AI-based Clinical Trials Solution Provider Market Size, Share & Industry Analysis, By Component (Software & Services), By Deployment (Cloud-based, On-Premise, & Hybrid), By Technology (Machine Learning & Deep Learning, & Others), By Therapeutic Area (Oncology, Cardiovascular, CNS/Neurology, Immunology & Autoimmune, & Others), By Phase (Phase I, Phase II, Phase III, and Phase IV), By Application (Trial Design and Protocol Optimization, Patient Identification, Recruitment & Retention, Clinical Operations Automation, & Others), By End User, and Regional Forecast, 2026-2034

AI-based Clinical Trials Solution Provider Market Size and Future Outlook

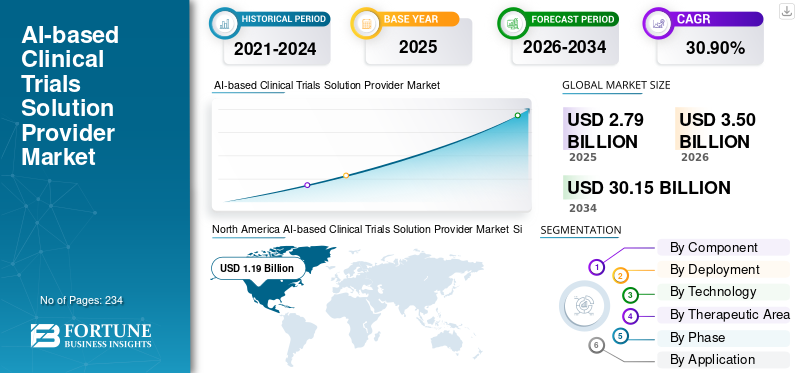

The global AI-based clinical trials solution provider market size was valued at USD 2.79 billion in 2025. The market is projected to grow from USD 3.50 billion in 2026 to USD 30.15 billion by 2034, exhibiting a CAGR of 30.90% during the forecast period. North America dominated the AI-based clinical trials solution provider market with a market share of 42.65% in 2025.

Artificial Intelligence (AI) is increasingly being integrated into clinical trial design, patient recruitment, site selection, monitoring, and data analysis. AI-driven clinical trial platforms help pharmaceutical and biotechnology companies accelerate drug development timelines while improving patient recruitment efficiency and reducing operational costs. Important elements contributing to market growth comprise increasing protocol complexities and financial pressures, ongoing issues with recruitment and retention, heightened use of hybrid and decentralized trial models as well as the necessity to manage substantial amounts of unstructured clinical and safety data with quicker turnarounds and improved compliance oversight.

Major companies such as Medidata (Dassault Systèmes), Veeva Systems, Oracle, and IQVIA are focusing on enhancements in AI-driven trial operations, patient matching, and centralized oversight to boost trial speed, quality, and scalability, in turn fostering increased adoption among sponsor organizations, CROs, and research networks worldwide.

Download Free sample to learn more about this report.

AI-BASED CLINICAL TRIALS SOLUTION PROVIDER MARKET TRENDS

Increasing Shift toward Hybrid/Decentralized Execution is a Remarkable Market Trend

The global market is experiencing a notable transition to hybrid/decentralized trial execution as sponsors and CROs aim to lessen dependence on in-person site visits while maintaining high data quality. Hybrid models integrate in-person clinical evaluations with remote appointments, eConsent, eCOA/ePRO, telehealth, and home nursing, facilitating participation and enhancing recruitment scope. This method also aids in controlling operational risk, thus trials can persist even when travel, staffing, or site limitations are imposed. With trials producing more ongoing patient data, teams increasingly require AI-driven workflows to assess signals, identify non-compliance, and prioritize monitoring actions. The overall result is an increased need for platforms that coordinate participant involvement, enable remote data collection, and provide centralized monitoring across different regions. Gradually, this trend is evolving into a standard practice for numerous study types instead of remaining a niche DCT model. The overall global AI-based clinical trials solution provider market growth is supported by these factors.

- For instance, in March 2025, Medable announced a landmark CNIL approval that expands access for digital/decentralized clinical trials across multiple countries using its eConsent and eCOA solutions, reinforcing broader rollout of hybrid/digital trial methods.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Trial Complexity and Cost Pressure is Propelling Market Growth

Rising trial complexity is a major driver as modern protocols now include more endpoints, more procedures, and more operational steps, which increases site workload, patient burden, and the risk of deviations. The 2025 SCRS Landscape Survey results highlighted by Clinical Leader indicate that approximately 24% of sites rejected a trial due to protocol complexity, while total endpoints increased by 29% and total procedures rose by 61% compared to a decade ago, all of which directly raises trial costs and timeline risks. As complexity increases, sponsors encounter additional protocol changes, slower recruitment, and elevated monitoring/quality costs, leading them to invest in AI to model trial outcomes earlier, anticipate challenges, and avert unnecessary rework. This establishes distinct ROI demands for AI solutions related to protocol optimization, recruitment forecasting, and operational automation, since even minor delays in extensive Phase II/III programs can be costly and harm reputations. The above mentioned factors are cumulatively responsible for driving the growth of the market.

- For example, in May 2025, Medidata launched Medidata Protocol Optimization, specifically positioning it to improve protocol design and reduce patient/site burden, and to predict impacts on site performance and costs ahead of First Patient In. This was aimed at reducing amendments and enrollment delays caused by complex protocols.

MARKET RESTRAINTS

Lack of Standardized Clinical Data Formats across Healthcare Systems to Limit Market Growth

The absence of standardized clinical data formats significantly limits AI trial solutions since they depend on clean, interoperable clinical data to conduct feasibility, patient matching, and monitoring analytics effectively at scale. In practice, data is frequently stored in various schemas, terminologies, and coding methods across hospitals, nations, and even departments, requiring vendors to invest time in mapping, normalization, and custom integrations before AI can provide value. This raises implementation expenses, extends sales cycles, and delays multi-country deployments, particularly for NLP applications where note structure and language differ significantly. It also decreases model portability; an algorithm developed using one health system’s format may yield subpar results in other settings, necessitating repeated re-validation and re-training. Despite standards such as FHIR, challenges persist, and the issue of records without borders remains unresolved, hindering the speed at which AI can be implemented across locations. The above mentioned factors are resulting in limiting the growth of the market to a certain extent.

- However, in May 2025, the Financial Times reported that a large patient data in the U.K.’s NHS is still stuck on paper and fragmented across disparate IT systems, and that integrating these systems into a unified record is complex.

MARKET OPPORTUNITIES

Increasing Outsourcing and CRO Standardization to Offer Market Growth Opportunities

Outsourcing is growing as sponsors seek to manage expenses, tap into worldwide site networks quickly, and conduct more trials without increasing internal staff, thus, they are relying more on CROs for execution. This generates a market opportunity as major CROs must standardize their delivery model across numerous studies, prompting them to implement repeatable, AI-driven platforms for feasibility, site selection, enrollment forecasting, and data evaluation. Standardization assists CROs in minimizing variability among programs, accelerating startup timelines, and providing sponsors with more consistent performance metrics. It also allows CROs to productize their services and expand the same toolset across various sponsors boosting consistent software and service revenue. As outsourcing grows, sponsors are increasingly favoring CROs that can show technology-driven efficiency over solely labor-intensive implementation, which further enhances adoption. In the coming years, it is anticipated that all the factors mentioned above would support the growth of the market.

- For instance, in January 2026, PSI CRO announced the launch of SYNETIC, an AI-powered semantic knowledge platform added to its INTELIA trial intelligence platform to accelerate site identification, startup, and patient enrollment.

MARKET CHALLENGES

Limited AI Expertise in Smaller Pharmaceutical Organizations/CROs Pose a Prominent Challenge to Market Growth

A lack of AI expertise poses a significant market challenge as numerous small to mid-sized pharma companies and smaller CROs lack specialized data science, MLOps, and validation teams needed to implement AI tools in a regulated trial setting. Lacking in-house expertise, they face challenges with selecting use cases, preparing data, governing models, and integrating vendors, resulting in delayed adoption and higher implementation expenses. Teams frequently utilize AI solely in separate pilot programs, struggling to expand its application across studies due to staff's inability to sustain models, track performance drift, or record controls for audits. This lack of capability increases buyers' reliance on vendors’ professional services, extending sales cycles and postponing ROI. Consequently, AI adoption is inconsistent as large sponsors and CROs expand more rapidly, whereas smaller entities fall behind even though there is a significant need to enhance productivity.

- Furthermore, as per a study published in September 2025 in Lab of the Future Survey, the Pistoia Alliance reported that 34% of respondents cited “lack of people” as a barrier to AI adoption (up from 23% in 2024) and highlighted rising demand for AI education/training.

Segmentation Analysis

By Component

Growing Number of Software Deployments to Propel Segmental Growth

In terms of component, the market is divided into software and services.

The software segment captured the largest global AI-based clinical trials solution provider market share. This is due to the reason that most AI-based clinical trial capabilities are delivered as scalable, repeatable modules inside enterprise platforms, which sponsors and CROs prefer to buy as multi-year subscriptions. Moreover, software is easier to standardize across hundreds of studies, push frequent model/feature updates, and maintain consistent audit trails, access controls, and validation workflows. Additionally, increasing number of new product launches or upgrades by operating players also supported the segment growth.

- For instance, in October 2025, Veeva Systems announced Veeva AI Agents planned to be released across all Veeva applications, including R&D.

The services segment is anticipated to rise with a CAGR of 33.63% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Rising Focus on Cloud-based Solutions Supported Segmental Dominance

On the basis of deployment, the market is divided into on-premise, cloud-based, and hybrid.

The cloud-based segment is anticipated to capture the largest global AI based clinical trials solution provider market share in 2025. This is as the sponsors and CROs prefer cloud platforms as they can roll out standardized workflows globally across multiple studies and geographies without heavy local infrastructure. Moreover, cloud makes it easier to connect to external data sources through APIs, which is critical for AI use cases such as eligibility matching, automated data cleaning, and RBQM analytics. It also supports centralized oversight, remote monitoring teams can access dashboards and alerts in near real time. Furthermore, the segment is set to hold 53.9% share in 2026.

- For instance, in August 2025, Oracle announced significant enhancements to its Oracle Clinical One Data Collection (EDC), highlighting improvements such as EHR interoperability and tighter integration with safety solutions.

The hybrid segment is anticipated to rise with a CAGR of 28.71% over the forecast period.

By Technology

High Usage in Various Applications to Boost Machine Learning & Deep Learning Segment Growth

Based on technology, the market is classified into natural language processing, machine learning & deep learning, and others.

The machine learning & deep learning segment dominated the global market in 2025. Sponsors and CROs use ML/DL to forecast enrollment and screen-failure risk, predict site performance, detect data anomalies and protocol deviations for RBQM, and prioritize monitoring actions from thousands of operational signals. Moreover, deep learning also supports complex, high-dimensional data use cases that rule-based systems cannot manage well. These models can be trained on historical study data to produce repeatable, measurable lift, which makes them easier to justify in procurement than newer, less standardized AI categories. Furthermore, the segment is set to hold 53.2% share in 2026.

- For instance, in June 2025, PhaseV announced its ClinOps AI platform, positioning it to improve clinical trial operations with precision-guided site selection, real-time trial/site performance monitoring, and predictive insights.

The natural language processing segment is anticipated to rise with a CAGR of 33.61% over the forecast period.

By Therapeutic Area

Increasing Number of Oncology Clinical Trials to Boost Segmental Growth

In terms of therapeutic area, the market is divided into oncology, cardiovascular, CNS/neurology, immunology & autoimmune, infectious diseases, and others.

The oncology segment captured the highest share of the global market in 2025. This is owing to the fact that it has the largest number of ongoing clinical trials creating a heavy operational and analytics burden. Oncology programs often run many parallel studies across lines of therapy, which increases the value of automation in trial operations, monitoring, and document workflows. The cost of delays is especially high in oncology, so AI tools that reduce screen failures and accelerate enrollment are easier to justify commercially. Furthermore, the segment is set to hold 35.3% share in 2026.

- For instance, in January 2026, Mount Sinai Tisch Cancer Center announced the launch of an AI-powered clinical trial-matching platform (PRISM) created by Triomics, aimed at expanding access to cancer clinical trials across the health system.

The immunology & autoimmune segment is anticipated to rise with a CAGR of 31.98% over the forecast period.

By Phase

Increasing Number of Candidates Entering Phase III to Boost Segmental Growth

In terms of phase, the market is divided into phase I, phase II, phase III, and phase IV.

The phase III segment accounted for the highest share of the global market in 2025. This is as these are pivotal, late-stage trials that typically involve the largest patient populations, most sites, and the highest regulatory scrutiny, so sponsors and CROs spend the most on systems that reduce execution risk. Moreover, the volume of data and documentation in Phase III is much higher, increasing demand for automation in data review and trial oversight workflows. Furthermore, the segment is set to hold 45.7% share in 2026.

- For instance, in November 2025, Tata Consultancy Services (TCS) launched the next-generation TCS ADD Risk Based Quality Management (RBQM) Platform, highlighting AI-powered modules for real-time risk monitoring, centralized site performance tracking, and AI-driven subject risk scores.

The phase IV segment is anticipated to rise with a CAGR of 34.99% over the forecast period.

By Application

High Usage in Patient Identification, Recruitment & Retention to Boost Segmental Growth

On the basis of application, the market is divided into trial design and protocol optimization, patient identification, recruitment & retention, clinical operations automation, clinical data management, regulatory & document intelligence, pharmacovigilance automation, and others.

The patient identification, recruitment & retention segment captured the highest share of the global market in 2025. This is due to the fact that enrollment is still the biggest operational bottleneck in clinical trials, and delays here directly cascade into higher costs and missed timelines. It also improves site feasibility and targeting by identifying where eligible patients actually exist, helping sponsors avoid underperforming sites and late-stage rescue efforts. Furthermore, the segment is set to hold 19.7% share in 2026.

- For instance, in August 2025, Cleveland Clinic announced the roll-out of Dyania Health’s AI platform across its health system to accelerate clinical trial recruitment by identifying eligible patients more efficiently from clinical data.

The clinical operations automation segment is anticipated to rise with a CAGR of 34.30% over the forecast period.

By End User

High Utilization by Pharmaceutical & Biotechnology Companies to Support Segment’s Leading Position

Based on end user, the market is segmented into pharmaceutical & biotechnology companies, CROs/CDMOs, academic & research institutes, and others.

In 2025, the pharmaceutical & biotechnology companies segment held the leading position in the global market. This is as they are the primary budget owners for clinical development and therefore make the largest, multi-year purchases of AI-enabled trial platforms and modules. They also run larger global portfolios, so they benefit most from enterprise-scale AI that can be standardized across programs. Furthermore, the segment is set to hold 51.5% share in 2026.

- For instance, in February 2026, Evinova announced that Bristol Myers Squibb signed an agreement to deploy Evinova’s AI-native clinical development platform including the Study Designer Cost Optimizer module across BMS’s global portfolio to improve trial design decisions and cost efficiency.

In addition, CROs/CDMOs are projected to witness 32.45% growth rate during the forecast period.

AI-based Clinical Trials Solution Provider Market Regional Outlook

By region, the market is divided into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

North America

North America AI-based Clinical Trials Solution Provider Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 0.96 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 1.19 billion. North America is at the forefront due to its strong pharmaceutical R&D spending and early AI adoption in clinical trials.

U.S. AI-based Clinical Trials Solution Provider Market

The U.S. market dominated the North American region and can be analytically approximated at around USD 1.38 billion in 2026, accounting for roughly 39.4% of the global market.

Europe

Europe market size is anticipated to grow at 29.44% CAGR during the forecast period. The regional market is driven by strong pharmacovigilance and compliance culture, growing adoption of hybrid trial models, and strong regulatory frameworks.

U.K. AI-based Clinical Trials Solution Provider Market

The U.K. market in 2026 is estimated at around USD 0.20 billion, representing roughly 5.7% of global revenues.

Germany AI-based Clinical Trials Solution Provider Market

Germany market size is projected to reach approximately USD 0.22 billion in 2026, equivalent to around 6.4% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 0.64 billion by 2026, making it the third largest region in the worldwide sector. The Asia Pacific area is experiencing expanding clinical trial activity in China, India, and South Korea, rapid digitization of hospitals/sites and increasing cloud adoption, which drives the market growth.

Japan AI-based Clinical Trials Solution Provider Market

The Japan market in 2026 is estimated at around USD 0.10 billion, accounting for roughly 2.7% of global revenues.

China AI-based Clinical Trials Solution Provider Market

China’s market is projected to reach revenues of around USD 0.21 billion in 2026, representing roughly 6.0% of global sales.

India AI-based Clinical Trials Solution Provider Market

The Indian market size in 2026 is estimated at around USD 0.10 billion, accounting for roughly 2.7% of global revenues.

Latin America and Middle East & Africa

The regions of the Middle East & Africa and Latin America are expected to experience slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.25 billion by 2026. Prominent factors such as emerging clinical trial destinations due to cost advantages and diverse patient populations, gradual adoption of AI tools supported by increasing investment in healthcare research infrastructure are boosting the market growth in these regions.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.07 billion by 2026, representing about 2.0% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Scalable AI Workflows and Expanding Base Strengthens Market Position of Leading Companies

The global market for AI-based clinical trials solutions remains moderately fragmented, with a mix of major eClinical platform providers, CRO-driven technology firms, and niche AI-focused companies actively competing. Key players in the space include Medidata (Dassault Systèmes), Veeva Systems, Oracle, IQVIA, and Signant Health. These companies maintain a competitive edge due to their extensive presence across sponsors and CROs. Further, their capability to integrate AI into essential clinical processes, and their use of scalable cloud-based deployments that support multi-study rollouts. Such capabilities play a crucial role in reinforcing their leadership in the market.

In addition, other notable contributors such as Triomics/Dyania Health and similar specialist vendors are concentrating on AI-powered solutions for patient matching, site feasibility, and operational intelligence. These companies are increasingly prioritizing the launch of advanced platforms, the expansion of AI copilots/agent-based workflows, and forming strategic collaborations with healthcare systems. They are also focusing on CRO networks to accelerate broader adoption across global clinical trial portfolios.

- For example, in July 2025, ArisGlobal announced strong momentum driven by continued innovation in LifeSphere NavaX, alongside 27 go-lives and new global pharma adoptions.

LIST OF KEY AI-BASED CLINICAL TRIALS SOLUTION PROVIDER COMPANIES PROFILED

- Dassault Systèmes (Medidata) (France)

- Veeva Systems (U.S.)

- Oracle (U.S.)

- IQVIA Inc. (U.S.)

- Signant Health (U.S.)

- TEMPUS (U.S.)

- Saama (U.S.)

- TriNetX, LLC (U.S.)

- Clario (U.S.)

- Medable Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: HEALWELL AI Inc. and WELL Health Technologies Corp. launched WELLTRUST, positioned as a consent-driven platform leveraging HEALWELL’s DARWEN AI to accelerate ethical patient identification and engagement for clinical research/trial recruitment.

- January 2026: Medable launched an agentic AI capability for research sites to help PIs oversee and monitor eCOA data, aimed at reducing site burden and improving operational oversight.

- November 2025: Caidya invested in additional Medidata Experiences solutions (including CTMS and Clinical Data Studio) to connect workflows/data across the trial lifecycle and scale data-driven decision-making.

- September 2025: Advarra launched an AI- and data-backed Study Design solution (using its Braid data/AI engine) to evaluate protocol feasibility and improve operational efficiency in clinical trials.

- April 2025: NetraMark and Worldwide Clinical Trials announced a global agreement to integrate NetraAI into Worldwide’s offerings to support AI-powered trial design optimization (initially Phase II and select Phase III), focused on patient-centric optimization and regulatory-aligned insights.

REPORT COVERAGE

The global AI-based clinical trials solution provider market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market outlook report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 30.90% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Deployment, Technology, Therapeutic Area, Phase, Application, End User, and Region |

| By Component |

|

| By Deployment |

|

| By Technology |

|

| By Therapeutic Area |

|

| By Phase |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.79 billion in 2025 and is projected to reach USD 30.15 billion by 2034.

In 2025, the market value stood at USD 1.19 billion.

The market is expected to exhibit a CAGR of 30.90% during the forecast period.

By component, the software segment is expected to lead the market.

The rising trial complexity, increasing cost pressure, and rising focus on trial quality and risk-based oversight are primarily driving market expansion.

Dassault Systèmes (Medidata), Veeva Systems, Oracle, and IQVIA Inc. are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 234

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us