Influenza Vaccine Market Size, Share & Industry Analysis, By Type (Inactivated and Live Attenuated), By Valency (Quadrivalent and Trivalent), By Age Group (Pediatric and Adults), By Distribution Channel (Hospital & Retail Pharmacies, Government Suppliers, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

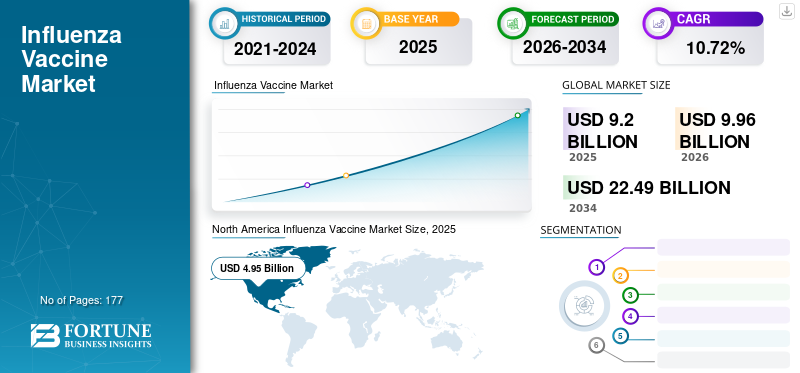

The global influenza vaccine market size was valued at USD 9.2 billion in 2025 and is projected to grow from USD 9.96 billion in 2026 to USD 22.49 billion by 2034, exhibiting a CAGR of 10.72% during the forecast (2026-2034). North America accounted for a market value of USD 4.95 billion in 2025 and dominated the influenza vaccine market with a market share of 53.79% in 2025. Every year, regional epidemics and outbreaks that result in thousands of deaths are caused by influenza viruses. According to data published by the World Health Organization (WHO) in October 2023, around 3 to 5 million severe influenza cases were recorded, leading to 290,000 to 650,000 deaths across the globe. Out of the total deaths caused by influenza, the majority occur in children. The increasing prevalence of seasonal outbreaks and epidemics is projected to drive the product sales during the forecast period.

There are numerous licensed seasonal influenza vaccines recommended by the Centers for Disease Control and Prevention (CDC), World Health Organization (WHO), and other governmental organizations to help fight the disease in the current market scenario. Furthermore, the WHO has launched the Global Influenza Program and GISRS, which collaborates with other agencies for the monitoring of the influenza virus and activities across the globe.

Furthermore, government agencies are advising people to get vaccinated early to provide maximum protection during the flu season. Moreover, pharmaceutical companies are continually facing new challenges in developing a suitable vaccine against a particular strain. Therefore, the rising demand for influenza vaccine is anticipated to drive the market.

The worldwide routine immunization programs and campaigns carried out in developing and developed countries were impacted by the coronavirus pandemic. However, factors including pressure from health departments and the expansion of government programs offering free doses increased the vaccination rate during the pandemic. Additionally, growing awareness among the public about the higher risk of getting infected with COVID-19 if the flu weakens the immune system is another factor contributing to the uptake of vaccines.

However, due to the coronavirus pandemic, the increasing focus on developing combination vaccines, mRNA vaccines, and others is offering various opportunities in the market. The development of a combination vaccine for COVID-19 and influenza virus would help reduce time and manufacturing cost, thus ramping up production.

For instance, in May 2021, Duke University researchers developed an mRNA-based COVID-19 and flu combination vaccine to protect an individual against both viruses simultaneously. Also, the major players in the market reported an increase in their revenues attributed to the increase in sales of vaccines during 2021. All these factors were responsible for the influenza vaccine market growth during post pandemic.

Download Free sample to learn more about this report.

Global Influenza Vaccine Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 9.2 billion

- 2026 Market Size: USD 9.96 billion

- 2034 Market Size: USD 22.49 billion

- CAGR: 10.72% from 2026–2034

Market Share:

- Region: North America dominated the market with a 53.79% share in 2025. This is driven by the rapid launch of effective products, technologically advanced vaccine manufacturing systems, and strong public health campaigns promoting vaccination.

- By Valency: The Quadrivalent segment held the largest market share in 2023. The segment's dominance is attributed to the greater demand for these vaccines, which offer broader protection, and the launch of novel products such as needle-free nasal influenza vaccines.

Key Country Highlights:

- Japan: The market is propelled by collaborations between major global and local players. For instance, Propeller Health partnered with Novartis to connect a digital health platform to specific medications, enhancing the management of respiratory conditions in the country.

- United States: Market growth is supported by a high prevalence of influenza, with approximately 37.2 million cases identified in 2021. The market is also driven by robust government-led awareness campaigns and a high rate of product approvals.

- China: As a key country in the fastest-growing Asia Pacific region, China's market is expanding due to its large population, rising healthcare expenditure, and increasing government initiatives to improve immunization coverage.

- Europe: The market is advanced by large-scale government procurement programs. For example, the European Commission, through its Health Emergency Preparedness and Response Authority (HERA), signed an agreement with GSK Plc to produce and supply 85.0 million doses of a pandemic influenza vaccine across 12 European countries

Influenza Vaccine Market Trends

Inclusion of Advanced and Effective Vaccines in Immunization Programs

In recent years, governments in several countries across the globe have been focusing on the implementation of various programs and strategies to increase the uptake of vaccines. This is majorly due to the frequent outbreaks of the influenza virus, coupled with the growing prevalence of influenza worldwide. Nowadays, greater awareness among the population with respect to infectious diseases has led to the implementation of vaccines through immunization programs for the prevention of conditions in developing and low income countries.

Developing countries have revised their immunization programs and included compulsory vaccination in their annual program for all age groups. For instance, in August 2023, the Health Service Executive (HSE), Ireland introduced the nasal spray flu vaccination program. Under this program, the vaccine is freely available for children aged 2-12 years. Similarly, in collaboration with the Washington State University Global Health Program in March 2021, the Kenya Ministry of Health’s National Vaccines Immunization Program initiated a vaccination drive in Mombasa and Nakuru counties of Kenya. Under the program, children aged 6-23 months were immunized for free. Such initiatives are anticipated to surge the demand for these vaccines resulting in robust market growth during the forecast period.

Download Free sample to learn more about this report.

Influenza Vaccine Market Growth Factors

Rising Adoption of Influenza Vaccines Due to Increasing Government Support for Immunization

To contain the outbreaks of the influenza virus, governments across the globe are expanding their support through various strategies, such as funding, campaigns, and others. Monitoring vaccine delivery, distribution, and availability requires national and international surveillance. The World Health Organization is one of the leading organizations that constantly monitors the demand for vaccines in association with other governments. These efforts are aimed to minimize the demand for vaccines.

- In October 2022, the Centers for Disease Control and Prevention (CDC), along with the National Foundation for Infectious Disease (NFID), launched a digital campaign, “Help Them Fight Flu,” in order to raise awareness among the parents to vaccinate their children against flu.

Organizations, such as the Centers for Disease Control and Prevention (CDC), WHO’s Global Influenza Surveillance and Response System (GISRS), and the health ministries of several countries are helping keep track of chronic diseases. Combined with this, Asian countries have started to roll out early influenza vaccination programs emphasizing the reduction of influenza and COVID-19 cases simultaneously. Therefore, active government support is expected to bolster the market growth rate over the forecast period.

Robust R&D Investments with Strong Pipeline Candidates to Drive Market Growth

To tap into the untapped avenues of the market, the leading players are focusing on increasing their investment in the research and development activities. In addition, launch of new products and expansion of manufacturing capabilities are some other strategies adopted by the key players to strengthen their market presence, thereby driving the market growth.

- In March 2021, Sanofi invested USD 714.3 million to establish a new vaccine manufacturing facility in Canada in order to increase the supply of its flu vaccines in the U.S., Canada, and Europe.

This, along with the strong pipeline of vaccines, and the growing government funding have facilitated the launch of therapeutically effective vaccines. Also, pharmaceutical companies are focusing on investing in R&D to launch new potential vaccines.

- For instance, in May 2023, the Phase 1 clinical trial for an innovative influenza vaccine was initiated. This experimental universal vaccine is being developed by a team of researchers at the National Institute of Allergy and Infectious Diseases’ (NIAID) Vaccine Research Center (VRC).

- Similarly, in April 2022, Novavax, Inc., announced the initial results from the Phase 1/2 clinical trial of its COVID-19-Influenza Combination Vaccine, stating the good tolerability and consistency of the pipeline candidate.

RESTRAINING FACTORS

Longer Timeline for Vaccine Production to Limit Market Growth

Establishing the efficacy, quality, and safety of a novel vaccine is a huge procedure that typically takes around 10-15 years to complete. Complexities in clinical development, vaccine research, and regulatory requirements are the three main causes of the lengthy timelines. There are considerable regional differences across the world in the regulatory frameworks for clinical trials. Therefore, this might cause significant delays in the creation of new vaccinations. Additionally, the presence of a broad range of pathogens that could contaminate the production can result in the loss of the product’s efficacy.

According to an article by the American Council on Science and Health (ACSH), the overall success rate for vaccines is around 33.4%.

Moreover, data from different countries or regions are often required for regulatory approval. However, there are different labeling requirements in many countries along with stretched timelines, which further adds complexity to the process of conducting clinical studies worldwide. Thus, the longer duration for conducting clinical trials and stringent regulatory requirements are anticipated to impede market growth.

In addition, factors, such as the lack of a standard manufacturing template for vaccines, stability, and inherent biological properties of the organism can also impede the market’s growth.

Influenza Vaccine Market Segmentation Analysis

By Type Analysis

Effectiveness Offered by Inactivated Products to Contribute to a Leading Position

On the basis of type, the market is classified into inactivated and live attenuated.

The inactivated segment is projected to dominate the market with a share of 92.31% in 2026. The demand for inactivated vaccines in developing and developed countries is due to the increasing focus of industrialists, as these are standardized according to the specific virus strain. The increasing demand, coupled with the high prevalence of influenza, is responsible for the highest CAGR of the segment during the forecast period.

- According to the data published by Elsevier B.V. in 2022, inactivated Quadrivalent Influenza Vaccine (QIV) given to children in the age group 6-35 months showed a strong antibody response even after 12 months of primary vaccination. Further, it lowered the incidence of influenza A/B infection.

On the other hand, live attenuated segment is anticipated to grow at a slower rate due to numerous challenges faced by companies in vaccine development and approval. Also, live attenuated vaccine is not recommended for some patients such as pregnant women, people with asthma, and weak immune systems.

To know how our report can help streamline your business, Speak to Analyst

By Valency Analysis

Quadrivalent Vaccines to Ace the Market Due to Growing Efficacy

Based on valency, the market is segmented into quadrivalent and trivalent.

The quadrivalent segment is expected to lead the market, contributing 94.27% globally in 2026. The quadrivalent segment dominated the market due to greater demand for the product. The sales have escalated in emerging as well as developed nations to meet the immunization targets set by governments to shield against influenza outbreaks. Additionally, the launch of novel vaccines has also contributed to the expansion of the quadrivalent segment. For instance, in October 2023, the Serum Institute of India (SII) and MyLab collaboratively launched the first needle-free nasal influenza vaccine in India. This vaccine is a live quadrivalent and it contains four strains of the virus. Furthermore, safety and immunogenicity properties, coupled with potential quadrivalent pipeline candidates, will help the segment record a higher CAGR during the forecast period.

On the other hand, trivalent vaccines are expected to record a smaller share in the market owing to the preference for trivalent over quadrivalent vaccines. This is limiting the trivalent vaccine availability.

By Age Group Analysis

High Infection Rates among Children Owing to Demand for Pediatric Vaccines

On the basis of age group, the market is segmented into pediatric and adults.

The pediatric segment is expected to register a higher CAGR among the age group segment. The dominance is attributable to the higher vaccination doses provided to newborns, infants, and children to shield them from an early age against influenza disease. The World Health Organization (WHO) as well as the Centers for Disease Control and Prevention (CDC) implemented immunization strategies such as the provision of vaccines at an early age as well as to every child globally. A high increase in influenza infection and frequency rates among young children has led to various strategies. The Centers for Disease Control and Prevention (CDC) also states that since 2010, flu-related hospitalizations among children have also increased the demand for higher infant age group pediatric vaccines. Furthermore, population increase in emerging countries, such as China and India, has led to the increasing demand for pediatric vaccines, propelling the market growth.

Besides, vaccination for adults has become mandatory to minimize the hospitalizations and deaths caused due to influenza. According to data published by Centers for Disease Control and Prevention (CDC) in 2021, it is estimated that approximately 70.0% to 85.0% of seasonal influenza-related deaths occur in people aged 65 and above. Adult vaccines hold a significant market share in the market due to the government's rise in immunization programs and the high vaccine dose procurement by GAVI, PAHO, and UNICEF. In addition, the immunization coverage provision has further led to an increase in the geriatric population getting vaccinated, increasing the demand for adult vaccines. The adults segment is expected to hold a 67.14% market share in 2026.

By Distribution Channel Analysis

Dominance of Hospitals & Retail Pharmacies Owing to Increased Immunization Rates

Based on distribution channel, the market is classified into hospital & retail pharmacies, government suppliers, and others.

The hospital & retail pharmacies segment will account for 66.88% market share in 2026. The hospital & retail pharmacies segment generated the highest revenue among all the distribution channels. This leading position is attributed to the fact that vaccination is generally preferred and conducted at smaller institutions. In addition, the large vaccine supply from hospitals is expected to generate a high market value in the forthcoming years. Therefore, the hospital & retail pharmacies segment is anticipated to witness the highest CAGR during the forecast period.

REGIONAL INSIGHTS

North America Influenza Vaccine Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed approximately USD 4.95 billion to the global market in 2025, accounting for 53.79% share, and is expected to reach USD 5.37 billion in 2026. The rapid launch of effective products, coupled with technologically advanced vaccine manufacturing systems across the region, is expected to drive market growth in the region. The US market is projected to reach USD 5.1 billion by 2026.

- According to data published by the World Health Organization (WHO), around 37.2 million influenza cases were identified in 2021 in the U.S.

Asia Pacific

The Asia Pacific region captured 13.49% of the global market in 2025, generating USD 1.24 billion in revenue, and is projected to reach USD 1.37 billion in 2026. Asia Pacific is expected to register a higher CAGR during the forecast period. The increasing number of government initiatives to provide these vaccines and create awareness about influenza is anticipated to drive market growth across the region. Also, the rising population across the region in China and India and the demand for effective vaccines leading to higher sales are expected to boost the market growth. The UK market is projected to reach USD 0.29 billion by 2026, while the Germany market is projected to reach USD 0.7 billion by 2026.

- In May 2021, the Health Minister of Australia launched the National Flu Vaccination Program with the objective to immunize Australians. Through this vaccination program, 20.0 million vaccine doses have been made available through pharmacies, GPs, and clinics.

Europe

In 2025, the Europe market stood at USD 2.45 billion, representing 26.67% of global demand, and is projected to grow to USD 2.63 billion in 2026. Europe held the second leading position in the global market. This is attributable to the expansion of vaccination coverage for high-risk people leading to higher immunization rates among the European population. The Japan market is projected to reach USD 0.32 billion by 2026, the China market is projected to reach USD 0.3 billion by 2026, and the India market is projected to reach USD 0.19 billion by 2026.

- For example, in July 2022, GSK Plc entered into an agreement with the European Commission’s Health Emergency Preparedness and Response Authority (HERA) to produce and supply 85.0 million doses of Adjupanrix, a pandemic influenza vaccine. As per the accord, the company would supply the doses to the 12 participating European countries.

Latin America and the Middle East & Africa

Latin America recorded a market size of USD 0.36 billion in 2025, capturing 3.93% of the global market share, and is projected to reach USD 0.38 billion in 2026.

In 2025, Middle East & Africa generated USD 0.19 billion, contributing 2.12% to global market revenue, and is projected to grow to USD 0.21 billion in 2026.

Latin America and the Middle East & Africa regions are expected to account for significant growth during the forecast period. This is attributable to the rising awareness of influenza virus, launch of influenza vaccine, and increasing government efforts to get everyone vaccinated, thereby fueling the market growth.

- For example, the Federal Health Ministry announced that more than 32.0 million doses of influenza vaccines would be administered for the 2021–2022 season in Mexico.

To know how our report can help streamline your business, Speak to Analyst

List of Key Companies in Influenza Vaccine Market

Strong Product Portfolio of Key Competitors to Dominate Market

Sanofi, a leading biopharmaceutical company, dominated the market share. The company focuses on establishing new manufacturing facilities and expanding its geographic footprint. Furthermore, the approval of its products for use in developing and developed nations also strengthens its market position.

- In July 2022, Sanofi’s two vaccines, Fluzone High-Dose Quadrivalent and Flublok Quadrivalent, received approval for influenza season 2022-2023 in the U.S. for adults over 65 years of age.

Other companies, such as CSL Limited, GlaxoSmithKline plc, and AstraZeneca, among others, have their products marketed globally. Additionally, factors such as the growing efforts to reduce the burden of diseases, increasing investments in research and development to launch next generation vaccines, and the surging vaccination rates are the primary focus of the market players to cater to the rising demand for these vaccines.

- In February 2022, CSL Limited invested in a new research and development facility situated in Waltham to support its growing R&D portfolio for seasonal and pandemic influenza vaccines. The company primarily focuses on utilizing the next-generation mRNA technology for the development of current and future vaccines.

LIST OF KEY COMPANIES PROFILED:

- GlaxoSmithKline plc (U.K.)

- Sanofi (France)

- AstraZeneca (U.K.)

- CSL Limited (Australia)

- BIKEN Co., Ltd. (Japan)

- Abbott (U.S.)

- SINOVAC (China)

- Viatris Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2024 – $100M Investment in Brazil

SINOVAC announced a $100 million investment in Brazil to establish local production of vaccines and monoclonal antibodies, and to advance cell therapy initiatives.

REPORT COVERAGE

The research report provides a detailed global influenza vaccine market analysis based on various dynamics. It focuses on key aspects such as leading companies, products, and distribution channels. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the market growth in recent years.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.72% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Valency

|

|

|

By Age Group

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.2 billion in 2025 and is projected to reach USD 22.49 billion by 2034.

In 2025, the market value stood at USD 9.2 billion.

The market will record a CAGR of 10.72% during the forecast period of 2026-2034.

The inactivated segment is expected to be the leading segment in the market during the forecast period.

Growing focus on immunization programs in developing economies to assist the adoption of vaccines, coupled with potential pipeline candidates, and technological advancements in the products and their manufacturing process, will drive the market.

Sanofi, GlaxoSmithKline plc, and CSL Limited (Seqirus) are the top players in the market.

North America is expected to hold the highest market share.

Increased awareness regarding immunization benefits, immunization coverage, and availability of effective vaccines in the market would drive the product adoption during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 177

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us