Industrial Disconnect Switch Market Size, Share & Industry Analysis, By Type (Fused and Non-Fused), By Mount (Panel, Din Rail, and Others), By Voltage (Upto 150 V, 150-300 V, and Above 300 V), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

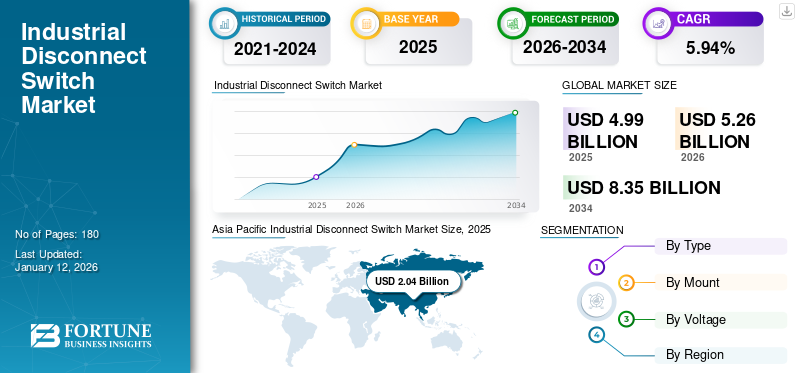

The global industrial disconnect switch market size was valued at USD 4.99 billion in 2025. The market is projected to grow from USD 5.26 billion in 2026 to USD 8.35 billion by 2034, exhibiting a CAGR of 5.94% during the forecast period. Asia Pacific dominated the industrial disconnect switch market with a share of 2.04% in 2025.

The industrial disconnect switch market is experiencing significant growth, driven by increasing industrialization, energy sector expansion, and safety regulations. The rise of manufacturing and industrial facilities globally is increasing the demand for reliable and safe electrical isolation solutions. Investments in power generation, transmission, and distribution infrastructure are driving the need for disconnect switches to ensure grid stability and safety. Additionally, stringent safety standards and compliance requirements for electric systems are fueling demand for high-quality industrial disconnect switches. The market refers to the global industry focused on the production, distribution, and application of disconnect switches that are designed for industrial developments.

- In March 2025, the Government of India announced an investment of USD 600 billion in the power generation sector with a strong focus on renewable energy and high-value manufacturing. Such high-scale government investments are expected to foster market growth over the forecast period.

General Electric (GE) is a prominent player in the market. GE's disconnect switch portfolio is extensive, offering solutions for various applications, including AC, DC, and railway applications. They offer a wide range of disconnect switches, including air and gas-insulated, manual, and motorized options.

Rapid growth in solar, wind, and EV charging infrastructure necessitates reliable disconnect switches to ensure electrical safety during maintenance and faults. As EV deployment accelerates, charging stations increasingly rely on high rated disconnect switches.

The industrial disconnect switch market share is growing due to a combination of technological, regulatory, and energy transition trends.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Modernization of Industrial Infrastructure to Drive Market Growth

The rising focus on industrial safety regulations and the growing demand for reliable power distribution electrical systems are major drivers for the industrial disconnect switch market. Additionally, rapid industrialization, increasing investments in manufacturing infrastructure, and the need for equipment protection during maintenance activities are further driving the market growth.

- In March 2025, TS Conductor announced plans to invest USD 134 million to develop high-capacity power lines for expansion of the power grid to meet rising demand from the domestic manufacturing sector and AI data centers.

Moreover, rising investments in smart factories and modernization of aging industrial infrastructure are further propelling the demand for advanced disconnect switch systems over the forecast period.

MARKET RESTRAINTS

High Installation Costs Restraint Market Growth

The market faces restraints due to high initial installation costs and ongoing maintenance expenses, especially for large-scale industrial setups. In addition, many small and medium enterprises (SMEs) prefer low-cost alternatives, hampering the penetration of premium solutions. The market also struggles with the slow pace of infrastructure development in some regions and limited awareness about modern disconnect technologies, which can hinder adoption rates of industrial disconnect switches and restrict overall market expansion in the near future.

MARKET OPPORTUNITIES

Increasing Demand for Smart Grid to Create Beneficial Market Opportunities in the Future

Significant opportunities are emerging with the rapid development of smart grid technologies, increased demand for automation, and a global shift toward renewable energy sources. The integration of IoT-enabled disconnect switches for real-time monitoring and remote control is gaining higher traction.

- In October 2024, Schneider Electric launched a smart grid solution Distributed Energy Resource Management System (DERMS) to enhance grid resiliency, net zero demands, and flexibility.

Furthermore, growing industrial investments in emerging markets such as Asia Pacific and Latin America provide a fertile ground for manufacturers to expand their footprint, offering customized, energy-efficient, and intelligent disconnect switch solutions that meet evolving industry standards, which is expected to generate new opportunities over the forecast period.

INDUSTRIAL DISCONNECT SWITCH MARKET TRENDS

Expansion in EV Charging and Renewable Infrastructure to Drive the Market

The rapid rollout of electric vehicle charging stations, especially Level 2 and DC fast chargers, requires reliable disconnect switches for: safe isolation of electrical circuits during maintenance or emergencies, compliance with safety codes such as NEC (National Electrical Code) that mandate disconnects near chargers. Growth in distributed energy sources also boosts the need for decentralized switchgear, including disconnect switches. These factors drive the industrial disconnect switch market growth.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Rising Power Transmission Safety Concerns to Boost Non-Fused Segment Growth

Based on type, the market is segmented into fused and non-fused.

Non-fused switches are expected to have the largest revenue share during the forecast period due to their enhanced safety and reliability, particularly in high-load environments. Non-fused switches are gaining traction due to their ease of use and versatility, being favored in diverse settings for their ability to isolate circuits without needing additional fuse protection. The aforementioned factors are expected to propel segment growth over the forecast period.

Fused switches offer both circuit isolation and over-current protection, making them essential in various industrial voltages. Industries such as manufacturing, mining, oil and gas, and utilities use fused switches to handle high current loads and fault levels. Their ability to withstand harsh conditions and offer quick isolation makes them essential for critical applications like motor control centers, and Heavy machinery.

By Mount

Increasing Demand for High Power Disconnect Switches to Boost Din Rail Mount Segment Growth

Based on mount, the market is segmented into panel, din rail, and others.

The din rail mount segment dominates and is likely to continue its dominance, followed by panel mount. The din rail segment is preferred for its ease of installation, flexibility, and modularity in various industrial settings. DIN rail switches are also favored for their compact size and adaptability.

Panel-mounted switches account for a significant share as they are used particularly in heavy-duty applications. They are installed directly into control panels or electrical boxes and are often preferred where robust switches are required. With the rise of industrial automation and smart control systems, there is growing demand for streamlined, modular panels. Panel mounts are well suited for programmable logic controllers, motor control centers, and other automation panels.

By Voltage

Increasing Demand for Remote Monitoring Systems Boosts the Upto 150V Segment Growth

Based on voltage, the market is segmented into upto 150 V, 150-300 V, and above 300 V.

The up to 150V segment is expected to hold the largest share of the market, driven by the growing need for remote monitoring and control systems in various industries and the increasing adoption of remote monitoring and control systems. This segment caters to various industrial and automation applications, demanding quick accessibility for disconnection solutions.

- In February 2021, Omron launched a K7GE-MG monitoring device that automatically measures the insulation resistance of electric equipment at manufacturing facilities and facilitates remote monitoring.

The development of industrial automation systems is expected to foster demand for the market in the coming years. The upto 150 V segment is ideal for low voltage control circuits, lighting systems, and DC power systems especially in industrial automation and renewable energy.

The above 300 V segment of the market is growing due to its crucial role in medium to high power industrial and infrastructure applications.

Industrial Disconnect Switch Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Industrial Disconnect Switch Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

A robust industrial base, stringent safety regulations, and the growing adoption of renewable energy sources primarily drive the market in North America. These factors, coupled with technological advancements and increasing investments in electrical infrastructure, contribute to a strong demand for disconnect switches that provide safe and reliable isolation for maintenance and repair activities. The emphasis on safety, particularly in industrial settings, fuels the demand for non-fused disconnect switches, further driving the regional market growth. The U.S. and Canada are upgrading aging electrical grids, substations, and industrial facilities. Disconnect switches are critical components for safely isolating electrical systems during maintenance or emergencies. The North America market generated USD 1.39 billion in 2025, representing 27.85% of the global market landscape, and is expected to reach USD 1.47 billion in 2026.

- In March 2025, Iberdrola announced plans to invest USD 20 billion in power generation, transmission, and distribution of electricity in the U.S. Heavy investments in grid infrastructure enhancement will fuel the market in coming years.

Europe

The market in Europe is experiencing growth primarily due to increased investment in electricity transmission and distribution infrastructure, rising industrialization, and stringent safety regulations. Key drivers include the expansion of the energy sector, rapid technological advancements enhancing switch efficiency, and the need for compliance with safety standards, particularly in industrial voltages. Furthermore, the transition to renewable energy sources and the focus on smart technologies are also influencing the demand for advanced disconnect switches. Europe is aggressively moving toward net zero emissions, with major investments in renewable energy (solar, wind, hydro) and electrification of industry. The rise of industry 4.0 in Germany, France, and Italy is boosting demand for automated machinery, robotics, and smart control panels. Europe contributed 15.96% to the global market in 2025, with a valuation of USD 0.8 billion, and is projected to reach USD 0.83 billion in 2026.

- In March 2025, General Electric Aerospace announced plans for investment across Europe manufacturing sites. The company aims to expand its production capabilities for commercial and aerospace industries.

Asia Pacific

Asia Pacific's industrial disconnect switch market growth is driven by rapid industrialization, urbanization, and investments in electrical infrastructure, particularly in China and India. Increasing focus on renewable energy and modernization of power distribution networks also contribute to the growth, as disconnect switches are essential for safe isolation during maintenance and emergencies. China, India, Indonesia, Vietnam, and Thailand are undergoing fast paced industrial growth. Industries such as manufacturing, construction, mining, and food processing require reliable disconnect switches for machinery, control panels, and motor isolation. Asia Pacific accounted for USD 2.04 billion in 2025, representing 40.88% of the global market share, and is projected to reach USD 2.16 billion in 2026.

Latin America

The market in Latin America is experiencing growth due to increasing industrialization, rising energy demands, and increased focus on renewable energy. Modernization of electrical grids, especially in power generation, transmission, and distribution, is boosting demand for reliable disconnect switches. Furthermore, the expansion of industrial and energy sectors, alongside government initiatives supporting renewable energy projects, is further driving the regional market growth. Brazil, Mexico, Argentina, and Chile are witnessing growth in automotive manufacturing, food and beverage processing, mining and metal refining, and chemical and pharmaceutical industries. Latin America contributed approximately USD 0.43 billion to the global market in 2025, accounting for 8.54% share, and is expected to reach USD 0.45 billion in 2026.

Middle East & Africa

The industrial disconnect switch market growth in the Middle East & Africa is driven by increasing demands for safer electrical systems, particularly in the context of industrial and commercial facilities. This is fueled by factors such as the need for reliable isolation during maintenance and emergencies, compliance with safety regulations, and the rapid growth of the energy sector and urbanization, which necessitate modernizing electrical grids and promoting sustainable energy solutions. Furthermore, the increasing emphasis on workplace safety and the adoption of non-contact safety switches are also key drivers of the regional market growth. Mega projects such as NEOM (Saudi Arabia), Lusail City (Qatar), and New Administrative Capital are fueling the demand for low and medium voltage disconnect switches in HVAC panels, backup generators, and lighting and motor control panels. In 2025, Middle East & Africa held 6.77% of the global market, reaching a valuation of USD 0.34 billion, and is projected to grow to USD 0.35 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies are Focused on Increasing Product Offerings Globally to Expand Market Share

The global market is fragmented with companies such as Littelfuse, General Electric, Schneider Electric SE, Havells India Ltd, and others which account for a significant market share. For instance, in November 2020, Littelfuse launched the DC disconnect switch product line Littelfuse LS6 (available in 1000 and 500 volts) and the LS6R (available in 1500 volts), catering to operations requirements for energy efficiency and convenience. Hence, these disconnect switches provide shock resistance and isolation of circuits and repair systems. The market players are focused on enhancing their industrial disconnect switches range to increase their market share.

LIST OF KEY INDUSTRIAL DISCONNECT SWITCH COMPANIES PROFILED

- General Electric (U.S.)

- Littelfuse Inc. (U.S.)

- Schneider Electric SE (France)

- Havells India Ltd (India)

- Siemens AG (Germany)

- Altech Corporation (U.S.)

- Eaton Corporation (Ireland)

- SDCEM (France)

- ABB (Switzerland)

- Sälzer Electric GmbH (Germany)

- Honeywell (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2023: Mennekes launched a new range of industrial ganged motor disconnect switches with multi-range 30 to 60-amp disconnect assembly for protection from harsh wash-down environments.

- October 2023: Littelfuse Inc. announced the launch of its Class J Fuse Disconnect Switch, which combines a switch and fuses into multiple fuses to offer convenience to users for opening and closing circuits while protecting against short circuits and overcurrent.

- June 2023: RS Group plc announced the expansion of its Altech Corporation disconnect switches with LSF Series and RT Series non-fusible motor disconnect switches and accessories.

- July 2023: Eaton Corporation announced supply contracts of battery disconnect units (BDU) for multiple EV manufacturers with 400 and 800-volt configurations. Eaton’s BDU integrates its Breaktor circuit protection technology for the reduction of cost and complexity.

- October 2020: Sécheron developed “SWI(N)” equipped with a new configuration for disconnect switch series SW. The enhancement covers applications where selector switches are required to stop the moving contact and lock it in an intermediate disconnected position.

REPORT COVERAGE

The global market analysis provides market size and forecast by all the segments included in the report. It includes details on the market dynamics and trends expected to drive the market in the forecast period. It offers information on key regions/countries, key industry developments, new product launches, details on partnerships, mergers & acquisitions, and investments in key countries. The report covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 5.94% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Mount

|

|

|

By Voltage

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.99 billion in 2025 and is projected to reach USD 8.35 billion by 2034.

In 2025, the market value stood at USD 2.04 billion.

The market is expected to exhibit a CAGR of 5.94% during the forecast period of 2026-2034.

The non-fused segment led the market by type.

The key factor is the modernization of industrial infrastructure to drive market growth across the globe.

Littelfuse, General Electric, Schneider Electric SE, Havells India Ltd, and others are the top players in the market.

Asia Pacific dominated the market in 2025 by holding the largest share.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us