Hyperphosphatemia Treatment Market Size, Share & Growth Analysis, By Drug Class (Sevelamer, Calcium-based Phosphate Binders, Lanthanum Carbonate, Iron-based Phosphate Binders, Others, and Non-Phosphate Binders), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

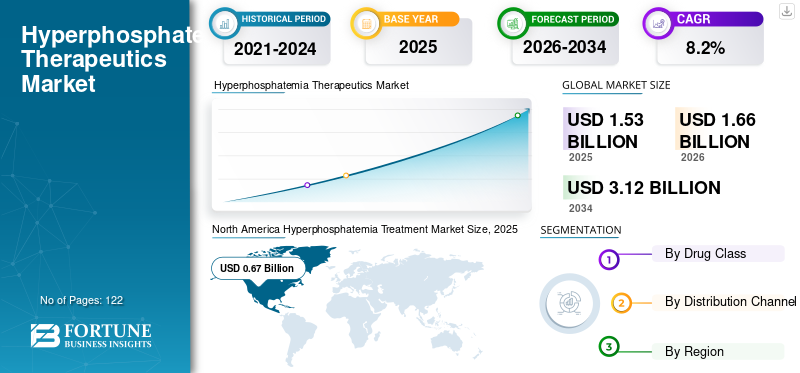

The global hyperphosphatemia treatment market size was estimated at USD 1.53 billion in 2025. The market is expected to rise from USD 1.66 billion in 2026 to USD 3.12 billion by 2034, expanding at a CAGR of 8.20% from 2026 to 2034. North America dominated the hyperphosphatemia treatment market with a market share of 43.78% in 2025.

Hyperphosphatemia or excess phosphate can be caused due to hypoparathyroidism, Chronic Kidney Disease (CKD), and other factors. The prevalence of chronic kidney disease has been increasing significantly across the world.

For instance, according to the data published by the International Society of Nephrology in 2022, chronic kidney disease affects more than 10% of the population globally. Moreover, the disease is more prevalent in the older population and individuals suffering from hypertension and diabetes mellitus.

The increasing prevalence of chronic kidney disease is directly proportional to the increasing burden of hyperphosphatemia. This factor has boosted the demand for effective therapeutics, thereby fueling the hyperphosphatemia treatment market growth.

Download Free sample to learn more about this report.

Hyperphosphatemia Treatment Market Overview & Key Metrics

Market Size & Forecast:

- 2025 Market Size: USD 1.53 billion

- 2026 Market Size: USD 1.66 billion

- 2034 Forecast Market Size: USD 3.12 billion

- CAGR: 8.2% (2026–2034)

Market Share:

- North America led the global hyperphosphatemia treatment market with a 43.78% share in 2025, driven by a high number of CKD patients undergoing dialysis and well-established healthcare infrastructure.

- Iron-based phosphate binders held the largest market share by drug class, supported by strong sales of branded drugs such as Auryxia and Velphoro. Non-phosphate binders like XPHOZAH (Tenapanor) are expected to witness rapid growth due to novel mechanisms and lower pill burden.

Key Country Highlights:

- Japan: Increasing adoption of non-calcium binders due to updated KDIGO guidelines.

- Submissions like Kyowa Kirin’s NDA for Tenapanor are driving innovation.

- United States: Over 808,000 ESRD patients as of 2023; nearly 69% on dialysis. FDA approval of XPHOZAH in 2023 expands treatment options with novel MOA.

- China: Rising CKD prevalence and regulatory approvals like Tenapanor (2023) support rapid market expansion. Shifting from traditional calcium binders to newer drug classes.

- Europe: Strong demand for iron- and sevelamer-based binders. Approvals and NICE recommendations (e.g., Kapruvia by CSL Vifor) fueling regional growth.

COVID-19 IMPACT

Market Experienced Slow Growth During COVID-19 due to Supply Chain Disruptions and Increased Mortality Rate

After the sudden onset of the COVID-19 outbreak in 2020, the growth of the hyperphosphatemia treatment market slowed down. This was due to a major decline in the number of chronic kidney disease and hemodialysis patients visiting the doctors for regular checkups, resulting in a limited number of people getting checked for hyperphosphatemia.

For instance, according to an article published by Elsevier Inc., in July 2020, approximately 28.2% of patients missed at least one or more dialysis sessions, and around 4.1% stopped reporting for dialysis.

However, in 2020, the market experienced a slow growth. This was due to the increased sales of products, such as Auryxia and Velphoro. For instance, in 2020, a product by Akebia Therapeutics, Inc. named Auryxia, generated a revenue of USD 128.9 million, experiencing an increase of 16% from the previous year.

Moreover, the market witnessed growth post-pandemic and is expected to grow significantly during the forecast period due to new product launches. For instance, Ardelyx’s XPHOZAH, a non-phosphate binder, got the U.S. FDA approval in October 2023 and is expected to be commercialized by the end of the same year.

Market Trends

Development of Innovative Hyperphosphatemia Treatment Options

It is very important to control the phosphate levels in dialysis patients. Even after improvements in dialysis technology, phosphate levels are still not controlled effectively. Moreover, variances in dialytic removal of phosphate, unexplained absorption of enteral phosphate through diet or vitamin D intake, and binder efficacy may be responsible for hyperphosphatemia in dialysis patients. Therefore, to increase the efficiency of the hyperphosphatemia treatment procedures in dialysis patients, researchers are focusing on developing novel hyperphosphatemia therapeutics and updating the treatment guidelines.

Earlier, sevelamer and calcium-based phosphate binders were the most commonly used binders. However, Kidney Disease: Improving Global Outcomes (KDIGO), a non-profit organization developing and implementing guidelines for kidney disease globally, updated the Clinical Practice Guideline for Chronic Kidney Disease–Mineral and Bone Disorder (CKD-MBD) in 2017. As per the updated guidelines, the dose of calcium-based phosphate binders should be limited among adult patients with Chronic Kidney Disease (CKD) receiving hyperphosphatemia treatment. This was due to the side effects of using these phosphate binders, such as increased risk of cardiovascular disease and hypercalcemia.

Moreover, market players have been focusing on creating awareness about the efficiency of their products so that healthcare professionals can use these drugs as the first line of treatment.

In June 2023, Akebia Therapeutics, Inc. announced the positive topline results of its Phase 4 collaborative study with U.S. Renal Care to study the effect of Auryxia when used as a first line of phosphate-lowering therapy. These results are important for nephrologists to understand the products’ efficiency.

Download Free sample to learn more about this report.

HYPERPHOSPHATEMIA TREATMENT MARKET GROWTH FACTORS

Increasing Prevalence of CKD is Fueling Demand for Effective Hyperphosphatemia Treatments

The burden of Chronic Kidney Disease (CKD) is increasing at a significant pace across the globe. For instance, as per the data published by the U.S. Centers for Disease Control and Prevention (CDC) in 2023, 35.5 million individuals, accounting for 14% of the U.S. population, were suffering from chronic kidney disease.

Hyperphosphatemia is most common in patients suffering from CKD and patients who are on dialysis. Therefore, the rising burden of these diseases has also been increasing the prevalence of hyperphosphatemia.

For instance, according to a research study published by the National Centers for Biotechnology Information (NCBI) in 2023, around 40% of dialysis patients who participated in the study suffered from hyperphosphatemia. As per the same study, 73% of Continuous Ambulatory Peritoneal Dialysis (CAPD) patients suffered from hyperphosphatemia.

This scenario has boosted the demand for effective hyperphosphatemia treatments, thereby fueling the market growth.

Increasing Market Players’ Focus on R&D for Development of New Therapeutics to Fuel Market Growth

The prevalence of hyperphosphatemia is increasing at a worrying pace across the world. This has augmented the demand for novel drugs with a new mechanism of action. Market players have increased their focus on launching new products with higher efficiency to expand their customer base.

For instance, Adrelyx discovered and developed a non-phosphate binder, XPHOZAH (tenapanor). Tenapanor is a minimally absorbed inhibitor of gastrointestinal sodium/hydrogen exchanger 3 (NHE3). The drug operates based on a non-phosphate-binding mechanism. Studies have shown that Tenapanor maintained serum phosphorus control through a considerable reduction in pill burden (by up to 80% as compared to phosphate binders).

In May 2023, the U.S. Food and Drug Administration (FDA) accepted Adrelyx’s resubmission of a New Drug Application (NDA) for Tenapanor. The drug is expected to be commercialized by October 2023. With positive results shown by the research studies, market players have increased their focus on developing such novel therapeutics.

The increasing focus of market players on R&D for developing new products and commercializing them is expected to fuel the market growth during the forecast period.

RESTRAINING FACTORS

Complications From Use of Hyperphosphatemia Therapeutics and Poor Medical Adherence to Hinder Market Growth

The demand for hyperphosphatemia treatment is growing at a significant rate due to the increasing burden of the disorder. However, certain limitations associated with using hyperphosphatemia therapeutics, such as gastrointestinal problems, hypercalcemia, and iron deposition in the organs, have been limiting its adoption among the patient population.

For instance, lanthanum carbonate phosphate binders cause gastrointestinal disorders in dialysis patients. Similarly, incorporating aluminium-based phosphate binders causes toxic effects, which can lead to bone diseases.

Adherence to the phosphate binder treatment is also a problem. Patients are required to take these drugs before and after every meal. These pills are generally large and require many pill dosages. Thus, hyperphosphatemia treatment results in a significant pill burden.

The above-mentioned complications can hamper the market growth.

Segmentation Analysis

By Drug Class Analysis

Strong Sales of Branded Products to Fuel Demand for Iron-based Phosphate Binders

Based on test type, the market is classified into sevelamer, calcium-based phosphate binders, lanthanum carbonate, iron-based phosphate binders, non-phosphate binders, and others.

The iron-based phosphate binders segment is projected to dominate the market with a share of 54.9% in 2026 and is expected to record a significant CAGR during the forecast period. The dominance of the segment is attributed to the strong sales of products from reputed brands Auryxia and Velphoro. Moreover, rising emphasis of the manufacturers on protecting their products from generic competition has also been fueling the segment’s growth.

Moreover, the non-phosphate binders segment is expected to grow significantly during the forecast period. XPHOZAH (tenapanor) is the only approved non-phosphate binder. Ardelyx is expected to commercialize its product XPHOZAH by October 2023. The drug has proven to be quite effective in lowering serum phosphate levels in adult patients. This factor will be responsible for the segment’s growth during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel Analysis

Increasing Number of Patients Visiting the Hospitals for Dialysis Treatment has been Fueling the Hospital Pharmacies Segment’s Growth

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

The hospital pharmacies segment dominated the global hyperphosphatemia treatment market share in 2025. The segment’s dominance is primarily due to the large number of patients seeking dialysis treatment in hospital facilities. Furthermore, emerging economies, such as India, where treatment price is one of the crucial factors, have witnessed a significant rise in the volume of dialysis patients in these settings. Thus, the high number of patients in hospital facilities is set to support the segment’s growth.

The online pharmacies segment is expected to record the fastest CAGR during the forecast period. The segment’s growth is attributed to the increasing shift of the patient population in metropolitan and capital cities toward e-commerce platforms to procure drugs to treat hyperphosphatemia. The segment’s expansion is further augmented by rapid growth in the number of online pharmacies, with leading e-commerce giants entering the lucrative segment in developed and emerging countries.

REGIONAL ANALYSIS

North America

Increasing CKD Patient Population Helped North America Dominate Global Market

North America dominated the market with a valuation of USD 0.67 billion in 2025 and USD 0.73 billion in 2026. The high revenue generated by the regional market is due to the presence of a large number of CKD patients undergoing dialysis in the region.

North America Hyperphosphatemia Treatment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

According to the statistics published by the National Institute of Diabetes and Digestive and Kidney Disorders (NIDDK) in May 2023, an estimated 808,000 people in the U.S. were living with End-Stage Renal Disease (ESRD), out of which 69% of them were on dialysis. Hence, the factor mentioned above is anticipated to significantly boost the demand for hyperphosphatemia therapeutics during the forecast period.

Europe

The market in Europe is projected to register considerable revenue during the analysis period. The rising number of approvals for hyperphosphatemia drugs by the European Commission and increasing number of patients undergoing dialysis in major countries are leading to a higher demand for iron-based and sevelamer-based phosphate binders in the region.

Asia Pacific

Asia Pacific is anticipated to witness lucrative growth during the forecast timeframe. The market in China, India, and other emerging countries is characterized by a higher prescription of calcium-based phosphate binders as compared to the developed countries. However, the changing prescription patterns in these countries and a significantly higher patient population undergoing dialysis in Asia Pacific are the major factors set to boost the demand for hyperphosphatemia treatment in the region during the forecast period.

Latin America and Middle East & Africa

The Latin America and the Middle East & Africa markets are booming due to the growing number of companies penetrating the untapped economies in these regions. The increasing number of distribution & supply agreements entered by manufacturers across these regions is set to support the adaoption of hyperphosphatemia therapeutics.

KEY INDUSTRY PLAYERS

Strong Sales of Hyperphosphatemia Therapeutics to Help Market Players Assert Dominance

Sanofi, Akebia Therapeutics, Inc., and CSL are some of the major players in the market, accounting for a significant share in 2022. The notable growth of these companies is attributed to their increasing focus on protecting their products from generic competition.

- In October 2022, Vifor, now a subsidiary of CSL, won the patent case against Teva Pharmaceutical Industries Ltd. for its product Velphoro. As a result, Velphoro’s patent against any generic competition will be protected till July 2030.

Other market players, such as Takeda Pharmaceutical Company Limited, Astellas Pharma Inc., and Lupin have been focusing on the expansion of their product portfolios for hyperphosphatemia therapeutics.

- For instance, in March 2022, Lupin launched Sevelamer Hydrochloride tablets in the U.S. These tablets are intended for the treatment of hyperphosphatemia among patients with chronic kidney disease. The launch of this product expanded the company’s product portfolio in the market.

LIST OF KEY COMPANIES PROFILED IN HYPERPHOSPHATEMIA TREATMENT MARKET:

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Lupin (India)

- Astellas Pharma Inc. (Japan)

- Akebia Therapeutics, Inc. (U.S.)

- CSL (Australia)

- Ardelyx (U.S.)

- Unicycive (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- August 2023 - Astellas Pharma Inc. collaborated with DivcoWest, a DivCore Capital Company. The collaboration planned to open new life science facility for Astellas at Morgan Avenue in Cambridge.

- July 2023 – Ardelyx received approval to use Tenapanor as a treatment for hyperphosphatemia in China. This approval aided the company in expanding its geographical presence in the international market.

- May 2023 – CSL Vifor announced the recommendation of England's National Institute for Health and Care Excellence (NICE) for Kapruvia as a treatment for moderate-to-severe CKD.

- October 2022 – Ardelyx’s partner Kyowa Kirin, Co. Ltd. (KKC) submitted a new drug application to the Japanese Ministry of Health, Labour and Welfare for tenapanor. This drug can contribute to company’s revenue growth if approved.

- December 2020 – Unicycive collaborated with Spectrum Pharmaceuticals. The collaboration aimed to sign a licensing agreement for Renazorb (lanthanum dioxycarbonate), a late-stage medicine for treating hyperphosphatemia.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The report provides a detailed analysis of the market’s competitive landscape. It also includes key insights, such as top industry developments covering partnerships, mergers, and acquisitions. Additionally, it focuses on key points, such as launch of new therapeutics in the market. Furthermore, the report covers regional analysis of different segments, profiles of key market players, market trends, and the impact of COVID-19 on the market. The report consists of quantitative and qualitative insights that have contributed to the market's growth.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.2% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Drug Class

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market value stood at USD 1.53 billion in 2025 and is projected to reach USD 3.12 billion by 2034.

In 2025, the market value stood at USD 0.67 billion.

The market is predicted to exhibit a CAGR of 8.2% during the forecast period of 2026-2034.

The iron-based phosphate binders segment led the market by drug class.

Increasing prevalence of chronic kidney disease and rising focus of market players on new product launches is fueling the markets growth.

Sanofi, Akebia Therapeutics, Inc., and CSL are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 122

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us