Heart Failure Monitoring Devices Market Size, Share & Industry Analysis, By Device Type (Implantable Hemodynamic Monitoring Devices, Wearable Monitoring Devices, and External/Non-Wearable Monitoring Systems), By Mode (Invasive and Non-Invasive), By End-user (Hospitals & ASCs, Specialty Clinics, Homecare Settings, and Long-term Care & Others), and Regional Forecast, 2026-2034

Heart Failure Monitoring Devices Market Size and Future Outlook

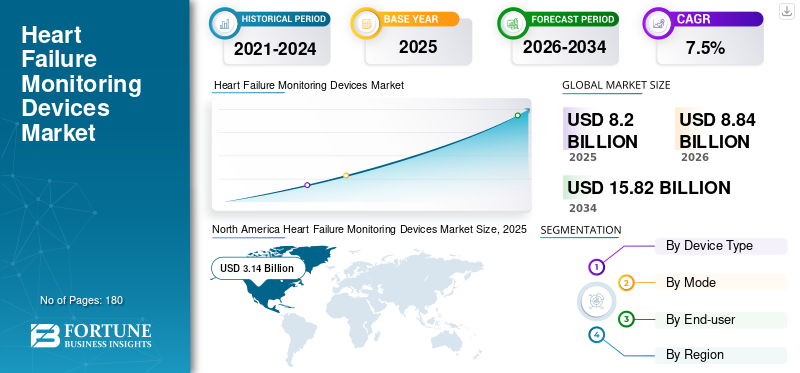

The global heart failure monitoring devices market size was valued at USD 8.20 billion in 2025. The market is projected to grow from USD 8.84 billion in 2026 to USD 15.82 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period. North America dominated the heart failure monitoring devices market with a market share of 38.29% in 2025.

Heart failure monitoring devices are tools used to track heart function and fluid levels in patients with heart failure, helping doctors detect early signs of worsening conditions and prevent hospital admissions. The market growth is attributed to key factors such as the increasing aging population, high heart failure patient pool, and the need to reduce hospital readmissions.

Furthermore, Abbott, Medtronic, and Boston Scientific Corporation held the major market share in 2025 due to their broad product offerings and strong branad reputations.

Download Free sample to learn more about this report.

Heart Failure Monitoring Devices Market Key Takeaways

- 2025 Market Size: USD 8.20 billion

- 2026 Market Size: USD 8.84 billion

- 2034 Forecast Market Size: USD 15.82 billion

- CAGR: 7.5% from 2026–2034

- North America dominated the heart failure monitoring devices market with a 38.29% share in 2025.

- The non-invasive segment is estimated to hold an 85.2% share in 2026.

- The hospitals & ASCs segment is set to hold a 45.4% share in 2026.

North America

North America remained the leading regional market, projected to reach USD 3.14 billion by 2026.

Europe

Europe is expected to grow at a 6.9% CAGR during the forecast period, reaching USD 2.92 billion by 2026.

Asia Pacific

Asia Pacific is projected to become the third-largest regional market, reaching USD 1.68 billion by 2026.

U.S.

U.S. The market is projected to reach USD 3.09 billion by 2026, accounting for approximately 34.9% of the global market.

Japan

Japan The market is projected to generate USD 0.27 billion in revenue by 2026, representing approximately 3.1% of the global market.

Read More

HEART FAILURE MONITORING DEVICES MARKET TRENDS

Integration of AI and Predictive Analytics to Emerge as a Key Trend

Currently, several companies are focusing on the integration of artificial intelligence and predictive analytics into monitoring systems to analyze patient data and provide early alerts before symptoms worsen.

This technology combines multiple sensor data points to predict heart failure events. Furthermore, advanced wearable technologies are enabling continuous tracking with greater accuracy, thereby improving clinical decision-making and reducing emergency hospital visits.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Burden of Heart Failure to Drive the Market Expansion

Over the past few years, there has been an increasing number of heart failure cases worldwide due to risk factors such as sedentary lifestyle, diabetes, hypertension, and obesity. Moreover, hospitals face high costs due to repeated admissions of heart failure patients. In such a scenario, monitoring devices help detect fluid buildup and early changes in cardiac pressure, enabling timely treatment and driving the global heart failure monitoring devices market growth.

- For instance, as per data from the Heart Failure Society of America, around 6.7 million U.S. adults over age 20 currently have heart failure (HF), with the prevalence projected to reach 8.5 million by 2030.

MARKET RESTRAINTS

High Cost of Implantable Devices and Limited Access to Restrict Market Growth

Despite the growing demand for heart failure monitoring devices, the high cost of implantable systems is limiting their adoption in low- and middle-income countries. Moreover, implant procedures require skilled professionals and hospital infrastructure, which is lacking in low- and middle-income countries. Furthermore, reimbursement policies remain limited in some regions, which is expected to slow the adoption of these devices and hinder market growth.

- For instance, in March 2022, Medscape mentioned that a CardioMEMS device costs hospitals approximately USD 20,000.

MARKET OPPORTUNITIES

Expansion of Remote Patient Monitoring Programs to Offer Significant Opportunities

In recent years, healthcare providers have increased the use of home-based monitoring systems due to the expansion of telehealth and remote patient monitoring programs, which is expected to drive the key companies to integrate artificial intelligence and cloud platforms into monitoring devices. Moreover, partnerships between device manufacturers and digital health companies have increased, as emerging markets such as India, Brazil, and Southeast Asia are investing heavily in telemedicine infrastructure, supporting market growth.

- For instance, in May 2025, Medtronic partnered with Corsano Health for the exclusive distribution of its multi-parameter wearable in Western Europe, targeting hospital and hospital-at-home monitoring of vital signs such as heart rate, SpO2, blood pressure, and ECG.

MARKET CHALLENGES

Data Management and Patient Compliance to Challenge Market Expansion

Hospitals require proper IT systems and trained staff to handle continuous data flow from monitoring devices. In such a scenario, the false alerts create extra workload for healthcare providers.

In addition, patient compliance is another challenge, especially for wearable and home-based devices. Moreover, some elderly patients find it challenging to utilize the digital systems regularly. Further, technical issues, such as connectivity problems, are also expected to affect device performance, challenging the market expansion.

Segmentation Analysis

By Device Type

High Usage of External/Non-Wearable Devices in Hospitals to Boost the Segment’s Growth

Based on device type, the market is segmented into implantable hemodynamic monitoring devices, wearable monitoring devices, and external/non-wearable monitoring systems.

To know how our report can help streamline your business, Speak to Analyst

The external/non-wearable monitoring systems segment accounted for the largest global heart failure monitoring devices market share in 2025. The segment’s growth is attributed to the widespread use of bedside monitors and advanced cardiac monitoring stations in hospitals and emergency settings.

Additionally, the wearable monitoring devices segment is expected to register a CAGR of 7.8% over the forecast period.

By Mode

Increasing Adoption of Non-Invasive Devices Due to Patient Comfort and Safety to Fuel the Segment’s Growth

By mode, the market is segmented into invasive and non-invasive.

The non-invasive segment accounted for the largest market share in 2025. The segment's growth is driven by the high adoption of non-invasive monitoring devices, which enable patients to monitor blood pressure, oxygen levels, heart rate, and other parameters without surgical intervention. Moreover, the segment is estimated to hold an 85.2% share in 2026.

Additionally, the invasive segment is expected to expand at a CAGR of 6.4% during the forecast period.

By End-user

Large Number of Hospitals to Drive the Hospitals & ASCs Segment’s Growth

On the basis of end-user, the market is segmented into hospitals & ASCs, specialty clinics, homecare settings, and long-term care & others.

In 2025, the hospitals & ASCs segment dominated the market in terms of end user. The segment’s growth is attributed to advanced infrastructure and the skilled professionals required to manage critical patients in intensive care units and cardiology departments, which favor the adoption of heart failure monitoring devices. Moreover, the increasing number of hospitals is also projected to contribute to this demand. Furthermore, the segment is set to hold a 45.4% share in 2026.

- For instance, the American Hospital Association reports that there are approximately 6,100 registered hospitals in the U.S. as of 2026.

In addition, the homecare settings segment is projected to grow at a CAGR of 7.9% over the forecast period.

Heart Failure Monitoring Devices Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Heart Failure Monitoring Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 2.93 billion, and also dominated in 2025, reaching a value of USD 3.14 billion. The growth is attributed to the advanced healthcare infrastructure and strong adoption of remote patient monitoring technologies. Further, a significant number of critical care beds in the region are favoring the adoption of cardiac failure monitoring devices.

- For instance, according to data from the National Center for Biotechnology Information (NCBI) in February 2023, the U.S. and its territories have 4,846 adult hospitals, totaling 79,876 adult critical care beds.

U.S. Heart Failure Monitoring Devices Market

By 2026, the U.S. reached USD 3.09 billion, representing about 34.9% of the global market.

Europe

Europe is projected to record a growth rate of 6.9% during the projection period, the second-highest globally, reaching USD 2.92 billion by 2026. The region is witnessing the increasing use of non-invasive, wearable monitoring devices for chronic disease management, which is anticipated to drive market growth.

U.K. Heart Failure Monitoring Devices Market

The U.K. market is projected to reach USD 0.43 billion by 2026, contributing approximately 4.8% to the global revenue.

Germany Heart Failure Monitoring Devices Market

The Germany market is projected to reach USD 1.00 billion by 2026, accounting for approximately 11.3% of global revenue.

Asia Pacific

By 2026, the Asia Pacific devices market is projected to reach USD 1.68 billion, making it the third-largest market worldwide. The increasing awareness of early diagnosis and remote monitoring, driven by the large patient pool for cardiovascular diseases in the region, is expected to drive market growth.

Japan Heart Failure Monitoring Devices Market

The Japan market is projected to generate USD 0.27 billion in revenue by 2026, accounting for approximately 3.1% of the global market.

China Heart Failure Monitoring Devices Market

The China market is expected to reach nearly USD 0.62 billion by 2026, accounting for 7.0% of global revenues.

India Heart Failure Monitoring Devices Market

The India market is projected to reach USD 0.24 billion by 2026, accounting for around 2.8% of global market revenue.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to experience moderate growth, with the Latin American market projected to reach USD 0.54 billion by 2026. Growing private healthcare investments and the expansion of cardiac care centers are supporting the demand for monitoring devices, driving the market growth in these regions.

GCC Heart Failure Monitoring Devices Market

By 2026, the GCC market is expected to reach USD 0.19 billion, accounting for 2.1% of total market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Focus on Product Innovation and Diversified Portfolios to Drive the Dominant Market Share of Key Players

In 2025, Abbott, Medtronic, and Boston Scientific Corporation held the largest global market share. The share is mainly due to their strong cardiac portfolios and international presence, along with their focus on product innovation, clinical validation, and digital integration.

Moreover, other prominent players are partnering with hospitals and digital health companies to expand their portfolios of remote patient monitoring devices. They are also focusing on wearable and non-invasive technologies to meet the growing demand for home-based cardiac care.

LIST OF KEY HEART FAILURE MONITORING DEVICES COMPANIES PROFILED

- Abbott (U.S.)

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Biotronik (Germany)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- ZOLL Medical Corporation (U.S.)

- iRhythm Technologies, Inc. (U.S.)

- Qardio, Inc. (U.S.)

- CardiacSense (Israel)

KEY INDUSTRY DEVELOPMENTS

- October 2025: BIOTRONIK and the University of Sydney signed a Memorandum of Understanding (MoU) to co-develop digital cardiac care solutions through 2028, combining BIOTRONIK's expertise in implanted devices and remote monitoring with the university's research at the Westmead Applied Research Centre.

- November 2024: SeeMedX, Inc. submitted a 510(k) to the FDA for its non-invasive cardiac monitoring device, offering real-time hemodynamic data such as fluid status and cardiac output to optimize heart failure treatment.

- November 2024: BIOTRONIK hosted the Digital Heart Summit 2025 in Berlin, where 120 experts discussed AI, real-world data, and patient-centric tech reshaping cardiovascular care.

- November 2024: Abbott launched the TEAM-HF clinical trial using its CardioMEMS HF System to monitor pulmonary artery pressures in up to 850 patients across 75 global sites.

- April 2024: BIOTRONIK announced CE approval and the first European implant of BIOMONITOR IV, its latest insertable cardiac monitor (ICM) featuring AI-powered SmartECG to reduce false positives by up to 86% while distinguishing PVCs and PACs.

- September 2023: Boston Scientific Corporation launched the LUX-Dx II+ ICM System for long-term monitoring of heart rhythm.

- February 2022: Abbott's CardioMEMS HF System received FDA approval for an expanded indication, enabling its use in earlier-stage heart failure patients.

REPORT COVERAGE

The report provides a detailed analysis of all market segments, highlighting the major drivers, trends, opportunities, restraints, and challenges influencing market growth. It also offers insights into technological advancements, significant industry developments, the prevalence of heart failure, market share evaluation, and in-depth profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Device Type, Mode, End-user, and Region |

| By Device Type |

|

| By Mode |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.20 billion in 2025 and is projected to reach USD 15.82 billion by 2034.

In 2025, the North America market value stood at USD 3.14 billion.

The market is expected to grow at a CAGR of 7.5% over the forecast period of 2026-2034.

The external/non-wearable monitoring systems segment led the market by device type in 2025.

The key factor driving the market is the rising burden of heart failure.

Abbott, Medtronic, and Boston Scientific Corporation are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us