High Voltage Cables Market Size, Share & Industry Analysis, By Installation (Overhead, Submarine, and Underground), By Voltage (100 – 250 KV, 251 – 400 KV, and Above 400 KV), By End-User (Industrial and Utility), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

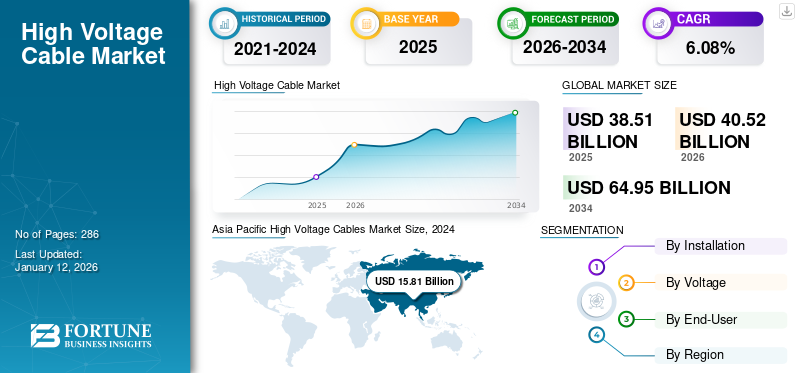

The global high voltage cables market size was valued at USD 38.51 billion in 2025 and is projected to grow from USD 40.52 billion in 2026 to USD 64.95 billion by 2034, exhibiting a CAGR of 6.08% during the forecast period.

High voltage cables are insulated conductors designed to transmit electrical power at voltages exceeding 100 kV. These cables are essential for long-distance power transmission and distribution networks, commonly found in electrical grids.

Increasing demand for efficient power transmission over long distances, coupled with the necessity to upgrade and expand power grids for renewable energy integration, is driving the demand for in the market.

Prysmian is a global market leader in the market. The company focuses on improving its power transmission solutions, specifically with high-voltage direct current (HVDC) technology for long-range transmission.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increased Need for Efficient Power Transmission Over Long Distances is Driving Market Growth

High-voltage power cables are vital for efficient long-distance electricity transmission, minimizing energy losses compared to low-voltage systems. This efficiency is crucial in extensive power grids spanning vast distances. Transmission lines, often made of copper or aluminum alloys, have inherent resistance, leading to power loss known as "copper loss" or "I2R loss." This loss is proportional to the current flowing through the line, and in order to cater to this, high-voltage levels are employed to reduce current and, consequently, power dissipation. By minimizing power loss, high-voltage cables enhance the overall efficiency of electrical grids.

Countries such as China and India have realized the benefits of high-voltage projects. For instance, in 2022, the State Grid Corporation of China (SGCC) commenced operations on a significant 2,080 km section of the Baihetan-Jiangsu 800 kV ultra-high voltage (UHV) direct current transmission line, which is integral to the nation's "west-to-east" power transmission initiative. The 800 kV UHV line integrates traditional and flexible direct current technologies, allowing for a power transmission capacity of 8 GW. China's program for power transmission from west to east aims to equalize electricity supply and demand across various regions.

Economic Advantages Associated with the High Voltage Transmission Line are Driving the Market Growth

High voltages are primarily used to minimize power loss during transmission. The increasing voltage reduces current while transmitting the same power, which is crucial as transmission lines have inherent resistance, impeding current flow. This resistance causes voltage drops and converts energy into heat. The power equation shows that power loss is proportional to the square of the current (I2R). Therefore, higher voltages, which allow for lower currents for equal power, significantly decrease I2R losses. Lower currents also translate to cost savings in construction as smaller conductors can be used, which eventually reduces material and construction expenses while still minimizing power loss.

For instance, the Zhundong Wannan HVDC Line is an overhead line operating at 1100kV that spans 3324 km from Zhundong, Changji, Xinjiang, China, to Wannan, Guquan, Anhui, China. Construction of the Zhundong–Wannan HVDC Line began in 2017 and was completed in 2020. The Zhundong Anhui South project was viewed as a key component of China’s Belt and Road Initiative (BRI, refer to sidebar “The Belt and Road Initiative”). The initiative offers substantial economic, social, and environmental advantages for the area.

MARKET RESTRAINTS

High Project Cost of High Voltage Transmission Line is Expected to Hinder the Market Growth

High-voltage transmission lines are beneficial in terms of reducing power loss. Still, their overall cost of is considerably high, which is attributed to various factors such as geographical challenges, offshore projects, etc. Projects with geographical challenges need a highly skilled workforce, technology, project management, etc. In addition, offshore projects demand different types of expertise, which also majorly contributes to the cost of the overall project.

For instance, the Biscay Gulf Project is worth ~USD 800 to 900 million for a new electrical interconnection linking Spain and France. The initiative is part of the European Commission’s Projects of Common Interest, as it enhances the reliability of power supply, facilitates greater integration of renewable energy into electricity grids, and helps develop a more efficient system. The EPCI contract for Cable Link 2 of the Biscay Gulf Project includes approximately 400 km of submarine and onshore power cables, providing a total capacity of 1 GW. The budget and cost of the project may vary depending on the offshore location and the complexity of the tools, which also negatively impact the high voltage cables market growth.

MARKET OPPORTUNITIES

Rising Integration of Renewable Energy into the Grid is Expected to Create Lucrative Opportunities

High-voltage power transmission systems are increasing as electricity produced at renewable energy facilities in far-off areas frequently needs to be sent to remote load centers. The growth of renewable energy sources, such as wind and solar farms, which are often located in remote areas, has increased the demand for high-voltage transmission to integrate these resources into the grid. Several countries are committed to climate change goals and trying their best to diversify their energy consumption sources.

For instance, in 2025, Bharat Heavy Electricals Ltd. obtained a Letter of Intent from Rajasthan Part I Power Transmission Ltd. to plan and implement the High Voltage Direct Current link and related AC substations to deliver renewable energy from Bhadla III (Rajasthan) and Fatehpur. HEL, in partnership with Hitachi Energy India Ltd., obtained the LOI. In this project, BHEL plans to set up two HVDC LCC terminal stations of 6,000 MW at Bhadla (Rajasthan) and Fatehpur (UP), as well as an over 800 kV HVDC LCC terminal station (4X1500 MW) linking Bhadla III and Fatehpur, including related AC substations.

MARKET CHALLENGES

Stringent Environmental Rules for Cable Installation and Disposal Pose a Challenge to Market Expansion

The high voltage cables market faces a major challenge in the growing difficulty and strictness of environmental rules governing cable installation and disposal. This challenge involves complex permit approvals, addressing worries about electromagnetic field (EMF) output, and managing the environmental consequences of building work, particularly in fragile environments or urban zones. These demands increase upfront costs while also causing delays, unpredictability, and possible long-term responsibilities for project planners. Enhanced environmental monitoring can increase scrutiny from regulatory bodies and residents, perhaps leading to project alterations or abandonment.

HIGH VOLTAGE CABLES MARKET TRENDS

Expansion Of Ultra-High Voltage Transmission Projects is the Latest Trend in the Market

Globally, the market is currently seeing a strong expansion towards the Ultra High Voltage (UHV) transmission systems. This trend is driven by the rising need for effective long-distance power transfer, especially from renewable energy projects located far from cities. Countries around the world are investing in boosting grid reliability and promote international electricity trading, which includes both improvements to current high voltage networks and the development of UHVDC (Ultra High Voltage Direct Current) systems.

For instance, the State Grid Corporation of China (SGCC) advanced its "west-to-east" power transmission initiative, which is a crucial element in the Baihetan-Jiangsu 800 kV ultra-high voltage (UHV) direct current transmission line, with 2,080 km already operational. Additionally, the Changji-Guquan UHVDC transmission line represents a global first, operating at 1,100kV. This project, also managed by SGCC, boasts the longest transmission distance globally. Furthermore, it has the largest transmission capacity globally, which spans 3,324 km and can deliver up to 12 GW of power.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Installation

Overhead Cables Dominate the Market due to Their Lower Installation Cost

Based on the installation, this market is segmented into overhead, submarine, and underground.

Overhead holds the dominating high voltage cables market share of 69.13% in 2026, as overhead power lines are typically the most affordable means to deliver significant quantities of electricity across extended distances. These power lines remain at a lower temperature than underground cables as they hang in the air, enhancing their capacity to transmit more current.

Submarine transmission lines are expected to grow the fastest during the forecast period, with a growth rate of 6.51% which is due to the rising renewable integration, especially in Europe. For instance, Prysmian is to supply the 525 kV HVDC XLPE Submarine Cable System in the U.K. The Eastern Green Link 1 (EGL1) will establish an essential electricity transmission connection between Torness in East Lothian, Scotland, and Hawthorn Pit in County Durham, England.

To know how our report can help streamline your business, Speak to Analyst

By Voltage

251 – 400 KV Segment Dominates the Market Due to Its Efficiency in Transmitting High Power Across Long Distances

Based on the voltage, this market is segmented into 100 – 250 KV, 251 – 400 KV, and above 400 KV.

The 251 – 400 KV segment holds the largest share of the market with 46.79% in 2026, as transmission lines can efficiently transmit substantial power across great distances while remaining economical and technologically viable.

Above 400 KV segment is expected to grow considerably in the coming years with a growth rate of 6.9% due to rising electricity demand, development of renewable energy sources, and necessity for effective and dependable power transmission across long distances. The growing use of renewable energy sources, such as solar and wind power, in distant locations is expected to drive demand for this segment.

By End-User

Utility Dominates the Market as it Handles Long-Distance Power Transmission and Distribution

Based on end-user, the market is segmented into utility and industrial.

The utility sector holds the major share of 86.23% the market in 2026, as electric utilities lay down more high-voltage (>100 kV) power cables than the industrial sector, mainly because utilities handle long-distance power transmission and distribution, which is best accomplished at high voltages to reduce energy loss.

Although industrial plants often utilize high-voltage electricity, they primarily require localized power distribution within the facility rather than long-range transmission.

HIGH VOLTAGE CABLES MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific is not only the dominating but also the fastest growing region in the market.

Asia Pacific

Asia Pacific High Voltage Cables Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 40.74% to the global market in 2025, with a valuation of USD 15.69 billion, and is projected to reach USD 16.59 billion in 2026. The region is emerging as a high-growth market for high-voltage cables, driven by industrialization and escalating electricity demands, especially in China, Southeast Asia, and India. Substantial investments in new power generation plants and transmission infrastructure to link remote locations are boosting demand. For instance, in 2021, Hitachi ABB Power Grids in India announced the commissioning of a 1,800 km 6GW ultra-high voltage direct current (UHVDC) transmission link connecting Raigarh to Pugalur. China is the key contributor to the APAC market, driven by extensive investments in ultra-high-voltage (UHV) transmission networks designed to deliver electricity from resource-abundant western regions to the heavily populated eastern areas. According to the IEA, in January 2023, China's State Grid Corporation declared investments of USD 77 billion in transmission for 2023 and USD 329 billion throughout the full duration of the 14th Five-Year Plan. In 2026, the Chinese market is estimated to reach USD 8.11 billion.

Europe

Other regions, such as the European high-voltage cable sector, are experiencing ongoing investment, driven by the shift to a low-carbon energy system. The Europe market generated USD 9.08 billion in 2025, representing 23.60% of the global market landscape, and is expected to reach USD 9.53 billion in 2026. Some of the major factors include offshore wind farm projects, interconnector initiatives to link national grids, and the strengthening of existing grids to accommodate greater renewable energy integration. For instance, the EU allocated more than USD 1.6 billion to cross-border infrastructure to strengthen its Energy Union and enhance competitiveness. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 1.67 billion in 2026, Germany to record USD 2.31 billion in 2026, and France to record USD 1.81 billion in 2025.

North America

In 2025, North America represented USD 6.59 billion, accounting for 17.13% of the worldwide market, and is projected to grow to USD 6.91 billion in 2026. In the region, the U.S. is estimated to reach USD 6.14 billion in 2026. North America high voltage cables market is driven by grid modernization, renewable energy integration with a focus on offshore wind, and replacement of aging infrastructure. According to the U.S. Energy Information Administration, expenditures on electricity transmission systems almost tripled from 2003 to 2023, rising to USD 27.7 billion. Moreover, in 2023, capital investment for electricity transmission rose by USD 2.7 billion (11%) compared to 2022.

Latin America

The market in Latin America reached USD 3.1 billion in 2025, representing 8.06% of total market revenue, and is projected to reach USD 3.21 billion in 2026. Over the forecast period, the Latin American high-voltage (HV) cable market offers growth potential, driven by infrastructure upgrades and the expansion of electricity access in rural areas. The Latin America market in 2026 is set to record USD 3.21 billion as its valuation.

Middle East & Africa

The Middle East & Africa market was valued at USD 4.03 billion in 2025, capturing 10.48% of global revenue, and is estimated to reach USD 4.27 billion in 2026. The Middle East & Africa are active in transmission links projects; this is due to the high energy requirements in these countries. The rise in the deployment of renewable projects in Middle East countries is driving the demand for transmission projects. In the Middle East & Africa, GCC is set to attain the value of USD 1.30 billion in 2025.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Market Is Characterized By Established Global Players And Smaller Regional Specialists, Leading to Competition On Price and Technology

The market is concentrated among major players like Prysmian Group, Nexans, and Hengtong, who possess a substantial market share attributed to their technological advancements and global reach. The demand for HVDC cables in renewable energy initiatives and grid infrastructure modernizations is fueling greater competition, prompting companies to emphasize innovation, cost optimization, and collaborative alliances to win contracts.

List of the Key High Voltage Cables Companies Profiled

- Prysmian Group (Italy)

- Sumitomo Electric Industries, Ltd. (Japan)

- Nexans (France)

- NKT A/S (Denmark)

- LS Cable & System Ltd. (South Korea)

- TBEA Co., Ltd (China)

- Dubai Cable Company (UAE)

- Wuxi Jiangnan Cable Co., Ltd. (Hong Kong)

- Taihan Cable & Solution Co., Ltd. (South Korea)

- Hengtong (China)

- Universal Cables Ltd (India)

- Southwire (U.S.)

- ZTT Group (China)

- Riyadh Cables Group Company (Saudi Arabia)

- Tratos (Italy)

- Brugg Cables (Switzerland)

- ZW Cables (China)

- Iljin Electric (South Korea)

KEY INDUSTRY DEVELOPMENTS

- March 2025- LS Cable & System of South Korea, along with its subsidiary LS Eco Energy Limited, secured the order for the initial delivery of MV-grade aluminum power cables. The two firms will provide 35 kV aluminum power cables valued at USD 25 million to a solar EPC company in the US. The cables will be utilized to construct power grids for solar energy facilities in California, New Jersey, and Indiana. These cables improve the reliability of solar energy systems because of their excellent durability and consistent high-voltage transmission capabilities.

- January 2025- Taihan Cable & Solution obtained a high-voltage power grid project in the U.K valued at USD 68.17 million. The order forms a component of the Memorandum of Understanding (MoU) for collaboration in the transmission and distribution sector, signed with Balfour Beatty in November 2023.

- September 2024- NKT secured an order from the Belgian transmission system operator (TSO) Elia Transmission Belgium (ETB) to provide 545 km of high-voltage cables for grid enhancements. ETB, which is Belgium’s national transmission system operator (TSO) and a member of the Elia Group, oversees the high-voltage transmission network in the country. Its network consists of 9,000 km of overhead wires and underground cables, essential for distributing electricity throughout the nation.

- July 2024- NKT started the construction of a new cable extrusion tower for the largest high-voltage offshore cable manufacturing facility in the world. The project will greatly enhance the company’s capacity to address the increasing need for larger and longer high-voltage offshore cables crucial for the green transition.

- August 2022- Prysmian Group announced it had developed and tested its initial 525 kV extruded submarine complete cable systems for High Voltage Direct Current (HVDC) use. It asserts that advancements in cable technology will allow for a significant augmentation of the peak transmission capability of bi-pole systems to over 2.5 GW, exceeding twice the capacity attained with the currently operational 320 kV DC systems.

Investment Analysis and Opportunities

- Globally, governmental investments in energy infrastructure are fueling the demand for high-voltage cables, especially for long-distance transmission, offshore wind farms, and grid interconnections, boosted by global shifts toward clean energy, electrification, and the modernization of outdated networks. This increase in investment generates prospects for market expansion, technological advancements, job creation, and supply chain improvements.

- Electric utility companies make some notable investments. For example, during the initial half of 2023, TenneT allocated ~USD 4 billion toward expanding and replacing the grid, nearly twice the sum from the previous year's corresponding period.

- Furthermore, in 2024, Prysmian, Nexans, NKT-SolidAl, and Hellenic Cables will guarantee power cable provision for their initiatives in the next 3 to 4 years. Valued at nearly USD 1 billion, this agreement entails providing and installing approximately 5,200 kilometers of underground cabling for voltage ranges between 90,000 and 400,000 volts.

REPORT COVERAGE

The global high voltage cables market report delivers a detailed insight into the market and focuses on key aspects such as leading companies, market trends and technology, and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Installation

|

|

By Voltage

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 38.51 billion in 2025.

The market is likely to grow at a CAGR of 6.08% over the forecast period.

The market size of Asia Pacific stood at USD 15.69 billion in 2025.

The Increased need for efficient power transmission over long distances and economic advantages associated with the high voltage transmission line are the key factors driving the market growth.

Some of the top players in the market are Nexans, NKT A/S, Prysmian Group, and others.

The global market size is expected to reach USD 64.95 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 286

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us