Battery Electrolyte Market Size, Share & Industry Analysis, By Battery Type (Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, and Others), By Electrolyte Form (Liquid Electrolytes, Gel, and Solid-State Electrolytes), By Application (Electric Vehicles (EVs), Energy Storage Systems, Consumer Electronics, Industrial & Motive Batteries, and Others), and Regional Forecast, 2026-2034

Battery Electrolyte Market Size and Future Outlook

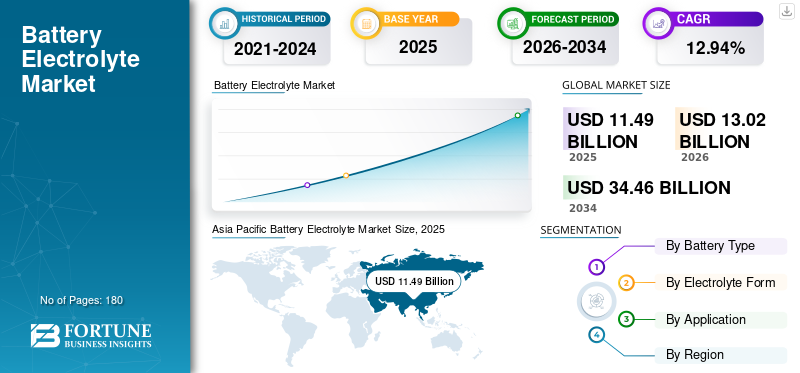

The global battery electrolyte market size was valued at USD 11.49 billion in 2025. The market is expected from reach USD 13.02 billion by 2026 USD 34.46 billion by 2034, exhibiting a CAGR of 12.94% during the forecast period. Asia Pacific dominated the battery electrolyte market with a market share of 42.38% in 2025.

A battery electrolyte is an ion-conducting medium, typically a liquid, gel, or solid, that facilitates the movement of charge-carrying ions between the cathode (positive) and anode (negative) electrodes. It ensures that electrical current flows to power devices, vehicles, or battery energy storage systems. The surge in EV production, driven by government emissions regulations and consumer demand, requires massive volumes of high-performance electrolytes for lithium-ion batteries.

- According to the International Energy Agency, China dominates the battery supply chain, controlling most cell production and key materials, while mineral extraction and processing remain highly concentrated. Volatile prices highlight the need for greater investment and diversification as demand for battery electrolytes

Tinci Materials dominates the global market as the undisputed leader and maintains a significant competitive edge through vertical integration, including raw material self-supply (lithium hexafluorophosphate) and leading production capacity in LiFSI. The prominent, influential players contributing significantly to market capacity and technology include Soulbrain (widely used by Samsung SDI), and Japanese giants Mitsubishi Chemical Group and UBE Corporation.

Asia Pacific holds the largest market share in terms of revenue, together with Japan and South Korea, these nations form the hub for both production and consumption.

Download Free sample to learn more about this report.

Battery Electrolyte Market Takeaways

- 2025 Market Size: USD 11.49 billion

- 2026 Market Size: USD 13.02 billion

- 2034 Forecast Market Size: USD 34.46 billion

- CAGR: 12.94% from 2026–2034

- Asia Pacific dominated the battery electrolyte market with a market share of 42.38% in 2025.

- Lithium-ion electrolytes dominated the market with a share of 75.4% in 2025.

- Liquid electrolytes dominated the market with a revenue share of 86.3% in 2025.

Asia Pacific

Asia Pacific held the dominant battery electrolyte market share in 2025, valued at USD 4.87 billion, and also took the leading share in 2026 with USD 5.59 billion.

North America

North America was valued at USD 2.51 billion in 2025, securing the position of the second-largest market.

Europe

Europe reached a valuation of USD 2.18 billion in 2025 and is projected to record a growth rate of 11.20% in the coming years.

U.S.

The U.S. market was valued at USD 2.17 billion in 2025, accounting for roughly 18.93% of the global market size.

Japan

The Japan market was valued at USD 0.56 billion in 2025, accounting for approximately 4.87% of global revenues.

Read More

BATTERY ELECTROLYTE MARKET TRENDS:

Shift Toward LFP and Cost-optimized Electrolyte Formulations is Shaping Market Trends

The battery electrolyte market is increasingly shaped by the shift toward lithium iron phosphate (LFP) chemistries and cost‑optimized formulations. As automakers and energy‑storage developers prioritize affordability, safety, and cycle life, LFP‑based cells are displacing higher‑nickel cathodes, prompting electrolyte suppliers to tailor salts, solvents, and additives specifically for LFP’s lower‑voltage, iron‑based system.

At the same time, manufacturers are streamlining electrolyte recipes, reducing expensive components such as LiPF₆, simplifying additive packages, and leveraging scale and process optimization to lower material and production costs without sacrificing performance. This dual trend toward LFP‑compatible and cost‑optimized electrolytes is becoming a key lever for cutting cell‑level battery prices and expanding deployment in EVs and grid‑scale storage.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Rapid Growth in Electric Vehicle Production is Driving Market

A rise in electric vehicle (EV) production is a primary driver of expansion in the battery electrolyte market growth. As global EV sales surge, demand for lithium‑ion cells rises in parallel, directly increasing demand for electrolyte salts, solvents, and additives. Automakers are scaling gigafactories and diversifying chemistries, including LFP and NMC (Nickel Manganese Cobalt), which require tailored electrolyte formulations to meet performance, safety, and cost targets. This volume‑driven ramp‑up forces electrolyte suppliers to invest in larger‑scale manufacturing, raw‑material sourcing, and formulation innovation, making EV‑linked cell production one of the most important growth levers for the electrolyte Market over the next decade.

- According to the International Energy Agency, global electric car production is growing rapidly, reaching 17.3 million vehicles in 2024, about 25% more than in 2023. The International Energy Agency expects this trend to continue, with sales exceeding 20 million in 2025. China leads the market, producing over 70% of the world’s EVs, and already accounts for one in every five cars sold globally in 2023.

MARKET RESTRAINTS:

High Volatility in Lithium Salt and Solvent Prices to Restrain Market Growth

High volatility in lithium‑salt and solvent prices acts as a key restraint on the market. Sharp swings in LiPF₆, lithium carbonate, and key organic solvents such as EC and DMC create uncertainty in raw‑material costs, compressing margins for electrolyte producers and complicating long‑term pricing agreements with cell makers. These price fluctuations also discourage investment in capacity expansion and formulation R&D, since sudden raw‑material spikes can erode returns or collapse. As a result, electrolyte manufacturers must balance cost‑pass‑through mechanisms, hedging strategies, and vertical integration, which in turn, slows the pace at which the market can scale in line with booming lithium‑ion demand.

MARKET OPPORTUNITIES:

Commercialization of Solid-state Battery Electrolytes is Expected to Create Lucrative Opportunities

The commercialization of solid‑state battery electrolytes represents a major market opportunity. As automakers and cell producers push for higher‑energy‑density, safer, and longer‑lived batteries, solid‑state electrolytes, ceramic, sulfide, or polymer‑based, offer a pathway to replace conventional liquid systems. This shift opens new revenue streams for electrolyte suppliers to develop and scale novel solid‑state materials, manufacturing processes, and interface‑engineering solutions. Early‑mover companies can capture premium‑priced, low‑volume applications such as premium EVs and specialty electronics. At the same time, longer‑term mass-market adoption could redefine the structure and value chain of the entire electrolyte industry.

MARKET CHALLENGES:

Rapid Technology Evolution and Uncertainty May Create Challenges for Market Growth

Rapid technology evolution and uncertainty pose a significant challenge for the market. Frequent shifts in cell chemistry, form factor, and performance targets, such as the move toward higher‑nickel cathodes, LFP dominance, and solid‑state architectures, require electrolyte suppliers to adapt formulations, additives, and manufacturing processes constantly.

This fast‑paced innovation increases R&D costs and risks, as investments in one electrolyte platform may become obsolete if the industry converges on a different technology path. At the same time, unclear regulatory, safety, and recycling standards add further uncertainty, making long‑term planning and capital allocation difficult for electrolyte producers trying to align with evolving battery‑technology roadmaps.

Segmentation Analysis

By Battery Type

Lithium-ion Electrolytes Dominated Market Due to High Demand in Various End-Use Industries

Based on battery type, the market is classified into Lithium-ion Electrolytes, Lead-acid Electrolytes, Flow Battery Electrolytes, and others.

In 2025, Lithium‑ion electrolytes dominated the market with a share of 75.4% due to the rapid expansion of the Electric Vehicle (EV) market, the need for high-performance batteries (longer range, faster charging), and growing grid-scale Energy Storage Systems (ESS). Increased safety requirements, advancements in solid-state/high-voltage electrolytes, and supportive government policies for green energy are further accelerating market growth.

Flow battery electrolytes are registering a significantly higher growth rate, driven by demand for long‑duration grid‑scale storage and the scalability of redox‑flow systems, positioning them as an increasingly important segment within the broader electrolyte landscape.

By Electrolyte Form

Liquid Electrolytes Led Market Due to Their Established Manufacturing

Based on electrolyte form, the market is classified into liquid electrolytes, gel, and solid-state electrolytes.

In 2025, the liquid electrolytes segment dominated the market, with a revenue share of 86.3%, underpinning the vast majority of commercial lithium‑ion cells used in EVs, consumer electronics, and stationary storage. Their established manufacturing infrastructure, performance familiarity, and cost‑effectiveness support continued leadership.

Solid‑state electrolytes are exhibiting a significant CAGR of 16.18%, driven by the push for safer, higher‑energy‑density batteries and the ongoing commercialization of solid‑state and semi‑solid architectures, which are gradually expanding their share of the electrolyte value chain.

By Application

Electric Vehicles (EVs) Segment Led Market Owing to Large-scale Production

Based on application, the market is classified into electric vehicles (EVs), energy storage systems, consumer electronics, industrial & motive batteries, and others.

In 2025, Electric vehicles (EVs) dominated the market with a share of 60.3%, accounting for the largest share of lithium‑ion cell demand and driving most of the volume for liquid electrolytes. Key drivers include the need for higher energy density, faster charging, improved safety, and the shift towards advanced formulations like solid-state electrolytes.

Energy storage systems, including grid‑scale and residential storage, are registering a CAGR of 12.87%, supported by renewable‑energy integration, policy incentives, and falling battery costs. This dual‑track expansion positions EVs as the incumbent driver while ESS emerges as a key growth engine for future electrolyte demand and formulation innovation.

To know how our report can help streamline your business, Speak to Analyst

Battery Electrolyte Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific held the dominant battery electrolyte market share in 2025, valued at USD 4.87 billion, and also took the leading share in 2026 with USD 5.59 billion. Countries such as China, Japan, South Korea, and India host major cell‑production hubs and EV programs, which directly boost demand for liquid and emerging solid‑state electrolytes. Expanding energy storage deployments and continuous investment in battery‑supply‑chain infrastructure further reinforce the region’s position as the largest and fastest‑growing electrolyte market globally.

Asia Pacific Battery Electrolyte Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Battery Electrolyte Market

The China market in 2025 was valued at USD 2.88 billion, accounting for roughly 25.03% of the global revenues. China’s market is driven by massive domestic EV adoption, world‑leading lithium‑ion cell production, and strong government support for electrification and clean energy. Expanding gigafactories, rising energy‑storage deployments, and continuous R&D in advanced electrolyte formulations further reinforce China’s position as the largest and fastest‑growing electrolyte market globally.

India Battery Electrolyte Market

India’s market is projected to be one of the largest worldwide, with 2025 revenues valued at around USD 0.52 billion, representing approximately 4.48% of the global market.

Japan Battery Electrolyte Market

The Japan Market in 2025 was valued at USD 0.56 billion, accounting for approximately 4.87% of global revenues.

Europe

Europe is projected to record a growth rate of 11.20% in the coming years, which is the third highest among all regions, and reached a valuation of USD 2.18 billion in 2025. Europe’s market is characterized by strong growth, driven by rapid EV adoption, expanding gigafactories, and rising energy‑storage deployments. Stringent environmental regulations and a push for localized, sustainable battery supply chains further support demand for advanced lithium‑ion and emerging solid‑state electrolyte formulations across the region.

Germany Battery Electrolyte Market

The German market in 2025 was valued at USD 0.59 billion. It is projected to reach USD 0.65 billion by 2026, representing approximately 4.85% of the global revenues.

North America

North America was valued at USD 2.51 billion in 2025, securing the position of the second-largest market. North America’s market is growing steadily, driven by EV adoption, grid‑scale energy storage, and new gigafactories, supported by policy incentives and a push for domestic, sustainable battery supply chains.

U.S. Battery Electrolyte Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 2.17 billion in 2025, accounting for roughly 18.93% of the global market size. The market is fueled by EV production, energy‑storage deployments, and domestic gigafactory investments backed by federal incentives and a growing focus on secure, localized supply chains.

Latin America

Latin America is expected to witness moderate growth during the forecast period. The Latin America market was valued at USD 0.73 billion in 2025, driven by rising EV adoption, expanding lithium‑ion deployments in consumer electronics, and growing grid‑scale energy storage projects. Brazil leads regional demand, supported by industrial capacity and policy incentives, while the broader region benefits from abundant lithium resources and increasing investments in local battery‑material supply chains.

Brazil Battery Electrolyte Market

Brazil's market was valued at USD 0.35 billion in 2025, accounting for a very minor share of the global market.

Middle East & Africa

The Middle East & Africa region is expected to witness significant growth during the forecast period. The Middle East & Africa market reached a valuation of USD 1.21 billion in 2025. Countries such as Saudi Arabia, the UAE, South Africa, and Egypt are leading regional demand, supported by government initiatives, renewable‑energy programs, and new lithium‑exploration and battery‑manufacturing projects that are gradually strengthening the local electrolyte‑supply ecosystem.

GCC Battery Electrolyte Market

The GCC market was valued at USD 0.59 billion in 2025, accounting for around 2.00% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players:

Vendors are Actively Expanding Their Market Shares through Partnerships, Business Expansion, and Technological Advancements

The global battery electrolyte market is fragmented, with prominent players in the battery industry including Tinci Materials, CAPCHEM, Soulbrain, Mitsubishi Chemical Group, Central Glass, UBE Corporation, and others. For instance, in December 2025, Neogen Ionics and Japan’s Morita formed an Indo‑Japan JV, Neogen Morita New Materials, to produce solid LiPF₆ battery‑salt in India, diversifying supply chains from China and supporting Aatmanirbhar Bharat through local high‑quality electrolyte‑salt manufacturing.

LIST OF KEY BATTERY ELECTROLYTE COMPANIES PROFILED:

- Tinci Materials (China)

- CAPCHEM (Shenzhen Capchem Technology) (China)

- Soulbrain (South Korea)

- Mitsubishi Chemical Group (Japan)

- Central Glass (Japan)

- UBE Corporation (Japan)

- BASF (Germany)

- LG Chem (South Korea)

- Dongwha Electrolyte (South Korea)

- Morita Chemical Industries (Japan)

- Zhejiang Yongtai Technology (China)

- Shanshan Technology (China)

- Targray (Canada)

KEY INDUSTRY DEVELOPMENTS:

- January 2026: Idemitsu Kosan announced the development of a large‑scale pilot plant in Chiba, Japan, to produce solid electrolytes for all‑solid‑state lithium‑ion batteries, supporting Toyota’s plan to launch EVs with such batteries by 2027–2028 and advancing commercial‑scale solid‑state battery deployment.

- January 2026: ProLogium signed an MoU with Delta to jointly develop a next‑generation battery energy management system, combining ProLogium’s solid‑state battery technology with Delta’s power and thermal management expertise to enable safer, high‑efficiency systems for energy and smart‑mobility applications.

- November 2025: Asahi Kasei licensed its acetonitrile‑based high ionic conductivity electrolyte to EAS Batteries for a new ultra‑high‑power LFP cell, enabling higher power output, improved low‑temperature performance, extended cycle life, and operation at higher voltage for demanding mobility and industrial applications.

- November 2025: LG Energy Solution partnered with U.S. startup South 8 Technologies to co‑develop space‑rated lithium‑ion batteries using liquefied gas electrolyte, enabling operation down to −60 °C for extreme‑environment aerospace missions, with KULR Technology and NASA also involved in the program.

- October 2025: Samsung SDI, BMW, and Solid Power collaborated to jointly validate all‑solid‑state battery cells, with Samsung SDI supplying ASSB cells using Solid Power’s solid electrolyte and BMW developing modules and packs for next‑generation EV evaluation vehicles.

REPORT COVERAGE

The global battery electrolyte market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and Liquid Nitrogen industry trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market report also includes a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

REPORT Scope & segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.94% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Battery Type, Electrolyte Form, Application, and Region |

|

By Battery Type |

· Lithium-ion Electrolytes · Lead-acid Electrolytes · Flow Battery Electrolytes · Others |

|

By Electrolyte Form |

· Liquid Electrolytes · Gel · Solid-State Electrolytes |

|

By Application |

· Electric Vehicles (EVs) · Energy Storage Systems · Consumer Electronics · Industrial & Motive Batteries · Others |

|

By Region |

· North America (By Battery Type, By Electrolyte Form, By Application, and Country) o U.S. (Application) o Canada (Application) · Europe (By Battery Type, By Electrolyte Form, By Application, and Country) o U.K. (Application) o Germany (Application) o France (Application) o Italy (Application) o Spain (Application) o Rest of Europe (Application) · Asia Pacific (By Battery Type, By Electrolyte Form, By Application, and Country) o China (Application) o India (Application) o Japan (Application) o South Korea (Application) o Rest of Asia Pacific (Application) · Latin America (By Battery Type, By Electrolyte Form, By Application, and Country) o Brazil (Application) o Mexico (Application) o Rest of Latin America (Application) · Middle East & Africa (By Battery Type, By Electrolyte Form, By Application, and Country) o GCC (Application) o South Africa (Application) o Rest of Middle East & Africa (Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.49 billion in 2025 and is projected to reach USD 34.46 billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 4.87 billion.

The market is expected to exhibit a CAGR of 12.94% during the forecast period of 2026-2034.

By application, the electric vehicles (EVs) segment led the market.

Rapid growth in electric vehicle production is driving the market.

Tinci Materials, CAPCHEM, Soulbrain, Mitsubishi Chemical Group, Central Glass, and UBE Corporation are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us