E-learning Services Market Size, Share & Industry Analysis, By Type (Custom E-learning, Responsive E-learning, Rapid E-learning, Micro E-learning, and Others (Translation & Localization, Game-based Learning, etc.)), By Learning Method (Blended Learning, Mobile Learning, and Virtual Classrooms), By Technology (Artificial Intelligence, Cloud Computing, and Augmented Reality and Virtual Reality), By End Use (Academic, Corporate, and Government), and Regional Forecast, 2026-2034

E – Learning Services Market Size

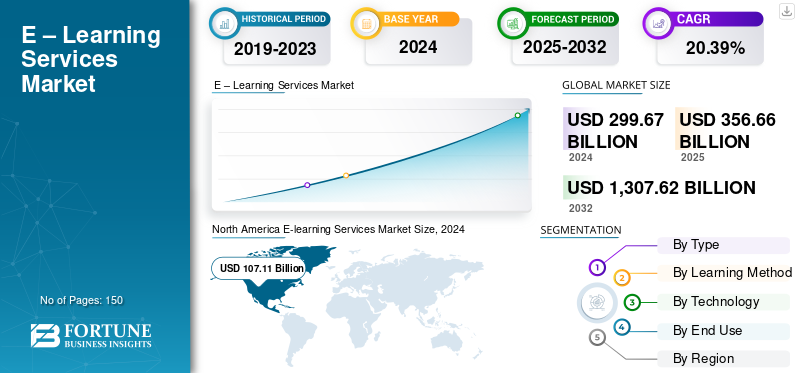

The global e-learning services market size was valued at USD 356.66 billion in 2025. The market is projected to grow from USD 426.39 billion in 2026 to USD 1,713.97 billion by 2034, exhibiting a CAGR of 18.99% during the forecast period. North America dominated the e-learning services market with a market share of 35.12% in 2025.

E-learning services offer education and training through digital technologies on virtual and online platforms by using tools such as interactive videos, simulations, and online courses to deliver learning remotely. These services include a variety of topics, including academic subjects, professional development, corporate training and skill development. E-learning is a versatile tool which appeals to students, professionals, and organizations.

Technological advancements, increased availability of the internet and smartphones, and the growing need for flexible and accessible learning are key drivers for the demand for e-learning services. Trends such integration of AI, virtual reality, and microlearning are driving new opportunities for market growth.

The top firms in the industry are Accenture, Infosys, Wipro, NIIT Ltd., Udemy, Inc., Coursera and AllenComm.

Download Free sample to learn more about this report.

Impact of Gen AI

Generative AI Transforms Market with Development, Delivery, and Optimization of Educational Content

The e-learning services market is experiencing tremendous growth with the advent of Generative AI, which is transforming the mechanisms regarding the development, delivery, and optimization of educational content. It automates basic tasks such as course generation, translation, customization, and learner evaluation, resulting in a quicker turnaround and improved quality and production with reduced expenses. Through behavior and preferences analysis, AI systems create adaptive learning attempts with a higher degree of engagement and retention. Scalability and data-driven training solutions can be used to serve the needs of institutions and organizations by creating reduced manual workload and improving access to training in a wide range of languages and skill levels. The key element in this integration of AI is to speed up the innovation and competitiveness at the level of global learning ecosystem.

MARKET DYNAMICS

Market Drivers

Growing Need of Workforce Upskilling & Reskilling Pressure Drives Market Growth

The market of e-learning services is characterized by notable growth mainly because of the rising demand for workforce upskilling and reskilling in the context of industries. With the ever-changing business processes that are being shaped by emerging technologies including artificial intelligence, automation, and advanced analytics, businesses are under constant pressure to increase the abilities of their employees. The e-learning platforms provide scalable, flexible and less expensive training modules that close the skill gaps and facilitate lifelong learning. Organizations are not only using digital learning as a means of increasing productivity but also as a strategic investment to keep up with the rapidly changing job environment brought about by digital transformation.

Market Restraints

Budget Constraints and ROI Scrutiny to Hinder Growth

Although there is an increasing use of digital learning solutions, a constraint in investment in e-learning services is the issue of costs and the perceived low returns that can be realized through the budget-based approach. Many organizations, particularly small and medium enterprises, hesitate to spend large amounts of money on training initiatives without clear performance measures. The need to demonstrate actual learning outcomes, productivity increases, and improved employee retention puts pressure on the service provider to prove its value propositions. The process of ROI questioning, therefore, slows down procurement processes and limits the implementation of major-scale implementation of the other advanced e-learning projects particularly in cost-sensitive sectors or when the economy is slowing down.

Market Opportunities

Rising Popularity of Immersive Learning for High-Stakes Training Create Opportunities

The emerging opportunities in the market of e-learning services are promising in relation to the rapid improvements in the development of immersive technologies such as virtual reality (VR), augmented reality (AR), and mixed reality (MR). High-stakes industry organizations are rapidly embracing the use of simulation-based training in skill-intensive and safety-critical tasks of the companies such as healthcare, manufacturing, aerospace, and energy. These simulation-based learning systems facilitate experiential learning that is free of operational risks, better retention of knowledge, and skills application. The service providers that provide AR/VR-enabled content and situation-based learning platforms will capture a large market as businesses worldwide seek new training tools to enhance performance in the real world and improve learning outcomes.

E-LEARNING SERVICES MARKET TRENDS

Growing Demand for Hybrid and Remote Work Emerges as a Major Trend

The continuation of the hybrid and remote work model has become a characteristic trend, increasing the demand for e-learning services. Digital-first training has been necessary in the continued need to develop consistent skills and organizational culture, as organizations continue to manage geographically dispersed teams. Using e-learning sites allows effective access to personalized content, collaborative instructional aids, and performance observation irrespective of the site. This shift to a hybrid work environment also increases the use of cloud-based learning management systems (LMS) and microlearning modules to sustain the learning process, maintain workforce unity, and enhance efficiency in decentralized corporate ecosystems.

SEGMENTATION ANALYSIS

By Type

Increasing Demand for Tailored Digital Training Solutions Boosts Custom E-learning Segment Growth

Based on the type, the market is segmented into custom e-learning, responsive e-learning, rapid e-learning, micro e-learning, and others (translation & localization, game-based learning, etc.)).

The custom e-learning segment held the largest revenue share of USD 138.47 billion in the overall global market in the year 2026. The segment’s growth is attributable to enterprises’ increasing demand for tailored digital training solutions aligned with their specific workflows, branding, and compliance needs. This factor is driving higher spend on bespoke content development over standardized modules.

Of all the segments, micro e-learning holds the highest CAGR of 23.54% in the global market. The segment’s growth is attributable to high preference of organizations and learners toward short, focused, mobile-friendly modules that support just-in-time learning, faster skill updates, and higher engagement in hybrid work environments.

By Learning Method

Blended Learning Segment Dominates Market Owing to Increasing Adoption of Hybrid Training Models

Based on learning method, the market is divided into blended learning, mobile learning, and virtual classrooms.

The blended learning segment dominates with a market share of USD 191.26 billion in 2026. The segment’s growth is mainly because organizations adopt hybrid training models that combine digital flexibility with instructor-led engagement to improve learning outcomes and ROI.

Mobile learning segment has the maximum CAGR of 21.90% in the global industry. The segment’s growth is mainly due to the widespread use of smartphones, improved connectivity, and demand for anytime–anywhere learning drive organizations to deliver training through mobile-first, bite-sized content formats.

By Technology

Cost-Effective and Easily Deployable E-Learning Solutions Augments the Cloud Computing Segment Growth

Based on the technology, the market is divided into artificial intelligence, cloud computing, and augmented reality and virtual reality.

The cloud computing segment accounted for the largest e-learning services market share at USD 309.32 billion in 2026. The segment’s growth is because it enables scalable, cost-effective, and easily deployable e-learning solutions, allowing organizations to deliver, manage, and update content seamlessly across global user bases.

Artificial intelligence represents the largest CAGR at 27.12% in the global market. The segment’s growth is because AI-driven personalization, adaptive learning paths, automated content creation, and analytics significantly enhance learner engagement and training efficiency across e-learning ecosystems.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Workforce Upskilling and Compliance Augments the Corporate Segment Growth

Based on the end use, the market is divided into academic, corporate, and government.

The corporate segment for accounted for the largest market share at USD 252.9 billion in 2026. The segment’s growth is attributable to increasing investments in digital training solutions for workforce upskilling, compliance, and continuous learning to boost productivity and maintain competitive advantage. Corporate segment also represents the largest CAGR at 21.32% in the market.

E-LEARNING SERVICES MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus On Partnerships and Acquisitions to Lead the Industry

The key players in the industry include Accenture, Infosys, Wipro, NIIT Ltd., Udemy, Inc., Coursera and AllenComm. These companies are adopting strategies such as incorporating cutting-edge technologies such as AI, VR, and gamification, expanding their course offerings, and forming strategic partnerships with other firms. Other strategies include focusing on customized learning experiences, leveraging data analytics for personalized learning, and expanding their geographical reach.

LIST OF KEY E-LEARNING SERVICES COMPANIES PROFILED

- Accenture (U.S.)

- Infosys (India)

- Wipro (India)

- NIIT Ltd. (India)

- Udemy, Inc. (U.S.)

- Coursera (U.S.)

- AllenComm (U.S.)

- SweetRush (U.S.)

- Infopro Learning (U.S.)

- Hurix Digital (India)

- Deloitte (U.K.)

- Capgemini (France)

- Learning Technologies Group (U.K.)

- Skillsoft (U.S.)

- GP Strategies (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025- Coursera, Inc., a leading global online learning platform, launched the Skill Tracks, a data-backed learning solution mapped to specific occupations that guides learners from foundational knowledge to expert proficiency through verified skill paths. Powered by Coursera’s Career Graph, which uses millions of labor market data points, third-party competency frameworks, and a proprietary skills taxonomy, Skill Tracks precisely map the relationships between jobs, skills, and learning content, ensuring organizations can close skill gaps quickly.

- May 2025- Udemy, an online learning and skills marketplace, launched Role Play, an artificial intelligence (AI) powered platform that aims to help professionals develop soft skills through simulations.

- March 2025- Infosys, a global leader in next-generation digital services and consulting, announced the launch of Infosys Springboard Makerlab, at the Symbiosis International University, in Pune. The new lab, a first of its kind, will provide young learners with hands-on experience in Science, Technology, Engineering, and Mathematics (STEM) fields, with the aim to help them become more employable. It is open to students from all Symbiosis schools and colleges as well as students from nearby educational institutions.

- December 2024- Accenture launched an on-demand learning program led by Accenture experts and powered by content from Stanford Online, designed to equip business and technology leaders with the knowledge and skills to harness the full potential of generative AI and drive greater business value for their organizations while balancing societal considerations.

- March 2024- Accenture announced the launch of Accenture LearnVantage to provide its clients with comprehensive technology learning and training services that will help them reskill and upskill their people in technology, data and AI to reinvent their organizations and achieve greater business value.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the e-learning services market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 18.99% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

By Learning Method

By Technology

By End Use

By Region North America (By Type, Learning Method, Technology, End Use and Country/Sub-region)

Europe (By Type, Learning Method, Technology, End Use and Country/Sub-region)

Asia Pacific (By Type, Learning Method, Technology, End Use and Country/Sub-region)

South America (By Type, Learning Method, Technology, End Use and Country/Sub-region)

Middle East & Africa (By Type, Learning Method, Technology, End Use and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 356.66 billion in 2025 and is projected to reach USD 1,713.97 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 18.99% during the forecast period.

Growing need of workforce upskilling & reskilling pressure is speeding up the market growth.

Accenture, Infosys, Wipro, NIIT Ltd., and Udemy, Inc. are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 125.26 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us