In Flight Internet Market Size, Share & Industry Analysis, By Component (Service and Equipment), Connectivity Type (Satellite and Air-to-Ground (ATG)), By Aircraft Type (Narrow body, Wide Body, and Regional Jet), By Installation (Retrofit and Line Fit), and Regional Forecast, 2026-2034

In Flight Internet Market Size & Industry Overview

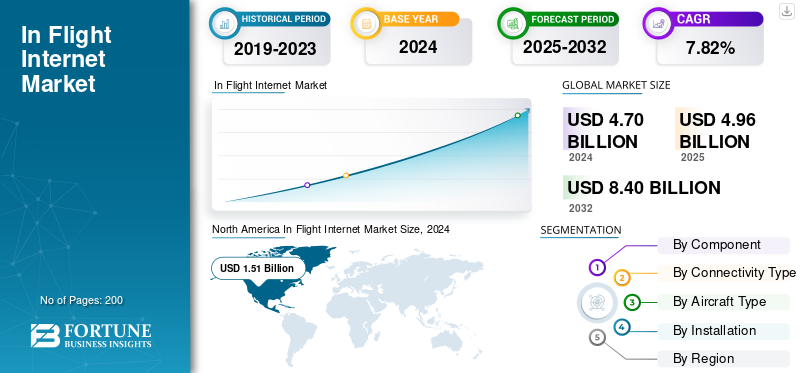

The global in flight internet market size was valued at USD 4.96 Billion in 2024. The market is projected to grow from USD 5.69 Billion in 2026 to USD 9.29 Billion by 2034, exhibiting a CAGR of 6.30% during the forecast period. North America dominated the in flight internet market with a market share of 32.10% in 2025.

The in-flight internet (IFC) market covers the hardware, bandwidth, integration, and managed services that bring real-time broadband to commercial aircraft cabins and flight decks, chiefly via satellite links (Ku/Ka on GEO today with fast-ramping LEO and hybrid multi-orbit options) and, in a few short-haul geographies, air-to-ground systems. Market expansion is shaped by rising passenger expectations for seamless, often free, flight Wi Fi; airline digitization agendas that rely on connected EFBs, predictive maintenance, live weather, and crew operations; and technology shifts that lift capacity and cut total cost of ownership, high-throughput satellites, electronically steered low-drag antennas, modular modems, and open architectures that let carriers change or blend providers. Line-fit offerability from the airframers and large retrofit programs at major MRO hubs sustain installation pipelines, while sponsorship models and payment platforms improve take-rates and monetization.

Competitive dynamics are anchored by a handful of certified, globally scaled key players: Viasat (including the former Inmarsat) with deep Ka capacity and OEM integrations; Intelsat with extensive Ku coverage and hybrid solutions; Panasonic Avionics coupling Ku networks with tightly integrated IFE platforms; Eutelsat OneWeb supplying LEO capacity into partner solutions; SpaceX Starlink building a direct-to-airline LEO footprint; Thales offering end-to-end cabin high speed connectivity solutions and avionics integration; Anuvu pursuing HTS and micro-GEO strategies for flexible coverage; and Hughes providing gateways and aero modems across Ka ecosystems.

Winning propositions combine multi-orbit reach, certified antennas with aerodynamic efficiency, robust SLAs, cybersecurity, regulatory compliance, and commercial aviation flexibility across free, freemium, and premium tiers aligned to airline brand, route mix, and turnaround constraints.

Download Free sample to learn more about this report.

In Flight Internet Market Key Takeaways

- 2025 Market Size: USD 4.96 billion

- 2026 Market Size: USD 5.69 billion

- 2034 Forecast Market Size: USD 9.29 billion

- CAGR: 6.30% from 2026–2034

- North America dominated the in flight internet market with a 32.10% share in 2025.

- The service segment is expected to account for 23.17% of the market share in 2026.

- The satellite segment is projected to hold 23.59% of the market share in 2026.

North America

North America led the global market in 2025 with a valuation of USD 1.59 billion and a 32.08% market share.

Europe

Europe accounted for 27.88% of global revenue in 2025 and is projected to reach USD 1.58 billion in 2026.

Asia Pacific

Asia Pacific captured 25.40% of global revenue in 2025 and is expected to reach USD 1.46 billion in 2026.

U.S.

The in flight internet market is projected to reach USD 1.55 billion by 2026.

Japan

The market is projected to reach USD 0.32 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

High-Quality Wi-Fi Becoming A Brand Standard, Leading To High Growth Of In Flight Internet

Airlines are shifting from “paid, basic connectivity” to “free, fast, always-on” as a core brand promise, which materially lifts take-rates, ad/sponsorship inventory, and NPS. The driver is twofold: passengers now benchmark the cabin against ground broadband, and airline operations increasingly depend on a live pipe for EFB updates, live weather, crew messaging, and predictive maintenance. As free tiers spread, carriers are upgrading to multi-gigabit architectures and revisiting commercial models (sponsor-funded, loyalty-gated, or freemium). This, in turn, accelerates retrofit programs across narrow-body fleets where the majority of daily sectors occur. The competitive effect is circular: once one network carrier offers “fast and free” across most flights, its rivals must respond or risk losing customers on short-haul routes, where choice is greatest.

- March 2025: United Airlines received FAA approval for its first Starlink-equipped aircraft and announced that service will be free for MileagePlus members, with rapid fleetwide retrofits slated to follow.

MARKET RESTRAINTS

Regulatory And Reliability Headwinds Raise Cost And Time To Certify, Restricting Market Growth

Despite a clear rising demand, IFC projects face non-trivial headwinds. Cybersecurity requirements are tightening, adding design, test, and documentation load to antennas, modems, routers, and software that interface with aircraft systems. Operators must also navigate export controls, spectrum coordination, and airworthiness approvals for every airframe/antenna combination (each STC consuming slots and MRO time). On-orbit incidents and fleet management (e.g., de-orbiting, in-service anomalies) can constrain capacity planning and force expensive re-routing of traffic. The net effect is longer lead times, more contingency inventory, and a higher bar for suppliers to prove resilience and maintain SLAs. Airlines balance these risks by favoring multi-orbit options and contractual performance guarantees, yet certification queues and security reviews still slow rollouts, especially on smaller sub fleets.

- August 2024: The FAA issued a proposed rulemaking to standardize cybersecurity design standards for transport-category airplanes, formalizing requirements that directly touch connected aircraft systems.

MARKET OPPORTUNITIES

Growth Opportunities Through Open Architectures And Multi-Orbit Flexibility Unlock Step-Change Adoption

A major upside lies in open in-flight connectivity frameworks that decouple aircraft from any single network. By allowing airlines to line-fit or retrofit kits that can communicate with multiple constellations (GEO/LEO) and switch providers over time, airframers reduce lock-in, sharpen competition on price/quality, and de-risk technology bets. That flexibility maps well to diverse route mixes: LEO excels on latency-sensitive; short-haul turns; GEO provides efficient capacity on trunk routes; and hybrid keeps the cabin online during polar or equatorial handoffs. For airlines, the commercial lever is equally attractive, procure bandwidth including a utility, then differentiate through tiering (free, freemium, and premium) and content partnerships. Cabin planners also achieve weight and drag savings through standardized mounts and power/data interfaces, resulting in reduced fuel burn and shop time.

- October 2024: Airbus reported further rollout progress of HBCplus, its flexible, supplier-furnished, multi-orbit line-fit/retrofit connectivity platform for A-Family programs.

IN FLIGHT INTERNET MARKET TRENDS

Electronically Steered Antennas and GEO+LEO Always Best Path To Act As A Major Technological Trend

The technology frontier is the pairing of electronically steered antennas (ESAs) with software-defined modems that select the optimal beam and orbit in real-time. ESAs eliminate moving parts, reduce drag, and simplify maintenance. Paired with multi-orbit network managers, they can stitch GEO capacity with LEO latency, providing passengers with streaming-grade performance even on congested city pairs and tight turns. Open modem APIs and virtualized network functions further shrink boxes, while high-speed security patching enhances security. Gate-to-gate certification expands usable minutes per flight. As more airframers offer line-fit options, airlines can avoid bespoke STCs and scale across their fleets. The direction of travel is clear: lighter terminals, smarter scheduling, and orbit-agnostic bandwidth procurement that lowers total cost per bit.

- May 2023: Intelsat and Airbus detailed a Ku-band ESA that can connect to GEO and LEO, such as OneWeb, with airline selections available on Airbus' line-fit beginning in H1 2026.

MARKET CHALLENGES

Supply Chains, STC Capacity, And OEM Backlogs Stretch Rollout Timelines Present Threats To Market Growth

Execution risk is concentrated in industrial plumbing, where long-dated OEM backlogs limit near-term line-fit slots, engine and component shortages constrain MRO capacity, and certification engineers are a bottleneck for concurrent antenna and radome STCs across multiple aircraft types. Even when hardware is available, hangar time often competes with heavy checks and lease transitions, forcing operators to sequence installations over several seasons. Financing adds another layer, retrofit waves must align with lease maturities and cabin refreshes to avoid write-offs, while bandwidth contracts need hedges against traffic swings. The result is a rollout cadence shaped more by shop capacity and paperwork than by appetite, particularly for regional jets and secondary hubs.

- January 2025: Airbus reported 766 deliveries in 2024 and an end-of-year backlog of 8,658 aircraft, underscoring sustained demand and the long-dated nature of line-fit opportunities and slot availability.

Download Free sample to learn more about this report.

In Flight Internet Market Segmentation Analysis

By Component

Service Segment Dominated For Recurring Spend And Free Wi-Fi Strategies

On the basis of component, the market is classified into service and equipment.

Service will be the dominating segment in the market with sahre of 23.17% in 2026. Service is the largest share of IFC as airlines commit to multi-year bandwidth, portal, monitoring, and SLA contracts across big narrow-body fleets. As carriers move to offer free or loyalty-gated access, session volumes rise, driving the need for higher capacity and quality tiers. Operations increasingly depend on connectivity (EFB updates, maintenance data, and crew apps), keeping spend recurring and sticky. Hardware is approaching saturation on many fleets, so incremental revenue now tends to skew toward usage, speed upgrades, and sponsorships.

- January 2023: Delta began rolling out fast, free onboard Wi-Fi services for SkyMiles members across mainline flights, signaling service-led spending growth.

By Connectivity Type

Satellite Connectivity Segment Dominated For Universal Coverage And Performance

In terms of connectivity type, the market is categorized into satellite and Air-to-Ground (ATG).

The satellite segment will dominating the market sahre with 23.59% in 2026. Satellite leads as it works on all geographies and stage lengths; ATG is limited to specific airspace. GEO brings efficient capacity on long-haul and trunk routes; LEO adds low latency for short-haul and polar corridors. Lighter radomes, ESAs, and open modems reduce drag and installation time, improving economics even on domestic fleets. Airlines are line-fitting satellite kits and retrofitting older aircraft to standardize and enhance passenger experience and operational applications.

- May 2022: Southwest chose Viasat Ka-band IFC, factory-installed on new deliveries, underscoring satellite as the default for capacity, coverage, and reliability.

By Aircraft Type

Narrow-body Aircraft Segment Dominated For Utilization And Seat Share

Based on the aircraft type, the market is segmented into narrow-body, wide-body, and regional jet.

Narrow-body aircraft operate the majority of global departures and seats, resulting in the highest number of monetizable sessions per aircraft. Airlines prioritize uniform Wi-Fi on single-aisle fleets to defend share on competitive short-haul routes and to support quick-turn digital workflows. Sustained OEM backlogs keep line-fit pipelines active, while retrofits standardize older sub fleets. As utilization remains high, carriers introduce higher-throughput plans and free tiers on narrow-body aircraft first, then extend them to wide-body aircraft for long-haul consistency.

- January 2025: Airbus reported 766 deliveries in 2024 and backlog 8,658 aircraft, confirming sustained narrowbody scale driving connectivity investment globally.

To know how our report can help streamline your business, Speak to Analyst

By Installation

Retrofit Installation Segment Dominated For Near-Term Volume and Speed

Based on installation, the market is segmented into retrofit and line fit.

The retrofit segment will hold a dominanting position in 2026, accounting for 18.61%, in flight internet market share. Retrofit is larger than line-fit as many in-service model aircraft still need modern multi-orbit terminals. Airlines align installs with heavy checks to minimize downtime; ESAs simplify certification and reduce drag. Standardized STCs across 737/A320 families enable replication at scale, and commercial models increasingly bundle hardware with service to smooth capex. Retrofit allows carriers to transition to free Wi-Fi strategies without waiting for new deliveries.

- September 2024: Hawaiian Airlines announced that Starlink Wi-Fi would be free across all Airbus-operated flights, illustrating how retrofit-led upgrades are accelerating passenger experience improvements fleetwide.

In Flight Internet Market Regional Analysis

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America In Flight Internet Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America contributed 32.08% to the global market in 2025, with a valuation of USD 1.59 Billion, and is projected to reach USD 1.83 Billion in 2026. The U.S. and Canada lead in revenue intensity, characterized by dense domestic networks, high passenger expectations, and early adoption of free or sponsored access. Standardized kits across the 737/A320 families accelerate rollouts; multi-orbit options enhance reliability and throughput on busy city pairs. Loyalty integration and ad/sponsorship models raise take-rates at low marginal cost, keeping monetization strong. The U.S. market is projected to reach USD 1.55 billion by 2026.

- May 2023: Air Canada and Bell launched free inflight messaging for Aeroplan members on Wi-Fi-equipped aircraft, boosting adoption across Canada.

Europe

Europe accounted for USD 1.38 Billion in 2025, representing 27.88% of the global market share, and is projected to reach USD 1.58 Billion in 2026. European carriers favor simple tiers, free messaging with paid higher-speed access, while preparing for ESA-enabled multi-orbit upgrades. Reliability, cybersecurity, and consistent portals across mixed fleets are priorities, with line-fit options expanding on new deliveries. The U.K. has been a notable leader in loyalty-linked messaging, which boosts engagement without significant price barriers. The UK market is projected to reach USD 0.37 billion by 2026, while the Germany market is projected to reach USD 0.3 billion by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 1.26 Billion in 2025, capturing 25.40% of global revenue, and is estimated to reach USD 1.46 Billion in 2026. The Asia Pacific region is experiencing rapid growth and is expected to grow at the highest CAGR by 2034 in in-flight Internet. Asia Pacific contributes the largest share in terms of traffic, combining China’s scale, India’s growth, and Japan's and Australia's quality emphasis. Short-haul density raises session volumes, while long-haul Asia–U.S./Europe services benefit from GEO+LEO combinations for reliability. Policy clarity and maturing hardware are accelerating installs and standardizing access across major fleets. The Japan market is projected to reach USD 0.32 billion by 2026, while the China market is projected to reach USD 0.58 billion by 2026, and the India market is projected to reach USD 0.28 billion by 2026.

Rest of the World

The rest of the world region is expected to witness moderate in flight internet market growth. The Rest of the World region captured 14.64% of the global market in 2025, generating USD 0.73 Billion in revenue, and is projected to reach USD 0.82 Billion in 2026. Middle East carriers set high standards on widebody-heavy fleets, often pairing premium cabins with wider complimentary access. Latin America is accelerating through retrofit programs and selective line-fit on new deliveries to improve reliability on long-haul and competitive regional routes. Strengthening SLAs and equipment commonality are compressing rollout timelines.

COMPETITIVE LANDSCAPE

Key Industry Players

Wide Range of Product Offerings, coupled with a Strong Distribution Network of Key Companies, supported their Leading Position

The in flight internet market consists of two main groups. First are full-stack integrators, including Viasat (formerly Inmarsat), Intelsat, Panasonic Avionics, Thales, and Anuvu. They combine satellite capacity, antennas and modems, software, certification, and global support under multi-year service agreements. Second are direct-to-airline LEO providers, notably SpaceX Starlink and Eutelsat OneWeb (often via partners). They compete on low latency, simpler pricing, and fast retrofits, which is pushing airlines toward multi-orbit service options.

Competition centers on five practical levers. Capacity control (owning or long-term securing Ka/Ku bandwidth) supports price and performance. Offerability (line-fit at Airbus/Boeing and breadth of STCs across A320/737 families) determines rollout speed. Terminal technology, especially electronically steered antennas with low drag, enables GEO+LEO agility and reduces maintenance. Service quality, peak-time throughput, gate-to-gate availability, cybersecurity, and SLAs, drives renewals. Commercial models are shifting to free or loyalty-gated access funded by sponsors, with optional premium tiers for streaming.

Switching costs remain significant due to hardware and certifications, but they are decreasing as open modems, standardized radomes, and multi-orbit managers become more widespread. Airframers’ open connectivity programs make provider changes easier over an aircraft’s life. Expect more partnerships between capacity owners and integrators, selective consolidation, and RFPs that mandate performance-based SLAs, open interfaces, and clear multi-orbit roadmaps as baseline requirements.

LIST OF KEY IN FLIGHT INTERNET COMPANIES PROFILED

- Viasat (U.S.)

- Intelsat (U.S.)

- Panasonic Avionics (U.S.)

- Thales Group (France)

- Eutelsat OneWeb (U.K.)

- SpaceX Starlink (U.S.)

- Anuvu (U.S.)

- Hughes Network Systems (U.S.)

- Gilat Satellite Networks (Israel)

- SITA FOR AIRCRAFT (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- Oct 2025 – Viasat introduced an iQe service-quality metric at NBAA to move airline evaluations beyond peak-speed marketing, aligning SLAs to real passenger experience and peak-time performance; may influence RFP scoring.

- September 2025 – United secured FAA approval for its first Starlink-equipped mainline Boeing 737-800, with initial service scheduled for mid-October, expanding beyond regional jets and signaling momentum for fleetwide LEO adoption.

- April 2025 – Intelsat and Embraer announced the factory installation of a multi-orbit ESA IFC solution (Skymark launch), designed to deliver streaming-grade gate-to-gate connectivity and reduce retrofit downtime, supporting OEM-level scale-up.

- April 2025 – Viasat launched “Amara”, a next-generation IFC platform that combines network, hardware, and digital tools to improve capacity utilization and measured quality, expected to support airline migrations to higher-tier, free, or freemium offers.

- Mar 2025 – United Airlines received FAA approval for its first Starlink-equipped aircraft. They began installing (≈40 regional jets/month) to enable free Wi-Fi for MileagePlus members, accelerating U.S. service-led IFC spend.

- September 2024 – Hawaiian Airlines partnered with SpaceX Starlink to offer free high-speed Wi-Fi across its Airbus fleet, aiming to improve NPS and achieve competitive long-haul parity; the rollout continues across the broader fleet.

- Apr 2024 – British Airways launched free inflight messaging for Executive Club members to lift adoption and loyalty; rollout targets full-fleet Wi-Fi coverage by the end of 2025 and should raise take-rates on European short-haul.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.30% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Connectivity Type, Aircraft Type, Installation, and Region |

|

By Component |

|

|

By Connectivity Type |

|

|

By Aircraft Type |

|

|

By Installation |

|

|

By Region |

North America (By Component, Connectivity Type, Aircraft Type, Installation, and Country)

Europe (By Component, Connectivity Type, Aircraft Type, Installation, and Country)

Asia Pacific (By Component, Connectivity Type, Aircraft Type, Installation, and Country)

Middle East & Africa (By Component, Connectivity Type, Aircraft Type, Installation, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.96 billion in 2025 and is projected to reach USD 9.29 billion by 2034.

In 2025, the market value stood at USD 1.59 billion.

The market is expected to exhibit a CAGR of 6.30% during the forecast period.

The narrow-body aircraft segment led the market in terms of aircraft type.

High-quality wi-fi becoming a brand standard, leading to high growth of in-flight internet.

Viasat (U.S.), Intelsat (U.S.), and Panasonic Avionics (U.S.) are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us