Hydrogen Truck Market Size, Share & Industry Analysis, By Component (Hydrogen Tank, Fuel Cell System, Battery, Motor, and others), By Powertrain (FCEV and H2-ICE), By Vehicle Type (Light Duty, Medium Duty, Heavy Duty, and others), By Application (Logistics & Freight, Municipal & Public Services, Off-road, and others) and Regional Forecasts, 2026-2034

Hydrogen Truck Market Size and Future Outlook

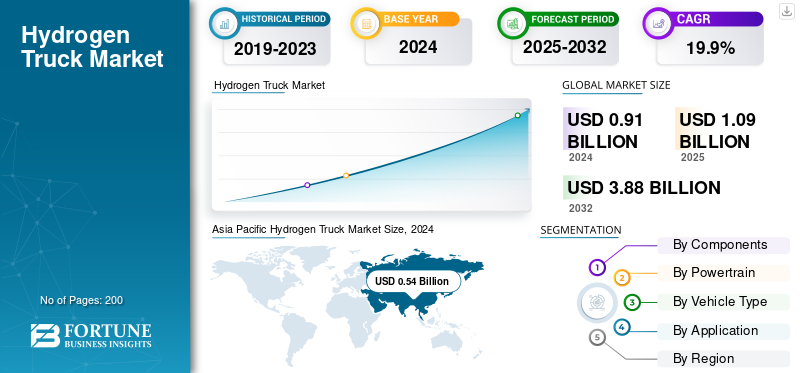

The global hydrogen truck market size was valued at USD 1.09 billion in 2025. The market is projected to grow from USD 1.36 billion in 2026 to USD 4.97 billion by 2034, exhibiting a CAGR of 17.62% during the forecast period. Asia Pacific dominated the hydrogen truck market with a market share of 60.52% in 2025.

Hydrogen trucks are vehicles that use hydrogen as a power source, either through a fuel cell that produces electricity to drive an electric motor or through a modified internal combustion engine (ICE) that directly burns hydrogen. They are built to handle heavy loads and long ranges while offering an alternative to conventional trucks that typically run on diesel, natural gas, or other fuels. Tailpipe emissions are minimal since fuel cell technology-driven trucks release only water vapor, while hydrogen ICE trucks can produce very low levels of nitrogen oxides (NOx) compared to diesel.

The attractive point of hydrogen-powered trucks comes from their quick refueling times, compared to diesel, and their ability to decarbonize freight without compromising payload or uptime. This makes them suitable for industries such as logistics, long-haul freight, and construction, where reliability and turnaround time are critical.

The market is growing as governments are tightening emission norms, the industry key players want greener supply chains, and infrastructure for hydrogen is slowly expanding. On the industrial side, companies are pushing different strategies. Toyota is working with Hino Motors in Japan to build hydrogen fuel cell trucks for freight transport. Daimler Truck has developed the GenH2 prototype targeting long-haul freight. Hyundai has already deployed its XCIENT hydrogen trucks in Switzerland for fleet operators. Nikola in the U.S. is building fuel cell trucks paired with its own hydrogen refueling stations. These moves show the sector is shifting from pilots to real operations.

Download Free sample to learn more about this report.

Hydrogen Truck Market Key Takeaways

- 2025 Market Size: USD 1.09 billion

- 2026 Market Size: USD 1.36 billion

- 2034 Forecast Market Size: USD 4.97 billion

- CAGR: 17.62% from 2026–2034

- Asia Pacific dominated the hydrogen truck market with a 60.52% share in 2025.

- Fuel Cell Systems is expected to lead the market with a 54.57% share in 2026.

- FCEVs are projected to dominate the market with a 71.54% share in 2026.

Asia Pacific

Asia Pacific led the global market with USD 0.66 billion in revenue in 2025 and is projected to reach USD 0.83 billion in 2026.

Europe

Europe accounted for 20.34% of the global market in 2025 and is expected to reach USD 0.27 billion in 2026.

North America

North America contributed 19.14% of global market revenue in 2025.

U.S.

The market is projected to reach USD 0.24 billion by 2026.

Japan

The hydrogen truck market is projected to reach USD 0.13 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Stricter Emission Norms are driving Demand for Hydrogen Trucks

Governments globally are tightening emission norms to cut carbon dioxide and nitrogen oxide from freight transport. Hydrogen trucks offer a zero or near-zero emission solution, with quick refueling and heavy-load capability, making them more attractive than diesel alternatives. Fleets are shifting toward hydrogen to meet sustainability targets.

- For instance, in June 2024, Hyundai deployed its XCIENT Fuel Cell trucks in Switzerland, supported by government incentives and emission-reduction targets for logistics fleets.

MARKET RESTRAINTS:

High Hydrogen Production and Vehicle Costs Limit Adoption

Hydrogen fuel and fuel-cell systems are still far more expensive than diesel or battery-electric alternatives. These high costs raise the total cost of ownership for fleets, slowing down commercial adoption until large-scale production brings prices down.

- For instance, in December 2023, Daimler Truck reported that its GenH2 fuel cell prototypes are still significantly more expensive to build than diesel models, and large-scale cost reductions will only come once hydrogen supply chains mature.

MARKET OPPORTUNITIES:

Government Support Creating Pathways for Hydrogen Corridors

Public funding and partnerships are accelerating the rollout of hydrogen fueling infrastructure and fleets. Incentives lower upfront costs and create demonstration projects that build operator confidence. These early-stage hydrogen corridors will enable long-haul freight and logistics companies to adopt trucks at scale.

- For instance, in May 2023, the governments of Victoria and New South Wales launched the Hume Hydrogen Highway initiative, backed by a joint investment of AUD 20 million. The project will establish multiple hydrogen refueling stations along the busy Melbourne–Sydney freight route and deploy around 25 hydrogen-powered heavy trucks.

HYDROGEN TRUCK MARKET TRENDS

OEMs Investing in Low-Cost Hydrogen Production Methods is a Significant Trend

Market leaders are focusing on cheaper hydrogen through renewable-powered electrolysis (green hydrogen) and carbon-captured natural gas (blue hydrogen). By reducing fuel costs, OEMs and renewable energy providers aim to make hydrogen trucks competitive with diesel in both price and performance.

- For instance, in February 2024, Reliance Industries claimed to convert 5,000 of its internal diesel trucks into hydrogen ICE trucks, while simultaneously building green hydrogen production capacity, in order to reduce operating fuel costs and improve performance benchmarks relative to existing diesel fleets.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Limited Hydrogen Refueling Infrastructure Slows Market Expansion

The lack of widespread hydrogen refueling stations is a major hurdle for fleet operators. Without reliable access to fueling stations, long-haul trucks face range limitations, keeping adoption restricted to pilot routes and specific regions.

- For instance, October 2024, in the U.S. most hydrogen stations are concentrated in California, limiting commercial truck operations outside the state despite rising OEM interest.

Hydrogen Truck Market Segmentation Analysis

By Component

Hydrogen Tank Dominates Owing to Storage Efficiency and Safety Requirements

On the basis of components, the market is segmented into hydrogen tanks, fuel cell systems, batteries, motor, and others.

The Fuel Cell Systems egment is expected to lead the market, contributing 54.57% globally in 2026.

In 2026, the market was dominated by the hydrogen tank segment, as it plays a critical role in storing compressed hydrogen safely at high pressure and ensuring consistent fuel delivery to the powertrain. Manufacturers are focusing on lightweight composite tanks to improve storage capacity while meeting strict safety standards.

- For instance, in November 2024, Hexagon Purus supplied advanced hydrogen storage tanks for fuel cell technology driven trucks, enabling long driving ranges without compromising payload.

By Powertrain

Fuel Cell Electric Vehicles Lead Due to Zero-Emission Performance

Based on powertrain, the market is categorized into fuel cell electric vehicles (FCEV) and hydrogen internal combustion engine (ICE) trucks.

In 2026 FCEVs segment is projected to lead the market with a 71.54% share. The FCEVs held the largest hydrogen truck market share, driven by their ability to provide zero tailpipe emissions, high efficiency, and longer ranges compared to battery-electric trucks. Fleet operators are adopting FCEVs to align with emission mandates and reduce operational downtime through faster refueling.

- For instance, in November 2022, Daimler Truck’s GenH2 prototype was designed as a long-haul FCEV, aiming to deliver 1,000 km ranges with only water vapor as the emission output.

By Vehicle Type

Heavy-Duty Trucks Dominate, Supported by Long-Haul Applications

On the basis of vehicle type, the market is divided into light-duty, medium-duty, and heavy-duty trucks.

The heavy-duty segment is anticipated to hold a dominant market share of 73.75% in 2026. The heavy-duty segment dominated due to the need for clean alternatives in long-haul freight, construction, and mining operations. Heavy-duty hydrogen trucks offer higher payload capacities and longer driving ranges, making them well-suited for industries where diesel engines have traditionally been the backbone.

- For instance, in May 2024, Volvo developed hydrogen powered heavy-duty trucks for long-haul transport, targeting fleet customers that require both endurance and sustainability.

To know how our report can help streamline your business, Speak to Analyst

By Application

Logistics and Freight Lead Due to Fleet Decarbonization Push

Based on application, the market is segmented into logistics & freight, municipal services, off-road, and others.

The logistics and freight segment is poised to account for 69.32% of the market share in 2026. The logistics and freight emerged as the leading segment, supported by the rapid demand for decarbonizing supply chains and meeting corporate sustainability targets. Fleet operators prefer hydrogen trucks for their quick refueling and reliable long-distance operation.

- For instance, in May 2025, Adani unveiled a 40-tonne hydrogen powered truck, boasting a range of approximately 200 km, designed to transport coal from the Gare Pelma III Block to a nearby power plant, targeting logistics and freight operations.

Hydrogen Truck Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Hydrogen Truck Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 0.66 Billion in 2025, capturing 60.52% of the global market share, and is projected to reach USD 0.83 Billion in 2026. This dominance is supported by strong government initiatives, large-scale vehicle manufacturing capacity, and early hydrogen adoption programs. China, Japan, and South Korea are leading the charge, with national roadmaps, subsidies, and investments in hydrogen refueling corridors to promote commercial vehicle adoption. The presence of domestic OEMs combined with global partnerships further reinforces the region’s leadership in hydrogen trucks. The Japan market is projected to reach USD 0.13 billion by 2026, the China market is projected to reach USD 0.46 billion by 2026, and the India market is projected to reach USD 0.05 billion by 2026.

- For instance, in April 2025, China launched a 1,150 km hydrogen trucking corridor route (Chongqing → Qinzhou) with refueling stations, for heavy-duty fuel cell trucks.

Europe

The Europe market accounted for USD 0.22 Billion in 2025, representing 20.34% of the global industry, and is expected to reach USD 0.27 Billion in 2026. The European market is driven by strict emission reduction targets and investments in hydrogen corridors, with countries such as Germany, France, and Netherlands piloting heavy-duty hydrogen truck fleets. The France market is projected to reach USD 0.04 billion by 2026, and the Germany market is projected to reach USD 0.11 billion by 2026.

North America

In 2025, North America generated USD 0.21 Billion, contributing 19.14% to global market revenue, and is projected to grow to USD 0.26 Billion in 2026. In North America, the U.S. is progressing with hydrogen truck pilots led by players such as Nikola and PACCAR, supported by funding from the Department of Energy and state-level clean transport programs. The U.S. market is projected to reach USD 0.24 billion by 2026.

Rest of the World

Over the forecast period, markets in the rest of the world, including Latin America and the Middle East & Africa, are expected to expand at a gradual pace. Government-led hydrogen strategies in countries such as Chile and Saudi Arabia are expected to create opportunities, though adoption will remain smaller compared to Asia Pacific, Europe, and North America.

COMPETITIVE LANDSCAPE

Key Industry Players:

Collaborations and Technology Diversification Strengthen Market Position

The hydrogen truck market displays a developing but semi-concentrated structure, with global OEMs, fuel-cell specialists, and regional manufacturers driving commercialization. Leading players are focusing on strategic alliances, pilot fleet deployments, and integrated fuel infrastructure to secure a competitive edge. Their strategies combine vehicle development with hydrogen supply partnerships, positioning them strongly for future large-scale adoption.

Daimler Truck, Hyundai Motor Company, and Toyota Motor Corporation are among the key leaders shaping this market. Daimler is advancing its GenH2 fuel cell trucks targeted at long-haul freight. Hyundai has already rolled out its XCIENT Fuel Cell trucks in Switzerland and South Korea. Toyota, working with Hino Motors, is developing hydrogen fuel cell trucks for urban logistics. These players reinforce their leadership with strong R&D, global partnerships, and early real-world deployments.

In addition, other active players include Nikola Corporation, Volvo Group, Iveco, and PACCAR Inc. These companies are investing in regional production hubs, partnerships with renewable energy providers, and dedicated refueling solutions to accelerate adoption.

- For instance, in March 2023, Nikola deployed its Tre FCEV trucks in the U.S. market while simultaneously building hydrogen fueling infrastructure through its HYLA brand, ensuring both vehicle supply and fuel availability for customers.

LIST OF KEY HYDROGEN TRUCK COMPANIES PROFILED:

- Hyundai Motor Company (South Korea)

- Daimler Truck AG (Germany)

- Volvo Trucks (Sweden)

- Hyzon Motors (U.S.)

- H2X Global Limited (Australia)

- Toyota Motor Corporation (Japan)

- Dongfeng Motor Corporation (China)

- FAW Group (China)

- Renault (France)

- Ashok Leyland (India)

KEY INDUSTRY DEVELOPMENTS:

- August 2025: Rockcheck Group (Inner Mongolia, China) signed a deal to deploy 1,000 hydrogen-powered heavy-duty trucks by 2026 in a zero-carbon freight corridor in Baotou, signaling large-scale adoption.

- July 2025: Hyundai Motor announced expansion of its XCIENT Fuel Cell trucks into the U.S. market, with first deliveries scheduled for California under state-backed clean transport programs.

- June 2025: Toyota Motor Europe & VDL Group launched zero tailpipe emissions logistics operations using Toyota's fuel cell system integrated into heavy-duty trucks in Brussels, underscoring Europe’s push into commercial hydrogen trucking.

- June 2025: Daimler Truck’s GenH2 Truck completes over 225,000 km in real-world trials with customers including Amazon, Holcim & INEOS in Germany, demonstrating hydrogen trucks can work in heavy logistics.

- March 2025: A batch of 100 hydrogen-powered heavy-duty trucks with 200 kW output rolled off the production line in Tianjin, China. These trucks offer a driving range exceeding 700 km and mark progress toward mass production of hydrogen heavy-duty vehicles.

REPORT COVERAGE

The global hydrogen truck market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 17.62% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Components

By Powertrain

By Vehicle Type

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.36 billion in 2026 and is projected to reach USD 4.97 billion by 2034.

In 2025, the market value stood at USD 0.21 billion.

The market is expected to exhibit a CAGR of 17.62% during the forecast period.

The heavy-duty segment led the market by vehicle type.

The key factor driving the market is stricter emission norms driving the demand for hydrogen trucks.

Hyundai Motor Group, Hyzon Motors, Dongfeng Motor Corporation, and Toyota Motor Corporation are some of the prominent players in the market.

Asia Pacific dominated the hydrogen truck market with a market share of 60.52% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us