Hepatitis Therapeutics Market Size, Share & Industry Analysis, By Indication (Hepatitis B {Nucleoside Analogues, Nucleotide Analogues, Interferons, and Others}, Hepatitis C {NS5A Inhibitors, NS5B Polymerase Inhibitors, Protease Inhibitors (NS3/4A), and Others}, Hepatitis D {Entry Inhibitors, Prenylation Inhibitors, and Interferons}, and Others), By Age Group (Adults and Pediatrics), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, and Online Pharmacies & Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

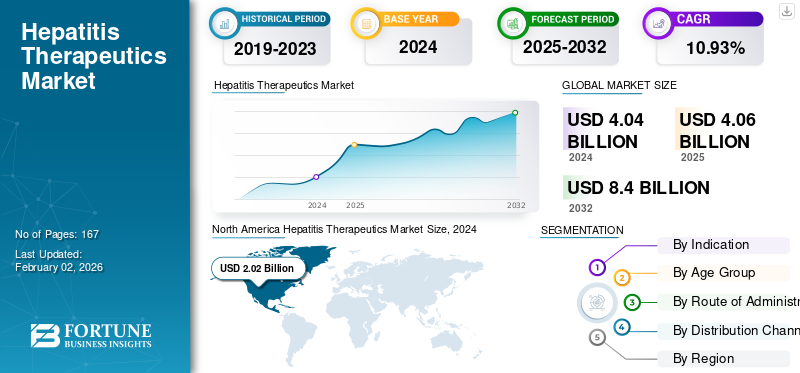

The global hepatitis therapeutics market size was valued at USD 4.06 billion in 2025. The market is projected to grow from USD 4.29 billion in 2026 to USD 10.12 billion by 2034, exhibiting a CAGR of 11.32% during the forecast period. North America dominated the global market with a share of 50.04% in 2025.

The global market is witnessing steady and substantial growth, driven by the rising prevalence of hepatitis indications and increasing diagnostic capabilities. Hepatitis is one of the most persistent infectious diseases affecting a large population across the globe. Increasing awareness of hepatitis and government-scheduled screening programs are anticipated to lead to market growth in the coming years. Additionally, the introduction of innovative therapeutic solutions and rising investments by key players are also expected to boost market growth.

- For instance, in September 2025, AusperBio Therapeutics, Inc., collaborated with Ausper Biopharma Co., Ltd. to advance targeted oligonucleotide therapies to achieve a functional cure for chronic hepatitis B (CHB), with an investment of USD 63.0 million in Series B2 financing.

Furthermore, many key industry players, such as Bristol-Myers Squibb Company, GSK plc., and Gilead Sciences, Inc., operating in the market, are focusing on developing various innovative candidates to support the rising demand for effective therapeutics for hepatitis.

Download Free sample to learn more about this report.

Hepatitis Therapeutics Market KEY TAKEAWAYS

- 2024 Market Size: USD 4.04 billion

- 2025 Market Size: USD 4.06 billion

- 2032 Forecast Market Size: USD 8.40 billion

- CAGR: 10.93% from 2025–2032

- North America dominated the hepatitis therapeutics market with a 50.0% share in 2024.

- The hepatitis D segment is projected to grow at a CAGR of 14.63% during the forecast period.

- The pediatrics segment is projected to grow at a CAGR of 13.67% during the forecast period.

North America

Valued at USD 2.03 billion in 2025, supported by high diagnosis rates, advanced healthcare infrastructure, and strong R&D investments.

Europe

Valued at USD 0.68 billion in 2025, driven by government screening programs and expanding reimbursement for hepatitis treatments.

Asia Pacific

Valued at USD 0.96 billion in 2025, driven by rising hepatitis prevalence and improving access to diagnosis and treatment.

U.S.

Projected to reach USD 1.90 billion by 2026, supported by favorable reimbursement policies and ongoing clinical research.

Japan

Projected to reach USD 0.22 billion by 2026, driven by increasing adoption of advanced hepatitis therapies and disease management programs.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Disease Burden is Accelerating Market Growth

The increasing prevalence of hepatitis infections globally is a major factor driving the hepatitis therapeutics market growth. A surge in chronic hepatitis B and C cases has intensified the need for effective antiviral therapies. As more individuals are diagnosed, the demand for treatment options has showcased significant growth. Such rising prevalence expands the patient pool and increases the demand for hepatitis therapeutics. Thus, the need for research and development by key companies to bridge this unmet clinical demand is increasing. These factors combined efforts are accelerating the adoption of hepatitis therapeutics.

- For instance, in 2024, the World Hepatitis Alliance reported that 254 million people were suffering from hepatitis B, while 50 million people were living with hepatitis C globally.

MARKET RESTRAINTS

Adverse Effects Associated with Hepatitis Therapeutics to Restrict Market Growth

Adverse effects related to hepatitis therapeutics pose a significant restraint on market growth. Numerous immunomodulatory drugs used for the treatment of hepatitis are associated with the risk of adverse side effects such as fatigue, anemia, depression, gastrointestinal discomfort, headaches, or hepatic complications in vulnerable patients. These can adversely affect patient compliance. These factors limit the revenue potential and long-term market expansion.

- For example, in June 2025, NIH published a study titled ‘Advances in treatment of hepatitis delta virus infection: Update on novel investigational drugs’ that reported some of the adverse effects, including bone marrow suppression, psychiatric decompensation, skin reactions, constitutional symptoms, and other autoimmune phenomena. These can restrict the market growth.

MARKET OPPORTUNITIES

Shifting Focus Toward Precision Medicine for Hepatitis Treatment to Offer Market Growth Opportunities

The shifting focus toward precision medicine in hepatitis treatment is expected to create significant market growth opportunities. Precision medicine is drastically improving treatment efficacy and safety. Tailored antiviral combinations and dosages mitigate the risk of adverse effects associated with existing treatments. Also, advancements in genomic sequencing and biomarker identification are further supporting the development of personalized antiviral drugs. Emphasizing these factors, numerous key companies are focusing on the development of precision medicine pipelines.

- For instance, in March 2025, Precision BioSciences, Inc. received the Investigational New Drug (IND) application from the U.S. FDA for PBGENE-HBV, an in vivo gene-editing therapy to cure chronic hepatitis B.

MARKET CHALLENGES

Stigma Regarding Hepatitis Treatment to Hinder Treatment Adoption and Pose a Critical Challenge to Market Growth

Stigma regarding the treatment of hepatitis continues to hinder therapy adoption and presents a critical challenge to market growth. Hepatitis is often stigmatized in relation to substance use and sexual transmission. This fear of contagion resulted in social discrimination, which discourages individuals from seeking testing or treatment, even when affordable care is available. Such hesitation reduces the effectiveness of national screening and vaccination campaigns and the reach of healthcare initiatives.

- For instance, in February 2024, NIH published an article titled ‘Experience and impact of stigma in people with chronic hepatitis B: a qualitative study in Asia, Europe, and the U.S.’. The study reported emotional, lifestyle, and social impacts of living with chronic hepatitis B, including prejudice, marginalization, and negative relationships and work experiences. These factors pose a significant challenge to the market.

HEPATITIS THERAPEUTICS MARKET TRENDS

Increasing Government Support is a Prominent Trend Observed in Market

Increasing government support has emerged as a prominent trend in the global market. Governments across the globe are collaborating strategically to eliminate viral hepatitis through large-scale screening, vaccination, and treatment programs. These initiatives aim to integrate hepatitis care into national health systems. Additionally, reimbursement frameworks developed by the government to facilitate access, fund activities, and raise awareness are strengthening supply chains for hepatitis medicines and diagnostics, supporting market growth.

- For instance, in January 2023, the National Center for Disease Control and Public Health (NCDC) in Georgia collaborated with the WHO for Viral Hepatitis Elimination. The collaboration aimed to develop and monitor national hepatitis elimination plans, improve viral hepatitis testing strategies, and strengthen diagnostic laboratory capacity in the region. Such developments support the market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Indication

Increasing Prevalence of Hepatitis B to Propel Segmental Growth

Based on the Indication, the market is divided into hepatitis B, hepatitis C, hepatitis D, and others.

The hepatitis B segment is anticipated to account for the largest hepatitis therapeutics market share of 62.33% in 2026. The high segmental share is primarily attributed to the high global prevalence of chronic Hepatitis B infection. Unlike other forms of hepatitis, Hepatitis B requires long-term antiviral therapy to suppress viral replication and prevent liver damage. The availability of multiple treatment options has expanded therapeutic adoption. Additionally, continuous efforts by governments and organizations to enhance Hepatitis B treatment programs to further strengthen this segment’s market position.

- For instance, in July 2025, the Hepatitis B Foundation received funding through the Eugene Washington PCORI Engagement Award Program, an initiative of the Patient-Centered Outcomes Research Institute (PCORI). The funding aimed to amplify and integrate patient input into the development of hepatitis B therapeutics and clinical research. Such developments are expected to drive the segmental growth.

The hepatitis D segment is anticipated to rise with a CAGR of 14.63% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Age Group

High Burden of Adult Patient Pool Boosted Segment Growth

Based on age group, the market is segmented into adults and pediatrics.

In 2026, the adults segment dominated the global market with a share of 92.02%. This dominance of the segment was due to the higher prevalence of chronic hepatitis B and C infections among adults. This higher prevalence of hepatitis in adults was primarily linked to lifestyle factors, occupational exposure, and historical transmission through unsafe medical practices. Moreover, clinical trials and drug approvals for hepatitis therapeutics are focused on adult populations, ensuring broader access and optimized dosing regimens. These factors reinforce the segmental growth of adults in hepatitis therapeutics.

- For instance, in August 2025, Aligos Therapeutics, Inc. initiated dosing in the Phase 2 B-SUPREME study of its investigational compound ALG-000184 in patients with chronic hepatitis B virus (HBV) infection. The study evaluates the safety and efficacy of ALG-000184 monotherapy compared with tenofovir disoproxil fumarate in approximately 200 adult subjects with chronic HBV infection.

The pediatrics segment is projected to grow at a CAGR of 13.67% over the forecast period.

By Route of Administration

Oral Segment to Lead Market Due to Ease of Administration

Based on the route of administration, the market is segmented into oral and parenteral.

The oral segment is anticipated to witness a dominating market share of 89.29% in 2026. The ease of administration, along with better patient compliance associated with orally administered drugs, resulted in dominance of the segment. Furthermore, the growing preference for oral combinations and once-daily regimens has enhanced adherence and patient outcomes. Emphasizing these advantages, key players are actively participating in the launch of new products for the market.

- For instance, in October 2025, Aldeyra Therapeutics, Inc. announced a significant improvement in liver function in patients treated with ADX-629. It is an orally administered RASP modulator for the treatment of immune-mediated diseases.

The parenteral segment is projected to grow at a CAGR of 15.70% over the forecast period.

By Distribution Channel

Strategic Collaboration of Hospital Pharmacies with Other Key Players Kept Them in a Leading Position

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies & others.

The hospital pharmacies dominated the global market. This high market share was driven by the dependence of hepatitis patients on hospital-based treatment, especially during diagnosis, monitoring, and management of advanced liver disease. These hospitals served as primary healthcare centers and ensured reliable access to medications. The key role of these hospital pharmacies in reducing the risk of hepatitis and raising awareness is crucial and has resulted in a higher market share. Furthermore, the segment is set to hold a 52.64% share in 2026.

- For instance, in July 2025, the Journal of Drug Delivery and Therapeutics published an article titled ‘Hepatitis Screening in Community Pharmacies as a Measure of Reducing the Rate of Infections’ that reported hepatitis screening in community pharmacies as a measure of reducing the rate of infections. Such strategic collaborations among

In addition, online pharmacies are projected to grow at a CAGR of 12.69% during the study period.

Hepatitis Therapeutics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Hepatitis Therapeutics Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 2.03 Billion in 2025, representing 50.04% of the global market landscape, and is expected to reach USD 2.13 Billion in 2026. The market in North America is expected to increase due to diagnostic rates of hepatitis and the growing prevalence of liver disorders in the region. These factors, coupled with robust healthcare and substantial investment in research and development, followed by clinical trials, are enabling market growth. The U.S. market is estimated to reach USD 1.9 billion by 2026. Furthermore, robust healthcare infrastructure and favorable reimbursement initiatives in the U.S. support market growth.

- For instance, in September 2025, AusperBio Therapeutics, Inc. completed patient enrollment in two Phase II clinical trials evaluating its lead candidate, AHB-137, in patients with chronic hepatitis B (CHB).

Europe

Europe contributed 16.75% to the global market in 2025, with a valuation of USD 0.68 billion, and is projected to reach USD 0.7 billion in 2026. The region is estimated to have widespread government screening activities to contain hepatitis and increasing national reimbursement schemes to improve access to critical treatment. Backed by these factors, countries including the U.K. market are estimated to reach USD 0.16 billion by 2026, while the Germany market is estimated to reach USD 0.10 billion by 2026.

Asia Pacific

Asia Pacific accounted for USD 0.96 billion in 2025, representing 23.52% of the global market share, and is projected to reach USD 1.06 billion in 2026. and secure the position of the third-largest region in the market. The Japan market is estimated to reach USD 0.22 billion by 2026, the China market is estimated to reach USD 0.29 billion by 2026, and the India market is estimated to reach USD 0.15 billion by 2026.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. Latin America contributed approximately USD .18 Billion to the global market in 2025, accounting for a 4.50% share, and is expected to reach USD 0.19 Billion in 2026. WHO-supported national hepatitis control plans, along with improved diagnostic capabilities, are anticipated to enhance access to treatment in these regions and drive further growth. In the Middle East & Africa, the GCC is set to reach a value of USD 0.09 billion in 2025.

In 2025, Middle East & Africa held 5.20% of the global market, reaching a valuation of USD 0.21 billion, and is projected to grow to USD 0.22 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Clinical Trials by Key Players to Propel Market Progress

The global hepatitis therapeutics market holds a semi-consolidated market structure, constituting prominent players such as GSK plc., Merck & Co., Inc., and Pfizer Inc. The significant market share of these companies is due to numerous strategic activities, including collaboration among operating entities to advance research activities through various ongoing clinical trials.

- For instance, in April 2025, Atea Pharmaceuticals, Inc. entered a Phase 3 trial evaluating the regimen of bemnifosbuvir and ruzasvir for the treatment of adults with chronic hepatitis C virus (HCV). This C-BEYOND was an open-label trial conducted in the U.S. and Canada comparing the combination regimen of bemnifosbuvir and ruzasvir to the combination regimen of sofosbuvir and velpatasvir.

Other notable players in the global market include Gilead Sciences, Inc., Hoffmann-La Roche Ltd., and Zydus Group. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY HEPATITIS THERAPEUTICS COMPANIES PROFILED

- Bristol-Myers Squibb Company (U.S.)

- Zydus Group (U.S.)

- GSK plc. (U.K.)

- AbbVie Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- F Hoffmann-La Roche Ltd (Switzerland)

- Atea Pharmaceuticals, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd.(Israel)

KEY INDUSTRY DEVELOPMENTS

- June 2025: AstriVax Therapeutics NV initiated clinical development with AVX70371 for the treatment of chronic hepatitis B virus (HBV) infection.

- March 2025: – Brii Biosciences Limited presented end-of-treatment (EOT) data from Cohorts 1-3 and Week 24 on-treatment data from Cohort 4 of its ongoing Phase 2 ENSURE study at the 34th Annual Meeting of the Asian Pacific Association for the Study of the Liver (APASL 2025).

- March 2025: Vir Biotechnology, Inc. completed enrollment for ECLIPSE 1, a Phase 3 trial evaluating the safety and efficacy of the combination of tobevibart and elebsiran in patients with chronic hepatitis delta (CHD).

- February 2024: GSK plc received Fast Track Designation from the U.S. FDA for bepirovirsen, an investigational antisense oligonucleotide (ASO) for the treatment of chronic hepatitis B (CHB).

- September 2020: Bayer AG acquired U.K.-based biotech company KaNDy Therapeutics Ltd. to expand its drug development pipeline in women’s healthcare.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.32% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Indication, Age Group, Route of Administration, Distribution Channel, and Region |

| By Indication |

|

| By Age Group |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.29 billion in 2026 and is projected to reach USD 10.12 billion by 2034.

In 2024, the market value stood at USD 2.03 billion.

The market is expected to exhibit a CAGR of 11.32% during the forecast period of 2026-2034.

By indication, the hepatitis B segment is expected to lead the market.

The increasing prevalence of hepatitis and growing awareness programs by the government are driving market expansion.

Bristol-Myers Squibb Company, Pfizer Inc., Merck & Co., Inc., and Biogen are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us