Automotive Brake Pads Market Size, Share & Industry Analysis, By Vehicle Type (Two Wheeler, Hatchback & Sedan, SUV, LCV, and HCV), By Material (Non-Asbestos Organic (NAO), Semi-Metallic, Ceramic, and Carbon Composite), By Sales Channel (OEM and Aftermarket (Retail and Authorized Service Centers)), By Propulsion Type (ICE, HEV, and EV), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

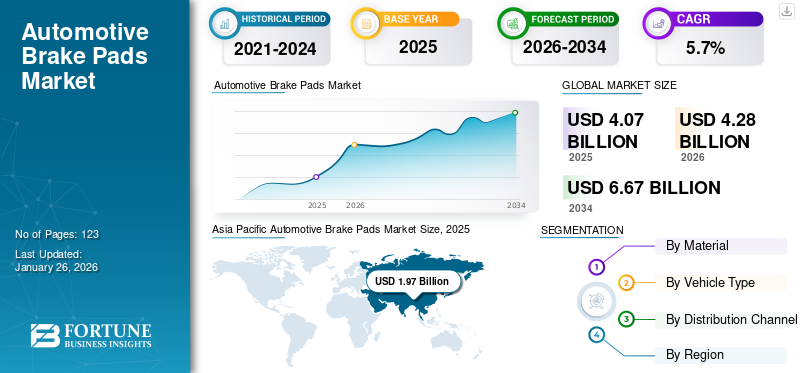

Automotive Brake Pads Market Size and Future Outlook

The global automotive brake pads market size was valued at USD 11.45 billion in 2025. The market is projected to grow from USD 12.11 billion in 2026 to USD 19.11 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. Asia Pacific dominated the automotive brake pads market with a market share of 41.74% in 2025.

Automotive brake pads are friction components fitted in disc braking systems that press against brake rotors to slow or stop vehicles, ensuring driving safety, braking efficiency, heat resistance, and vehicle control performance. Market growth is driven by rising vehicle production, increasing demand for passenger and commercial vehicles, stricter vehicle safety regulations, expanding electric vehicle adoption, and growing aftermarket replacement demand for durable braking components.

Major players in the market include Brembo S.p.A., ADVICS Co., Ltd., Akebono Brake Industry Co., Ltd., Robert Bosch Gmbh, Hitachi Astemo, Ltd., and ZF Group, competing through advanced friction materials, low-noise braking technologies, EV-compatible brake pads, OEM partnerships, lightweight braking systems, and extensive global aftermarket distribution networks.

Download Free sample to learn more about this report.

AUTOMOTIVE BRAKE PADS MARKET TRENDS

Increasing Adoption of Ceramic Brake Pads Enhances Performance and Driving Comfort

The growing adoption of ceramic brake pads is emerging as one of the major market trends due to their superior performance characteristics and enhanced driving comfort. Ceramic brake pads are increasingly preferred in passenger vehicles since they generate lower noise levels, produce less brake dust, and offer smoother braking performance compared to traditional semi-metallic alternatives. These advantages are becoming particularly important as consumers prioritize comfort, cleanliness, and premium driving experiences.

- In October 2025, Akebono Brake Corporation expanded its ProACT and EURO ultra-premium ceramic brake pad lines with seven new part numbers covering over 2 million vehicles. The launch strengthens the company’s aftermarket presence while highlighting rising demand for advanced ceramic brake pads offering improved durability, noise reduction, and OE-level braking performance.

Development of Low-Copper and Environmentally Sustainable Brake Pad Materials Gains Momentum

The transition toward environmentally sustainable brake pad materials is becoming a prominent trend in the market. Regulatory authorities in several countries are implementing restrictions on the use of copper and hazardous materials in brake pads as brake wear particles contribute to environmental pollution and water contamination. As a result, brake pad manufacturers are increasingly developing low-copper and copper-free brake pad formulations to comply with evolving environmental standards.

- In February 2026, DRiV expanded its Ferodo Premier copper-free brake pads for commercial vehicles. The OE-quality pads feature advanced friction materials and a high-performance coating that improves braking efficiency, durability, and bedding-in performance. The launch highlights increasing industry focus on sustainable, low-maintenance, and environmentally compliant brake pad technologies.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Vehicle Parc and Aging Fleet Accelerate Replacement Brake Pad Consumption

The continuous expansion of the global vehicle parc, combined with the aging of vehicles in operation, is a major driver. Passenger cars, light commercial vehicles and two wheeler, and heavy-duty vehicles are remaining on roads for longer periods due to improved engine durability and rising vehicle ownership costs. Older vehicles require more frequent brake maintenance as brake pads experience regular wear through continuous friction and heat generation. As the average age of vehicles increases across developed markets such as North America and Europe, replacement cycles for braking components are becoming more frequent, creating sustained aftermarket demand for brake pads.

- In September 2024, the European Union reported that the average vehicle age reached 12.3 years for cars, 12.5 years for vans and buses, and 13.9 years for trucks. Greece recorded some of the oldest fleets, with trucks averaging 23 years. The aging vehicle parc across Europe is increasing demand for replacement brake pads, brake servicing, and maintenance solutions as older vehicles require more frequent braking system inspections and component replacement.

Increasing Road Safety Awareness and Stringent Braking Regulations Support Market Growth

Growing awareness regarding road safety and the implementation of stringent automotive safety regulations are significantly driving automotive brake pads market growth. Governments and transportation authorities are enforcing stricter vehicle safety standards to reduce road accidents and improve braking efficiency. Regulations mandating regular vehicle inspections and minimum braking performance requirements are encouraging vehicle owners to replace worn brake pads more frequently, thereby supporting consistent aftermarket demand.

- In February 2026, the Indian government mandated advanced safety systems for medium and heavy commercial vehicles, including electronic stability control, advanced emergency braking, and enhanced braking standards, effective from October 2027. The regulations are expected to increase demand for high-performance and durable brake pads capable of supporting advanced braking technologies and improved vehicle safety requirements.

Expansion of E-Commerce and Commercial Vehicle Fleets Increases Brake Pad Replacement Rates

The rapid growth of e-commerce, logistics operations, and freight transportation activities is significantly driving demand for automotive brake pads globally. Rising online retail penetration has increased the deployment of delivery vans, light commercial vehicles, and heavy-duty trucks for last-mile and long-distance transportation. These vehicles operate continuously under demanding driving conditions, resulting in accelerated brake system wear and higher replacement frequency for brake pads.

- In March 2025, ICER Brakes launched its LMD brake pad range for last-mile delivery vehicles. The copper-free NAO brake pads offer 40% to 75% longer lifespan than conventional pads while reducing particulate emissions during braking. The launch reflects growing demand for durable, low-maintenance, and environmentally sustainable braking solutions for commercial delivery fleets.

Rising Adoption of Electric Vehicles Increases Demand for Specialized Brake Pad Technologies

The rising global adoption of electric vehicles is becoming a significant driver for the market as manufacturers develop advanced braking solutions tailored for EV platforms. Although electric vehicles utilize regenerative braking systems that reduce direct friction braking frequency, they still require high-performance brake pads capable of delivering reliable stopping power, corrosion resistance, and thermal stability under varying driving conditions. This is creating strong demand for specialized brake pad materials designed specifically for electric mobility applications.

MARKET RESTRAINTS

Increasing Adoption of Regenerative Braking Systems Reduces Brake Pad Replacement Frequency

The growing adoption of Electric Vehicles (EVs) and hybrid vehicles equipped with regenerative braking systems is emerging as a significant restraint for the market. Regenerative braking technology slows vehicles by converting kinetic energy into electrical energy, thereby reducing reliance on conventional friction braking systems. As a result, brake pads experience substantially lower wear and require less frequent replacement compared to those used in internal combustion engine vehicles.

- In June 2023, ZF partnered with British electric truck manufacturer Tevva to develop an advanced regenerative braking system for 7.5-ton electric trucks. The system recuperates up to four times more energy than conventional air brake systems while reducing friction brake usage and brake pad wear, highlighting the growing impact of regenerative braking technologies on brake component lifespan.

MARKET OPPORTUNITIES

Growing Demand for Low-Noise and Eco-Friendly Brake Pads Creates Product Innovation Opportunities

The increasing consumer preference for environmentally sustainable and low-noise automotive components is creating significant growth opportunities in the market. Governments and environmental agencies across multiple regions are introducing stricter regulations regarding particulate emissions, copper usage, and hazardous materials generated from brake pad wear. This is encouraging manufacturers to develop eco-friendly brake pads using ceramic materials, organic compounds, and low-copper friction technologies.

- In July 2024, Resonac developed a high-performance non-asbestos disc brake pads for EVs featuring strong braking power, high abrasion resistance, and low-noise braking performance. The brake pad also reduces wear debris emissions by 30% compared to conventional low-steel variants, supporting growing demand for environmentally friendly and durable braking solutions for electric vehicles.

Expansion of Automotive Aftermarket Networks in Emerging Economies Supports Future Growth

The rapid development of automotive aftermarket infrastructure in emerging economies presents a major opportunity for the global market. Countries across Asia Pacific, Latin America, and the Middle East & Africa are experiencing strong growth in vehicle ownership, urbanization, and transportation activities. As vehicle populations expand, the demand for maintenance services and replacement automotive components, including brake pads, is increasing steadily.

- In April 2023, Brakes India opened its 100th Qik Brake Service centre in Pune, expanding its nationwide brake service network across 62 cities. The initiative strengthens customer access to brake diagnostics, pad replacement, and maintenance services, reflecting rising awareness regarding vehicle safety and growing demand for organized automotive servicing infrastructure in India.

MARKET CHALLENGES

Volatility in Raw Material Prices Creates Cost Pressures for Manufacturers

Fluctuating prices of raw materials used in automotive brake pad production are restraining market profitability and operational stability for manufacturers. Brake pads are manufactured using various materials, including steel, copper, graphite, ceramic compounds, rubber, and specialized friction modifiers. Variations in the prices of these raw materials significantly affect production costs, particularly for manufacturers operating with narrow profit margins in highly competitive markets.

Segmentation Analysis

By Vehicle Type

Strong Global Demand for SUVs Generated Segment Demand

Based on vehicle type, the market is segmented into two-wheeler, hatchback & sedan, SUV, LCV, and HCV.

The SUV segment dominated the market in 2025, and is set to propel with the fastest-growing CAGR over the forecast period. Strong global demand for SUVs, crossover vehicles, and premium utility vehicles is accelerating brake pad consumption in this segment. Increasing preference for larger vehicles with enhanced safety features and superior driving performance is driving OEM production volumes and creating substantial aftermarket replacement opportunities globally.

- In November 2025, Brembo launched its XTRA Ceramic Severe Duty Brake Pads at AAPEX for pickup trucks, SUVs, commercial fleets, and police vehicles. Scheduled for North American launch in early 2026, the copper-free pads offer improved stopping power, fade resistance, noise reduction, and enhanced durability.

The hatchback & sedan segment holds the second largest automotive brake pads market share. Stable passenger vehicle production and consistent replacement demand are supporting growth in segment. Increasing vehicle parc across emerging economies and rising consumer awareness regarding routine vehicle maintenance are contributing to sustained brake pad consumption in both OEM and aftermarket channels globally.

To know how our report can help streamline your business, Speak to Analyst

By Material

High Durability, Superior Heat Dissipation, and Strong Braking Performance Augmented Semi-Metallic Segment Growth

Based on material, the market is segmented into non-asbestos organic (NAO), semi-metallic,

ceramic, and carbon composite.

The semi-metallic segment dominated the market in 2025, owing to its widespread adoption across passenger and commercial vehicles. High durability, superior heat dissipation, and strong braking performance are driving demand for semi-metallic brake pads globally. These brake pads are extensively utilized in heavy-duty and high-performance vehicles due to their ability to withstand elevated temperatures and demanding operating environments.

The carbon composite segment represented the fastest-growing segment, propelling at a CAGR of 8.0% during the forecast period. Rising demand for high-performance and motorsport vehicles is driving the adoption of carbon composite brake pads globally. These brake pads provide exceptional heat resistance, lightweight characteristics, and superior braking efficiency, making them highly suitable for sports cars and advanced automotive applications.

- In April 2026, Tribol Braking announced the launch of the full-composite brake pad, scheduled for summer 2026. Featuring a ColdForge-Carbon backing plate, the pad is 70% lighter than steel alternatives and significantly reduces heat transfer, improving braking performance, durability, corrosion resistance, and EV efficiency.

By Sales Channel

Increasing Vehicle Parc, Rising Average Vehicle Age Drive Aftermarket Segment Demand

Based on sales channel, the market is segmented into OEM and aftermarket. The aftermarket is further divided into retail and authorized service centers.

The aftermarket segment held the largest market share in 2025 and is expected to maintain its leading position throughout the forecast period. Increasing vehicle parc, rising average vehicle age, and frequent brake component replacement requirements are driving strong demand in the aftermarket segment. Growing consumer awareness regarding preventive vehicle maintenance and expanding automotive repair networks are further supporting aftermarket brake pad sales globally.

- In September 2025, Friction One opened a new brake pad and rotor manufacturing facility in Juarez, Mexico, expanding its North American footprint. The plant targets 16 million brake pad sets annually by 2026 and supports growing demand for copper-free braking solutions through advanced automation and localized production capabilities.

The OEM segment is estimated to propel with a CAGR of 4.7% over the forecast period. Growth in global vehicle production and increasing integration of advanced braking systems are supporting demand for OEM brake pads. Automakers are focusing on enhancing vehicle safety, braking performance, and regulatory compliance, which is driving the adoption of high-quality factory-installed brake components globally.

By Propulsion Type

Sustained Production and Widespread Adoption Boosted ICE Segment Growth

Based on propulsion type, the market is segmented into ICE, EV, and HEV.

The ICE segment dominated the market in 2025, owing to the large global fleet of internal combustion engine vehicles. Sustained production and widespread adoption of conventional gasoline and diesel vehicles continue to support demand for brake pads in the ICE segment. Strong replacement demand from aging vehicle fleets and expanding automotive ownership across developing economies are contributing to consistent market growth globally.

The EV segment represented the fastest-growing demand with a CAGR of 9.3% over the forecast period. Rapid adoption of electric vehicles and increasing investments in sustainable mobility solutions are accelerating demand for specialized brake pads in EVs. The need for lightweight, low-noise, and highly durable braking materials compatible with regenerative braking systems is driving innovation within the segment.

- In February 2026, Delphi launched a new premium brake pad range specifically designed for Battery Electric Vehicles (BEVs). The range offers low-noise, low-dust, copper-free braking solutions for major EV models, including Tesla, BMW, Mercedes-Benz, Porsche, and Nissan.

Automotive Brake Pads Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Brake Pads Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominated the market in 2025 and is expected to remain the fastest-growing regional market throughout the forecast period. Rapid urbanization, expanding automotive production, and rising vehicle ownership across China, India, and Japan are driving strong market growth in the Asia Pacific. Increasing investments in transportation infrastructure and growing demand for passenger and commercial vehicles continue to support brake pad consumption.

- In October 2025, Akebono Brake Industry showcased advanced brake pads and braking technologies at JAPAN MOBILITY SHOW 2025, including high-end aftermarket brake pads alongside WRC brake calipers, EV motorcycle brake systems, and high-performance multi-piston disc brake solutions for automotive and industrial applications.

China Automotive Brake Pads Market

The Chinese market is estimated at around USD 2.60 billion in 2026, accounting for roughly 21.5% of global market revenues. Growth is driven by strong vehicle production, expanding EV adoption, rising aftermarket demand, and increasing investments in advanced braking technologies and premium automotive components.

Japan Automotive Brake Pads Market

The Japanese market is estimated at around USD 0.74 billion in 2026, accounting for roughly 6.1% of global market revenues. Growth is supported by advanced automotive manufacturing, strong hybrid vehicle demand, technological innovation in braking systems, and long-standing OEM supply partnerships with global automakers.

India Automotive Brake Pads Market

The Indian market is estimated at around USD 0.66 billion in 2026, accounting for roughly 5.4% of global market revenues. Growth is fueled by rising vehicle ownership, expanding domestic automobile production, rapid aftermarket expansion, and increasing adoption of electric and commercial vehicles nationwide.

North America

The North America region held the second-largest share of the global market in 2025. The region is expected to grow at a CAGR of 5.3% over the forecast period. Strong automotive production, high vehicle ownership rates, and increasing demand for advanced safety systems are supporting market growth across North America. Rising replacement demand for brake components and growing consumer awareness regarding preventive vehicle maintenance are further driving brake pad consumption in the region.

- In May 2025, Akebono Brake Corporation expanded its Ultra-Premium Disc Brake Pad portfolio by adding new part numbers across its ProACT, EURO, and Severe Duty product lines. The expansion enhances compatibility for passenger, luxury, and commercial vehicles while strengthening Akebono’s premium braking solutions for aftermarket applications.

U.S. Automotive Brake Pads Market

The U.S. market is estimated at around USD 2.64 billion in 2026, accounting for roughly 21.8% of global market revenues. Growth is driven by high vehicle parc volumes, strong aftermarket sales, increasing demand for SUVs and electric vehicles, and continuous advancements in braking performance technologies.

Europe

Europe represented the third-largest market share in 2025. The presence of leading automotive manufacturers and stringent vehicle safety regulations is supporting demand for high-performance brake pads across Europe. Increasing focus on sustainable mobility and low-emission transportation technologies is encouraging the adoption of advanced and environmentally friendly braking materials in the region.

- In August 2025, ZF unveiled new TRW Motorcycle Brake Pads featuring a heavy-metal-free friction material that improves braking performance and heat resistance. The copper, nickel, and antimony-free brake pads reduce brake dust and noise while meeting ECE-R90 standards. ZF stated that over 80% of its motorcycle brake pad portfolio has transitioned to the new formulations, with 90% by the end of 2025.

Germany Automotive Brake Pads Market

The Germany’s market is estimated at around USD 0.48 billion in 2026, accounting for roughly 4.0% of global market revenues. Growth is driven by premium vehicle manufacturing, increasing EV production, advanced automotive engineering capabilities, and strong demand for high-performance and environmentally compliant braking solutions.

U.K. Automotive Brake Pads Market

The U.K. market is estimated at around USD 0.33 billion in 2026, accounting for roughly 2.8% of global market revenues. Growth is supported by rising EV registrations, growing aftermarket replacement demand, increasing focus on vehicle safety standards, and investments in sustainable automotive technologies.

Rest of the World

Rest of the world witnesses a steady market growth. Increasing automotive sales, improving road infrastructure, and rising commercial transportation activities are supporting market growth across South America, the Middle East & Africa. Growing awareness regarding vehicle safety and maintenance practices is also contributing to rising demand for brake replacement components in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Friction Technologies and OEM Partnerships Define Competitive Landscape

The global automotive brake pads market is highly competitive, with leading players competing through advanced friction materials, OEM partnerships, lightweight brake pad technologies, and broad aftermarket distribution networks. Key companies, including Brembo S.p.A., ADVICS Co., Ltd., Akebono Brake Industry Co., Ltd., Robert Bosch Gmbh, Hitachi Astemo, Ltd., and ZF Group, focus on improving braking efficiency, durability, low-noise performance, and EV-compatible brake pad solutions. Companies are expanding manufacturing capabilities, strengthening supply agreements with automakers, and investing in low-dust and environmentally compliant braking technologies to enhance market presence. Increasing demand for electric vehicles, high-performance vehicles, and advanced integrated braking systems continues to intensify competition globally.

- In June 2024, Brakes India and ADVICS announced a joint venture to develop advanced braking systems for India’s light vehicle market. The partnership will initially focus on Electronic Stability Control and other advanced braking technologies.

LIST OF KEY AUTOMOTIVE BRAKE PADS COMPANIES PROFILED IN REPORT

- Brembo S.p.A. (Italy)

- ADVICS Co., Ltd. (Japan)

- Akebono Brake Industry Co., Ltd. (Japan)

- Robert Bosch Gmbh (Germany)

- Hitachi Astemo, Ltd. (Japan)

- ZF Group (Germany)

- HL Mando Corporation (South Korea)

- Continental AG (Germany)

- Nisshinbo Brake Inc. (Japan)

- Valeo SA (France)

- Delphi Technologies (U.K.)

- Tenneco Inc. (U.S.)

- EBC Brakes (U.K.)

- Brakes India Private Limited (India)

- ICER Brakes S.A. (Spain)

KEY INDUSTRY DEVELOPMENTS

- February 2026: DRiV expanded its Ferodo Premier copper-free brake pads for commercial vehicles, introducing advanced OE-quality friction materials and a new high-performance red coating to improve bedding-in performance. The brake pads deliver enhanced stopping power, durability, and reduced wear while eliminating copper-related environmental concerns.

- December 2025: ADVICS and SmartDrive announced BRAKEPAD SCAN powered by ADVICS, an image-based brake pad inspection service scheduled for launch in February 2026. Using a handheld camera and image analysis technology, the system measures brake pad wear with the help of wear sensor without tire removal, improving workshop efficiency, maintenance transparency, and customer satisfaction while helping mechanics standardize inspection quality and reduce missed replacement opportunities.

- May 2025: Brembo unveiled Greentell brakes and pads that cut brake dust emissions by 90 percent using laser metal deposition coating technology. Designed for mass-market vehicles, the system also reduces surface corrosion by 80 percent and improves durability.

- January 2025: Uno Minda launched its Perfomaxx brake pad series for the Indian aftermarket, featuring Heavy Duty Organic Brake Pads with advanced Rubber Metal Rubber (RMR) technology. The new brake pads offer enhanced friction control, reduced noise, improved safety, and compatibility across passenger vehicles and light commercial vehicles.

- September 2024: Brembo introduced its expanded aftermarket brake pad strategy at Automechanika Frankfurt 2024. The company launched new copper-free Xtra and Xtra Ceramic brake pads, alongside extended Beyond EV and Greenance ranges for electric and high-mileage vehicles.

- August 2023: Momentum USA introduced AmeriPLATINUM Plus Max Duty brake pads designed for fleet, emergency-service, and severe-duty applications. The copper-free pads feature A.R.M.-R.A.C. technology to improve durability, reduce noise and vibration, prevent rust-related delamination, and enhance brake system performance under demanding operating conditions.

- March 2023: Tenneco’s Ferodo expanded its zero-copper brake pad portfolio for commercial vehicles, introducing advanced friction formulations for heavy-duty trucks and trailers. The new pads meet evolving environmental regulations while maintaining braking performance, durability, temperature stability, and compatibility with EV and electronic braking systems.

REPORT COVERAGE

The global automotive brake pads market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.9% from 2026-2034 |

| Unit | Value (USD billion) |

| Segmentation | By Vehicle Type, By Material, By Sales Channel, By Propulsion Type, and By Region |

| By Vehicle Type |

|

| By Material |

|

| By Sales Channel |

|

| By Propulsion Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.45 billion in 2025 and is projected to reach USD 19.11 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 4.78 billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period of 2026-2034.

The SUV segment led the market by vehicle type.

Rising vehicle parc and aging fleet accelerate replacement brake pad consumption.

Top players in the market include Brembo S.p.A., ADVICS Co., Ltd., Akebono Brake Industry Co., Ltd., Robert Bosch Gmbh, Hitachi Astemo, Ltd., and ZF Group.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 287

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us