Electric Fuse Market Size, Share & Industry Analysis, By Voltage (Low, Medium, and High), By End User (Consumer Electronics, Automotive, Industrial, Utilities, Commercial, and Residential), and Regional Forecast, 2026-2034

Electric Fuse Market Size and Future Outlook

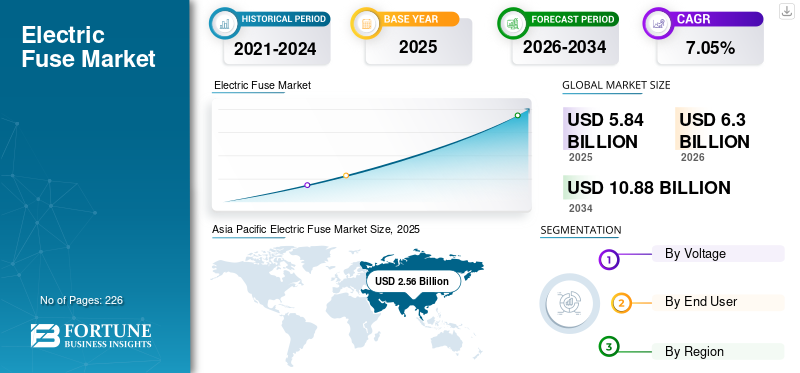

The global electric fuse market size was valued at USD 5.84 billion in 2025. The market is projected to grow from USD 6.30 billion in 2026 to USD 10.88 billion by 2034, with a CAGR of 7.05% over the forecast period. Asia Pacific dominated the electric fuse market with a market share of 43.84% in 2025.

An electric fuse is a fundamental electrical protection device designed to safeguard circuits and equipment from damage caused by overcurrent or short circuits. It operates by melting a calibrated metal element when the current exceeds a safe limit, thereby interrupting the flow of electricity. Electric fuses are widely used across residential, commercial, industrial, automotive, and electronic applications due to their simplicity, reliability, and cost-effectiveness. They are available in various voltage and current ratings, including low-, medium-, and high-voltage types, to suit different power systems. Fuses provide fast fault response and help prevent fire hazards, equipment failure, and safety risks. Despite the emergence of resettable protection devices, electric fuses remain a critical component in electrical safety architectures worldwide.

The growth of the electric fuse market is primarily driven by the rising electrification of residential, commercial, and industrial infrastructure across both developed and emerging economies. Increasing investments in power generation, transmission, and distribution networks, including the integration of renewable energy sources, are boosting demand for reliable circuit protection devices. The rapid expansion of the automotive, electronics, and electric vehicle industries is further accelerating the need for advanced, high-performance fuses. Growth in consumer electronics, appliances, and data centers continues to support steady volume demand, particularly for low-voltage fuses. Additionally, stricter electrical safety regulations and standards are encouraging the replacement of outdated protection systems with compliant fuse solutions. Together, these factors are driving consistent global market expansion.

Littelfuse, Eaton, Schneider Electric, Mersen, and ABB are among the key participants shaping the market. These companies play a pivotal role as a worldwide leader in circuit protection solutions, with a strong focus on electric fuses across low-, medium-, and high-voltage applications. These companies are particularly influential in automotive, electronics, and industrial markets, supplying fuses used in vehicles, electric vehicles, renewable energy systems, and industrial equipment.

Download Free sample to learn more about this report.

Electric Fuse Market Trends

Rising Demand for Application-Specific and High Voltage Fuses is a Key Market Trend

A key trend in the market is the growing demand for application-specific and high-voltage fuse solutions, driven by increasingly complex electrical systems and technological advancements. As power networks become more decentralized, fuse designs are being optimized for solar inverters, wind turbines, battery energy storage systems, and electric vehicle platforms. According to the International Energy Agency (IEA), global electricity demand grew by more than 2.5% in 2023, increasing stress on electrical networks and underscoring the importance of fast-acting, reliable protection devices. Leading manufacturers such as Littelfuse and Mersen recently expanded their product lines for DC and high-voltage applications used in renewable energy and EV charging systems. In parallel, international standards bodies such as the International Electrotechnical Commission (IEC) continue updating fuse safety and performance standards to address higher fault currents and voltage levels. This shift reflects how fuses are evolving from commodity components into engineered safety solutions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Expansion of Power Infrastructure and Electrification to Push the Market Growth

The accelerating expansion of power generation, transmission, and distribution infrastructure is a major driver for the market. Governments and utilities worldwide are investing heavily in grid upgrades to support urbanization, industrial growth, and electrification. The International Renewable Energy Agency (IRENA) reported that more than 500 GW of renewable power capacity was added globally in 2023 alone, significantly increasing the need for overcurrent protection across substations, transformers, and inverter systems. Each new solar or wind installation requires multiple layers of fuse protection to ensure operational safety and grid stability. Additionally, the electrification of heating, industrial processes, and transport is increasing load density across networks. Utilities are responding by modernizing substations and feeder lines, where medium- and high-voltage fuses remain critical components. This sustained infrastructure build-out directly translates into consistent demand for electric fuses across voltage categories.

Market Restraints

Growing Preference for Resettable Protection Devices to Limit the Market Expansion

A key market restraint is the increasing preference for resettable protection devices, such as circuit breakers and electronic protection systems, in specific applications. Commercial buildings, data centers, and industrial facilities often favor resettable solutions as they reduce downtime and eliminate the need for manual fuse replacement after fault events. The International Electrotechnical Commission (IEC) noted growing adoption of intelligent circuit protection systems in smart buildings and automated facilities, particularly in developed markets. As building management systems become more integrated, facility operators increasingly value protection devices that support remote diagnostics and rapid reset. While fuses remain favored for their simplicity, speed, and cost advantages, this shift toward resettable technologies can limit their adoption in applications where operational continuity outweighs upfront costs.

Market Opportunities

Electric Vehicles and Charging Infrastructure to Create New Growth Avenues

The rapid global rollout of Electric Vehicles (EVs) and charging infrastructure presents a strong market opportunity. According to the International Energy Agency (IEA), global EV sales exceeded 14 million units in 2023, sharply increasing demand for specialized fuses used in battery packs, power electronics, onboard chargers, and fast-charging stations. Each EV contains multiple fuse components designed to safely handle high currents and DC voltages. Charging infrastructure expansion further amplifies this opportunity, as DC fast chargers require numerous layers of fuse protection to ensure user and grid safety. Key players such as Littelfuse, Eaton, and TE Connectivity have launched EV-specific fuse solutions to address these requirements. As governments continue to support EV adoption through policy and infrastructure funding, fuse manufacturers are well-positioned to benefit from long-term, application-driven electric fuse market growth.

Market Challenges

Volatility in Raw Material Supply to Limit Market Growth

One of the significant challenges facing the electric fuse industry is volatility in raw material supply, particularly for metals such as copper and silver that are essential for fuse elements and terminals. According to data from the World Bank, global demand for copper surged in 2023 due to renewable energy and EV production, tightening the supply for electrical equipment manufacturers. Fuse producers face cost pressure and procurement uncertainty when material availability fluctuates, especially for high-performance fuses that require precise alloy compositions. Leading manufacturers have acknowledged the need to diversify sourcing and redesign products to optimize material usage. In some cases, longer procurement cycles have delayed deliveries to utilities and industrial customers. These supply-side constraints increase operational risk and complicate long-term production planning, particularly as demand rises simultaneously from multiple electrification-driven industries.

Segmentation Analysis

By Voltage

Expanding Construction Industry to Lead the Low Voltage Segment Growth

Based on voltage, the market is segmented into low, medium, and high.

The low voltage segment accounted for approximately 44.65% of the market share, highlighting its dominance in everyday circuit protection needs, spanning from household panels to vehicle power distribution systems. The low-voltage fuse segment remains the most widely deployed component in the global market, underpinned by its extensive use in residential wiring, commercial buildings, light industrial systems, automotive electrical circuits, and consumer electronics. Their broad applicability is driven by affordability, ease of replacement, and compliance with electrical safety standards, making them indispensable in both established and emerging markets. The expanding construction sector and rising electrification of urban infrastructure in regions such as the Asia Pacific further support sustained demand for low-voltage protection devices.

The high-voltage segment is expected to grow at a CAGR of 7.73% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User Analysis

Surging Automation and Deployment of Smart Manufacturing Technologies to Propel Industrial Segment Growth

Based on end user, the market is segmented into consumer electronics, automotive, industrial, utilities, commercial, and residential.

The industrial segment represents the largest electric fuse market share, accounting for approximately 36.48% share in 2025, with electrical systems used for motors, control panels, transformers, and factory automation requiring reliable protection to prevent damage and downtime. The industrial segment is a cornerstone of the market, driven by the needs of manufacturing plants, process industries, automation equipment, and heavy machinery protection. Industrial fuse usage has expanded alongside the growth of automation and the deployment of innovative manufacturing technologies, as well as increased safety standards governing power distribution in factories. The proliferation of industrial automation and robotics heightens demand for both traditional and smart protection devices across varying voltage levels. The segment’s strong demand is reflected in dedicated reports highlighting its robust market position and steady expansion as industries modernize electrical infrastructure to support digital operations and uptime priorities.

The automotive segment is expected to grow at a CAGR of 8.57% during the forecast period.

Electric Fuse Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Electric Fuse Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market is the largest region, valued at USD 2.56 billion in 2025, accounting for approximately 43.83% of global market revenues. The region dominates the market, driven by rapid industrialization, large-scale infrastructure projects, and robust manufacturing sectors. China is the strongest contributor, supported by expansive power grids and renewable capacity exceeding 600 GW as part of its energy expansion efforts, creating large-volume demand for protective devices, including specialized fuses for solar, wind, and storage systems. India’s electrification programs, smart city initiatives, and growth in rail and commercial infrastructure further amplify regional consumption. Japan and South Korea also contribute through advanced electronics and automotive applications. The region’s combination of utility projects, industrial growth, and consumer electronics demand underpins sustained fuse deployment across voltage classes.

China Electric Fuse Market

China remains the dominant contributor in the Asia Pacific, estimated at USD 1.15 billion in 2025 and set to reach USD 1.25 billion in 2026. It represents a high-volume consumption market due to extensive power infrastructure, manufacturing capacity, and large-scale deployment of solar, wind, and EV ecosystems. Demand spans from low-cost consumer electronics fuses to heavy-duty industrial and utility-grade applications.

India Electric Fuse Market

India was estimated at USD 0.48 billion in 2025 and is expected to reach USD 0.52 billion in 2026. India’s market is driven by electrification programs, expansion of transmission and distribution networks, and growth in residential and commercial construction. Increasing focus on electrical safety standards is gradually shifting demand toward higher-quality protection devices.

Japan Electric Fuse Market

Japan was valued at USD 0.33 billion in 2025 and is likely to reach USD 0.36 billion in 2026. Japan’s market is technology-centric, with strong demand from automotive electronics, robotics, and consumer electronics manufacturing. High reliability requirements and compact electrical designs favor advanced miniature and specialty fuse products.

North America

North America market was valued at USD 1.60 billion in 2025, accounting for approximately 27.33% of the global market. The region’s market is characterized by mature infrastructure, advanced safety standards, and strong replacement demand driven by grid modernization and electrification initiatives. The U.S. and Canada are key markets as utilities upgrade aging substations and distribution networks, while automotive electrification and data center construction further support demand for diverse fuse types. For example, industry data notes consistent demand for high-performance fuse systems tied to smart grid upgrades and renewable projects in states such as California and Texas, reflecting an emphasis on reliability and resilience in critical infrastructure. North America’s focus on advanced technology adoption and stringent electrical codes encourages manufacturers to innovate with high-quality, intelligent protective devices.

U.S. Electric Fuse Market

The U.S. market was estimated at USD 1.38 billion in 2025 and is set to reach USD 1.49 billion in 2026. The U.S. market is driven by grid modernization, large-scale integration of renewables, EV charging infrastructure, and strong demand from industrial automation and data centers. Strict electrical safety standards and replacement demand from aging infrastructure keep fuse consumption consistently high.

Europe

Europe accounted for USD 1.01 billion in 2025, representing approximately 17.38% of global revenues. In Europe, the market is shaped by strict regulatory frameworks, sustainability mandates, and investments in renewable energy integration. Countries such as Germany, France, and the U.K. are leading adopters of advanced protection products as they expand grid capacity and electrify transportation systems. A notable instance is the increased deployment of fuses in offshore wind installations, where European countries expanded renewable capacity and reportedly raised protection device requirements by a significant margin between 2022 and 2024. The region’s focus on energy transition, decarbonization, and electrical safety standards (e.g., IEC/EN compliance) further drives demand for engineered fuse solutions across low-, medium-, and high-voltage applications.

Germany Electric Fuse Market

Germany was estimated at USD 0.26 billion in 2025 and is expected to reach USD 0.28 billion in 2026. The country’s demand for electric fuses is anchored in its advanced manufacturing base, industrial automation, and energy transition initiatives. The high penetration of renewable energy, smart factories, and industrial control systems drives the continuous use of precision and high-reliability fuse solutions.

U.K. Electric Fuse Market

The U.K. market was valued at USD 0.15 billion in 2025 and is projected to reach USD 0.16 billion in 2026. The U.K. market is supported by upgrades in commercial buildings, rail electrification, and renewable energy systems, especially offshore wind. Emphasis on electrical safety compliance and retrofitting of older buildings sustains steady demand for low- and medium-voltage fuses.

Latin America

Latin America accounted for USD 0.42 billion in 2025, or approximately 7.22% of global revenues. The market in Latin America is moderately developed but expanding as governments and utilities focus on grid expansion, reliability, and industrial growth. Brazil and Mexico are notable markets with ongoing infrastructure modernization and electrification, which is increasing demand for protective devices. Urbanization and expanding manufacturing bases in countries such as Chile and Argentina create incremental opportunities for fuse adoption in industrial and commercial installations. While challenges such as logistical constraints and enforcement of electrical standards persist, the region’s electrification initiatives and infrastructure projects continue to drive stable market activity for electric fuses.

Middle East & Africa

The Middle East & Africa were valued at USD 0.25 billion in 2025. In the region, the market is gaining traction on the back of infrastructure expansion, energy diversification, and industrial projects, particularly in the Gulf Cooperation Council (GCC) countries and South Africa. Large initiatives such as Saudi Arabia’s multi-billion-dollar investments in power grid expansion and renewable energy projects require robust protection systems, boosting demand for both medium- and high-voltage fuses. Nigeria’s power sector reforms and transmission expansion programs further illustrate the region’s push toward improved electricity access and system reliability. The combination of oil & gas infrastructure growth, urban mega-projects, and electrification efforts positions the area as an emerging market for engineered protective devices.

GCC Electric Fuse Market

The GCC market was estimated at USD 0.11 billion in 2025 and is set to reach USD 0.12 billion in 2026. The GCC market benefits from large infrastructure projects, power network expansion, and industrial development linked to energy diversification plans. Demand is concentrated in utilities, oil & gas facilities, commercial complexes, and significant residential developments.

Competitive Landscape

KEY INDUSTRY PLAYERS

Industry Players are Focusing on Advanced Circuit Protection and System Integration, Enhancing their Product Portfolio

Littelfuse, Eaton, Schneider Electric, Mersen, and ABB are leading players in the common electric fuse industry, supplying low- and medium-voltage fuses for residential, commercial, and industrial applications. Key players focus on circuit protection solutions such as cartridge fuses, HRC fuses, and distribution fuses used in switchgear and panel boards. Their role extends beyond manufacturing to integrating fuse technology within broader power distribution, safety, and energy management systems, ensuring reliability and compliance with global electrical standards.

For instance; In October 2023, Littelfuse has introduced upgraded 656 (PCB-mounted) and 658 (surface-mounted) fuse blocks designed for 5 × 20 mm fuses with higher current handling capability. Previously rated up to 16 A, the new variants now support 20 A and 30 A ratings, expanding design flexibility for engineers. This enhancement allows electronics designers to accommodate higher current applications while maintaining compact fuse configurations.

List of Top Electric Fuse Companies Profiled

- Littelfuse (U.S.)

- Eaton (Ireland)

- Schneider Electric (France)

- Mersen (France)

- ABB (Switzerland)

- Siemens (Germany)

- Bel Fuse (U.S.)

- TE Connectivity (Switzerland)

- Legrand (France)

- SIBA (Germany)

- Panasonic (Japan)

- Schurter (Switzerland)

- Sensata Technologies (U.S.)

- Fuji Electric (Japan)

- Conquer Electronics (China)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Littelfuse introduced six new automotive current sensors designed to improve efficiency, performance, and safety in electric and hybrid vehicles. These automotive-qualified sensors provide accurate, isolated current measurement for battery management, motor control, and safety applications, using open-loop Hall-effect technology in compact bus-bar-mounted designs. They support both analog and CAN/LIN digital outputs, allowing easy integration into modern EV systems.

- September 2025: Eaton unveiled a new, comprehensive global fuse portfolio designed to support electric vehicles and energy storage systems. These products protect both low- and high-voltage architectures, improving safety and fault isolation in electrified powertrains and grid-connected storage. Eaton showcased these at The Battery Show 2025, highlighting its push into critical components for EV charging and renewable integration.

- July 2025: A New Zealand start-up launched smart electrical panels that replace traditional fuse boxes and help households significantly reduce power costs. The system tracks electricity use in real time, automates appliances, and provides advanced safety alerts through a mobile app. By analyzing usage patterns and shifting consumption to cheaper time periods, homeowners can optimize energy bills and identify electrical faults early. The company reports strong early demand, with thousands of units already ordered at launch.

- May 2025: Littelfuse introduced the Nano² 415 SMD Series Fuse, its first surface-mount fuse capable of 1500 A interrupting at 277 V, a record for compact low-voltage designs. This product targets applications in consumer electronics, industrial systems, EV charging, and home automation, where space-efficient yet powerful protection is critical.

- May 2024: Littelfuse opened a central new manufacturing facility in Piedras Negras, Mexico, doubling capacity in the region with advanced automation and sustainable practices. This expansion enhances production for industrial, renewable energy, and data-center protection applications while creating local jobs and strengthening supply resilience.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.05% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Voltage

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 5.84 billion in 2025 and is projected to reach USD 10.88 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.56 billion.

The market is expected to grow at a CAGR of 7.05% over the forecast period of 2025-2032.

By voltage, the low voltage segment led the market.

Expansion of power infrastructure and electrification are the key factors driving the market.

Littelfuse, Eaton, Schneider Electric, Mersen, and ABB are the major players in the global market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 226

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us