Individual Health Insurance Market Size, Share & Industry Analysis, By Type (Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), Exclusive Provider Organization (EPO), and Others), By Payor (Private and Public), By Mode (Offline and Online), By Distribution Channel (Direct Sales, Agents, Brokers, Banks, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

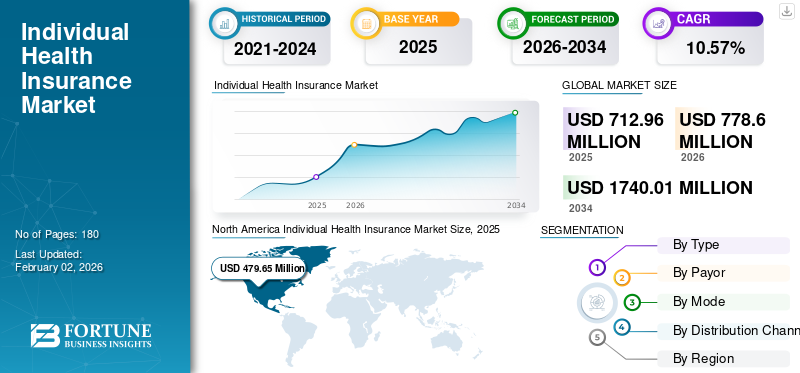

The global individual health insurance market size was valued at USD 712.96 million in 2025 and is projected to grow from USD 778.6 million in 2026 to USD 1,740.01 million by 2034, exhibiting a CAGR of 10.57% during the forecast period. North America dominated the individual health insurance market with a market share of 33.11% in 2025.

Individual health insurance refers to a personal health insurance plan offering medical coverage tailored to one’s needs. The market is influenced by the rising occurrence of prevalence of various chronic conditions, increasing per capita health expenditure, increasing number of traumatic injuries and surgeries among patients, rising awareness about the availability of various individual insurance plans, among others.

- According to 2024 statistics published by the Centers for Medicare & Medicaid Services (CMS), it was reported that the healthcare expenditure is around USD 14,570.0 per person in the U.S.

Several major insurance providers such as UnitedHealth Group, Cigna Healthcare, and others, are focusing on introducing new insurance plans covering a wide array of health insurance applications, further anticipated to maintain their market share.

Download Free sample to learn more about this report.

Individual Health Insurance MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 712.96 million

- 2026 Market Size: USD 778.6 million

- 2034 Forecast Market Size: USD 1,740.01 million

- CAGR: 10.57% from 2026–2034

- North America dominated the individual health insurance market with a 33.11% share in 2025.

- Health Maintenance Organization (HMO) segment led the market in 2024 due to lower premiums and wider coverage benefits.

- Private insurance segment held the dominant share in 2024, driven by higher flexibility and faster service delivery.

North American

North America generated USD 524.28 million in 2026, supported by high healthcare spending and strong insurer penetration.

Europe

Europe reached USD 138.72 million in 2026, driven by rising chronic disease prevalence and strong government awareness initiatives.

Asia Pacific

Asia Pacific reached USD 96.36 million in 2026, supported by a large elderly population and increasing healthcare costs.

U.S.

High insurance penetration supported by chronic disease burden and advanced coverage offerings.

Japan

Strong demand driven by aging population and increased focus on comprehensive health coverage.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Frequency of Prolonged Diseases to Augment Product Demand Among Individuals

The increasing prevalence of chronic disorders, such as cancer, cardiovascular diseases, neurological diseases, and other diseases are resulting in an increased number of consultations and procedures, including surgical procedures. The growing aging population is one of the vital factor aiding in increasing patient population suffering from these disorders. Thus, the increasing geriatric population and healthcare costs are prominently driving the demand for health insurance plans among individuals.

- According to statistics from the Centers for Disease Control and Prevention (CDC), about 36.7 million new cancer cases were reported in the U.S. from 2022 to 2023.

Escalating demand for health insurance plans, coupled with the growing focus of key players toward offering innovative insurance plans, is likely to support the growing adoption rate for these plans, thereby contributing to the global individual health insurance market growth.

MARKET RESTRAINTS

Increasing Insurance Premiums to Hinder the Market Development

There is a growing requirement for these insurance plans among the general population. However, one of the major issues limiting the implementation of these plans is the high premiums associated with these insurance plans. The direct cost associated with health insurance premiums is overpriced due to rising healthcare costs, increasing claims, and others. Increasing insurance premiums by the key providers is limiting the adoption rate for these products, further expected to hinder market augmentation considerably, specifically in emerging countries such as Brazil, Mexico, and others.

- For example, according to the 2020 data published by The Commonwealth Fund, only 23% of people had private medical/hospital insurance in Brazil.

Therefore, high premiums associated with these insurance policies, coupled with limited awareness about these policies are expected to hamper the adoption rate among the population globally.

MARKET OPPORTUNITIES

Focus on Initiatives and Customer-centric Insurance Models Drives Market Opportunity

The growing demand for customized insurance products among the general population is leading to robust efforts by the health insurance companies to shift to a more customer-centric strategy and develop insurance models and products that cater to individual requirements and preferences.

The companies are striving to introduce applications and various products that cater to the increasing need for personalized products among the general population with different sets of conditions, illnesses, and age groups.

- For instance, in June 2025, Bajaj Allianz General Insurance launched a first-of-its-kind “state-wise health insurance policy” offering health cover tailored to the specific medical needs, treatment costs, and others.

Along with tailored health insurance products, the increasing focus of insurance companies on customer-centric business models and adopting such models is creating a favorable impact by facilitating customer engagement, maximizing customer ownership, and thus leading to higher customer retention rates.

The growing technological advancements allowing digital transformation in the insurance sector and strategic collaborations among various insurtech companies and others hold untapped potential for the business by reducing customer acquisition costs and earning higher revenue per customer, thereby expected to contribute to global individual health insurance market size.

MARKET CHALLENGES

Increasing Concerns Regarding Cyberattacks and Data Privacy to Limit Adoption

The increasing use of big data technology in the health insurance industry has numerous advantages, such as reduced operating costs, improved industry profitability, and others. However, the technology holds challenges, including data leaks of personal information such as biometric, medical, and health information of the insured individual.

The data leak of such sensitive information poses a threat of using the data illegally, resulting in the infringement of human dignity. Therefore, the increasing use of big data in the insurance industry challenges the protection of the privacy data of individuals, which is anticipated to limit the adoption of these insurance products among the general population globally.

Additionally, the lack of laws and regulations specifically for anti-insurance fraud is one of the major reasons for the data privacy concerns and cyberattacks.

- For instance, according to a 2023 article published by the China Daily, there were around 1,213 cases related to health insurance fraud between 2021 and 2023.

Other Important Challenges

- Uncertain Regulations May Limit Product Adoption: Frequent changes in healthcare policies and insurance regulations create instability for insurers and policyholders.

- Limited Consumer Awareness to Hamper Product Demand: Limited understanding of insurance benefits, particularly in emerging regions, is expected to limit the market penetration.

Individual Health Insurance Market Trends

Increasing Integration of Artificial Intelligence & Automation for Faster Claims

There has been a changing inclination toward integrating artificial intelligence and machine learning in insurance products by the market players globally. The development and integration of artificial intelligence and machine learning are anticipated to overcome several challenges and enable better fraud detection, risk assessment, and personalized offerings.

Moreover, artificial intelligence-driven automation further streamlines claims processing, reducing errors, and helps in accelerating approvals and reducing administrative costs. The key players are utilizing digital transformation to adapt modern trends and enhance the operations and overall service provided to the customers by introducing innovative insurance products in the market.

- For instance, in April 2025, Future Generali India Life Insurance Company Ltd., launched an artificial intelligence platform that aims to simplify assessing appropriate cover for an individual’s health insurance requirements.

The benefits accompanying innovative insurance products have increased the adoption rate for these products globally.

Other Prominent Trends

- Preferential Shift to Value-Based Care Among the Insurers: Insurers are designing plans emphasizing cost-effectiveness and better patient outcomes, supporting value-based care models.

- Increasing Focus on Provision of Subsidies Among Governmental Organizations: Enhanced subsidies, particularly in the U.S. under the Affordable Care Act, have boosted individual plan enrollments.

Download Free sample to learn more about this report.

Trade Protection

The insurers in the U.S. have indicated that the increasing cost of medical devices and pharmaceuticals could result in higher insurance premiums for individuals starting in 2026, influencing cost structures and product pricing in the market.

Segmentation Analysis

By Type

Increasing Implementation of Health Maintenance Organization (HMO) Policies Drives Segmental Growth

Based on type, the market is categorized into health maintenance organization (HMO), preferred provider organization (PPO), exclusive provider organization (EPO), and others.

The health maintenance organization (HMO) led the individual health insurance market share in 2024. The growing benefits of health maintenance organization policies, such as comparatively lower premiums, flexibility, and more coverage, among others, are resulting in the increasing demand for these policies among the general population.

- For instance, in December 2024, Leadway Health HMO launched Leadway Health HMO International Health Plan with a coverage limit of upto USD 2.0 million, ensuring policyholders receive premium medical care in healthcare facilities globally.

The preferred provider organizations (PPO) is projected to expand with a significant CAGR during the projected year. The growth is attributed to rising need, furthermore driving the attention of prominent insurance providers toward introducing novel health insurance products for individuals in the market.

By Payor

Increasing Focus of Customized Plans Among Private Insurers to Boost Segmental Growth

Based on payor, the market is bifurcated into private and public.

The private segment held the dominant market share in 2024. The growth is due to the growing benefits of private insurance, such as faster service, flexibility, extensive coverage, and others, resulting in a growing adoption rate and demand for private health insurance among individuals.

- For instance, according to data published by the U.S. Census Bureau, approximately 65.4% of people were covered under private health insurance in the U.S. in 2023.

The public segment is estimated to rise with a sizeable CAGR during the forecast period. The growing health care costs, along with the introduction of innovative health insurance policies for individuals among governmental organizations, anticipated to maintain the increasing adoption of these insurance products in the market.

By Mode

Increasing Number of Agents & Brokers to Boost Offline Segment’s Growth

Based on mode, the market is bifurcated into offline and online.

The offline segment dominated the market in 2024. This is due to distinct factors, including personalized guidance, reduced risk of cyber fraud, and the growing adoption rate and demand for these individual insurance plans among the general population globally. This, along with increasing licensed insurance agencies and brokers, is also likely to support the growth of the segment in the market.

- For example, according to 2024 data published by AgentMethods, there are 927,600 licensed agencies and brokers working in the U.S.

On the other hand, the online segment is also expected to grow with a considerable CAGR during the forecast period. The increasing benefits of online health insurance plans, such as convenience, flexibility, increased transparency, easy documentation, and others resulting in the increasing consumer choice toward these insurance plans.

By Distribution Channel

Rising Population of Agents to Boost Segment Growth

Based on distribution channel, the market is categorized into direct sales, agents, brokers, banks, and others.

The agents segment dominated the market in 2024. The growth is due to the increasing number of health insurance agents, resulting in the rising adoption rate for individual health insurance policies among the population, further likely to contribute to the growth of the segment.

- For instance, according to 2024 data published by AgentMethods, there are 902,500 life and health insurance agents working in the U.S.

On the other hand, the direct sales segment is expected to grow with a considerable CAGR during the forecast period. The growth is owing to increasing focus toward raising awareness for these insurance products through the company websites and portals.

Individual Health Insurance Market Regional Outlook

By region, the market spans across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Individual Health Insurance Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America represented USD 479.65 million, accounting for 33.11% of the worldwide market, and is projected to grow to USD 524.28 million in 2026. The increasing per capita healthcare expenditure, adequate reimbursement policies, developed healthcare infrastructure, increasing focus toward strategic initiatives among governmental organizations, and the growing number of insurers introducing novel policies contributing to the growing adoption rate of health insurance policies in the region.

- According to 2024 data published by the U.S. Census Bureau, about 92% people had health insurance in the U.S.

U.S.

The increasing prevalence of various chronic conditions, including cancer and cardiovascular disorders, and the introduction of innovative insurance policies with improved health insurance coverage are some of the vital factors supporting the growing demand for these policies in the market.

Europe

The Europe market generated USD 127.57 million in 2025, representing 27.17% of the global market landscape, and is expected to reach USD 138.72 million in 2026. The growth is due to the increasing prevalence of chronic disorders, resulting in the rising demand for novel insurance policies among the general population. Increasing demand and growing strategic initiatives among governmental organizations to raise awareness about the benefits of health insurance plans are further anticipated to support the adoption of these products in the market.

- For instance, according to 2025 statistics published by the British Heart Foundation, it was reported that about 6.4 million people are suffering from circulatory heart disease in the U.K.

Asia Pacific

Asia Pacific contributed 26.52% to the global market in 2025, with a valuation of USD 87.87 million, and is projected to reach USD 96.36 million in 2026. The growing elderly population, huge patient pool, increasing healthcare costs, emerging healthcare organization, and growing adoption of digital platforms are crucial factors expected to boost the demand for innovative policies in the market. Additionally, an increasing number of prominent players focusing on mergers and acquisitions among other players to strengthen their brand presence is expected to support the market growth.

- For instance, according to 2023 China’s government data, approximately 297 million people in China are aged 60 and above.

Latin America

The market in Latin America reached USD 11.49 million in 2025, representing 25.06% of total market revenue, and is projected to reach USD 12.41 million in 2026. Increasing healthcare spending, growing awareness about the advantages of health insurance policies, and growing focus of key players toward the provision of innovative insurance policies are some of the crucial factors contributing to the market growth. This, coupled with the growing number of agents and brokers in the region focusing on an increasing number of insurance claims, is further likely to support the market growth.

- For example, according to 2023 data announced by the National Center for Biotechnology Information (NCBI), healthcare expense in Brazil increased from 8.3% of GDP in 2010 to 9.2% in 2018.

Middle East & Africa

The Middle East & Africa market was valued at USD 6.38 million in 2025, capturing 24.57% of global revenue, and is estimated to reach USD 6.82 million in 2026. The growth of this region is due to the growing number of insurtech companies focusing on integrating technology to provide novel policies in the market. Furthermore, a growing number of strategic initiatives among governmental organizations to expand the universal coverage in Middle East countries is further likely to aid the growth of the market.

- For instance, in August 2024, the South African Government passed the National Health Bill to expand the universal coverage for health insurance among the general population in the country.

COMPETITIVE LANDSCAPE

Key Industry Players

Initiation of New Insurance Policies Among Major Companies Fuels the Market Position

The global market is fragmented, with many insurance providers accounting for a significant portion of the individual health insurance market share.

UnitedHealth Group, China Post Life Insurance Co., Ltd., are some of the major companies operating in the industry. The growth is due to distinct factors, including a strong focus on the introduction of new insurance products, acquisitions, and partnerships among the other players, and other factors in the market.

- In March 2023, China Post Life Insurance Co., Ltd. launched the “Health Insurance + Service” to improve the products and services for health insurance, particularly for individual policy plans.

Elevance Health, among other players, is also growing in the market due to the company’s increased focus on business expansion in developing countries, including China, Brazil, and others. The growing focus on providing innovative insurance policies is further expected to support their increasing share in the market.

List of Key Individual Health Insurance Companies Profiled

- China Post Life Insurance Co., Ltd. (China)

- UnitedHealth Group (U.S.)

- AIA Group Ltd. (Hong Kong)

- Bupa Global (U.K.)

- Elevance Health (U.S.)

- AXA (France)

- Cigna Healthcare (U.S.)

- CVS Health (U.S.)

- Allianz (Germany)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Curative Health Insurance Company launched Curative Telehealth with an aim to provide fast, seamless healthcare services to its members globally. This helped the company to increase its brand presence.

- February 2025: AXA launched AXA Health Max Elite, a critical insurance plan covering over 150 medical conditions, including mental health disorders, and others. This helped the company in strengthening its global presence.

- May 2024: AXA partnered with Daman, a UAE health insurer, to launch a new international private medical insurance plan with an aim to strengthen its product portfolio.

- April 2024: Pivot Health partnered with Pan-American Life Insurance Company (PALIC) with an aim to market short-term medical (STM) insurance policies in more than 25 U.S. states. This helped the company in strengthening its geographical presence.

- November 2021: Enhance Health, LLC, partnered with Bain Capital Insurance to develop a Medicare insurance distribution and care navigation platform. This helped the company to strengthen its presence.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.57% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Type

|

|

By Payor

|

|

|

By Mode

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 712.96 million in 2025 and is projected to record a valuation of USD 1,740.01 million by 2034.

In 2025, the market value stood at USD 712.96 million.

The market is expected to exhibit a CAGR of 10.57% during the forecast period of 2026-2034.

The health maintenance organization (HMO) segment led the market by type.

The key factors driving the market are the increasing prevalence of chronic disorders, growing per capita healthcare expenditure, and the growing number of product launches.

UnitedHealth Group, Elevance Health, and China Post Life Insurance Co., Ltd., are the top players in the market.

North America dominated the market in 2025 by holding the largest share.

Increased awareness of innovative individual health insurance policies, the launch of novel insurance products, and an increase in the demand for these products in developing nations favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us