Medium Voltage Cables Market Size, Share & Industry Analysis, By Installation (Overhead and Underground), By Voltage (1 kV - 15 kV, 16 kV - 35 kV, and 36 kV - 70 kV), By Application (Industrial, Commercial, and Utility), and Regional Forecast, 2026-2034

Medium Voltage Cables Market Size and Future Outlook

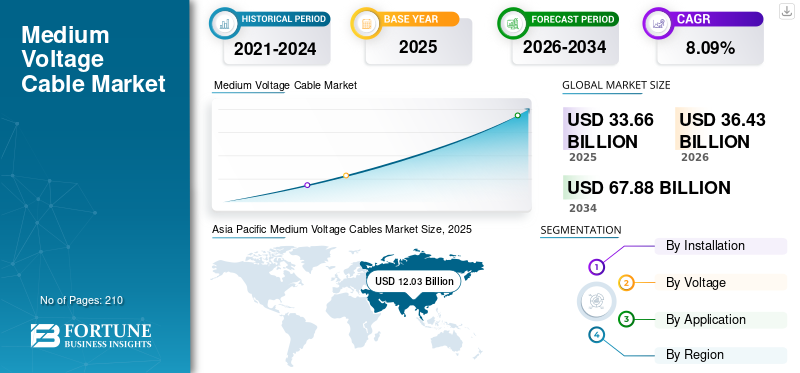

The global medium voltage cables market size was valued at USD 33.66 billion in 2025. The market is projected to grow from USD 36.43 billion in 2026 to USD 67.88 billion by 2034, exhibiting a CAGR of 8.09% during the forecast period. Asia Pacific dominated the global medium voltage cable market with a market share of 38.71% in 2025.

The medium voltage cables market is rising globally due to several technical and infrastructure-specific shifts across power, industrial, and transportation networks. Utilities are upgrading aging distribution grids to support higher load density, distributed energy resources, and improved system reliability, driving replacement of legacy conductors with Medium Voltage (MV) underground and submarine cables.

Rapid expansion of renewable energy projects, especially solar parks, onshore wind farms, and battery-storage facilities, requires MV export circuits to connect generation assets to substations. In industrial sectors, new data centers, manufacturing plants, and electrified mining operations depend on MV networks to handle higher power requirements with lower losses and improved fault performance. These factors have been driving the market share in recent years. Sumitomo Electric Industries delivers high-quality medium-voltage cables known for their advanced materials, reliable performance, and innovative power transmission technologies.

- For instance, in June 2025, Prysmian Group invested USD 500 million in a U.S. facility for medium-voltage cables. The Italian cable manufacturer announced a project to build a facility exceeding 650,000 sq ft in McKinney, Texas, which will significantly increase medium voltage cable production capacity and create approximately 120 new jobs. The plant is expected to begin operations in 2027.

Major companies in the global medium-voltage cable market include Prysmian Group, Nexans, Southwire, NKT, LS Cable & System, and others. These manufacturers supply medium voltage Cables for utilities, renewable energy projects, industrial facilities, and infrastructure development. Their focus on advanced materials, grid-modernization solutions, and large-scale project capabilities strengthens their global presence and competitiveness.

Download Free sample to learn more about this report.

MEDIUM VOLTAGE CABLES MARKET TRENDS:

Technological Advancements and Use of Advanced Materials & Insulation Systems are Key Market Trends

Medium voltage cables increasingly incorporate built-in sensors (temperature, partial discharge, current) and communication modules. These “smart” cables allow real-time monitoring of condition and loading, enabling predictive maintenance instead of reactive fixes. For instance, an embedded fiber-optic or sensor network inside MV sheaths lets operators detect overheating or incipient faults, thereby extending asset life and reducing unplanned downtime. A smart grid for medium-voltage cables integrates advanced sensing, automation, and communication technologies to optimize power distribution, enhance reliability, and enable real-time monitoring and control.

In addition, a shift toward new insulation materials (such as cross-linked polyethylene – XLPE) and enhanced armoring to support higher thermal loads, flexing environments (underground, subsea), and longer service lives presents an excellent market opportunity.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Modernization & Upgradation of Grid Infrastructure to Propel Market Growth

The modernization and upgradation of electrical distribution networks, where utilities are replacing aging conductors with MV underground solutions to increase load capacity, reduce fault risk, and handle two-way power flows from distributed energy sources, is a major growth driver. Large-scale solar parks, wind farms, and energy-storage facilities rely on MV export circuits to move power to substations, making MV cables a core component of renewable project design rather than an optional add-on. Data center expansion is another driver as hyperscale facilities require stable, medium-voltage feeders to support high-density compute loads and ensure redundancy.

- For instance, in May 2024, the U.S. Department of Energy launched the “Federal-State Modern Grid Deployment Initiative” to accelerate transmission and distribution upgrades across states, reflecting utilities’ shift toward replacing older medium-voltage cable infrastructure.

MARKET RESTRAINTS:

High Installation Cost & Installation Complexity to Limit Market Expansion

A significant restraint for medium voltage (MV) cable adoption is the growing complexity and cost of upgrading or installing MV networks within constrained or legacy infrastructure environments. Many utilities operate networks that were originally built for lower load densities and simpler radial configurations, meaning MV cable upgrades often require extensive civil works, rerouting, or trench enlargement to meet modern safety clearances and thermal performance standards. In dense urban areas, excavation restrictions, right-of-way limitations, and conflicts with existing utilities such as fiber ducts, water mains, and gas pipelines significantly slow project timelines and increase installation costs. Additionally, permitting processes for underground MV installations have become more stringent as municipalities enforce stricter environmental, noise, and traffic-impact assessments. These factors impacted the medium voltage cables market growth.

MARKET OPPORTUNITIES:

Electrification of Ports, Industrial Parks, and Logistic Hubs Are Anticipated to Create Growth Opportunities

A major opportunity for medium voltage (MV) cables lies in the rapid expansion of electrification across sectors that traditionally depended on localized or fossil-fuel-based power systems. Ports, mining operations, industrial parks, and large logistics hubs are increasingly transitioning to electric equipment, automated systems, and high-efficiency drives, requiring robust MV distribution backbones to deliver stable, high-capacity power over short and medium distances. Offshore energy infrastructure also presents strong potential, as electrified platforms, subsea processing units, and shore-to-platform power links depend heavily on MV export and interconnection circuits. In transportation, the growth of electric rail, metro systems, and charging infrastructure for heavy-duty EV fleets demands new MV feeders to support traction loads and clustered charging points.

MARKET CHALLENGES:

Technical & Implementation Complexities Present Significant Challenges for Market Growth

Medium voltage (MV) cable projects face several technical and implementation challenges that slow adoption and complicate network upgrades. A major issue is the integration of MV circuits into congested underground corridors, where limited trench space, existing utility conflicts, and strict municipal excavation restrictions significantly constrain installation options. In many regions, MV cables must be routed around telecom ducts, water mains, and aging infrastructure, forcing deeper or more complex alignments that increase thermal resistance and reduce permissible ampacity unless additional engineering measures are applied.

Segmentation Analysis

By Installation

Overhead is Dominant Owing to Easier Access for Inspection and Less Complex Civil Work Required for Inspection

On the basis of the installation, the market is classified into overhead and underground. In 2025, the overhead segment will account for 62.97% market share in 2026. Overhead medium-voltage (MV) cables offer practical, engineering, and operational advantages that underground systems cannot match in many contexts. Their installation requires significantly less civil work, allowing utilities to deploy or expand MV feeders rapidly across long distances, particularly in rural, semi-urban, and industrial corridors where trenching is costly or technically difficult.

The underground segment is experiencing the fastest growth and is expected to grow at a CAGR of 10.43%. Underground cables offer significantly higher resilience to weather-related disruptions, such as storms, high winds, and lightning, reducing outage frequency and improving network reliability. Additionally, large renewable projects, data centers, and industrial campuses favor underground MV systems for their stability, reduced electromagnetic exposure, and compatibility with controlled-access sites.

To know how our report can help streamline your business, Speak to Analyst

By Voltage

1kV-15kV Segment Commands Market Owing to Its Ability to Handle a Large Volume of Waste

On the basis of voltage, the market is classified into 1kV-15kV, 16kV-35kV, and 36kV-70kV. In 2026, the 1kV-15kV segment dominates with a 50.16% share. Medium-voltage cables in the 1 kV to 15 kV range are popular as they offer an optimal balance between power capacity, installation flexibility, and cost-effectiveness for modern distribution needs. This voltage class is well-suited for feeding commercial complexes, industrial plants, renewable energy installations, and suburban distribution circuits where loads are substantial but do not require the complexity of high-voltage systems.

The 16kV-35kV segment is experiencing the fastest growth and is expected to grow at a CAGR of 10.78%. The MV cables in this range provide improved thermal performance and reduced line losses, making them well-suited for dense industrial corridors and expanding metropolitan networks. They also integrate efficiently with modern ring-main and looped distribution architectures, supporting redundancy and network resilience.

By Application

Utility Segment Leads as They Widely Use MV Cables to Eliminate Overhead Fault Risk and Reduce Outage Frequency

On the basis of application, the market is classified into industrial, commercial, and utility. In 2026, the utility segment dominates the market with a 50.31% share. Utilities remain the largest application segment for MV cables, as they underpin distribution network expansion and modernization efforts. For instance, a major U.S. utility replaced an existing overhead MV feeder with a 15 kV underground cable section in July 2023 to improve reliability in storm-prone suburbs. The utility chose MV cable to support looped distribution, eliminate overhead fault risk, and reduce outage frequency in its feeder network.

The industrial segment is experiencing the fastest growth and is expected to grow at a CAGR of 11.09%. Medium-voltage (MV) cables are gaining popularity in the industrial sector as modern facilities increasingly require stable, high-capacity power distribution that low-voltage systems cannot support efficiently. As industries adopt larger motors, automated production lines, high-density process equipment, and energy-intensive technologies, MV cables allow these loads to be supplied through fewer feeders with lower electrical losses and better voltage stability across long internal routes.

Medium Voltage Cables Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Medium Voltage Cables Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 43.12% of the global market in 2025, generating USD 13.03 billion in revenue, and is projected to reach USD 14.29 billion in 2026. Medium-voltage (MV) cable demand is high in the Asia Pacific region as the region is undergoing rapid, infrastructure-heavy electrification that requires stronger and more reliable distribution networks. Large industrial corridors, manufacturing clusters, and transport hubs across countries such as India, China, Vietnam, and Indonesia increasingly depend on MV feeders to support high-density industrial loads and continuous production cycles.

Europe

In 2025, the Europe market stood at USD 6.66 billion, representing 20.83% of global demand, and is projected to grow to USD 7.1 billion in 2026. The demand for medium voltage cables in Europe is driven by its power infrastructure around electrification, grid resilience, and renewable integration. Many European countries are replacing aging distribution assets installed decades ago, shifting from overhead lines to underground MV circuits to reduce outage risks and improve urban safety.

The market in Germany is valued at USD 1.6 billion in 2026. Germany is rapidly upgrading distribution networks to integrate renewable generation, expand electrified transport, and replace aging underground assets in densely built urban areas. Industrial regions also rely on MV systems to support high-capacity manufacturing loads, driving market growth.

North America

North America is valued at USD 5.80 billion in 2025 and is projected to record a growth rate of 6.86% during the forecast period. Extreme weather events in North America have pushed utilities to harden grids with more resilient MV underground systems. Additionally, the rapid expansion of renewable energy projects, particularly solar and onshore wind, requires extensive MV collection and interconnection networks, driving sustained demand across both countries.

The U.S. is valued at USD 5.25 billion in 2026. The rapid expansion of power infrastructure and growing electricity consumption are driving the medium voltage cable demand in the U.S. Utilities are upgrading aging transmission and distribution networks to improve grid reliability and support renewable energy integration, which requires extensive MV cabling. The surge in utility-scale solar and wind projects, along with increased grid-connected battery storage, also drives higher installation of MV cables for efficient power transfer. For instance, in February 2025, American Electric Power (AEP) and its affiliate Transource Energy LLC announced a USD 1.7 billion investment plan to upgrade transmission infrastructure across multiple states under PJM Interconnection. This investment is intended to modernize aging transmission lines and add capacity to meet rising electricity demand

Middle East & Africa

In 2025, Middle East & Africa generated USD 3.66 billion, contributing 11.87% to global market revenue, and is projected to grow to USD 3.97 billion in 2026. and secure the position of the fourth-largest region in the market. In the region, the GCC is valued at USD 1.35 billion in 2025. This growth is primarily due to the expansion of grid interconnections for industrial zones, the electrification of mining and desalination facilities, and the replacement of aging distribution networks in fast-growing urban corridors.

Latin America

Latin America recorded a market size of USD 2.34 billion in 2025, capturing 7.35% of the global market share, and is projected to reach USD 2.5 billion in 2026. The Latin America region is anticipated to show tremendous opportunities for medium voltage cables over the forecast period. Medium voltage cable uptake in Latin America is rising as countries expand MV networks to support copper and lithium processing hubs in Chile and Argentina, strengthen interconnections for Brazil’s industrial southeast, and supply new electrified transport corridors such as Bogotá’s metro and São Paulo’s upgraded rail systems. The Latin American market is valued at USD 2.50 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players:

Vendors are Actively Expanding Their Market Via Partnerships, Business Expansion, and Technological Advancements

Companies operating in the medium-voltage (MV) cable segment are adopting targeted growth strategies focused on strengthening technical capability, expanding manufacturing presence, and improving access to high-demand sectors. Many are forming partnerships with utilities, EPC contractors, and renewable project developers to secure long-term supply positions for grid upgrades, data centers, and solar or wind installations.

- For instance, in April 2024, NKT A/S announced that it is investing approximately EUR 100 million (USD 109 million) across its factories in Denmark, Sweden, and the Czech Republic to expand its medium-voltage cable production capacity (20-110 kV range).

LIST OF KEY MEDIUM VOLTAGE CABLE COMPANIES PROFILED:

- Prysmian Group (Italy)

- Nexans (France)

- NKT A/S (Denmark)

- ABB (Switzerland)

- Brugg Cables (Switzerland)

- Riyadh Cables Group Company (Saudi Arabia)

- ZTT (China)

- General Cable Technologies Corporation (U.S.)

- FURUKAWA ELECTRIC CO., LTD. (Japan)

- Jiangnan Group Limited. (China)

- Tratos (England)

- Universal Cables Ltd. (India)

- Schneider Electric (France)

- DUCAB (UAE)

- Synergy Cables (Israel)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025, Prysmian Group signed a long-term framework with E.ON to supply low & medium-voltage cables for German grid integration.

- In April 2025, Nexans (France) launched the “AMCL 12/24 kV” medium-voltage cable with thermoplastic insulation and recycled materials.

- In January 2025, NKT A/S completed investment in two of three sites (Czech Republic, Sweden), adding new medium-voltage power-cable production lines.

- In February 2024, Nexans was awarded a major contract to supply 6,000 kilometers of low and medium voltage cables and services to a leading Italian energy company to support Italy's energy transition from February 2024 for 16 months. This agreement strengthens Nexans' position as a long-term partner of the power plant and a key player in sustainable electrification. The low-voltage and medium-voltage cables are manufactured at Nexans' Italian factory in Battipaglia, utilizing 100% guaranteed low-voltage carbon, which reduces greenhouse gas emissions by 35-50%, depending on the product. In addition to reducing greenhouse gas emissions, these products will be used in underground power lines designed to withstand even more extreme weather events affecting power distribution infrastructure globally.

- In February 2024, Itron, Inc. and Schneider Electric are collaborating to enhance energy and power grid management as homeowners and businesses increasingly adopt distributed energy resources (DERs), such as rooftop solar, battery energy storage, electric vehicles, and grid-side microgrids. Companies are gradually integrating their smart grid and distributed energy resource (DER) management solutions to digitize electricity supply and demand in the medium-voltage range. Electricity demand is growing rapidly due to the electrification of transportation, heating, and other sectors. According to the U.S. Energy Information Administration, by 2050, the U.S. grid capacity is projected to nearly double from 2022, and the Canadian grid capacity is expected to reach 226 GW by 2050.

REPORT COVERAGE

The global medium voltage cables market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.09% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Installation, Voltage, Application, and Region |

| By Installation |

|

| By Voltage |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 36.43 billion in 2026 and is projected to reach USD 67.88 billion by 2034.

In 2025, the market value stood at USD 33.66 billion.

The market is expected to exhibit a CAGR of 8.09% during the forecast period of 2026-2034

The utility segment led the market by application

The growing adoption of medium voltage cables in the manufacturing & industrial sectors is expected to propel market growth

Prysmian Group, Nexans, NKT A/S, and ABB are some of the prominent players in the market.

Asia Pacific dominated the market in 2026.

Rapid electrification, grid modernization, renewable integration, and industrial power upgrades are collectively driving global medium voltage cable demand.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us