5G in Aviation Market Size, Share& Industry Analysis By Platform (5G Airport and 5G Aircraft), Technology (FWA, URLLC/MMTC, and eMBB), Communication Infrastructure (Small Cell, Radio Access Network, and Distributed Antenna Systems), 5G Services (Airport Operations, and Aircraft Operations), and Regional Forecast, 2026-2034

5G in Aviation Market Size and industry Overview

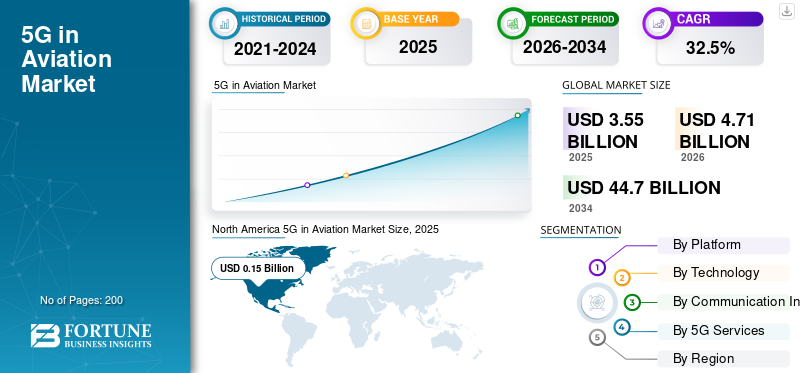

The global 5G in aviation market size was valued at USD 3.55 billion in 2025. The market is projected to grow from USD 4.71 billion in 2026 to USD 44.70 billion by 2034, exhibiting a CAGR of 32.50% during the forecast period. North America dominated the 5G market in aviation, with a market share of 42.86% in 2025, highlighting its strategic importance for industry planning. This growth is driven by airport digital transformation, the need for secure connectivity, operational efficiency requirements, safety-driven network modernization, spectrum coordination efforts, and the controlled adoption of low-latency communications infrastructure.

5G in Aviation is a core wireless communication and networking system connecting the aviation infrastructure and technologies, which facilitates data exchange to its end-users. The mobile networks of the fifth generation are broadly commercializing wireless communication and networking technology through the replacement of 4G LTE communication and hardware infrastructure. The 5G connectivity upgrade offers faster internet connectivity compared to previous technologies. Expanding the technical scope of aviation Internet of Things (IoT), along with Augmented Reality (AR) and Virtual Reality (VR) concepts, is the main object of 5G in the aviation market.

The 5G in the aviation market represents a specialized intersection of telecommunications infrastructure and safety-critical aerospace operations. Unlike consumer or general enterprise 5G deployments, aviation adoption is governed by regulatory compliance, interference management, and system certification requirements. As a result, market size growth follows infrastructure modernization cycles rather than rapid technology replacement. Adoption is incremental, capital-intensive, and closely aligned with long-term airport and airline investment plans.

Airports currently form the primary demand center. Airport operators deploy private or hybrid 5G networks to digitize airside operations, baggage handling, security screening, terminal management, and ground vehicle coordination. These use cases prioritize reliability, deterministic latency, and coverage control over peak data rates. Aircraft-based applications remain in earlier stages, progressing cautiously due to avionics integration complexity and certification timelines.

Institutional buyers evaluate 5G in aviation solutions through total cost of ownership, lifecycle support, cybersecurity resilience, and interoperability with legacy systems. Stakeholders require assurance that 5G deployments do not compromise navigation, surveillance, or safety communications. Consequently, procurement decisions emphasize phased rollouts, pilot programs, and extensive validation.

From a technology standpoint, enhanced Mobile Broadband supports passenger-facing and data-intensive airport systems, while Ultra-Reliable Low-Latency Communication underpins time-sensitive operational workflows. Fixed Wireless Access enables backhaul connectivity in remote or hard-to-wire airport zones. Small cells and distributed antenna systems dominate infrastructure choices due to precision coverage and interference mitigation.

Regionally, North America and Europe lead early adoption through airport modernization initiatives and regulatory frameworks. Asia-Pacific demonstrates strong medium-term potential driven by new airport construction and smart infrastructure programs. Competitive dynamics involve telecom equipment providers, aviation system integrators, and network operators operating within tightly regulated ecosystems. Overall, the 5G in the aviation industry shows disciplined, predictable growth anchored in safety, efficiency, and long-term infrastructure planning.

5G in aviation facilitates the tremendous potential of integrating digital technology with mass utilization, thus fueling the market growth of 5G in the aviation market. 5G in the aviation industry is at a nascent stage. However, the aviation industry's adoption rate and application are well-articulated due to its low latency and ultra-high reliability with technological assimilation in digital aviation. Market forecasting for digital aviation is estimated to encompass the whole ecosystem of commercial and business aviation, from aircraft OEMs to airlines, and towards their facility users, from MRO service providers to all stakeholders.

Download Free sample to learn more about this report.

5G in Aviation Market Key Takeaways

- 2025 Market Size: USD 3.55 billion

- 2026 Market Size: USD 4.71 billion

- 2034 Forecast Market Size: USD 44.70 billion

- CAGR: 32.50% from 2026–2034

- North America dominated the 5G in aviation market with a 42.86% share in 2025.

- The 5G airport segment accounted for the largest market share in 2025.

- Private and hybrid network architectures dominated the market due to enhanced operational control and cybersecurity.

North America

North America leads adoption through airport modernization initiatives and deployment of private 5G networks.

Asia Pacific

Asia Pacific is expected to witness strong growth, supported by smart airport projects and digital aviation programs.

Europe

Europe is advancing through private network deployments focused on operational efficiency and regulatory compliance.

U.S.

Strong investment in airport digital transformation and secure connectivity infrastructure is driving market growth.

Japan

Adoption focuses on resilience, disaster preparedness, and reliable 5G-enabled airport operations.

Read More

5G in Aviation Market Trends

Download Free sample to learn more about this report.

Collaborations between Leading Telecom Players to Augment Market Development

The company Seamless Air Alliance is a non-profit organization formed in 2019. The alliance aims to facilitate the usage of 5G technology in mobile devices while traveling. The coalition was established by leading technology companies, including One Web, Airtel, GoGo, and Sprint. Among these, One Web is a multi-global communications company. It has several objectives, chief among which is launching a network of microsatellites in low-Earth orbit.

GoGo is a multinational company that operates in-flight broadband systems with airlines, while Sprint and Airtel are leading telecommunications companies that primarily provide wireless services. These companies utilize their core competencies to develop advanced infrastructure, enabling 5G connectivity in the aviation industry.

The alliance offers several benefits, comprising of in-cabin broadband services. Its main aim is to allow passengers to use their mobile devices and connect to the network using satellite systems. Technology standardization will address the issues related to internet access for passengers on board and the login system, which requires a more sophisticated network. These companies are making these technologies for commercial use, meaning that 5G roaming should only be available in aircraft cabins from 2019 onwards.

- North America witnessed 5G in the aviation market growth from USD 0.09 Billion in 2019 to USD 0.15 billion in 2020.

Moreover, several industry players have already invested in 5G infrastructures, which will enable IoT for baggage handling, passenger boarding, security check-ins, and other airport-side operations. The augmentation of 5G technology would improve passenger experience and boost operational efficiencies. On the other hand, aviation MRO operations will be assisted by IoT to anticipate and resolve several issues before they become bothersome.

5G in Aviation Market Growth Factors

Increasing Demand for the Aviation 5G Industry to Propel Market Growth of Market

Factors such as a rise in demand for 5G infrastructure for aircraft flight operations, several applications of 5G, such as high-speed data streaming and real-time health monitoring, are projected to be some of the leading 5G trends in the aviation market. In drones, 5G technology can be used to provide real-time data effectively.

The growing demand for high-speed internet connectivity in airports and for aircraft communication and networking is also expected to fuel the market's growth. 5G technology in aviation is used for aircraft safety and security purposes at the airport. It can also use voice communication, high-speed internet connection at airports and air traffic control towers, and air traffic management. The introduction of 5G connectivity for the Nextgen air traffic system is estimated to grow the demand for 5G in the aviation industry.

On the airport side, ground operators send real-time data with the help of a fast internet connection to baggage and gates, which is projected to fuel the growth of 5G infrastructure for airports. Moreover, increasing demand for better flight experience and fast internet connection throughout the flight journey is expected to boost the growth of the 5G services market in aircraft operations.

Rising Demand for Fast Internet Connectivity in the Aviation Industry to Boost 5G in the Aviation Market

Internet connectivity plays a crucial role in better aircraft connectivity. 5G represents a technologically advanced seismic shift along with fast internet service. 5G technology can be used a hundred times faster than its predecessor, 4G LTE. In addition, 5G networks have much higher capacity, providing a constant, guaranteed, and high-speed connection to passengers.

The effects of better Wi-Fi connectivity are a primary aspect of the aviation industry. Passengers can access high-definition video according to their preference during air travel, substantially augmenting the 5G in the aviation market revenue. Seamless Air Alliance, which includes a host of airlines, telecommunications providers, and other tech firms, provides Wi-Fi connectivity in the air as it is on the ground. It aims to create industry standards that enable travelers on any flight to go online with their own devices.

The need for resilient, low-latency connectivity to support increasingly digital airport operations is driving market growth. Modern airports function as complex, data-driven environments requiring real-time coordination across airside, landside, and terminal systems. Fifth-generation networks enable reliable communication for asset tracking, ground handling coordination, and predictive maintenance activities.

Operational efficiency pressures reinforce adoption. Airlines and airport authorities face ongoing cost constraints and capacity challenges. 5G supports automation, situational awareness, and data integration, allowing operators to reduce turnaround times and improve resource utilization. Network slicing enables prioritization of safety-critical applications, a key requirement in aviation environments.

Passenger experience modernization also contributes to demand. Biometric boarding, real-time flight information systems, and high-capacity in-terminal connectivity rely on robust wireless infrastructure. While secondary to operational use cases, these applications improve overall return on investment.

Public infrastructure investment programs further support adoption. Governments increasingly fund airport digitization initiatives, provided safety and regulatory conditions are met. Over time, the shift toward smart airport architectures sustains demand for advanced connectivity platforms grounded in operational necessity rather than discretionary upgrades.

RESTRAINING FACTORS

High cost of infrastructure and technology development to restrain the 5G in the Aviation Market Growth

High infrastructure development cost, lack of 5G infrastructure availability, 5G spectrum distribution issues, and technology adoption rate are the major factors hampering the market growth of the aviation 5G market. Despite clear drivers, several constraints moderate the pace of 5G adoption in aviation. Spectrum coexistence remains a central concern. Aviation systems operate within sensitive radio environments, and potential interference with radio altimeters and navigation equipment has prompted heightened regulatory scrutiny. These concerns result in conservative power limits, restricted deployment zones, and extended testing periods.

Certification complexity represents another restraint. Any aircraft-based 5G installation requires rigorous validation and approval processes. These timelines extend deployment schedules and increase program costs, particularly for airlines operating mixed fleets.

Capital intensity also limits adoption. Deploying private or hybrid 5G networks at airports involves substantial upfront investment in infrastructure, integration, and cybersecurity. Smaller airports often lack the financial capacity for large-scale rollouts without public support.

Cybersecurity considerations add further complexity. As aviation systems become more connected, exposure to cyber threats increases. Stakeholders require robust encryption, access controls, and continuous monitoring, raising implementation costs.

Market Opportunities

Several opportunities support medium-term growth in the 5G in the aviation market. Greenfield airport projects represent significant potential, particularly in the Asia-Pacific and the Middle East. New airports can embed 5G infrastructure from the design phase, avoiding retrofit constraints.

Aircraft operations offer a longer-term opportunity. As certification pathways mature, 5G can support real-time aircraft health monitoring, enhanced cockpit-ground data exchange, and predictive maintenance coordination. These applications offer measurable efficiency gains.

Public–private partnerships create additional opportunities. Collaboration between airport authorities, telecom operators, and technology providers enables shared investment and risk mitigation. Such models accelerate deployment while maintaining regulatory oversight.

Edge-enabled automation represents another growth avenue. Combining 5G with artificial intelligence enables autonomous vehicles, enhances security analytics, and facilitates operational optimization.

Managed service models offer upside. Airports are increasingly opting for outsourced network management to reduce internal complexity. Vendors offering end-to-end services, compliance support, and lifecycle management can establish recurring revenue streams and foster long-term customer relationships.

5G in Aviation Market Segmentation Analysis

By Platform Analysis

“Growing Demand for Internet Connectivity at Airports Estimated to Boost 5G in Aviation Market”

The 5G market in aviation is segmented into 5G airports and 5G aircraft, based on the platform.

The 5G airport segment holds a higher market share in the 5G aviation market. The growth of this segment is projected to the increasing demand for better Wi-Fi connectivity for passengers. In July 2020, in accordance with the 3GPP R16 standards, the standards were approved and released, paving the way for large-scale spectrum distribution and 5G deployment within airports worldwide.

5G Airport represents the most mature and commercially deployed segment within the 5G in the aviation market. Airports operate as complex operational hubs requiring continuous connectivity across airside, landside, and terminal environments. 5G Airport deployments support ground handling coordination, baggage tracking, perimeter security, predictive maintenance, and real-time monitoring of assets and personnel.

Private and hybrid network architectures dominate this segment, allowing airport authorities to retain operational control, enforce cybersecurity policies, and manage quality-of-service parameters. Small cell density and localized coverage planning are critical to avoid interference with navigation and surveillance systems. Adoption is strongest among large international hubs with high passenger volumes and complex operational footprints. As airport digitization accelerates, 5G Airport platforms remain the primary contributor to the overall market size.

On the other hand, the 5G aircraft segment is estimated to grow at a higher CAGR during the forecast period. This growth is due to the several applications of 5G in flight and passenger drone operations, such as technologically advanced real-time monitoring and in-flight entertainment services. Factors such as the proliferation of 5G technologies, a high adoption rate of in-flight entertainment, and the standardization of in-flight 5G Communication equipment and services are expected to influence market growth in the 5G aircraft segment.

5G Aircraft platforms represent an emerging but strategically important segment. Aircraft-based applications focus on connectivity between the aircraft and ground systems, including real-time maintenance data transmission, flight operations support, and enhanced situational awareness. Deployment is constrained by avionics certification requirements, electromagnetic compatibility testing, and spectrum coexistence concerns.

Airlines evaluate 5G Aircraft solutions cautiously, prioritizing safety validation and interoperability with existing satellite and air-to-ground communication systems. While near-term adoption remains limited, long-term potential exists as regulatory frameworks evolve and aircraft connectivity architectures modernize. Growth in this segment is gradual, reflecting aviation’s conservative technology adoption cycle.

By Technology Analysis

“Increasing Demand for Latent-free Cloud Access and Real-Time Air Traffic Alerts Drives Market Growth”

By technology, the market is segmented into Massive Machine Type Communications (mMTC) and Ultra-Reliable Low-Latency Communications (URLLC), enhanced mobile broadband segment (eMBB), and Fixed Wireless Access (FWA).

The enhanced mobile broadband (eMBB) segment is estimated to hold a significant market share of the 5G market in aviation. In April 2020, Gogo and Airspan launched 5G air-to-ground broadband for aviation, utilizing Airspan’s carrier-grade 5G technology for Gogo's in-flight entertainment services.

Enhanced Mobile Broadband supports data-intensive applications such as passenger connectivity, high-resolution video surveillance, and digital signage. While enhanced Mobile Broadband is not the primary driver of aviation 5G adoption, it contributes to overall return on investment by enabling high-capacity services. Airports prioritize enhanced Mobile Broadband for terminal environments where user density is high and bandwidth demand fluctuates significantly. Adoption is balanced against interference management and network prioritization requirements.

The ultra-reliable and low-latency communications (URLLC) segment is expected to be the fastest-growing technology segment by CAGR during the forecast period. This growth is attributed to the high demand and adoption rate of URLLC, as well as eMBB, low latency, and improved serviceability. The mMTC (Massive Machine Type Communications) is expected to hold a significant market share during the forecast period, attributed to technologically advanced IoT-based 5G technology for aircraft and airport operations, as well as its accessibility in no-network areas.

Ultra-reliable low-latency communication and massive Machine-Type Communication technologies underpin mission-critical aviation use cases. These capabilities enable deterministic performance for safety-sensitive applications, including autonomous ground vehicles, runway inspection systems, and real-time asset tracking. Ultra-Reliable Low-Latency Communication supports precise timing and low jitter, which are essential for operational coordination. Massive Machine-Type Communication enables connectivity for large volumes of sensors and devices deployed across airport environments. Together, these technologies form the backbone of operational automation initiatives.

Fixed Wireless Access plays a foundational role in aviation 5G deployments, particularly for backhaul connectivity across expansive airport campuses. Fixed Wireless Access provides cost-effective connectivity for remote facilities, temporary structures, and hard-to-wire locations, including hangars and maintenance zones. Airports leverage Fixed Wireless Access to extend network coverage without extensive cabling, improving deployment flexibility. This technology supports operational resilience, especially during infrastructure expansion or reconfiguration projects.

By Communication Infrastructure Analysis

To know how our report can help streamline your business, Speak to Analyst

“Increasing Demand for Sophisticated Communication Infrastructure at Airport is Responsible for Market Growth”

Based on the communication infrastructure, 5G in the aviation market is segmented into a small cell, Radio Access Network (RAN), and Distributed Antenna System (DAS).

The small cell segment is projected to lead the market during the forecast period. This growth is attributed to the exponentially growing aviation sector worldwide, driven by increasing air passenger numbers, rising demand for Wi-Fi connectivity among onboard passengers, and digital connectivity advancements within the aviation industry. The small cell segment is more environment-friendly and will deliver a more seamless 5G signal with reduced power consumption.

Small cell infrastructure dominates aviation 5G deployments due to its suitability for controlled, high-density environments. Small cells enable precise coverage planning within terminals, hangars, aprons, and service corridors. Their low power output reduces interference risk and supports compliance with aviation safety regulations. Airports deploy extensive small cell networks to ensure consistent connectivity while maintaining strict control over signal propagation.

- The small cell segment is expected to hold a 49% share in 2020.

Thus, airlines are projected to focus on developing small cells due to better coverage and quality of 5G networks. Due to this, the demand for small cells in the 5G market in aviation is witnessing high market growth. The RAN segment is expected to hold a significant market share during the forecast period, primarily due to the high adoption rate of RAN-based technology and the increasing demand for Open RAN Network services from service providers.

Radio Access Network components form the core of 5G aviation infrastructure. These systems manage connectivity, handovers, and network slicing across private and hybrid deployments. Aviation-specific Radio Access Network configurations prioritize reliability, redundancy, and secure access control. Integration with existing airport information technology systems is a key consideration, requiring coordination between telecom vendors and aviation system integrators.

Distributed Antenna Systems complement small cell deployments in large indoor spaces. These systems provide uniform coverage across terminals, reducing dead zones and supporting high device density. Distributed Antenna Systems are particularly effective in legacy terminals where structural constraints limit the placement of small cells. Their use enhances passenger connectivity while maintaining operational network performance.

By 5G Services Analysis

“Increasing Number of Tasks Associated with High-Speed 5G Services to Support Market Growth”

Based on 5G Services, the market is classified into airport operations and aircraft operations.

The airport operation segment is projected to grow at the highest CAGR during the forecast period due to the acceptance of high-speed 5G Connected services for ground operations to send real-time data towards the baggage system and check-in gate system.

Airport Operations services account for the largest share of the 5G in the aviation market. These services encompass ground handling coordination, baggage management, security operations, maintenance workflows, and airside vehicle communication. 5G enables real-time data exchange across these functions, improving efficiency and situational awareness. Airport authorities prioritize these services due to their direct impact on operational performance and cost control.

In May 2021, NTT Ltd. and Cologne Bonn Airport are mulling the experimental joint research for intelligent airport operations. Intelligent airport networks help revolutionize passenger experience, specifically at security checkpoints, runway monitoring, and building management. Passenger demand and airport fleets increase in size, IoT, and 5G usage, effectively changing the aviation and aerospace industry, which will help boost the market.

The aircraft segment is anticipated to grow steadily during the forecast period, driven by high demand for in-flight connectivity among OEMs and airlines for their commercial and business aircraft fleets.

Aircraft Operations services represent a longer-term growth area. These services focus on aircraft-ground data exchange, predictive maintenance, and operational analytics. Adoption depends on the progress of certification and integration with existing avionics systems. While current deployments remain limited, interest is growing as airlines seek to optimize maintenance and fleet utilization. Over time, Aircraft Operations services are expected to make meaningful contributions to market growth as regulatory clarity improves.

In March 2021, Global Eagle received the STC certification to install the Airconnect Global Ku inflight connectivity (IFC) system, which can be installed onboard a Boeing 737 aircraft. It is anticipated to demonstrate the in-flight connectivity solutions capability on Turkish Airlines’ short-haul narrow-body aircraft fleet for international and domestic routes.

REGIONAL ANALYSIS

North America 5G in Aviation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America 5G in the Aviation Market Analysis

North America leads early adoption due to airport modernization initiatives and structured regulatory frameworks. Major hubs deploy private 5G networks to support operational digitization. Public funding and industry collaboration support controlled rollouts, emphasizing safety, interoperability, and cybersecurity.

The United States represents the largest national market, driven by its extensive airport infrastructure and significant investment in technology. Deployment focuses on airport operations rather than aircraft connectivity. Regulatory oversight has a significant impact on the rollout pace and network design.

North America is expected to lead the 5G market share in aviation throughout the forecast period, driven by the expansion of the aviation industry. Key players, including Cisco Systems, ANUVU, Gogo, Inseego Corp, Intelsat, SmartSky Networks, Panasonic Avionics, AT&T, T-Mobile, Sprint, Verizon, and Charter, will further drive the growth of 5G in the aviation market.

The market is primarily driven by the increasing demand for air travel and a desire for a better flight experience. In addition, increasing passenger traffic in this region leads to a greater need for improved internet connectivity in both domestic & international airports, as well as on aircraft. Additionally, the expansion of connected aircraft and smart airports in this region is expected to boost the regional market's growth.

Asia-Pacific 5G in aviation Market Analysis

The Asia-Pacific region is the second-largest market and is competing with North America to become the largest. Asia-Pacific also shows remarkable growth due to an increase in the budget allocated for the aviation infrastructure sector in China, Japan, and India. Along with the rest of the Asia-Pacific region, these countries are projected to drive 5G adoption in the aviation market. China is a leading provider of 5G technologies, thanks to companies like Huawei and China Mobile.

The Asia-Pacific region shows strong growth potential, driven by new airport construction and smart infrastructure programs. Governments actively support digital aviation initiatives, thereby accelerating the medium-term adoption of these technologies. Japan emphasizes resilience and disaster preparedness. 5G supports airport operations and transportation integration. Deployment remains cautious, prioritizing reliability and certification. China’s market is expanding through large-scale airport development and the deployment of domestic technology. Focus remains on operational efficiency and infrastructure modernization.

Europe 5G in the aviation Market Analysis

Europe demonstrates a disciplined approach to adoption, shaped by regulatory harmonization and cross-border interoperability requirements. Airports emphasize private network deployments supporting operational efficiency. Safety validation and spectrum coordination guide implementation strategies.

Germany focuses on industrial-grade aviation connectivity supporting efficiency and security. Large airports integrate 5G with automation and logistics systems. Vendor selection prioritizes reliability, compliance, and long-term support. The United Kingdom balances airport modernization with regulatory oversight. Deployments primarily focus on ground operations and passenger services. Public–private collaboration supports phased adoption aligned with safety requirements.

Latin America 5G in aviation Market Analysis

Latin America represents an emerging market with selective adoption at major hubs. Cost considerations shape the deployment scope, favoring use cases related to airport operations.

Middle East & Africa 5G in aviation Market Analysis

The Middle East & Africa region is showing growing adoption, driven by new airport projects and hub development. Investments emphasize modern infrastructure and operational efficiency.

List of Top 5G in Aviation Companies:

- AeroMobile Communications Limited (U.K.)

- Cisco Systems Inc. (The U.S.)

- Telefonaktiebolaget LM Ericsson (Sweden)

- ANUVU Inc. (Global Eagle Entertainment Inc.) (U.S.)

- Gogo LLC (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Inseego Corp. (U.S.)

- Intelsat Corporation (U.S.)

- Nokia Corporation (Finland)

- OneWeb Ltd (U.K.)

- Panasonic Avionics Corporation (U.S.)

- SmartSky Networks LLC (U.S.)

Competitive Landscape

The competitive landscape of 5G in the aviation market is characterized by collaboration rather than pure competition. Telecom infrastructure vendors, aviation system integrators, network operators, and airport technology specialists form interconnected ecosystems. No single vendor dominates globally due to regulatory diversity and localized deployment requirements.

Large telecom equipment providers supply Radio Access Network, core network, and small cell technologies. These companies leverage experience from enterprise and public sector deployments while adapting solutions to aviation safety standards. Their strengths lie in scalability, interoperability, and long-term product roadmaps.

Aviation technology integrators play a critical role in deployment. These firms bridge the gap between telecom systems and aviation operations, ensuring compatibility with airport management systems, security platforms, and regulatory requirements. Their expertise reduces integration risk and accelerates deployment.

Network operators contribute connectivity services, spectrum management, and operational support. Many participate in public–private partnerships with airport authorities, offering hybrid deployment models. Their involvement reduces infrastructure burden on airports while maintaining service quality.

Niche players focus on specialized applications such as edge analytics, cybersecurity, or autonomous systems. These firms enhance functionality within broader ecosystems rather than competing directly with infrastructure vendors.

As per the 5G in the aviation market forecast, this market is dominated by a few key companies due to their prime product portfolio, informed strategic decisions, and market share dominance. Furthermore, these companies have a widespread geographic presence and continually invest in R&D, resulting in secure regulatory approvals.

5G in the Aviation Industry: Key Developments

- March 2024: Nokia expanded its private 5G aviation portfolio to support airport operations, focusing on secure connectivity, low-latency performance, and integration with existing airport systems.

- June 2024: Ericsson partnered with airport authorities to deploy hybrid 5G networks, enabling phased modernization while maintaining strict interference controls and regulatory compliance.

- October 2024: Huawei introduced aviation-specific 5G solutions targeting smart airport initiatives, emphasizing automation, asset tracking, and operational analytics capabilities.

- February 2025: Samsung Networks' advanced small cell technologies optimized for airport environments, supporting high-density deployments with controlled signal propagation.

- May 2025: AT&T expanded managed private 5G services for aviation customers, providing end-to-end network management, cybersecurity monitoring, and lifecycle support.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

This report mainly provides an all-inclusive analysis of 5G in the aviation market across the globe. The market estimates presented in the report are a result of in-depth secondary research, primary interviews, and in-house expert reviews. In addition, these market estimates are considered by studying the impact of several social, political, and economic factors affecting the growth of 5G in the aviation market.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Platform

|

|

By Technology

|

|

|

By Communication Infrastructure

|

|

|

By 5G Services

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global 5G in aviation market was USD 4.71 billion in 2026 and is projected to grow to USD 44.7 billion by 2034, exhibiting a CAGR of 32.5% during the forecast period 2026–2034.

Growth is driven by rising demand for high-speed inflight connectivity, smart airports, and IoT integration for operations such as baggage handling, real-time aircraft monitoring, and passenger services.

The market will be exhibiting steady growth at a CAGR of 32.5%in the forecast period (2026-2034)

North America dominated the market with 42.86% share in 2025, fueled by major telecom and aviation companies, advanced 5G infrastructure, and connected aircraft initiatives.

Key applications include inflight entertainment, real-time aircraft health monitoring, next-gen air traffic systems, baggage handling automation, passenger boarding efficiency, and connected drones.

The market is segmented by platform (5G airports, 5G aircraft), technology (eMBB, URLLC, mMTC, FWA), communication infrastructure (small cells, RAN, DAS), and services (airport operations, aircraft operations).

Trends include alliances between telecom and aviation players (e.g., Seamless Air Alliance), deployment of 5G-ready airports, and integration of AR/VR for passenger experience and training.

Major players include Huawei Technologies, Cisco Systems, Gogo LLC, Nokia Corporation, Panasonic Avionics, Intelsat, Ericsson, SmartSky Networks, OneWeb, and AeroMobile Communications.

Key challenges include high infrastructure costs, 5G spectrum allocation issues, and dependence on 4G non-standalone networks, which affect full-scale deployment in airports and aircraft.

The market is set for rapid expansion as airlines modernize fleets, airports invest in smart infrastructure, and demand for seamless passenger connectivity rises, especially in North America and Asia-Pacific.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us