Industrial Brown Sugar Market Size, Share & Industry Analysis, By Type (Light Brown Sugar and Dark Brown Sugar), By Nature (Organic and Conventional), By Application (Beverages, Confectionery, Bakery, Dairy Products, and Other Food Applications), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

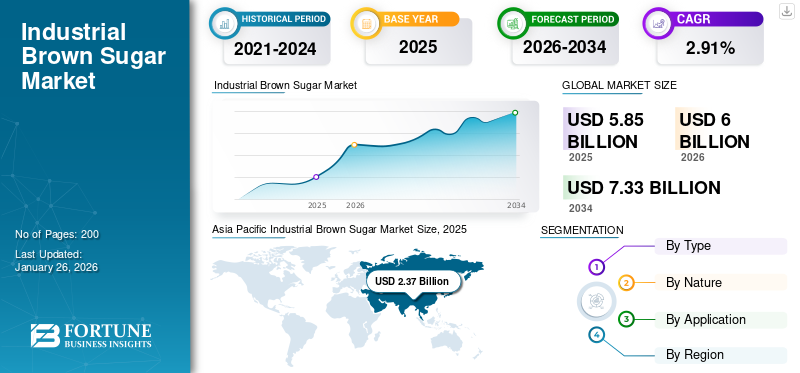

The global industrial brown sugar market size was valued at USD 5.85 billion in 2025. The market is projected to grow from USD 6.00 billion in 2026 to USD 7.33 billion by 2034, exhibiting a CAGR of 2.91% during the forecast period. Asia Pacific dominated the industrial brown sugar market with a market share of 40.52% in 2025.

Industrial brown sugar is mainly produced and marketed for large-scale industrial applications such as food and confectionery manufacturers, catering, the baking industry, pharmaceutical, and beverage industries. The global industrial brown sugar market will continue to expand in the coming years, with the major drivers being changing tastes and preferences and the growing food and beverage sector.

Some prominent players operating in the global market are Tate & Lyle Plc, Cargill Inc., Agrana Group, ASR Group, and Louis Dreyfus Company.

Download Free sample to learn more about this report.

Global Industrial Brown Sugar Market Overview

Market Size & Forecast:

- 2025 Market Size: USD 5.85 billion

- 2026 Market Size: USD 6.00 billion

- 2034 Forecast Market Size: USD 7.33 billion

- CAGR: 2.91% from 2026–2034

Market Share:

- Asia Pacific dominated the industrial brown sugar market with a 40.52% share in 2025, driven by its vast population, strong domestic confectionery demand, and favorable climate for sugarcane cultivation in countries like China, India, and Indonesia.

- By type, the light brown sugar segment held the largest market share in 2024, attributed to its mild flavor and extensive use in baked goods and sauces.

- By nature, the conventional segment dominated in 2024 due to its cost-effectiveness and higher yields, while the organic segment is expected to grow significantly.

- By application, the bakery segment led the market in 2024, owing to high demand for brown sugar in baked products for its flavor and moisture-retaining properties.

Key Country Highlights:

- China: A key player in sugarcane production and consumption, driving domestic demand for brown sugar across food and beverage applications.

- United States: Rising health awareness and preference for minimally processed sweeteners are driving brown sugar consumption in the bakery and confectionery sectors.

- Germany: Retail baked goods sales rose from USD 18.77 billion in 2022 to USD 19.41 billion in 2023, supporting brown sugar demand in the bakery industry.

- Brazil: One of the largest global producers of brown sugar, driven by favorable climatic conditions and exports led by companies like Raizen and Copersucar.

- Saudi Arabia & UAE: Increasing demand for processed foods and natural sweeteners is driving industrial brown sugar usage, especially in bakery and confectionery applications.

INDUSTRIAL BROWN SUGAR MARKET TRENDS

Emerging Health and Wellness Trends to Pave Growth Prospects

Consumers have become more health conscious due to the detrimental effects of excessive sugar consumption. Therefore, they seek better alternatives, such as sugar substitutes or low-calorie sweeteners. This shift is thus driving innovation in brown sugar products, including sustainably sourced and organic options, creating a positive outlook for the brown sugar market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Growing Consumption of Ready-to-Eat Foods to Propel Market Growth

Rising consumption of Ready-to-Eat (RTE) foods is among the major growth drivers for the global industrial brown sugar market share. Brown sugar is used in different RTE products, including baked products, confectionery, and beverages, as a sweetener and flavor enhancer. The increasing demand for convenience foods as well as ready-to-drink beverages is driving the use of brown sugar as a basic ingredient for these foods and beverages. The busy and hectic lifestyles of modern consumers are driving the higher demand for RTE foods, which are simple and quick to prepare. Brown sugar is a simple ingredient for these foods, offering taste and texture without further processing.

MARKET RESTRAINTS

Growing Competition from Alternative Sweeteners to Hamper Market Growth

The global industrial brown sugar industry has been facing intense competition from a wide range of artificial and natural sweeteners such as agave syrup, coconut sugar, stevia, monk fruit, and others. These substitutes often offer fewer calories, distinctive flavor profiles, or a lower glycemic index. These factors lead consumers increasingly to exploring such alternatives that focus on health consciousness, especially in diet-specific or functional products, further hampering the global industrial brown sugar market growth.

MARKET OPPORTUNITIES

Extensive Applications in Nutraceuticals/Functional Foods to Pave Growth Prospects

Brown sugar is commonly sought as a healthier alternative to white refined sugar since it retains some molasses, which is rich in antioxidants and minerals. Consumers are increasingly seeking natural sweeteners, and brown sugar is included in this trend, especially in comparison to artificial sweeteners. This perception further assists in driving its growing application in functional foods and nutraceuticals, where health benefits are a key selling point. Due to the rising applications for industrial brown sugar and its source of protein, it can be used in developing food and drink products such as cereals, protein bars, yogurt, and probiotic drinks. Moreover, functional properties and health properties linked with brown sugar are driving its use in the market for functional foods, thus opening up significant scope for development and innovation for food manufacturers.

Segmentation Analysis

By Type

Light Brown Segment Dominates Due to Low Molasses Content and Mild Flavor

Based on type, the global market is bifurcated into light brown sugar and dark brown sugar.

The light brown sugar segment held the dominant share in 2024. It is known to have a lower molasses content, giving it a mild taste and mainly used in the manufacturing of cakes, cookies, and sauces to offer light caramel sweetness to the baked goods.

The dark brown sugar segment is expected to grow with the highest CAGR in the forecast period. It is often preferred over light brown sugar as it possesses a stronger flavor and a darker color due to the presence of high molasses content. Products such as barbecue sauces, gingerbread, and others require a stronger molasses flavor, further fueling the demand for dark brown sugar.

By Nature

Conventional Segment Dominates Owing to Cost-Effectiveness and Ease of Production

Based on nature, the market is split into organic and conventional.

The conventional segment dominates the global market, owing to its cost-effectiveness, ease of production, and high yields. Conventional farming of sugarcane is generally more cost-effective than organic farming. Thus, offering high yields and more revenue per unit of land, which further gives a great advantage to conventional brown sugar manufacturers.

The organic segment is expected to grow significantly in the forecast period. The surge in demand for organic food products, coupled with a shift toward sustainable alternatives and natural products, has played a pivotal role in the organic industrial brown sugar market's growth. These market trends are expected to continue in the future as manufacturers turn to organic ingredients in order to meet the growing demand.

By Application

Bakery Segment Dominates the Market Owing to High Demand and Popularity

Based on application, the market is categorized into beverages, confectionery, bakery, dairy products, and other food applications.

The bakery segment held the dominant global brown sugar market share in 2024. The bakery industry prefers brown sugar over regular sugar owing to the presence of molasses and hygroscopic properties, which further anticipates the demand for brown sugar in the future. Moreover, bakery products are in extremely high demand owing to the economic dynamics of the food and beverage industry. According to the Agriculture and Agri-Food Canada report, the global retail sales of baked goods increased from USD 439.98 billion in 2022 to USD 473.99 billion in 2023. The rise in demand for indigenous bakery products in developing regions such as South America and the Asia Pacific further emerges as a prominent factor boosting the growth of the industrial brown sugar market.

The confectionery segment is expected to grow significantly in the forecast period. The industrial brown sugar is a significant ingredient used in the manufacturing of confectionery, owing to the presence of molasses content, which further contributes to a moist, chewy texture and caramel-like taste to the products. This feature makes it a preferred choice for confectionery products, propelling the segment's growth.

Industrial Brown Sugar Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Industrial Brown Sugar Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market was valued at USD 2.37 billion in 2025, capturing 40.52% of global revenue, and is estimated to reach USD 2.43 billion in 2026. Asia Pacific dominates the global market for industrial brown sugar, with most of the world's brown sugar being produced and consumed in Asia. The region's vast population, rapidly expanding domestic confectionery market, and strong cultural affinity for natural sweeteners are the reasons behind its dominance. Many major sugar-producing countries in the region, such as China, India, and Indonesia, have tropical climates suitable for sugarcane cultivation. Consumers increasingly sought out natural and unprocessed sweeteners, and brown sugar is considered as a healthier variant because it is minimally processed and contains some molasses. Growing disposable incomes in the region are fueling demand for premium consumer goods such as bakery products, thereby increasing demand for brown sugar.

North America

North America contributed 19.06% to the global market in 2025, with a valuation of USD 1.11 billion, and is projected to reach USD 1.15 billion in 2026. The rising demand for brown sugar in North America is prompted mainly by an inclination toward less processed and natural ingredients, a growing concern about health, and an increasing demand for bakery and other foods. North America, particularly the U.S., consumes significant amounts of brown sugar owing to the intense demand for bakery products in the region. The growing number of local food producers and distributors also drives the growth in brown sugar consumption. Increased concern regarding the health effects of sugar intake has led consumers to seek healthier sweeteners, with brown sugar being viewed as a more natural and less processed alternative to white sugar. The bakery and confectionery sectors are dependent to a great extent on brown sugar because of its distinct taste and hygroscopic nature, which contribute to the moistness and texture of baked foods.

Europe

Europe accounted for USD 1.27 billion in 2025, representing 21.73% of the global market share, and is projected to reach USD 1.3 billion in 2026. Europe is expected to grow significantly in the global market. The major driver for the growth of the market is the rising demand for bakery products in urban areas of the region. According to the Agriculture and Agri-Food Canada report, retail sales of baked goods in Germany increased from USD 18,765 million in 2022 to USD 19,405 million in 2023. The bakery sector is known to be a key consumer of industrial brown sugar, requiring granulated, powdered, or liquid forms of brown sugar. The region is also experiencing a growing trend toward healthier soft drinks, including those with added proteins, dairy, and prebiotics, which is creating new opportunities for industrial liquid brown sugar.

South America

The South African industrial brown sugar market is experiencing substantial growth, with predictions for continued expansion in the coming years. Brazil is a major consumer of brown sugar in Latin America. The country has advanced technological methods of sugar processing and ideal climatic conditions for growing sugarcane and, therefore, is one of the leading sugar producers of high quality brown sugar. According to the United States Department of Agriculture (USDA), in 2023/24, Brazil produced 705 million metric tons (MMT) of sugarcane. The increasing demand for healthier sugar alternatives and sustainable initiatives is further driving the brown sugar market growth in South America. Brazilian brown sugar is renowned for its quality and is being exported to most countries globally, with the market largely established in Africa. The largest exporters of brown sugar in Brazil are Raizen and Copersucar, and Cargill Inc.

Middle East & Africa

The market in Middle East & Africa reached USD 0.44 billion in 2025, representing 7.49% of total market revenue, and is projected to reach USD 0.45 billion in 2026. Industrial application of brown sugar in the Middle East & Africa is growing because of several reasons, such as the rising consumption of processed foods, a growing number of food processing industries, and the application of brown sugar in different industries, such as the bakery and confectionery industries. The Middle East & Africa are witnessing rising demand for brown sugar, and both the industries and consumers are seeking naturally less processed sweeteners as well as other ingredients. Importantly, Saudi Arabia, the United Arab Emirates (UAE), and South Africa are large consumers of brown sugar because of a combination of factors such as a large population, rising disposable incomes, and a fast-growing middle class that is open to international food trends. In addition, the rising trend of home baking and cooking is also boosting demand because the moisture-retaining quality and flavor of brown sugar are highly sought after in a wide variety of recipes.

Latin America

In 2025, the Latin America market stood at USD 0.65 billion, representing 11.20% of global demand, and is projected to grow to USD 0.67 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus on Improving Production Capacity to Strengthen Market Presence

The global industrial brown sugar market is highly fragmented, with the presence of several players. Prominent players in the market include Tate & Lyle Plc, Cargill Inc., Agrana Group, ASR Group, and Louis Dreyfus Company. The players in the market are focusing on increasing production capacities to meet the demand for brown sugar for several applications emerging from various sectors.

- For instance, in February 2024, Sucro Limited, an integrated sugar company in North America, constructed a new cane sugar refinery in the Greater Chicago Area. The new facility would provide significant value-added specialty sugar capabilities, which also include large grain crystals used in specialty foods and confectionery, a brown sugar line, organic sugar refining, and specialty liquid production capabilities.

LIST OF KEY INDUSTRIAL BROWN SUGAR COMPANIES PROFILED

- Tate & Lyle Plc (U.K.)

- American Sugar Refining, Inc. (U.S.)

- Cargill Inc. (U.S.)

- American Crystal Sugar Company (U.S.)

- Amalgamated Sugar Company (U.S.)

- Raizen S.A. (Brazil)

- Taikoo Sugar Limited (China)

- Südzucker AG (Germany)

- Louis Dreyfus Company (U.S.)

- Agrana Group (Austria)

KEY INDUSTRY DEVELOPMENTS

- February 2025: “Tafadis” sugar refinery owned by Madar Group planned to start production, with a production capacity of 2,000 tons per day, with 200 tons of brown sugar, 1,300 tons of white sugar and more than 300 tons of liquid sugar.

- January 2025: Muwariziki Sugar Millers Limited, a Kenya-based private firm, established a USD 11.52 million sugar factory in Rangwe Sub-County, Homa Bay County. The factory would focus on producing brown sugar, bagasse, molasses, and ethanol.

- June 2022: EID Parry, a sugar and nutraceutical producer, signed a commercial partnership with Nutrition Innovation, a food technology company, to introduce Nucane low GI sugar. The partnership would help Parry to give more consumers access to natural brown sugar solutions and expand its portfolio.

- March 2022: The Agricultural Human Resources Extension and Development Agency of Indonesia boosted the brown sugar production in the country in order to reduce dependence on granulated sugar.

- August 2020: Central Sugars Refinery Sdn Bhd (CSR) completed the construction of its new facility in Padang Terap, Kedah. The new facility would produce brown sugar products, such as Better Brown and Commercial Brown.

REPORT COVERAGE

The global industrial brown sugar market analysis provides market sizing & forecasting by all the segments. It includes details on the market dynamics and trends expected to drive the market in the forecast period. It offers information about key regions/countries, key industry developments, new product launches, and details on partnerships, mergers & acquisitions in key countries. The global brown sugar market report covers the industry analysis, a detailed competitive landscape on the market share, and profiles of major players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 2.91% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Nature

|

|

|

By Application

|

|

|

By Geography North America (By Type, Nature, Application, and Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.85 billion in 2025 and is projected to reach USD 7.33 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.37 billion.

The market is expected to exhibit a CAGR of 2.91% during the forecast period of 2026-2034.

The bakery segment led the market by application.

The growing consumption of ready-to-eat foods aiding market growth.

Tate & Lyle Plc, Cargill Inc., Agrana Group, ASR Group, Louis Dreyfus Company, and others, are some prominent players in the global market.

Asia Pacific dominated the market with a share of 40.52% in 2025.

Increasing demand for Western bakery products in developing economies is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us