Industrial Image Processing Hardware Market Size, Share & Industry Analysis, By Product Type (Industrial Cameras, Frame Grabbers, Vision Controllers & Processors, Optics, and Others), By Processing Technology (CPU-Based, GPU-Based, FPGA-Based, ASIC/SoC-Based, and AI Accelerator-Based), By Application (Inspection & Defect Detection, Measurement & Gauging, Identification & Code Reading, Positioning & Guidance, and Others), By End-Use Industry (Automotive, Electronics & Semiconductor, Food & Beverage, Healthcare, Packaging & Printing, and Others), and Regional Forecast, 2026 – 2034

Industrial Image Processing Hardware Market Size and Future Outlook

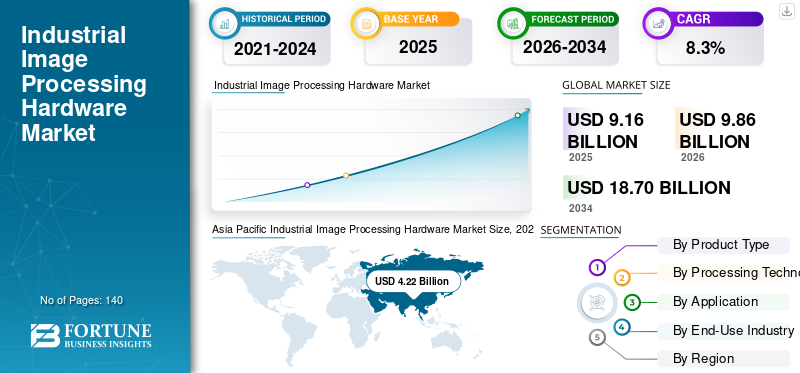

The global industrial image processing hardware market size was valued at USD 9.16 billion in 2025. The market is projected to grow from USD 9.86 billion in 2026 to USD 18.70 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period. Asia Pacific dominated the global market with a market share of 46.07% in 2025.

Industrial image processing hardware comprises specialized imaging technologies and machine vision components designed to capture, process, analyze, and transmit visual data across automated industrial environments within the global image processing ecosystem. These hardware systems include industrial cameras, vision controllers and processors, frame grabbers, optics and lenses, lighting systems, vision sensors, and communication interface hardware that collectively support high-speed inspection, measurement, identification, positioning, and process monitoring applications in manufacturing and logistics operations. Image processing hardware enables manufacturers to improve production accuracy, reduce defect rates, enhance operational consistency, and support enabling real-time automation across complex production workflows. The increasing demand for real time inspection and high performance manufacturing environments is accelerating the adoption of advanced image processing solutions across the industrial sector. These systems are widely deployed in automotive manufacturing, electronics and semiconductor production, food and beverage processing, pharmaceuticals, packaging, aerospace, warehousing, and smart factory environments where high resolution inspection and automated visual analysis are critical to operational performance.

- For instance, in March 2025, Basler AG expanded its AI-powered machine vision portfolio with advanced embedded vision solutions and high-performance industrial camera systems. These solutions are designed to support intelligent factory automation, robotics guidance, and real-time industrial inspection applications.

Cognex Corporation, Keyence Corporation, Basler AG, Teledyne FLIR LLC, Omron Corporation, Sony Group Corporation, Allied Vision Technologies GmbH, IDS Imaging Development Systems GmbH, Baumer Holding AG, and Advantech Co., Ltd. are among the major companies operating in the market. Their market positioning is supported by expertise in industrial imaging technologies, AI-enabled machine vision systems, embedded processing platforms, high-speed inspection solutions, and smart manufacturing integration capabilities, along with continued investments in advanced sensor technologies, edge computing architectures, 3D vision systems, and intelligent automation platforms to support evolving industrial automation and precision manufacturing requirements.

Download Free sample to learn more about this report.

INDUSTRIAL IMAGE PROCESSING HARDWARE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 9.16 billion

- 2026 Market Size: USD 9.86 billion

- 2034 Forecast Market Size: USD 18.70 billion

- CAGR: 8.3% from 2026–2034

- Asia Pacific dominated the market with a 46.07% share in 2025.

- AI accelerator-based segment is projected to grow at a CAGR of 11.9%.

- Predictive maintenance segment is expected to grow at a CAGR of 10.4%.

North America

North America accounted for over USD 2.34 billion in 2025, driven by AI-enabled machine vision and smart manufacturing adoption.

Europe

Europe maintained strong growth through Industry 4.0 adoption and increasing deployment of intelligent factory automation technologies.

Asia Pacific

Asia Pacific generated USD 4.22 billion in 2025 and remained the largest regional market, supported by strong automation and semiconductor investments.

U.S.

The market is estimated to reach USD 1.97 billion in 2026.

Japan

The market is estimated at USD 0.75 billion in 2026.

Read More

INDUSTRIAL IMAGE PROCESSING HARDWARE MARKET TRENDS

Rising Adoption of AI-Enabled Machine Vision and Edge-Based Inspection Systems to Transform Industrial Automation Environments

The demand for image processing hardware is increasingly being driven by the rapid adoption of AI-enabled machine vision systems, edge-based image processing platforms, and intelligent industrial automation technologies across manufacturing and logistics sectors. As enterprises continue accelerating Industry 4.0 initiatives and smart factory deployments, manufacturers are investing heavily in advanced imaging hardware capable of supporting high-speed inspection, automated defect detection, real-time process monitoring, and precision robotic guidance across complex production environments. The market is witnessing the growing demand for high-resolution industrial cameras, AI-enabled vision controllers, embedded image processing systems, 3D imaging technologies, and intelligent vision sensors that can improve operational efficiency, reduce quality inconsistencies, minimize production downtime, and support predictive manufacturing workflows.

- For instance, in March 2025, Cognex Corporation introduced advanced AI-enabled machine vision systems and edge-based industrial imaging solutions designed to improve automated defect detection, robotic guidance, and real-time inspection capabilities across manufacturing and logistics applications, according to the company’s official product announcement.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Adoption of Smart Manufacturing, AI-Based Inspection, and Industrial Automation to Drive Market Growth

The industrial image processing hardware market growth is being driven by the rapid expansion of smart manufacturing facilities, AI-enabled industrial automation systems, and digitally connected production environments across global manufacturing sectors. As enterprises continue accelerating Industry 4.0 transformation initiatives, manufacturers are investing heavily in advanced machine vision hardware capable of supporting automated inspection, robotic guidance, high-speed quality control, process monitoring, and real-time production analytics across complex industrial operations. Image processing hardware is becoming a critical component within modern factory automation ecosystems as enterprises seek to improve production accuracy, reduce operational downtime, minimize material waste, optimize labor utilization, and enhance manufacturing scalability within high-volume production environments.

- For instance, in February 2025, Siemens announced the expansion of its industrial AI and machine vision capabilities through new smart manufacturing solutions designed to support automated inspection, edge-based analytics, and intelligent production optimization across industrial automation environments, according to the company’s official industrial automation announcement.

MARKET RESTRAINTS

High System Integration Complexity and Elevated Deployment Costs May Limit Market Penetration

The growth of the market is constrained by the high complexity associated with industrial vision system integration, production-line customization requirements, and the substantial technical expertise required to deploy advanced image processing infrastructure across diverse manufacturing environments. Unlike conventional industrial hardware installations, industrial image processing systems often require extensive calibration, optics configuration, lighting optimization, software interoperability testing, robotic synchronization, and integration with existing manufacturing execution systems MES and factory automation infrastructure, resulting in longer implementation timelines and higher deployment costs for enterprises. Many organizations, particularly small and medium-sized manufacturers, continue to face challenges related to high upfront investment requirements, uncertain return on investment ROI visibility, and shortages of skilled machine vision engineers, automation specialists, and industrial AI professionals capable of managing complex imaging and inspection environments.

MARKET OPPORTUNITIES

Increasing Demand for High-Speed Semiconductor Inspection and AI-Based Quality Control to Create Long-Term Market Opportunities

A major opportunity emerging within the market is the rising deployment of high-speed semiconductor inspection systems, AI-powered quality control infrastructure, and precision manufacturing technologies across advanced industrial sectors. As semiconductor manufacturers, electronics producers, and EV battery manufacturers continue expanding production capacity, the demand is increasing for industrial imaging hardware capable of delivering ultra-precise defect detection, micron-level measurement accuracy, and real-time process verification across high-volume manufacturing environments. This is creating substantial opportunities for vendors offering advanced industrial cameras, embedded vision processors, 3D imaging systems, intelligent lighting platforms, and AI-enabled inspection hardware optimized for automated production ecosystems.

- For instance, in April 2025, Keyence Corporation expanded its machine vision portfolio with the launch of new AI-integrated vision inspection systems designed to improve automated defect detection, dimensional measurement accuracy, and high-speed production inspection capabilities for advanced manufacturing applications, according to the company’s official product announcement.

MARKET CHALLENGES

Increasing Processing Complexity and Multi-System Synchronization Requirements to Challenge Operational Scalability

One of the major challenges affecting the market is the increasing technical complexity associated with synchronizing imaging hardware across high-speed industrial automation environments and multi-system manufacturing architectures. Modern industrial production facilities often require machine vision systems to operate simultaneously with robotics platforms, conveyor systems, industrial sensors, programmable controllers, and AI-enabled analytics infrastructure while maintaining real-time inspection accuracy and production continuity. Managing these highly synchronized operations creates substantial integration challenges, particularly in industries requiring micron-level inspection precision and ultra-fast production throughput. Industrial image processing systems also face operational difficulties related to variable lighting conditions, reflective surfaces, motion blur, environmental contamination, and rapidly changing product configurations that can impact imaging consistency and inspection reliability.

Segmentation Analysis

By Product Type

Industrial Cameras Segment Led the Market Owing to Rising Deployment of Automated Optical Inspection across Various Industries

By product type, the market is segmented into industrial cameras, frame grabbers, vision controllers & processors, optics, lighting systems, vision sensors, and communication interface hardware.

The industrial cameras segment held the largest market share in 2025 as they serve as the primary image acquisition component across industrial image processing and machine vision environments. The increasing adoption of automated optical inspection AOI systems, robotic guidance technologies, semiconductor inspection platforms, and AI-enabled quality control systems across automotive, electronics, logistics, food processing, and pharmaceutical manufacturing facilities has significantly strengthened the demand for high-resolution industrial cameras globally. Manufacturers are increasingly deploying area scan cameras, line scan cameras, 3D imaging cameras, and smart vision cameras to support real-time inspection, defect detection, dimensional measurement, and precision automation across high-speed production environments. The growing expansion of EV battery manufacturing, semiconductor fabrication, smart warehousing, and industrial robotics infrastructure has further accelerated the deployment of advanced industrial camera systems capable of supporting low-latency image capture and intelligent manufacturing operations.

- For instance, in October 2024, Basler AG announced the expansion of its ace 2 industrial camera portfolio with new high-performance models designed for factory automation, semiconductor inspection, logistics automation, and robotics applications, according to the company’s official product release.

The vision controllers & processors segment is expected to witness the highest growth at a CAGR of 10.1% over the analysis period. This is driven by the increasing adoption of edge AI processing, embedded vision systems, real-time industrial analytics, and AI-enabled machine vision applications requiring high-speed image processing capabilities across advanced manufacturing environments.

To know how our report can help streamline your business, Speak to Analyst

By Processing Technology

CPU-Based Segment Led the Market Owing to Broad Industrial Adoption and Compatibility across Existing Automation Infrastructure

By processing technology, the market is segmented into CPU-based, GPU-based, FPGA-based, ASIC/SoC-based, and AI accelerator-based.

The CPU-based segment held the largest market share in 2025 as CPUs continue to serve as the foundational processing architecture across a wide range of industrial image processing and machine vision applications. Many industrial manufacturers continue deploying CPU-based vision systems due to their strong compatibility with existing factory automation infrastructure, industrial PCs, programmable logic controllers PLCs, and conventional machine vision software platforms. CPU-based image processing systems are widely utilized in automated inspection, barcode reading, positioning and guidance, process monitoring, and quality verification applications across automotive, packaging, food processing, pharmaceuticals, logistics, and general manufacturing environments. In addition, CPUs remain highly preferred for industrial applications requiring operational flexibility, lower deployment complexity, and cost-effective integration within existing production ecosystems.

The AI accelerator-based segment is expected to witness the highest growth at a CAGR of 11.9% during the forecast period. The segment growth is driven by the increasing adoption of edge AI vision systems, deep learning-enabled defect detection, real-time analytics platforms, and advanced industrial automation applications requiring ultra-fast parallel image processing capabilities across high-speed manufacturing environments.

By Application

Inspection & Defect Detection Segment Led the Market Owing to Rising Deployment of Image Processing Hardware for Quality Enhancement

By application, the market is segmented into inspection & defect detection, measurement & gauging, identification & code reading, positioning & guidance, sorting & classification, process monitoring, and predictive maintenance.

The inspection & defect detection segment held the largest industrial image processing hardware market share in 2025 as industrial manufacturers increasingly deploy machine vision and image processing hardware to improve product quality, minimize production errors, reduce material waste, and enhance operational consistency across automated manufacturing environments. High-speed industrial production facilities require advanced imaging systems capable of detecting microscopic defects, surface irregularities, assembly inconsistencies, dimensional deviations, and packaging errors in real time. As a result, industrial cameras, AI-enabled vision processors, lighting systems, and intelligent inspection hardware are witnessing significant deployment across semiconductor fabrication, automotive manufacturing, electronics assembly, pharmaceuticals, food processing, and packaging operations.

The predictive maintenance segment is expected to witness the highest growth with a CAGR of 10.4% over the analysis period. The segmental expansion is driven by the increasing adoption of AI-enabled condition monitoring systems, edge-based industrial analytics, real-time equipment diagnostics, and intelligent maintenance platforms designed to minimize operational downtime and improve asset reliability across automated industrial environments.

By End-Use Industry

Electronics & Semiconductor Segment Led the Market Owing to Rising Product Demand for High-Speed Inspection

By end-use industry, the market is segmented into automotive, electronics & semiconductor, food & beverage, healthcare, packaging & printing, aerospace & defense, machinery & heavy industry, logistics & warehousing, consumer goods, and others (textile, agriculture).

The electronics & semiconductor segment held the largest market share in 2025 as semiconductor fabrication facilities, PCB manufacturing plants, display panel production units, and electronics assembly operations increasingly rely on advanced industrial image processing hardware for high-speed inspection, micron-level defect detection, precision alignment, and automated production verification. Semiconductor and electronics manufacturing environments require highly accurate machine vision systems capable of supporting wafer inspection, SMT inspection, chip packaging verification, solder joint analysis, micro-component positioning, and contamination detection across complex and high-throughput production lines. As a result, manufacturers are significantly investing in high-resolution industrial cameras, AI-enabled vision controllers, embedded image processing systems, precision optics, and intelligent lighting technologies to improve production quality and reduce defect-related losses.

The logistics & warehousing segment is expected to witness significant growth at a CAGR of 9.8% over the analysis period. This is driven by the increasing deployment of automated warehouse systems, AI-enabled parcel inspection platforms, robotic picking technologies, autonomous mobile robots AMRs, and intelligent inventory tracking infrastructure across global supply chain and e-commerce operations.

Industrial Image Processing Hardware Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Industrial Image Processing Hardware Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific generated the highest revenue of USD 4.22 billion in 2025 and is anticipated to remain dominant during the forecast period. The regional market expansion is strongly associated with the increasing deployment of AI-enabled machine vision systems, automated optical inspection technologies, semiconductor manufacturing equipment, industrial robotics platforms, and intelligent warehouse automation infrastructure across automotive, electronics, semiconductor, logistics, food processing, and advanced manufacturing industries. Asia Pacific has emerged as the global center for industrial automation and electronics manufacturing, supported by large-scale semiconductor fabrication investments, rapid EV battery production expansion, strong robotics adoption, and accelerating smart factory modernization initiatives across China, Japan, South Korea, India, and ASEAN economies.

China Industrial Image Processing Hardware Market

The China market is projected to remain dominant in the Asia Pacific region, with 2026 revenues estimated to be around USD 1.91 billion, representing roughly 19.3% of global sales.

Japan Industrial Image Processing Hardware Market

The Japan market is estimated to touch around USD 0.75 billion in 2026, accounting for roughly 7.6% of the global sales.

India Industrial Image Processing Hardware Market

The India market is estimated at around USD 0.54 billion in 2026, accounting for roughly 5.5% of global sales.

North America

The North America market accounted for over USD 2.34 billion in 2025, supported by rising investments in industrial automation, AI-enabled machine vision deployment, and expanding smart manufacturing infrastructure across the U.S., Canada, and Mexico. The regional demand is strongly influenced by the increasing adoption of automated optical inspection systems, warehouse automation technologies, semiconductor manufacturing equipment, robotic guidance platforms, and intelligent production monitoring systems across automotive, electronics, aerospace, logistics, healthcare, and packaging industries. The region benefits from advanced industrial automation infrastructure, strong AI and edge computing capabilities, high robotics adoption, and the presence of major machine vision and industrial imaging technology providers continuously investing in intelligent inspection systems, embedded vision platforms, and next-generation industrial automation technologies.

U.S. Industrial Image Processing Hardware Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 1.97 billion in 2026. The market is driven by strong adoption of advanced manufacturing technologies, rapid expansion of warehouse automation infrastructure, and increasing investments in semiconductor fabrication, aerospace production, electric vehicle manufacturing, and AI-driven industrial automation systems. The country has emerged as one of the leading adopters of intelligent machine vision technologies integrated with robotic automation, predictive analytics, edge AI processing, and high-speed industrial inspection systems. The demand for image processing hardware remains particularly strong across semiconductor manufacturing, automotive assembly, logistics automation, electronics production, pharmaceutical packaging, and aerospace inspection applications where enterprises increasingly require high-resolution imaging systems, AI-enabled defect detection platforms, robotic guidance technologies, and real-time production monitoring capabilities.

Europe

The Europe market is driven by strong demand for precision manufacturing, advanced machine vision systems, and intelligent factory automation technologies across Germany, the U.K., France, Italy, Spain, and other industrial economies. The regional demand is closely associated with automotive production, industrial machinery manufacturing, semiconductor equipment deployment, pharmaceutical processing, packaging automation, and food manufacturing environments where enterprises increasingly rely on industrial imaging technologies to improve production accuracy, operational efficiency, and manufacturing consistency. Europe benefits from a highly developed industrial engineering ecosystem, strong adoption of Industry 4.0 technologies, and growing implementation of AI-enabled inspection systems, collaborative robotics, and smart production infrastructure across advanced manufacturing facilities.

U.K. Industrial Image Processing Hardware Market

The U.K. market is estimated to reach around USD 0.27 billion in 2026, representing roughly 2.7% of the global sales.

Germany Industrial Image Processing Hardware Market

The Germany market is projected to reach approximately USD 0.61 billion in 2026, equivalent to around 6.2% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in industrial automation, smart manufacturing initiatives, and AI-enabled industrial inspection technologies across GCC countries, Israel, South Africa, and North Africa. The product demand is closely associated with the rising deployment of automated packaging systems, warehouse automation infrastructure, intelligent logistics platforms, and machine vision technologies across industries including food & beverage, pharmaceuticals, logistics, industrial manufacturing, and energy. The GCC countries, particularly the UAE and Saudi Arabia, continue investing in industrial diversification programs, smart factory modernization, and digitally connected manufacturing infrastructure aimed at strengthening non-oil industrial capabilities and accelerating Industry 4.0 adoption.

GCC Industrial Image Processing Hardware Market

The GCC market is projected to reach around USD 0.16 billion in 2026, representing roughly 1.6% of the global sales.

South America

The South America market is driven by increasing industrial modernization, rising adoption of factory automation technologies, and growing investments in production efficiency across major economies such as Brazil, Argentina, and Chile. The regional product demand is primarily associated with automotive manufacturing, food & beverage processing, packaging operations, logistics infrastructure, agriculture-related industries, and general industrial manufacturing rather than large-scale semiconductor or advanced electronics production activities. Brazil and Argentina remain the leading contributors supported by their comparatively established industrial sectors, expanding warehouse automation initiatives, increasing deployment of machine vision inspection systems, and gradual adoption of AI-enabled manufacturing technologies aimed at improving operational efficiency, product quality, and production consistency.

Brazil Industrial Image Processing Hardware Market

The Brazil market is projected to reach around USD 0.15 billion in 2026, representing roughly 1.6% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Broad Industrial Imaging Portfolios and Embedded Processing Platforms to Strengthen Industry Positions

The market is moderately fragmented and technology-intensive, with competitive positioning shaped by capabilities in industrial machine vision systems, AI-enabled image processing, embedded vision technologies, precision optics, and intelligent automation infrastructure. Leading companies including Cognex Corporation, Keyence Corporation, Basler AG, Teledyne FLIR LLC, Omron Corporation, Sony Group Corporation, Allied Vision Technologies GmbH, IDS Imaging Development Systems GmbH, Baumer Holding AG, and Advantech Co., Ltd. maintain strong market positions through broad industrial imaging portfolios combining high-resolution industrial cameras, AI-enabled vision controllers, embedded processing platforms, intelligent lighting systems, 3D imaging technologies, and real-time inspection solutions across complex manufacturing and automation environments.

Competitive differentiation is increasingly influenced by the ability to support AI-driven industrial inspection, edge-based image processing, robotic guidance systems, semiconductor inspection applications, and intelligent factory automation platforms. Companies are continuously investing in embedded AI vision systems, high-speed imaging technologies, advanced CMOS sensors, edge computing architectures, and industrial automation integration capabilities to improve operational accuracy, accelerate inspection performance, optimize manufacturing efficiency, and support digitally connected smart factory ecosystems across automotive, electronics & semiconductor, logistics, healthcare, packaging, and aerospace industries.

- For instance, in May 2026, Cognex Corporation launched the In-Sight 3900 Vision System, a fully integrated embedded AI vision system powered by Qualcomm Dragonwing platforms, designed to deliver high-speed, high-resolution edge inspection for factory-floor applications.

LIST OF KEY INDUSTRIAL IMAGE PROCESSING HARDWARE COMPANIES PROFILED

- Cognex Corporation (U.S.)

- Keyence Corporation (Japan)

- Basler AG (Germany)

- Teledyne FLIR LLC (U.S.)

- Omron Corporation (Japan)

- Sony Group Corporation (Japan)

- Allied Vision Technologies GmbH (Germany)

- IDS Imaging Development Systems GmbH (Germany)

- Baumer Holding AG (Switzerland)

- Advantech Co., Ltd. (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Zebra Technologies Corporation introduced new industrial fixed scanning and machine vision solutions designed to improve automated tracking, intelligent inspection, and warehouse automation efficiency across logistics and manufacturing environments.

- February 2026: Omron Corporation announced the expansion of its FH Series machine vision systems with enhanced AI-powered inspection capabilities aimed at improving high-speed defect detection and precision manufacturing automation applications.

- November 2025: IDS Imaging Development Systems GmbH launched new uEye EVS industrial cameras featuring event-based vision sensor technology designed for high-speed motion analysis and real-time industrial automation applications.

- August 2025: Allied Vision Technologies GmbH introduced new Alvium camera modules with embedded edge processing capabilities. The modules have been designed for compact industrial vision systems, robotics integration, and AI-enabled automation environments.

- April 2025: Baumer Holding AG expanded its industrial sensor and vision portfolio with new high-performance LX series cameras. These solutions have been developed for semiconductor inspection, precision measurement, and automated manufacturing applications.

REPORT COVERAGE

The global industrial image processing hardware market analysis includes a comprehensive study of the market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers, acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides an in-depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Processing Technology, Application, End-Use Industry, and Region |

| By Product Type |

|

| By Processing Technology |

|

| By Application |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 9.16 billion in 2025 and is projected to reach USD 18.70 billion by 2034.

In 2025, the North America market value stood at USD 2.34 billion.

The market is expected to exhibit a CAGR of 8.3% during the forecast period (2026-2034).

By end-use industry, the electronics & semiconductor segment led the market in 2025.

Smart manufacturing adoption, industrial automation growth, AI-enabled machine vision, semiconductor expansion, warehouse automation, and increasing automated quality inspection demand are key factors driving the market.

Cognex, Keyence, Basler, Teledyne FLIR, Omron, Sony, Allied Vision, IDS Imaging, Baumer, and Advantech are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us