Hydrofluoric Acid Market Size, Share & Industry Analysis, By Grade (Anhydrous and Diluted), By Application (Fluorocarbon, Fluorinated Derivatives, Metal Pickling, Glass Etching, Oil Refining, and Others), and Regional Forecast, 2026-2034

Hydrofluoric Acid Market Size and Future Outlook

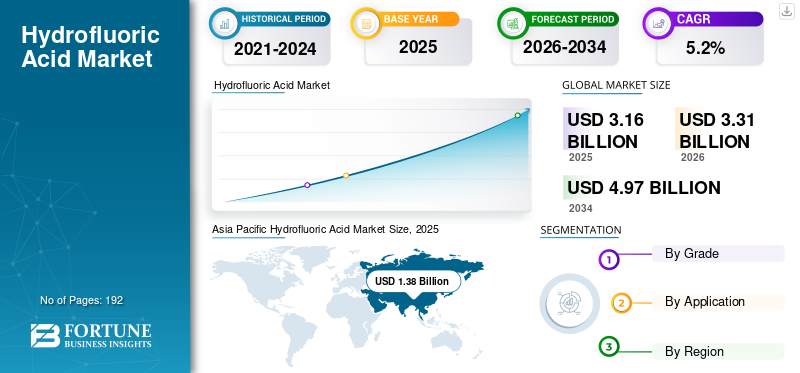

The global hydrofluoric acid market size was valued at USD 3.16 billion in 2025. The market is projected to grow from USD 3.31 billion in 2026 to USD 4.97 billion by 2034 at a CAGR of 5.2% during the forecast period. Asia Pacific dominated the global hydrofluoric acid market with a market share of 43.67% in 2025.

Hydrofluoric acid (HF) is a critical inorganic chemical used both as a direct processing chemical and as an intermediate to produce a wide range of fluorine-containing chemicals. Major consumption pathways include fluorocarbon and broader fluorochemical production, metal pickling and surface treatment, petroleum alkylation, and glass etching. Industry background sources also highlight that HF is used in aluminum-related processing and other industrial applications, making demand closely tied to industrial production cycles and fluorochemical supply chains.

Asia Pacific as the largest region and fluorocarbon production as the leading application, which fits the practical reality that a large portion of HF demand is pulled by fluorine chemistry and industrial processing clusters concentrated in Asia. Derivados del Fluor, S.A.U., Foosung Co., Ltd., Honeywell, Orbia Fluor & Energy Materials, Navin Fluorine International Ltd., and Sinochem Lantian Co., Ltd. are the key players operating in the market.

Download Free sample to learn more about this report.

Hydrofluoric Acid Market Key Takeaways

- 2025 Market Size: USD 3.16 billion

- 2026 Market Size: USD 3.31 billion

- 2034 Forecast Market Size: USD 4.97 billion

- CAGR: 5.2% from 2026-2034

- Asia Pacific dominated the hydrofluoric acid market with a 43.67% share in 2025.

- The diluted (aqueous) hydrofluoric acid segment is anticipated to grow at a CAGR of 5.4% during the forecast period.

- The fluorinated derivatives segment is expected to grow at a CAGR of 4.9% during the forecast period.

Asia Pacific

Asia Pacific remained the leading regional market in 2025, supported by strong fluorochemical and electronics manufacturing activities.

North America

North America demand is driven by petroleum alkylation, stainless steel pickling, and downstream chemical manufacturing applications.

Europe

Europe's market is supported by stringent environmental regulations and strong demand from metal treatment and chemical manufacturing industries.

U.S.

The market was valued at USD 0.28 billion in 2025, accounting for approximately 18.7% of global sales.

Japan

Demand is supported by the country's advanced electronics, semiconductor, and specialty chemical manufacturing sectors.

Read More

HYDROFLUORIC ACID MARKET TRENDS

Grade Differentiation and Premiumization Toward Anhydrous to be a New Market Trend

The trend is the increasing segmentation of HF by grade, concentration, and impurity specification, rather than treating HF as a single commodity. Anhydrous HF tends to hold a leading position by grade, reflecting its importance as an intermediate for downstream fluorochemical synthesis and industrial chemical processes. This trend elevates the importance of quality control, consistent concentration, and reliable delivery formats across the supply chain.

This grade differentiation also changes how value is distributed across applications. Higher-purity requirements in electronics and advanced fluorochemical support premium pricing and longer-term contracting, while bulk industrial applications remain more cost-driven. As a result, suppliers with purification and packaging capabilities can grow value share even if their tonnage share is smaller, creating a market structure where portfolio strategy matters as much as scale.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Cooling and Industrial Fluorochemical Demand to Foster Market Growth

Hydrofluoric acid sits at the front end of fluorochemical value chains, so demand is structurally supported by production of fluorocarbons and related fluorinated molecules used in refrigerants, blowing agents, and specialty fluorochemical. Market research coverage consistently identifies fluorocarbon production as the largest application area, indicating that cooling and industrial fluorochemical demand continues to be the biggest direct lever on HF consumption.

In 2025, the demand was additionally reinforced by ongoing refrigerant portfolio transitions. Regulations and industry conversion cycles are shifting the mix of fluorinated products rather than removing the need for fluorine chemistry in the near term, so HF remains embedded upstream even as product compositions change. This dynamic keeps HF demand resilient across replacement cycles in cooling equipment, while also supporting higher-value specialty fluorochemical production in selected regions.

MARKET RESTRAINTS

Severe Hazard Profile Increases Delivered Cost and Restricts Flexible Logistics

Hydrofluoric acid’s toxicity and corrosive nature significantly increase the cost and complexity of handling, transportation, storage, and workplace safety. These factors act as a structural restraint on hydrofluoric acid market growth, as strict compliance requirements add costs for both producers and end users, making HF less logistically flexible than many commodity chemicals. The need for specialized containers, trained operators, and extended qualification timelines further limits adoption, particularly in smaller applications where technical substitutes are available.

Regulatory hazard classifications reinforce this constraint. ECHA’s dossier information reflects the severity of HF hazards, which translates into stricter site-level controls and risk management expectations across Europe. These realities tend to shift purchasing toward larger, established suppliers with strong EHS systems and away from fragmented sourcing, which can cap incremental penetration in smaller end uses and increase barriers to entry for new producers and distributors.

MARKET OPPORTUNITIES

Semiconductor Expansion Increases High-Purity HF Consumption and Value Intensity

Electronics and semiconductor manufacturing create an attractive opportunity as they demand higher chemical purity and more controlled delivery systems. Market research commentary highlights semiconductor-linked demand as a growth contributor, which aligns with the industry reality that wet etching and cleaning steps require specialty-grade process chemicals. This can raise value growth faster than volume growth as electronics-grade material typically carries higher pricing due to tighter impurity control and packaging requirements.

Industry forecasts supported the direction of this opportunity in 2025. For HF suppliers, this shifts the competitive focus toward purification capability, contamination control, and qualified supply relationships, increasing differentiation and margin potential within the overall HF market.

MARKET CHALLENGES

Feedstock Security and Supply-Chain Volatility to Challenge Market Growth

HF production is tightly linked to fluorspar availability and conversion economics, and supply disruption risks are amplified by HF’s hazardous logistics profile. Even when demand is strong, the market can face localized shortages due to feedstock constraints, conversion outages, or shipping restrictions, since HF cannot be rerouted as easily as less hazardous bulk chemicals. This creates volatility in lead times and delivered prices, which can weigh on downstream planning for refrigerants, metals, and electronics users.

Over the medium term, the Kigali-driven transition in fluorochemical portfolios adds another layer of complexity.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitics can affect the Hydrofluoric Acid (HF) market first through supply availability, cost, and lead times, as HF is upstream-linked to fluorspar and is often traded across borders in hazardous-chemical logistics chains.

On the demand and industry-structure side, protectionism tends to accelerate regionalization as downstream buyers (fluorochemicals, electronics, metals, refining) place more weight on assured supply, multi-sourcing, and localized inventories, even at higher cost. This can lift “cost-to-serve” and encourage longer contracts, while also shifting trade flows away from spot optimization.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in hydrofluoric acid is increasingly concentrated in semiconductor-grade and ultra-high-purity HF, as device scaling keeps tightening impurity tolerances and pushes fabs to demand cleaner, more consistent wet-chemistry performance. Semiconductor industry specifications (e.g., SEMI chemical standards referenced in technical literature) have historically driven impurity limits down to ppb-level for HF solutions, forcing suppliers to invest in advanced purification trains, contamination-controlled packaging, and better analytical control loops.

SEGMENTATION ANALYSIS

By Grade

Anhydrous Segment Dominates as it is a Preferred Intermediate for Making Downstream Fluorochemicals and Other Fluorine Derivatives

Based on grade, the market is segmented into anhydrous and diluted.

Anhydrous holds the dominant market share. Anhydrous Hydrofluoric acid (AHF) typically anchors the core industrial value chain as it is the preferred intermediate for making downstream fluorochemicals and other fluorine derivatives. USGS notes that acid-grade fluorspar is used to produce anhydrous HF, and that HF is the primary feedstock for most fluorine-bearing chemicals such as refrigerants and fluoropolymers, which structurally supports demand for AHF-grade supply into large, integrated chemical complexes.

Diluted (aqueous) hydrofluoric acid is more visible in direct-use processing applications, where it functions as an active etchant/cleaning/pickling reagent rather than as a synthesis intermediate. EPA’s industry background describes HF’s use in glass etching/polishing, stainless steel pickling, and other industrial processing uses, which commonly employ aqueous HF solutions blended or controlled to specific concentrations for safe handling and process performance. The segment anticipated to grow at a CAGR of 5.4% during the study period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Fluorocarbon Leads Due to High Adoption in Panels and Interior Components

Based on application, the market is segmented into fluorocarbon, fluorinated derivatives, metal pickling, glass etching, oil refining, and others.

Fluorocarbon segment dominates the market during the forecast period. Fluorocarbon is an upstream reactant/intermediate for many fluorinated molecules used in refrigerants and fluorochemical chains. HF is the primary feedstock for virtually all fluorine-bearing chemicals, particularly refrigerants and fluoropolymers, which keeps this segment anchored even as product mixes change. Growth projects at 5.9% CAGR through 2034, driven by energy efficiency mandates.

The fluorinated derivatives segment holds a significant share with growth rate of 4.9% during the forecast period. This segment captures HF consumption used to make other fluorine intermediates and derivative chemicals (e.g., inorganic fluorides, fluorinated building blocks, and fluoropolymer related feedstocks that aren’t counted directly under “fluorocarbon” in a segmentation scheme). USGS’ framing that HF is the primary feedstock for virtually all fluorine-bearing chemicals provides the most defensible basis for why this segment remains a core pillar of demand

Metal pickling is a steady, industrial base-load segment where HF is used (often with nitric acid) to remove oxides/scale and restore corrosion resistance especially for stainless. World stainless explicitly states that the most important constituents of stainless pickling products are nitric and hydrofluoric acids, which is a strong, industry association anchor for the relevance of HF in this segment. The segment is anticipated to grow at a CAGR of 4.8% during the study period.

Glass etching to register a positive growth. HF is unique in its ability to chemically dissolve silica-based glass, making it a core wet-etch agent for frosting, patterning, and surface modification. Peer-reviewed literature notes that at room temperature many glasses can only be dissolved in hydrofluoric acid or HF-containing aqueous solutions, which is why HF remains central to wet etching methods.

The others segment includes electronics/semiconductor etching & cleaning, uranium conversion, mineral digestion, and various niche industrial cleaning uses. While total volumes are relatively small, this segment can be highly value-skewed when demand for electronics-grade HF increases, due to stringent impurity specifications and the need for specialized packaging. It is also the most heterogeneous segment, as demand drivers vary widely. Electronics-related uses are cyclical and tied to semiconductor capital expenditure, whereas nuclear and mineral processing applications are more policy-driven or linked to specific long-term projects.

HYDROFLUORIC ACID MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Hydrofluoric Acid Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading hydrofluoric acid market share in 2025. The growth is driven by its concentration of fluorochemical manufacturing and heavy industrial processing demand. The region’s demand also benefits from the breadth of applications described in EPA’s background especially fluorocarbon-related production and industrial uses amplified by large scale manufacturing ecosystems. Asia Pacific tends to be both volume-dominant and increasingly value intensive where higher purity supply is needed for advanced manufacturing.

China Hydrofluoric Acid Market

China’s market is one of the largest globally, with 2025 revenue valued at USD 0.71 billion, representing roughly 22.5% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

In North America, hydrofluoric acid demand is supported by a mix of industrial processing and downstream chemical manufacturing, with steady pull from applications such as petroleum alkylation, stainless steel pickling, and fluorochemical supply chains. EPA’s HF industry background highlights petroleum alkylation and stainless pickling as key uses, which aligns with demand clusters around refining and metals-processing hubs.

U.S. Hydrofluoric Acid Market

In 2025, the U.S. market was valued at USD 0.28 billion, driven primarily by strong demand from the industrial sectors. The U.S. accounts for roughly 18.7% of global market sales.

Europe

Europe’s HF market is shaped by strong EHS/compliance intensity and a solid industrial base where HF is used in metal pickling, surface treatment, and chemical manufacturing value chains. The most important constituents of stainless steel pickling products are nitric and hydrofluoric acids, underpinning recurring industrial demand in fabrication and finishing. EPA’s background also lists stainless pickling among the main HF uses, reinforcing that this is not a niche application.

Germany Hydrofluoric Acid Market

The Germany market in 2025 was valued at around USD 0.14 billion, representing roughly 4.4% of global market revenues.

U.K. Hydrofluoric Acid Market

The U.K. market in 2025 was valued at around USD 0.09 billion, representing roughly 3.0% of global market revenues.

Latin America

Latin America holds a smaller share of global HF demand but remains relevant through industrial processing (metals, glass-related uses) and selective chemical manufacturing growth. The core application set described by EPA glass etching/polishing, stainless pickling, and industrial uses maps well to demand that rises and falls with local manufacturing and infrastructure cycles.

Brazil Hydrofluoric Acid Market

The Brazil market in 2025 was valued at around USD 0.12 billion, representing roughly 3.9% of global market revenues.

Middle East & Africa

In the Middle East & Africa, HF demand is typically influenced by refining and industrial hubs, with consumption patterns tied to the presence of alkylation units and broader industrial processing needs. EIA notes alkylation can use hydrofluoric acid (or sulfuric acid) as the catalyst, and industry references emphasize the operational importance of alkylation for producing alkylate for gasoline blending making refining configuration a key determinant of HF demand in this region.

GCC Hydrofluoric Acid Market

The GCC market in 2025 was valued at around USD 0.09 billion, representing roughly 2.7% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Process Optimization and Product Quality Enhancement to Strengthen Market Position

Major investments are underway in the market as manufacturers respond to rising sustainability expectations and higher performance requirements across end-use industries. Leading producers, such as Derivados del Fluor, S.A.U., Foosung Co., Ltd., Honeywell, Orbia Fluor & Energy Materials, Navin Fluorine International Ltd., Sinochem Lantian Co., Ltd., are directing capital toward process optimization, product quality enhancement and environmentally aligned manufacturing practices. Innovation efforts are increasingly focused on enhancing purity consistency, reducing the environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY HYDROFLUORIC ACID COMPANIES PROFILED IN REPORT

- Derivados del Fluor, S.A.U. (Spain)

- Foosung Co., Ltd. (South Korea)

- Honeywell (U.S.)

- Orbia Fluor & Energy Materials (U.S.)

- Navin Fluorine International Ltd. (India)

- Sinochem Lantian Co., Ltd. (China)

- Solvay (Belgium)

- Stella Chemifa Corporation (Japan)

- TANFAC Industries Ltd. (India)

- Morita Chemical Industries (Japan)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Navin Fluorine International Limited announced an exclusive technology tie-up with Buss ChemTech AG during their FY25 earnings call. This partnership targets the commercialization of solar and electronic grade hydrofluoric acid (HF), aligning with their upcoming anhydrous HF plant commissioning in FY26.

- October 2024: Tanfac Industries invested around USD 12 million from internal funds to expand its hydrofluoric acid output twofold to 29,500 MTPA, strengthening its position to capture rising domestic and export demand while enhancing competitiveness.

REPORT COVERAGE

The hydrofluoric acid report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, grade, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.2% from 2026 to 2034 |

|

Segmentation |

By Grade, By Application, By Region |

|

By Grade |

· Anhydrous · Diluted |

|

By Application |

· Fluorocarbon · Fluorinated Derivatives · Metal Pickling · Glass Etching · Oil Refining · Others |

|

By Region |

· North America (By Grade, By Application, By Country) o U.S. (By Application) o Canada (By Application) · Europe (By Grade, By Application, By Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Rest of Europe (By Application) · Asia Pacific (By Grade, By Application, By Country) o China (By Application) o India (By Application) o Japan (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Grade, By Application, By Country) o Mexico (By Application) o Brazil (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Grade, By Application, By Country) o GCC (By Application) o South Africa (By Application) o Rest of Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.16 Billion in 2025 and is projected to reach USD 4.97 Billion by 2034.

Recording a CAGR of 5.2%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The fluorocarbon segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Cooling and industrial fluorochemical demand to drive market growth

- 2021-2034

- 2025

- 2021-2024

- 192

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us