in October 2025, the HHS Office of Inspector General published a data brief that found many Medicare Advantage and Medicaid managed care plans had limited behavioral health provider networks and included inactive providers on their network lists. The report noted that 72% of inactive in-network behavioral health providers should not have been listed as available, showing how inaccurate and fragmented provider data can create “ghost networks” and weaken network reliability.

MARKET OPPORTUNITIES

Rising Adoption of AI for Provider Data Management to Fuel Industry Growth

AI-based provider data automation is emerging as a strong market opportunity as payer organizations are under pressure to manage large provider networks more quickly, accurately, and with greater operational control. When provider data is handled through fragmented, manual processes, it increases the risk of directory errors, delayed updates, inefficient onboarding, and poor network planning. As a result, payers are showing greater interest in AI-enabled platforms that can automate validation, improve provider data exchange, and support more intelligent network optimization. This is creating growth opportunities for vendors that can help health plans build cleaner provider data foundations and manage networks more efficiently at scale.

- For instance, in August 2025, Atlas Systems partnered with SonderMind to automate provider-payer data exchange through its AI-enabled, FHIR-compatible PRIME platform. The platform supported onboarding, data validation, ongoing monitoring, credentialing, roster reconciliation, and mock audits, all of which are directly linked to the efficiency of payer network management. This kind of partnership shows how AI-based provider data automation is opening up new market opportunities by helping payers improve network operations and reduce administrative friction.

MARKET CHALLENGES

Slow Credentialing and Enrollment Cycles to Challenge Market Growth

Slow credentialing and enrollment cycles represent a major market challenge, as payer network management depends on providers being onboarded, verified, and activated promptly. When these processes take too long, health plans face delays in expanding networks, providers experience slower time-to-revenue, and patients may face access limitations due to incomplete or delayed network availability. This also increases administrative workload, creates workflow bottlenecks, and weakens the overall efficiency of network operations. As a result, even when payers invest in network management solutions, slow credentialing and enrollment timelines can limit operational gains and pose a challenge to the global healthcare payer network management market growth.

- For instance, in January 2026, Medallion released its 2026 State of Payer Enrollment and Medical Credentialing Report, which described a widening operational crisis in healthcare, stating that credentialing and enrollment delays are increasingly tied to revenue leakage, rising provider churn, and burnout across the healthcare ecosystem. This highlights how prolonged onboarding and enrollment cycles continue to create friction in provider network operations, presenting a clear challenge for market growth.

Segmentation Analysis

By Offering

Software Segment Led the Market due to Rising Demand for Core Payer Network Management Applications

Based on offering, the market is categorized into software and services.

The software segment dominated the market as payer network management is fundamentally driven by technology platforms that automate provider lifecycle workflows such as credentialing, contracting, provider data updates, directory management, and compliance monitoring. As health plans seek to reduce manual intervention and manage network operations at scale, they increasingly rely on configurable software platforms rather than one-time support services. This creates stronger recurring demand for core payer network management applications, since software becomes the operating backbone for managing provider relationships and network accuracy across the organization. As these activities are ongoing and data-intensive, software holds a larger share of the market than services. Strategic partnership among key companies for software advancement reinforces segmental growth.

- For instance, in August 2025, Newgen Software partnered with Gartner Market Guide for U.S. Healthcare Payers’ Provider Network Management Applications. The company noted that Gartner defines these solutions as payer-specific applications that help manage healthcare provider networks and payer-provider interactions.

The services segment is expected to grow at a CAGR of 6.87% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Cloud Based Segment Dominated due to their Ability to Maintain Legacy Infrastructure

Based on deployment, the market is segmented into cloud based, on premises, and hybrid.

In 2025, the cloud based segment accounted for the largest healthcare payer network management market share as payer organizations increasingly prefer platforms that can be scaled quickly, integrated across multiple workflows, and updated without heavy on-site infrastructure dependency. As provider networks grow larger and more dynamic cloud based solutions help health plans manage high data volumes, connect multiple downstream systems, and support real-time processing more efficiently. This improves flexibility, speeds implementation, and lowers the burden of maintaining legacy infrastructure. As payers are prioritizing modernization, interoperability, and enterprise-scale performance, cloud-based platforms are likely to hold the leading share over on-premise and hybrid models.

Additionally, novel product launches by key companies and the regulatory approvals strengthen their market position.

- For instance, in June 2025, Milliman MedInsight expanded its payer platform through the launch of Payer Insights. The application gives health plan organizations actionable intelligence and broader operational insight through its cloud-based environment.

The hybrid segment is projected to grow at a CAGR of 8.14% over the forecast period.

By Application

Provider Data Management Segment Led due to its Ability to Serves as the Foundation For Almost Every Payer Network Management Function

Based on application, the market is segmented into provider credentialing management, provider contracting management, provider data management, claims management, provider network management, reporting & analytics, and others.

Provider data management dominated the market, as accurate provider data serves as the foundation for almost every payer network management function, including credentialing, contracting, provider directory maintenance, claims accuracy, compliance, and network adequacy assessment. When provider data is incomplete or outdated, it creates downstream problems. As a result, payers are placing greater emphasis on platforms that can clean, validate, unify, and continuously update provider data across the enterprise. Since provider data quality directly affects multiple payer workflows, provider data management is likely the largest application segment in the market.

- For instance, in February 2026, LexisNexis Risk Solutions was named a Leader in the IDC MarketScape: U.S. Provider Data Management for Payers 2025-2026 Vendor Assessment. IDC stated that the company’s commitment to cleansed, high-quality provider data positioned it clearly for payers prioritizing provider data quality at scale. Such recognition reflects the continued priority of provider data management for health plans, supporting the dominance of this application segment.

The reporting & analytics segment is projected to grow at a CAGR of 11.19% over the study period.

Healthcare Payer Network Management Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Healthcare Payer Network Management Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant market share in 2024, reaching USD 1.88 billion, and maintained its leading position in 2025 at USD 2.03 billion. The region is growing strongly as health plans in the U.S. are facing rising pressure to comply with interoperability and prior-authorization requirements while also improving provider data accuracy and payer-to-payer connectivity.

U.S. Healthcare Payer Network Management Market

With North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 2.02 billion by 2026, accounting for roughly 41.42% of the global market.

Europe

Europe is projected to grow at a CAGR of 8.76% over the coming years, the second-highest among all regions. The region is expected to reach a valuation of USD 1.12 billion by 2026. Europe is growing as the European Health Data Space is accelerating cross-border access to patient data and the development of digital health infrastructure.

U.K. Healthcare Payer Network Management Market

The U.K. market is estimated to reach around USD 0.22 billion by 2026, representing roughly 4.47% of the global market.

Germany Healthcare Payer Network Management Market

Germany's market is projected to reach approximately USD 0.24 billion by 2026, equivalent to around 4.86% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 1.01 billion by 2026 and secure the position of the third-largest region of the market. The region is expanding due to rapid digital health adoption, rising medical cost pressure, and growing demand for population health and public health insurance technology modernization.

Japan Healthcare Payer Network Management Market

The Japanese market is estimated to reach around USD 0.21 billion by 2026, accounting for approximately 4.33% of the global market.

China Healthcare Payer Network Management Market

China's market is projected to be one of the largest worldwide, with 2026 revenue estimates around USD 0.32 billion, representing approximately 6.52% of global sales.

India Healthcare Payer Network Management Market

The Indian market is estimated to reach around USD 0.11 billion by 2026, accounting for roughly 2.32% of global revenue.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin American market is set to reach a valuation of USD 0.31 billion by 2026. Latin America is growing as healthcare systems across Central and South America are placing greater focus on interoperability and health data connectivity.

In the Middle East & Africa, the GCC is set to reach USD 0.09 billion by 2026.

South Africa Healthcare Payer Network Management Market

The South African market is projected to reach approximately USD 0.04 billion by 2026, accounting for roughly 0.82% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on New Product Launches to Boost Their Market Share

The global healthcare payer network management market is highly consolidated, with companies such as CitiusTech, Quest Analytics, Availity, HiLabs, LexisNexis Risk Solutions, and HealthStream holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector boost these companies' market share gains.

- For instance, in February 2025, Symplr launched the Symplr Operations Platform (SOP). Built on scalable Amazon Web Services (AWS) cloud infrastructure, the platform helped healthcare CIOs unify disparate systems into a single solution, with standardized processes that are easier to maintain and measure. The symplr Operations Platform empowers healthcare organizations to drive exponential value from their systems while improving operational efficiency across cross-functional teams.

Other notable players in the global market include Kyruus Health and Newgen Software Technologies Limited. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY HEALTHCARE PAYER NETWORK MANAGEMENT COMPANIES

- CitiusTech (U.S.)

- Quest Analytics (U.S.)

- Availity (U.S.)

- HiLabs (U.S.)

- LexisNexis Risk Solutions (U.S.)

- HealthStream (U.S.)

- Verisys (U.S.)

- Newgen Software Technologies Limited (India)

- Kyruus Health. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Office Ally, a leading provider of healthcare technology clearinghouse and software solutions, acquired Jopari Solutions Inc., a leader in straight-through electronic claims processing for Property & Casualty (P&C), Commercial, and Government healthcare.

- February 2026: Verato, the identity intelligence company, announced it will debut new provider identity intelligence innovations and host multiple customer-led sessions at ViVE 2026, taking place February 22–25 at the Los Angeles Convention Center.

- January 2026: Abridge, the leading enterprise-grade AI for clinical conversations collaborated with Availity, the nation’s largest real-time health information network, to launch a first-of-its-kind prior authorization experience. The engagement uses cutting-edge technology grounded in the clinician-patient conversation to facilitate a more efficient process between clinicians and health plans in medical necessity review.

- September 2025: symplr expanded the capabilities of its Operations Platform, unifying provider data previously scattered across multiple systems. By integrating credentialing, privileging, enrollment, scheduling, communication, performance management, and offboarding, symplr's updated platform helps health systems replace disconnected tools with one integrated provider journey.

- April 2025: WNS-HealthHelp, a trusted healthcare technology platform for health plans and a part of WNS, a digital-led business transformation and services company, today announced its strategic collaboration with Availity, North America’s largest real-time health information network.

REPORT COVERAGE

The report provides a detailed global healthcare payer network management market analysis of the market across key segments, including offering, deployment, and application. It examines how payer organizations are adopting network management platforms to improve provider credentialing, contracting, provider data accuracy, claims-linked workflows, and reporting efficiency. The study also covers key market drivers, restraints, opportunities, and challenges influencing industry growth, along with an assessment of emerging technology trends, including cloud adoption, AI-enabled provider data management, and workflow automation. In addition, the report offers regional insights, competitive landscape analysis, and recent company developments to highlight how the market is evolving across different geographies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.97% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, Deployment, Application, and Region |

| By Offering |

|

| By Deployment |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.48 billion in 2025 and is projected to reach USD 9.72 billion by 2034.

In 2025, the market value stood at USD 2.03 billion.

The market is expected to grow at a CAGR of 8.97% over the forecast period.

By offering, the software segment led the market.

Growing need to improve provider data accuracy is the key factor driving the market.

CitiusTech, Quest Analytics, Availity, Inc., HiLabs, and LexisNexis Risk Solutions are the major market players in the global market.

North America dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us