High Strength Glass Market Size, Share & Industry Analysis, By Product Type (Tempered (Toughened) Glass, Laminated Glass, Heat Strengthened Glass, and Others), By End Use (Construction & Architecture, Automotive & Transportation, Solar Energy, and Others), and Regional Forecast, 2026-2034

High Strength Glass Market Size and Future Outlook

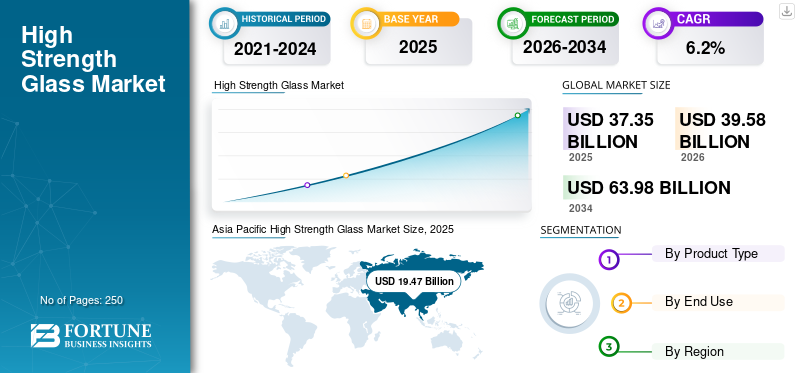

The global high strength glass market size was valued at USD 37.35 billion in 2025. The market is projected to grow from USD 39.58 billion in 2026 to USD 63.98 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the high strength glass market with a market share of 52.12% in 2025.

High strength glass refers to engineered glass materials that undergo chemical or thermal strengthening processes to significantly enhance their mechanical strength, impact resistance, and durability compared to conventional annealed glass. Glass attains exceptional properties through tempering, ion-exchange, lamination, or hybrid strengthening techniques. The product’s improved load-bearing capacity, safety performance, and resistance to thermal stress, makes it a preferred choice for structurally demanding and safety-critical applications. It is widely used across construction & architecture, solar energy, electronics, and automotive sectors where performance, safety compliance, and lightweighting are critical. The demand for high strength glass is primarily driven by the rising adoption of energy-efficient facades and curtain walls, increasing vehicle lightweighting initiatives, expanding solar photovoltaic installations, and focus on safety regulations in buildings and transportation.

The market is led by global glass manufacturers and specialty technology providers that maintain strong positions through vertically integrated float glass production, advanced coating capabilities, and proprietary strengthening technologies. Major players such as AGC Inc., Saint-Gobain, NSG Group, Xinyi Glass, and Corning Inc. sustain competitiveness through large-scale production networks, R&D-driven product innovation, and strategic supply agreements with automotive OEMs and solar module manufacturers.

Download Free sample to learn more about this report.

HIGH STRENGTH GLASS MARKET TRENDS

Shift toward Energy-Efficient Facades and High-Performance Coated Glass to Fuel Product Adoption

A key trend is the growing preference for energy-efficient buildings that use advanced glass systems to reduce cooling loads and improve indoor comfort. Architectural projects increasingly specify coated, insulated, and safety-grade glazing solutions for curtain walls and large facade panels. This pushes the demand for processed glass that combines strength with performance features such as low-emissivity coatings, solar control, and enhanced durability. As green building standards and refurbishment activity expand, the industry is moving toward higher value-added glass configurations, where strength is a baseline requirement and coatings deliver additional performance benefits. The trend is likely to support the demand for high performance glass products during the forecast period.

- Green building codes in Europe are primarily driven by the Energy Performance of Buildings Directive (EPBD), which requires all new buildings to be Nearly Zero-Energy Buildings (NZEB). Key standards focus on high-energy performance, energy efficient, and reduced carbon emissions, supported by certifications such as BREEAM and LEED. Such initiatives and government norms will fuel product demand in the foreseeable future.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Safety-Grade Glazing in High-Rise Buildings and Mobility to Drive Market Growth

The product demand is increasing as safety expectations rise across buildings and transportation. In construction, tougher glazing is required for impact resistance, fall protection, hurricane and blast performance, and safer breakage behavior, especially in high-rise facades, railings, skylights, and public infrastructure. In mobility, OEMs and regulators continue to push for improved passenger safety and structural integrity, increasing the use of tempered and laminated safety glass in windshields, side windows, and roofs. As modern designs use larger glass areas and thinner yet stronger formats, high strength glass becomes essential to meet both safety compliance and durability requirements. This safety-driven demand supports stable long-term consumption across core end-use industries. Hence, the steady demand for high performance building materials from high-rise construction and automotive will drive the global high strength glass market growth during the forecast period.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Energy and Processing Costs May Limit Market Expansion

The product manufacturing and processing are energy-intensive due to heating, tempering, lamination, and precision finishing. This makes the cost structure sensitive to fluctuations in electricity and fuel prices, especially in regions with volatile energy markets. In addition, quality standards are strict. Hence, yield losses and rejection rates can increase costs if process stability is not maintained. Many buyers, particularly in cost-sensitive construction projects, remain price-focused, limiting their ability to use high-performance glass products. As a result, while the demand is steady, profitability can be pressured during periods of energy inflation or when competition intensifies in standard-grade applications. Hence, high energy and processing costs may limit market expansion during the mid-term forecast.

MARKET OPPORTUNITIES

Growth of Solar and Harsh-Environment Applications to Create High-Value Demand Pockets

Solar energy is a high-growth opportunity with rising performance requirements. Projects increasingly require stronger and more durable glass to withstand hail, wind, sand abrasion, and extreme temperature changes. This is particularly relevant in the Middle East, parts of Asia, and regions with expanding desert solar projects. Suppliers that can offer consistent quality, high strength, and long-life performance are better positioned to win large-volume contracts. This creates a strong opportunity for processors with advanced heat-strengthening, lamination, and coating capabilities. As solar installations expand globally, this end-use will remain one of the most attractive growth markets for high strength glass.

Segmentation Analysis

By Product Type

Tempered (Toughened) Glass Segment Dominated due to High Usage for Safety across Construction and Mobility Sectors

Based on product type, the market is segmented into tempered (toughened) glass, laminated glass, heat strengthened glass, and others.

The tempered (toughened) glass segment held the largest market share in 2025. The strong demand is mainly due to its strong impact resistance and safer break pattern, making it widely used in facades, doors, partitions, railings, and automotive side glazing. It is preferred where safety compliance and durability are critical, while also supporting modern design trends such as larger glass panels. Steady demand from construction activity and ongoing adoption in mobility and public infrastructure will fuel the segment’s growth till 2034.

The laminated glass segment is projected to grow at a CAGR of 5.7% over the forecast period, supported by specification-led demand across safety-critical applications. The product demand is mainly driven by its ability to hold together upon breakage, making it suitable for windshields, overhead glazing, skylights, and security-focused architectural applications. It is increasingly used where fall protection, intrusion resistance, and better acoustic performance are required. As building codes and safety expectations tighten, laminated configurations are increasingly preferred in premium projects.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Construction & Architecture Segment Dominated in 2025 due to Safety Codes and High-Performance Facade Demand

Based on end use, the market is segmented into construction & architecture, automotive & transportation, solar energy, and others.

The construction & architecture segment accounted for the largest global high strength glass market share in 2025, supported by safety standards, large-scale glazing adoption, and increased use of curtain walls and facade systems. The glass is required in railings, skylights, overhead glazing, and high-rise facades to meet impact and safety compliance. The rising emphasis on energy-efficient buildings and modern design trends also supports stable demand.

The automotive and transportation segment is anticipated to grow at a CAGR of 5.4% over the forecast period. This growth is driven by ongoing safety requirements and the increasing glass area in vehicles, including larger windshields and panoramic roof designs. High strength glass helps improve structural performance, durability, and long-life clarity. As vehicles adopt lighter structures and more advanced glazing formats, the need for reliable toughened and laminated solutions remains stable.

The solar energy segment is expected to grow at the fastest CAGR of 7.5% over the analysis period. This is due to accelerating photovoltaic installations and rising durability requirements for module protection. High strength glass is increasingly required to withstand hail, wind loads, thermal cycling, and harsh outdoor conditions while maintaining optical performance over a long service life. Growth is especially strong in high-irradiation regions and large-scale utility projects where reliability is critical.

High Strength Glass Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific High Strength Glass Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025, reaching USD 19.47 billion, and is projected to reach USD 20.68 billion in 2026. The region’s leadership is supported by large-scale construction activity, rapid urbanization, and its position as a manufacturing hub for processed architectural and automotive glass. Asia Pacific benefits from the strong adoption of safety-grade glazing in high-rise buildings, expanding infrastructure spending, and rising vehicle and solar module production. With growing deployment of solar projects and increasing use of modern facade systems, the region continues to lead both in volume and in faster-growing applications.

China High Strength Glass Market

The China market is anticipated to reach a value of USD 10.37 billion in 2026, accounting for approximately 26% of global revenues. The product demand is primarily supported by China’s large-scale construction pipeline, including high-rise commercial buildings and urban infrastructure. In addition, China’s leadership in solar manufacturing and utility-scale installations increases the product demand in photovoltaic modules.

To know how our report can help streamline your business, Speak to Analyst

India High Strength Glass Market

The India market is set to reach USD 2.04 billion in 2026, representing roughly 5% of global revenues. The demand is driven by rapid urbanization, strong growth in residential and commercial construction, and increasing use of safety-grade glazing in modern building designs. The rising adoption of glass-intensive facades in offices, malls, airports, and metro infrastructure is driving the demand for tempered and laminated solutions.

North America

North America reached USD 6.32 billion in 2025 and is projected to touch USD 6.70 billion in 2026. Demand is supported by commercial construction, infrastructure upgrades, and steady specification-led adoption of safety glazing in public buildings. The region also benefits from the demand for high-performance glazing solutions used in architectural applications where durability and safety compliance are critical. Growth is expected to remain stable, driven by refurbishment cycles and long-term investments in building performance.

U.S. High Strength Glass Market

The U.S. market is anticipated to touch USD 6.06 billion in 2026, accounting for approximately 15% of global revenues. The demand is supported by specification-led construction markets where safety compliance, building performance, and durability standards remain high. Refurbishment and retrofit activity across commercial buildings also sustains steady consumption, particularly for energy-efficient facade upgrades and high-performance glazing systems.

Europe

The Europe market, which reached a valuation of USD 7.25 billion in 2025, is projected to grow at a rate of 4.3% over the forecast period. The region is shaped by strict safety standards, strong refurbishment activity, and high penetration of energy-efficient facade solutions. Europe’s market is more specification-led, with demand concentrated in premium architectural glazing, regulated safety applications, and automotive programs that emphasize durability and compliance. Investments in high-performance coated glass production support the region’s shift toward value-added products.

Germany High Strength Glass Market

The Germany market is anticipated to touch a value of USD 2.02 billion in 2026, accounting for approximately 5% of global revenues. Demand is driven by Germany’s premium construction standards, strong refurbishment activity, and high penetration of energy-efficient glazing in both residential and commercial buildings.

U.K. High Strength Glass Market

The U.K. market is anticipated to reach a value of USD 1.44 billion in 2026, representing around 4% of global revenues. Demand is supported by urban construction activity and refurbishment-driven upgrades in commercial buildings where safety glazing and energy performance improvements are increasingly required.

Latin America

The Latin America market reached USD 1.49 billion in 2025, driven by the gradual expansion of commercial construction, the increasing use of safety glass in urban buildings, and selective growth in solar and infrastructure projects. The market remains relatively price-sensitive, but the demand for safer glazing solutions is rising in premium projects.

Brazil High Strength Glass Market

The Brazil market is poised to touch a value of USD 0.62 billion in 2026, accounting for approximately 2% of global revenues. The increasing use of safety glazing in urban residential and commercial projects, and a rising preference for modern building aesthetics featuring larger glass surfaces will support the product demand in the country.

Middle East & Africa

The Middle East & Africa market was valued at USD 1.75 billion in 2025. The region represents a smaller but steadily developing market, supported by growing demand from large-scale infrastructure and real estate projects. Further growth is reinforced by energy and expansion that require durable glasses and long-life materials, where high strength glass is essential for performance reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Emphasize Wider Production Footprints and Capacity Investments to Gain an Edge

The high strength glass market is led by global manufacturers and technology-driven processors such as AGC Inc., Saint-Gobain, NSG Group, Guardian Glass, and Corning Inc., supported by broad production footprints and strong downstream relationships. Players are increasingly competing on integrated capabilities, float glass scale, tempering/lamination depth, coating technologies, and technical support for specification-heavy projects. Recent actions show a clear strategic direction, including capacity investments to strengthen high-performance coated glass supply and digital process optimization to improve energy efficiency and yield in furnace operations. As the demand for solar and premium facades rises, competitive advantage is shifting toward companies that can deliver consistent quality at scale and meet regulatory requirements. Furthermore, investments in technological advancements in glass manufacturing may change the competitive positioning during the forecast period.

LIST OF KEY HIGH STRENGTH GLASS COMPANIES PROFILED

- AGC Inc. (Japan)

- Corning Inc (U.S.)

- Guardian Glass (U.S.)

- NSG Group (Japan)

- Saint-Gobain (France)

- SCHOTT AG (Germany)

- Xinyi Glass (China)

- Cardinal Glass (U.S.)

- Euroglas (Germany)

- Flat Glass Group (China)

KEY INDUSTRY DEVELOPMENTS

- August 2025: India inaugurated its first tempered glass manufacturing facility for mobile devices in Noida, supporting domestic electronics supply chains. The manufacturing facility is established via partnership between Optiemus Infracom and Corning, a U.S.-based material technology firm, which will strengthen the company’s presence in domestic market.

- March 2025: NSG Group (Pilkington) announced an investment in an advanced glass-coating line in Poland to expand the production of high-performance, energy-saving coated glass to meet European building demand. The move strengthens the regional supply of value-added architectural glazing aligned with sustainability and energy-efficiency requirements, while improving local responsiveness for large-scale facade projects.

- January 2024: Saint-Gobain successfully acquired the “Glass Service”, a specialist in digital solutions for glass furnaces. The acquisition strengthens Saint-Gobain’s capability in furnace optimization, modeling, and control systems, supporting lower energy consumption, improved productivity, and process efficiency in glass manufacturing.

- January 2024: Sapphire Tuff inaugurated a state-of-the-art glass processing facility in Pune with advanced convection furnace technology. The expansion highlights ongoing investments in processing capacity to support higher-quality toughened glass output to meet diversified architectural and industrial demand.

- October 2021: Guardian Glass announced a significant investment at its float glass production facility in Goole, East Yorkshire, aimed at strengthening supply capabilities and improving operational efficiency. The upgrade will enhance the company’s ability to supply float glass primarily to the U.K. and Ireland markets, while also improving the plant’s energy performance.

REPORT COVERAGE

The global high strength glass market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Product Type, End Use, and Region |

| By Product Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 37.35 billion in 2025 and is projected to reach USD 63.98 billion by 2034.

In 2025, the market value stood at USD 19.47 billion.

The market is slated to exhibit a CAGR of 6.2% during the forecast period of 2026-2034.

The construction & architecture end use segment led the market in 2025.

Rising demand for safety-grade glazing in high-rise buildings and mobility is a key factor expected to drive market growth.

Saint-Gobain, NSG Group, Xinyi Glass, and Corning Inc. are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Shift toward energy-efficient facades and high-performance coated glass are major factors favoring product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us