Drill Pipe Market Size, Share & Industry Analysis, By Grade (API and Premium), By Application (Onshore and Offshore), and Regional Forecast, 2026-2034

Drill Pipe Market Overview

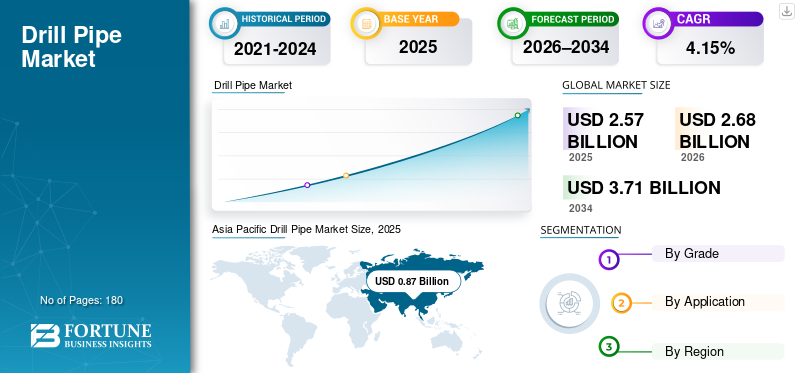

The global drill pipe market size was valued at USD 2.57 billion in 2025 and is expected to reach USD 2.68 billion by 2026. The market is projected to reach USD 3.71 billion by 2034, exhibiting a CAGR of 4.15% during the forecast period of 2026-2034. Asia Pacific dominated the drill pipe market with a market share of 33.85% in 2025.

Asia Pacific holds the largest share in terms of revenue, driven by rapid and ongoing unconventional oil and gas exploration, specifically in shale plays, horizontal drilling, and hydraulic fracturing. The region's, particularly China and India's, heavy investments in drilling technology and infrastructure have solidified this leadership.

- In January 2026, Kuwait Oil Company (KOC) awarded Egypt Drilling Company (EDC) a landmark onshore drilling contract for a 1,500-horsepower rig, marking the first time an Egyptian firm secured such a deal with KOC. Operations will commence in early 2027, leveraging EDC's Kuwait branch and top safety performance to expand its regional footprint.

Drill pipe is a high-strength, hollow, seamless steel or aluminum pipe used in oil and gas drilling to connect surface equipment to the bottom-hole assembly. It facilitates drilling by rotating the bit, supporting the string weight, and circulating drilling fluid (mud). Demand is primarily driven by rising offshore, deepwater, and unconventional (horizontal/shale) drilling, along with increased global investments in energy exploration and enhanced oilfield technologies.

Tenaris S.A. is a leading global manufacturer and supplier of steel pipes and related services for the energy industry, holding a significant, dominant position in the drill pipe market. Furthermore, Key players such as Vallourec, TMK Group, Sumitomo Corporation, Nippon Steel Corporation, ArcelorMittal, and others in this space focus on providing high-strength, API-compliant drill pipe for onshore and offshore drilling, with significant activity in North America, Europe, and Asia.

Download Free sample to learn more about this report.

DRILL PIPE MARKET Key Takeaways

- 2025 Market Size: USD 2.57 Billion

- 2026 Market Size: USD 2.68 Billion

- 2034 Forecast Market Size: USD 3.71 Billion

- CAGR: 4.15% from 2026–2034

- Asia Pacific dominated the drill pipe market with a 33.85% share, generating USD 0.66 billion in 2025.

- The onshore segment held the largest market share in 2025 due to established infrastructure and cost-efficient drilling operations.

- The API grade segment dominated the market in 2025 owing to its standardized reliability, cost-effectiveness, and widespread adoption in conventional drilling.

North America

North America led the market with USD 0.87 billion in 2025 and is projected to reach USD 0.91 billion in 2026

Asia Pacific

Asia Pacific generated USD 0.66 billion in 2025, supported by strong drilling activity across China, India.

Europe

Europe reached USD 0.40 billion in 2025 and is expected to grow steadily, supported by selective offshore projects and mature basin developments.

U.S.

The drill pipe market reached USD 0.72 billion in 2025.

Japan

The drill pipe market generated USD 0.10 billion in 2025.

Read More

DRILL PIPE MARKET TRENDS

Shift Toward Premium and High-Performance Drill Pipes is Shaping Market Trend

The drill pipe market is undergoing a clear shift toward premium and high-performance variants, driven by the demands of challenging drilling environments such as deepwater, unconventional resources, and extended-reach operations. These advanced pipes feature superior strength, enhanced fatigue resistance, and specialized coatings that boost durability against corrosion, extreme temperatures, and high torque. Innovations such as lightweight alloys, gas-tight connections, and integrated sensor technology enable real-time monitoring, reducing downtime and operational strain.

Manufacturers prioritize hybrid designs and anti-corrosive materials to improve efficiency and longevity, aligning with the industry's focus on safety, cost savings, and precision in complex geological formations.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Global Oil & Gas Exploration and Production (E&P) Activity Drives Market Growth

Rising global oil and gas exploration and production activities are propelling the drill pipe market growth by surging energy demand and advancements in drilling technologies. Operators increasingly target challenging frontiers such as deepwater reservoirs, shale formations, and unconventional resources, necessitating robust drill pipes capable of enduring extreme pressures and harsh conditions. This surge in E&P efforts, particularly in emerging basins across North America, the Middle East, and Asia Pacific, amplifies demand for high-strength, fatigue-resistant pipes with superior torque capacity and corrosion protection.

- In January 2026, Essar Oil and Gas Exploration & Production Ltd plans a USD 100 million investment for a new drilling program at its Raniganj East CBM block in West Bengal, India's largest producer. The initiative includes horizontal wells to boost output, building on prior investments with over 450 wells drilled and extensive pipeline infrastructure, targeting enhanced recovery amid shale potential.

Technological innovations, including premium connections and lightweight composite materials, enhance drilling efficiency, reduce non-productive time, and lower overall costs. As companies prioritize precision and sustainability, the market shifts toward eco-friendly drill pipe manufacturing and recyclable alloys, ensuring reliable performance amid intensified resource extraction.

MARKET RESTRAINTS

High Volatility in Oil & Gas Prices to Restraint Market Growth

High volatility in oil and gas prices poses a significant restraint on drill pipe market growth, creating uncertainty that prompts operators to scale back investments in exploration and production. Fluctuating crude prices lead to project delays or cancellations, particularly in high-cost offshore and unconventional drilling, directly curbing demand for premium drill pipes. Companies adopt cautious strategies, prioritizing cost-cutting measures such as deferred maintenance and reduced rig counts over new equipment purchases.

This price instability disrupts supply chains, squeezes manufacturer margins, and slows innovation in high-performance materials and connections. While short-term hedging offers some relief, prolonged swings deter long-term commitments, shifting focus toward reusable inventory and standardized pipes rather than advanced, specialized solutions tailored for harsh environments.

MARKET OPPORTUNITIES

Growth in Offshore and Gas-Focused Drilling is Expected to Create Lucrative Opportunities

Growth in offshore and gas-focused drilling presents lucrative opportunities for the drill pipe market, as operators expand into deepwater fields and unconventional gas reservoirs worldwide. These complex environments demand specialized drill pipes with exceptional tensile strength, fatigue resistance, and corrosion protection to withstand high pressures, extreme depths, and aggressive sour gas conditions.

- In January 2026, ONGC spudded the stratigraphic well AND-P-1, in the Andaman offshore basin, 267 nautical miles from the Andaman & Nicobar Islands.

Advancements in premium connections, sour service materials, and lightweight alloys enable longer laterals and faster drilling rates, reducing operational risks and costs. Emerging regions such as the Middle East and Asia Pacific offer vast untapped potential, while floating production systems and subsea tiebacks further boost demand for high-performance, gas-tight pipes. Strategic partnerships between manufacturers and E&P firms accelerate innovation, positioning the market for sustained expansion amid rising global energy needs.

MARKET CHALLENGES

Logistics and Supply Chain Disruptions Create Challenges for Market Growth

Logistics and supply chain disruptions present formidable challenges, hampering timely delivery and inflating operational costs across global operations. Geopolitical tensions, port congestion, and trade restrictions delay raw material shipments such as specialized steel alloys and premium forgings, forcing manufacturers into production bottlenecks and inventory shortages.

Transportation hurdles in remote drilling sites, coupled with volatile freight rates and container scarcities, exacerbate lead times for heavy, oversized pipes essential for offshore and deepwater projects. These interruptions strain E&P budgets, prompting operators to postpone rig mobilizations and well completions. Additionally, fluctuating energy costs and labor shortages compound vulnerabilities, pushing industry players toward regional sourcing and stockpiling strategies despite higher expenses, ultimately slowing market expansion and innovation adoption.

Segmentation Analysis

By Grade

To know how our report can help streamline your business, Speak to Analyst

API Segment is Dominant Due to High Compatibility

Based on grade, the market is classified into API and premium. In 2025, API specifications dominated with a substantial drill pipe market share by providing standardized reliability for conventional drilling operations worldwide. Their widespread adoption ensures compatibility, cost-effectiveness, and proven performance in standard onshore and shallow-water applications.

Premium drill pipes are gaining rapid traction with a CAGR of 6.34% over the forecast period, driven by demands for superior strength and durability in challenging deepwater and high-pressure environments. Enhanced connections and materials promise faster drilling and reduced downtime, positioning this segment for accelerated market expansion.

By Application

Onshore Application Leads Owing to Large-Scale Conventional Oil and Gas Extraction

Based on application, the market is classified into onshore and offshore. In 2025, the onshore segment dominated the global market by leveraging established infrastructure and cost efficiencies in accessible terrains worldwide. Its reliability suits conventional oil and gas extraction, maintaining a steady demand for standard pipes.

Offshore drilling is poised for rapid growth with CAGR of 3.30% over the analysis period, fueled by deepwater explorations and advanced subsea technologies. Specialized high-strength pipes enable complex operations, promising expanded market share amid rising global energy pursuits.

Drill Pipe Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Asia Pacific Drill Pipe Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2025, valued at USD 0.87 billion, and is anticipated to hold the leading share in 2026 with USD 0.91 billion. North America remains the most technology-intensive drill pipe market, driven by high rig productivity and complex well designs that demand higher fatigue resistance and premium connections.

U.S. Drill Pipe Market

The U.S. in 2025 reached around USD 0.72 billion, accounting for roughly 82.95% of the global drill pipe revenues. The U.S. dominates regional demand because shale drilling requires long horizontal laterals, frequent tripping, and high torque, which accelerates drill pipe wear and replacement cycles.

Europe

Europe is projected to record a growth rate of 3.20% in the coming years, which is the third highest among all regions, and reached a valuation of USD 0.40 billion by 2025. Europe’s drill pipe demand is comparatively smaller and more project-driven, shaped by a declining onshore footprint and selective offshore activity in mature basins.

Germany Drill Pipe Market

The German market in 2025 hit USD 0.07 billion representing approximately 2.57% of the global revenues.

Asia Pacific

Asia Pacific reached USD 0.66 billion by 2025, securing the second-largest market share. Asia Pacific is a diverse drill pipe market with demand split across large national oil companies, emerging exploration programs, and mature producing regions with ongoing development drilling. China is a major volume center, supported by sustained onshore drilling and efforts to improve energy security, creating consistent baseline demand for both API and premium grades.

China Drill Pipe Market

China is projected to be one of the largest markets worldwide, achieving USD 0.27 billion in 2025, representing approximately 10.43% of the global market.

India Drill Pipe Market

India’s market is projected to be one of the largest, with 2025 revenues hitting USD 0.18 billion, representing approximately 7.13% of the global market.

Japan Drill Pipe Market

In 2025, Japan captured USD 0.10 billion, accounting for approximately 3.78% of global revenues.

Latin America

Latin America reached a valuation of USD 0.28 billion in 2025 and is expected to witness moderate growth during the forecast period. The region’s drill pipe market is anchored by offshore and deepwater activity in certain countries, where premium drill pipe demand can be disproportionately high versus volume.

Brazil Drill Pipe Market

Brazil's is projected to reach approximately USD 0.20 billion by 2025, accounting for roughly 8.14% of the global market.

Middle East & Africa

The Middle East & Africa achieved USD 0.33 billion in 2025 and is anticipated to register significant growth during the forecast period. The region witnesses high-volume drilling activities with sustained development programs that create consistent demand for drill pipes across a wide range of well types. National oil companies often drive procurement through long-term contracts and qualification systems, emphasizing reliability, standardization, and lifecycle support.

GCC Drill Pipe Market

The GCC market captured USD 0.26 billion by 2025, accounting for around 10.15% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors are Actively Expanding their Market Share through Partnerships, Business Expansion, and Technological Advancements

The market has a fragmented structure, comprising prominent players such as Vallourec, TMK Group, Sumitomo Corporation, Nippon Steel Corporation, ArcelorMittal, and others. In September 2025, Vallourec secured a major contract from Petrobras through competitive bidding to supply OCTG products and services for offshore operations from 2026 to 2029, potentially worth up to USD 1 billion. Such developments are expected to fuel market growth over the forecast period.

LIST OF KEY DRILL PIPE COMPANIES PROFILED

- Vallourec (France)

- Tenaris (Luxembourg)

- NOV – National Oilwell Varco (U.S.)

- TMK Group (Russia)

- Sumitomo Corporation (Japan)

- Nippon Steel Corporation (Japan)

- ArcelorMittal (Luxembourg)

- Jiangsu Changbao Steel Tube Co., Ltd. (China)

- Tianjin Pipe Corporation – TPCO (China)

- Hilong Group (China)

- DP Master Manufacturing (U.S.)

- Oil Country Tubular Limited – OCTL (India)

- Seah Steel Corporation (South Korea)

- United Drilling Tools Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Halliburton launched the StreamStar wired drill pipe interface system on October 30, 2025, revolutionizing drilling with continuous surface power and real-time data for closed-loop automation. It minimizes downhole batteries, enables instant two-way communication for precise geosteering, and integrates with iStar and LOGIX platforms to boost efficiency and reduce well construction time.

- June 2025: SLB announced a strategic collaboration with Cactus Drilling to scale automated and autonomous drilling solutions across U.S. land rigs. Cactus will integrate SLB's DrillSync platform with Precise controls, DrillOps AI automation, and Neuro for self-learning directional drilling, enhancing efficiency, safety, and real-time data insights.

- January 2025: Vår Energi awarded Reelwell a multi-year contract for DualLink powered wired drill pipe technology, with Odfjell Technology as partner, marking its first Norwegian Continental Shelf deployment. The system provides real-time telemetry and downhole power, enhancing drilling efficiency, precision, and sustainability by cutting emissions on the COSLPioneer rig.

- December 2024: Odfjell Technology and Reelwell signed a strategic cooperation to deploy Dual Link digital pipe technology, integrating real-time telemetry, downhole power, and analytics for superior drilling efficiency. Odfjell handles offshore operations while Reelwell supplies the platform, enhancing safety, well placement, and performance in the North Sea and beyond.

- August 2024: GA Drilling partnered with Petrobras and its Cenpes R&D center to develop a next-generation downhole anchoring and drive system for autonomous reeled drilling. This innovation replaces conventional drill pipes with continuous tubing, enabling deep offshore wells from lighter intervention vessels to cut costs, boost efficiency, reduce risks, and support geothermal applications through real-time telemetry and downhole control.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.15% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Grade, Application, and Region |

|

By Grade |

· API · Premium |

|

By Application |

· Onshore · Offshore |

|

By Geography |

· North America (By Grade, By Application, and Country) o U.S. (Application) o Canada (Application) · Europe (By Grade, By Application, and Country) o U.K. (Application) o Germany (Application) o France (Application) o Italy (Application) o Spain (Application) o Rest of Europe (Application) · Asia Pacific (By Grade, By Application, and Country) o China (Application) o India (Application) o Japan (Application) o South Korea (Application) o Rest of Asia Pacific (Application) · Latin America (By Grade, By Application, and Country) o Brazil (Application) o Mexico (Application) o Rest of Latin America (Application) · Middle East & Africa (By Grade, By Application, and Country) o GCC (Application) o South Africa (Application) o Rest of the Middle East & Africa (Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.57 billion in 2025 and is projected to reach USD 3.71 billion by 2034.

In 2025, North Americas market value stood at USD 0.87 billion.

The market is expected to exhibit a CAGR of 4.15% during the forecast period of 2026-2034.

The onshore sector is the leading application segment in the market.

Rising oil & gas exploration and production activity is a key aspect for market’s growth.

Vallourec, TMK Group, Sumitomo Corporation, Nippon Steel Corporation, ArcelorMittal, and others are some of the prominent players in the market.

North America dominated the market in 2025 by holding the largest share.

Growth in offshore and gas-focused drilling presents lucrative opportunities for the drill pipe market, as operators expand into deepwater fields and unconventional gas reservoirs worldwide. These complex environments demand specialized drill pipes with exceptional tensile strength, fatigue resistance, and corrosion protection to withstand high pressures, extreme depths, and aggressive sour gas conditions.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us