Lithium-ion Battery Market Size, Share & Industry Analysis, By Type (Lithium Cobalt Oxide, Lithium Iron Phosphate, Lithium Nickel Cobalt Aluminum Oxide, Lithium Manganese Oxide, Lithium Nickel Manganese Cobalt, and Lithium Titanate Oxide), By Application (Consumer Electronics, Automotive, Energy Storage System, Industrial, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

- The lithium-ion battery market size was valued at USD 134.08 billion in 2025 and is projected to grow to USD 865.33 billion by 2034, expanding at a CAGR of around 22.85% during 2026–2034.

- Adoption of lithium-ion batteries is expected to accelerate as demand rises from electric mobility, clean energy, and energy storage solutions, supported by continued technology innovations and growing investment in battery manufacturing.

- Increasing deployment across the automotive, consumer electronics, industrial, and utility-scale sectors is driving global lithium-ion battery demand, strengthening the industry's long-term growth outlook.

- Asia Pacific currently leads the global lithium-ion battery market, accounting for 56.10% of market share in 2025, supported by strong battery manufacturing capabilities, robust raw material processing infrastructure, and rising electric vehicle adoption.

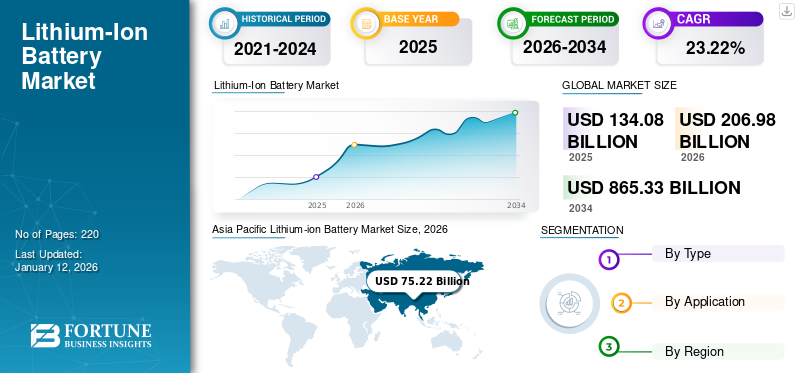

The global Lithium-ion (Li-ion) battery market size was valued at USD 134.08 billion in 2025 and is projected to grow from USD 206.98 billion in 2026 to USD 865.33 billion by 2034, exhibiting a CAGR of 22.85% during the forecast period. Asia Pacific dominated the global lithium-ion battery market, accounting for 56.10% of the market share in 2025.

Li-ion battery, or LIB, is a rechargeable battery used in laptops, cellphones, and hybrid & electric cars. Li-ion battery usage is growing across various applications owing to its lightweight and high energy density, which increases battery life and the ability to recharge.

The market is expected to grow significantly due to increasing demand for electric vehicles and global inclination towards adopting renewable energy in various industries. BYD Company is one of the key players in the market. The company is mainly engaged in the design, production, and distribution of rechargeable batteries catering to the automotive and consumer electronics industries.

The global lithium-ion battery market is experiencing sustained structural expansion, supported by accelerating electrification trends, growing investment in battery manufacturing, and rising deployment of energy storage solutions. Demand for lithium-ion technologies continues to increase across the automotive sector, consumer electronics, industrial systems, and utility-scale applications. Market participants increasingly view lithium-ion batteries as foundational infrastructure supporting clean energy transitions and long-term electrification objectives.

Battery manufacturers continue scaling production capacity to address increasing energy density requirements and changing application needs. The automotive sector remains a principal growth engine as electric vehicle adoption accelerates across developed and emerging economies. Demand for lithium-ion batteries within passenger mobility systems is reshaping global supply chains, increasing pressure on raw material procurement strategies and processing infrastructure. Battery markets increasingly depend on access to lithium, nickel, cobalt, manganese, and graphite resources.

Technology innovations are materially influencing competitive positioning across the lithium-ion battery industry. Manufacturers are strengthening investment in battery chemistries that improve performance, thermal stability, and affordability. Lithium iron phosphate batteries continue gaining broader acceptance due to lower cost structures and enhanced safety profiles, particularly across electric mobility and stationary storage systems. At the same time, high-energy-density chemistries maintain strategic relevance for premium electric vehicles and industrial applications requiring longer operating cycles.

Download Free sample to learn more about this report.

Lithium-ion (LI-ion) BATTERY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 134.08 Billion

- 2026 Market Size: USD 206.98 Billion

- 2034 Forecast Market Size: USD 865.33 Billion

- CAGR: 22.85% from 2026–2034

- Asia Pacific dominated the lithium-ion battery market with a 56.10% share in 2025.

- Lithium Iron Phosphate (LFP) batteries are projected to hold 52.13% of the market in 2026.

- The automotive segment is expected to account for 42.52% of the global market in 2026.

Asia Pacific

Asia Pacific accounted for 56.10% of the global market in 2025, reaching USD 75.22 billion and projected to grow to USD 95.90 billion in 2026.

North America

North America represented 22.15% of the global market in 2025, valued at USD 26.69 billion and expected to reach USD 35.70 billion in 2026.

Europe

Europe held a 17.88% market share in 2025, generating USD 23.97 billion and projected to reach USD 29.37 billion in 2026.

U.S.

The lithium-ion battery market is projected to reach USD 34.23 billion in 2026.

Japan

The lithium-ion battery market is expected to reach USD 9.94 billion in 2025.

Read More

Market Dynamics

Market Trends

Growing Sales of Electric Vehicles to Mitigate Environmental Impact is an Emerging Trend in the Market

Electric vehicles have reduced the impact of climate change compared to internal combustion engines. Government bodies across the globe are approaching greener and pollution-free mobility as passenger and commercial electric vehicles are changing trends for future transportation, which will certainly boost lithium-ion battery market growth.

According to the International Energy Agency, new electric car registrations were 1.4 million in 2023, witnessing an increase of 40% compared to 2022. Electric vehicle companies, such as Tesla, have adopted these batteries in cars. Europe has strictly imposed emissions regulations & norms and implemented major public electric mobility transportation projects.

Rising Inclination towards Energy Projects to Drive Industry Growth

The growing interest in keeping the environment clean has encouraged the growth of renewable energy projects, such as solar power plants, nuclear power plants, and wind energy projects, contributing to the growing demand for lithium-ion batteries. These batteries are one of the favored options for renewable energy storage. They are widely seen as a main solution to compensate for the intermittency of wind and solar energy. Utilities worldwide have ramped up their storage capabilities using Li-ion supersized batteries, huge packs that can be stored anywhere between 100 and 800 megawatts (MW) of energy. In August 2023, California-based Moss Landing's energy storage facility is reportedly the world’s largest, with a total capacity of 750 MW/3000 MWh.

The lithium-ion battery market is increasingly shaped by structural changes in battery chemistry, manufacturing localization, and evolving end-use demand. Battery manufacturers are shifting investment toward diversified chemistry portfolios to balance performance, affordability, and supply chain resilience. Lithium iron phosphate battery adoption continues accelerating, particularly in mass-market electric vehicles and stationary energy storage solutions, due to lower material costs and improved thermal stability.

Regional battery production ecosystems are expanding rapidly as governments prioritize supply chain localization. North America, Europe, and the Asia-Pacific continue investing in gigafactory development to reduce dependence on concentrated battery imports and strengthen domestic manufacturing competitiveness. This transition is reshaping procurement behavior across raw material suppliers, cell manufacturers, and automotive sector stakeholders. Vertical integration strategies are increasingly common as companies seek tighter control over lithium, graphite, nickel, and cobalt sourcing.

Technology innovations remain central to market evolution. Battery developers continue prioritizing improvements in energy density, charging efficiency, and operational lifespan. Solid-state battery research is attracting increasing institutional attention due to potential advantages in safety and energy performance, although commercialization timelines remain uncertain. At the same time, recycling technologies are becoming strategically important as battery markets seek sustainable approaches to raw material recovery and waste reduction.

The energy storage segment is emerging as a strong contributor to the lithium-ion battery market growth. Utilities and commercial operators increasingly deploy battery systems to stabilize renewable energy generation and improve grid flexibility. This trend is expected to strengthen as clean energy penetration rises and electricity networks require more responsive storage infrastructure.

Download Free sample to learn more about this report.

Market Drivers

Increased Adoption of Batteries in Power Grid and Energy Storage Systems Plays a Key Role in the Market

Implementing strict government regulations to regulate rising pollution levels enhances the industries that use these batteries. The power industry is working to produce and store renewable energy for the future. Low cost, discharge rate, and minimal installation space are key factors driving the adoption of Li-ion batteries in smart grid and energy storage systems. Since these batteries are more resistant to high temperatures, they are ideal for use in remote areas and thermal control applications. For instance, in June 2024, GS Yuasa Corporation received orders for lithium-ion battery storage systems with a capacity of 50 MWh from Tsunokobaru Power Storage Station from Chiyoda Corporation.

Declining Prices of Li-ion Batteries Have Catalyzed Their Adoption in Various Sectors

Traditionally, the major factor that hampered the adoption of these batteries from 1990 was their price. Li-ion batteries contain many components, and the main element of any Lithium-ion battery (LIB) is its cell, which accounts for 50% of its cost. However, recent developments by lithium-ion battery manufacturing companies have helped decrease the prices of these batteries, which are also predicted to decline in the coming years. The declining prices of parts and the adoption of advanced technologies to increase battery capacity are key factors that have led to the rise in the adoption of lithium-ion batteries.

Growth in the lithium-ion battery market is strongly supported by accelerating electric vehicle adoption and increasing investment across the automotive sector. Governments continue strengthening emissions regulations and offering policy incentives aimed at encouraging electric mobility. These initiatives are increasing vehicle electrification rates and strengthening long-term demand visibility for lithium-ion batteries across passenger and commercial transportation categories.

Expanding renewable energy deployment is another significant growth catalyst. Energy storage solutions are increasingly essential to stabilize intermittent solar and wind generation. Grid operators and utilities continue investing in large-scale battery systems to support energy balancing requirements, reduce transmission inefficiencies, and strengthen electricity reliability. This transition materially expands commercial demand for advanced battery technologies.

Consumer electronics continue contributing to market size expansion. Smartphones, wearable devices, laptops, and connected electronics increasingly require higher energy density batteries with improved durability and faster charging capabilities. Battery manufacturers continue investing in product optimization to meet changing performance expectations across consumer applications.

Market Restraints

Growing Demand for Substitute Batteries is Hindering Market Growth

The increasing demand for other batteries, such as lead-acid batteries, sodium-nickel chloride, flow batteries, and lithium-air batteries, in consumer electronics, electric vehicles, and energy storage systems is projected to hinder the growth of these batteries. Moreover, continuous technological advancement in battery technology threatens the dominance of lithium-ion batteries in the market.

Sodium-ion batteries are emerging as the most promising alternative to lithium batteries. For instance, in November 2024, JAC launched an electric vehicle powered by sodium-ion batteries in China. Furthermore, in May 2024, the Guangxi branch of China Southern Power Grid announced the development of a sodium-ion battery energy storage station with a capacity of 100 MWh while generating 73 million kWh of clean energy per year. Such instances pose a major restraint to adopting lithium-ion batteries in the end-user industries.

The lithium-ion battery market continues facing structural constraints related to raw material concentration, supply chain vulnerabilities, and manufacturing capital intensity. Dependence on lithium, cobalt, nickel, and graphite exposes battery manufacturers to procurement disruptions and commodity price volatility. Concentrated mining activity in a limited number of countries creates supply security concerns, particularly as demand accelerates across the automotive sector and energy storage solutions markets.

Raw material price fluctuations remain a significant challenge for profitability and long-term procurement planning. Unexpected changes in lithium or nickel pricing can materially influence battery production costs, creating uncertainty for manufacturers and downstream users. Volatile pricing environments often delay purchasing decisions or alter product strategies among automotive and industrial buyers.

Manufacturing expansion also requires substantial capital investment. Gigafactory development involves significant infrastructure spending, advanced automation systems, and long commissioning timelines. Smaller manufacturers and SMEs may struggle to compete against vertically integrated market leaders with stronger financial capabilities and established supply agreements.

Geopolitical tensions introduce additional operational risks. Trade restrictions, export controls, and localized sourcing mandates may disrupt established supply chains and increase operating costs. Although long-term fundamentals remain favorable, these structural barriers continue influencing lithium-ion battery market growth trajectories and investment decisions.

Market Opportunities

Increasing demand for Lithium-ion batteries in the Automotive industry provides a Huge Opportunity for Market Growth.

The rising popularity of electric vehicles powered by lithium-ion batteries is expected to pose lucrative growth opportunities for market players operating in the Lithium-ion battery market. According to the International Energy Agency, approx 14 million new electric cars were registered in 2023, which brought the total number to 40 million electric vehicles globally. Moreover, electric car sales increased by 3.5 million in 2023, a 35% year-on-year increase from 2022. This trend indicates the surging demand for electric vehicles, which is also expected to propel the growth of the lithium-ion battery market shortly.

The lithium-ion battery market presents opportunities through accelerating electrification, localized manufacturing, and expanding clean energy infrastructure. Electric mobility remains one of the strongest opportunity areas as vehicle manufacturers continue increasing battery-electric product portfolios. Demand for lithium-ion batteries is expected to strengthen as governments intensify decarbonization initiatives and transportation electrification targets.

Energy storage solutions represent another substantial opportunity segment. Utilities, commercial facilities, and industrial operators increasingly deploy battery systems to improve grid resilience and manage renewable energy intermittency. Growing electricity demand and rising solar and wind integration continue to strengthen long-term demand visibility for stationary battery storage infrastructure.

Lithium iron phosphate battery technologies present particularly attractive growth potential. Their lower cost profile and improved safety characteristics are expanding adoption across electric buses, entry-level passenger vehicles, and grid storage systems. Battery manufacturers continue increasing production capabilities to address this evolving market preference while maintaining cost competitiveness.

Battery recycling and circular economy initiatives are also emerging as important commercial opportunities. Companies investing in raw material recovery technologies may strengthen supply resilience while reducing dependency on newly mined resources. Recycling ecosystems increasingly attract institutional interest due to sustainability priorities and long-term material security considerations.

Market Challenges

Scarce Resource Availability is Expected to Create Challenges for the Market

Lithium-ion battery production heavily relies on limited resources such as cobalt, lithium, and nickel, which increases concern about availability and geopolitical risks. The factor mentioned earlier will create a major challenge for lithium-ion battery manufacturers to secure as demand for lithium-ion batteries increases, driven by the introduction of new battery technologies in the consumer electronics and automotive industries.

Moreover, scaling up production to meet demand from end-use industries such as renewable energy storage, automotive, and others poses a major challenge for lithium-ion battery manufacturers while catering to market demand and dealing with scarce raw material availability.

IMPACT OF COVID-19

The COVID-19 pandemic affected the growth of this market during 2020. The outbreak of COVID-19 has restricted the supply of batteries. The key battery component is mainly available in the Asia Pacific, but the pandemic has over-exposed the dependency on raw materials in the region. Lithium and cobalt serve as key functional elements in battery cathodes and electrolytes. China dominates the production of components and controls approximately 80% of the global supply chain of these materials. Many countries have imposed travel restrictions, which have impacted the flow of raw materials, and many power plants have been shut down worldwide, affecting the market.

Segmentation Analysis

By Type Analysis

Lithium Iron Phosphate Batteries are Set to Lead the Market

Based on type, the market is segmented into lithium cobalt oxide, lithium iron phosphate, lithium nickel cobalt aluminum oxide, lithium manganese oxide, lithium nickel manganese cobalt, and lithium titanate oxide.

Lithium Cobalt Oxide (LCO)

Lithium cobalt oxide accounted for a major share in 2020 due to its wide adoption in mobile phones, laptops, cameras, and other modern electronic gadgets. Lithium cobalt oxide batteries continue to maintain relevance within the lithium-ion battery market, particularly across compact consumer electronic devices requiring high energy density and lightweight performance.

Although the chemistry has gradually lost share in electric mobility systems, lithium cobalt oxide remains strategically important for portable electronics, where efficiency and compactness strongly influence purchasing behavior. Smartphones, tablets, laptops, wearable devices, and digital consumer products remain the primary demand centers.

Consumer electronics manufacturers continue prioritizing batteries capable of supporting extended device performance and smaller product form factors. Lithium cobalt oxide batteries remain well-positioned due to strong energy density characteristics and stable operating performance in compact applications. Premium electronic products increasingly depend on battery systems that balance durability with reduced charging frequency.

However, cobalt dependency remains a structural challenge. Supply chain concentration and raw material volatility continue to affect production economics. Sustainability concerns surrounding cobalt sourcing are also influencing procurement strategies among technology manufacturers and institutional investors.

Lithium Iron Phosphate (LFP)

Lithium iron phosphate batteries accounted for the fastest-growing segment due to their properties, such as long life span, lightweight, and providing excellent safety for products. The segment is expected to hold 52.13% of the market share in 2026. The lithium iron phosphate segment is projected to exhibit a CAGR of 16.70% during the forecast period.

Lithium iron phosphate batteries continue strengthening their position within the lithium-ion battery market due to affordability, thermal stability, and longer operational lifespan. The chemistry increasingly benefits from lower dependence on expensive raw material inputs such as cobalt and nickel, making it commercially attractive for battery manufacturers focused on cost competitiveness. Demand remains particularly strong across electric mobility systems and stationary energy storage solutions.

The automotive sector continues to accelerate the adoption of lithium iron phosphate batteries, especially in mass-market electric vehicles and commercial fleets. Vehicle manufacturers increasingly prioritize affordability and safety for large-scale deployment, strengthening lithium iron phosphate demand across passenger and commercial mobility systems. Electric buses and logistics fleets also increasingly rely on LFP systems due to predictable operating performance and lower lifecycle costs.

Energy storage solutions remain another important application area. Utility operators increasingly deploy LFP batteries to stabilize renewable electricity generation and support energy balancing requirements. Their longer cycle life and strong thermal resilience make them particularly suitable for grid infrastructure and industrial backup systems.

Nickel Manganese Cobalt (NMC)

Nickel manganese cobalt batteries remain strategically important within the lithium-ion battery industry due to strong energy density performance and extended driving range capabilities. Premium electric vehicles continue to represent a major demand center, as automotive sector participants prioritize battery systems capable of supporting longer operational cycles and high-performance requirements.

Battery manufacturers continue adjusting nickel and cobalt ratios to improve affordability while maintaining energy efficiency. This transition reflects broader efforts to reduce dependence on expensive and supply-constrained raw material inputs without compromising battery performance. Manufacturers increasingly pursue chemistry improvements aimed at improving charging speed and operating stability.

Industrial systems and specialized mobility applications also contribute to segment growth. Robotics, premium electronics, and energy-intensive systems increasingly favor NMC chemistry because of strong energy-to-weight efficiency and compact performance characteristics. However, production costs remain higher than those of lithium iron phosphate systems, influencing commercialization strategies.

Nickel Cobalt Aluminum (NCA)

Nickel cobalt aluminum batteries maintain strategic relevance due to exceptionally high energy density and superior operational performance. Premium automotive manufacturers continue relying on NCA chemistry to improve electric vehicle range while maintaining lightweight system architecture. These advantages remain important for performance-oriented electric mobility systems.

The automotive sector remains the principal consumer of NCA batteries. High-end vehicle manufacturers prioritize longer driving range and faster charging performance to strengthen market differentiation. Battery systems using NCA chemistry continue to support advanced mobility applications where energy efficiency remains a primary purchasing consideration.

To know how our report can help streamline your business, Speak to Analyst

By Application Analysis

Growing Demand for EVs or HEVs to Lead Lithium-ion Battery Market

By application, the market is segmented into automotive, consumer electronics, energy storage systems, industrial, and others.

Automotive

The automotive sector is expected to be the dominating application for Li-ion batteries. The automotive segment is projected to dominate the market with a share of 42.52% in 2026. The rising awareness about the benefits of battery-operated vehicles and increasing prices of petrol and diesel, specifically in the Asia Pacific, North America, and Europe, has attracted consumers to these electric or hybrid vehicles.

The automotive sector remains the largest and fastest-growing application segment within the lithium-ion battery market, supported by accelerating electric vehicle adoption and expanding government decarbonization policies. Passenger vehicles, commercial fleets, electric buses, and specialized mobility systems continue increasing battery demand at scale. Automotive manufacturers increasingly prioritize battery efficiency, affordability, and charging performance to improve market competitiveness.

Battery-electric vehicle adoption continues to strengthen demand visibility across global battery markets. Governments are increasingly implementing emissions standards, financial incentives, and electrification policies to reduce dependence on internal combustion technologies. These initiatives materially strengthen lithium-ion battery market growth across passenger mobility ecosystems.

Battery manufacturers continue scaling production capabilities to address rising automotive sector demand. Strategic partnerships between vehicle manufacturers and battery suppliers are becoming increasingly common as companies seek supply continuity and greater control over raw material procurement. Vertical integration strategies are also expanding to reduce exposure to supply chain risks and pricing volatility.

Consumer Electronics

The consumer electronics sector is considered to be the fastest-growing application for lithium-ion batteries. The continuous development in the consumer electronics sector has led to an increase in the adoption of lithium-ion batteries in these applications. They offer multiple advantages such as high power capacity, reduced pollution, and increased safety.

Consumer electronics continue to represent one of the most established application segments within the lithium-ion battery market, supported by sustained global demand for smartphones, laptops, tablets, wearable devices, gaming systems, and portable digital electronics. Device manufacturers increasingly prioritize compact battery systems capable of supporting longer operational life, faster charging speeds, and reduced product weight. This demand continues to strengthen reliance on high-performance lithium-ion technologies across global electronics supply chains.

Battery manufacturers continue investing in technology innovations that improve energy density and thermal efficiency for compact devices. Premium electronics brands increasingly require battery systems that support advanced processors, high-resolution displays, and continuous connectivity without materially increasing device size. Lithium cobalt oxide and nickel-based chemistries continue to maintain strong relevance due to their ability to deliver higher energy output within smaller physical footprints.

Replacement cycles and growing digitalization trends continue supporting market growth. Rising consumer preference for connected ecosystems, artificial intelligence-enabled devices, and smart wearables further increases battery consumption intensity. Manufacturers increasingly focus on charging optimization and lifecycle improvements to strengthen product competitiveness.

Energy Storage

Energy storage solutions represent a rapidly expanding application segment within the lithium-ion battery market, supported by increasing renewable energy deployment and rising grid reliability requirements. Utility operators and commercial facilities increasingly deploy battery systems to balance intermittent solar and wind generation while improving electricity system flexibility. This trend materially strengthens demand for scalable battery infrastructure.

Grid modernization efforts continue to accelerate investment in large-scale storage systems. Energy storage enables electricity providers to stabilize supply, reduce curtailment, and improve power distribution efficiency during peak consumption periods. Lithium-ion batteries increasingly function as strategic infrastructure supporting energy transition objectives and long-term grid resilience.

Commercial and industrial facilities also continue increasing battery adoption to reduce energy costs and improve operational continuity. Backup power systems and demand response capabilities are becoming more important across manufacturing, healthcare, telecommunications, and data infrastructure environments. These systems increasingly rely on lithium-ion batteries due to performance efficiency and modular scalability.

Battery manufacturers continue improving chemistry optimization to increase storage duration and operational durability. As renewable electricity penetration rises globally, demand for advanced energy storage solutions is expected to strengthen significantly, improving long-term market visibility.

Industrial

Industrial applications continue contributing meaningfully to the lithium-ion battery market share, supported by growing electrification across manufacturing systems, robotics, warehousing, mining, and heavy industrial equipment. Companies increasingly deploy battery-powered systems to improve operational efficiency, reduce emissions intensity, and strengthen workplace automation capabilities.

Material handling systems, including forklifts and warehouse automation equipment, represent major adoption categories. Industrial operators increasingly prefer lithium-ion batteries due to reduced maintenance requirements, longer lifespan, and faster charging performance compared with traditional lead-acid systems. Manufacturing facilities increasingly integrate battery-powered automation to strengthen productivity and operational consistency.

Mining and construction equipment are also gradually transitioning toward electrified systems. Operators continue evaluating battery technologies capable of reducing fuel dependency and supporting sustainability targets. Industrial electrification remains especially attractive in regions prioritizing emissions reductions and energy efficiency improvements.

Regional Insights

The market has been studied geographically across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia-Pacific Lithium-ion Battery Market Analysis

Presence of a Large Automotive Sector in the Region to Drive Market Growth

Asia Pacific is expected to dominate the lithium-ion battery market during the forecast period. Asia Pacific contributed 56.10% to the global market in 2025, with a valuation of USD 75.22 billion, and is projected to reach USD 95.9 billion in 2026. China and Japan are considered the world's largest markets for electric vehicles. The automotive sector is widely adopting lithium-ion batteries. In addition, the growing demand for smartphones, laptops, and other electronic devices in various countries, such as China, India, Japan, and Singapore, is expected to expand the market in the region.

Asia-Pacific dominates the global lithium-ion battery market share due to strong manufacturing ecosystems, abundant processing capacity, and rising electric mobility demand. China, Japan, and South Korea remain major battery production centers. Rapid industrialization, energy storage expansion, and increasing consumer electronics demand continue to support sustained market growth across regional battery markets.

Japan Lithium-ion Battery Market:

Japan maintains a strong market position through advanced battery technology innovations and established manufacturing expertise. Battery manufacturers continue focusing on high-performance lithium-ion technologies for the automotive sector and consumer electronics applications. Investment in research and development, energy efficiency improvements, and battery recycling continues to support long-term industrial competitiveness and market stability.

China Lithium-ion Battery Market:

Favorable Regulatory Landscape Leads to Market Growth in the Country

The market in China is estimated to be USD 56.23 billion in 2026. Meanwhile, India is likely to hit USD 12.13 billion, and Japan’s market is expected to reach USD 9.94 billion in 2025. China leads the global lithium-ion battery market size due to its dominant battery manufacturing capacity, strong raw material processing capabilities, and accelerating electric vehicle demand. Government incentives and industrial policies continue to strengthen battery production ecosystems. Lithium iron phosphate battery adoption remains particularly strong, supporting cost-efficient electric mobility and energy storage solutions deployment.

China poses a lucrative market for lithium-ion battery manufacturers as the country has the world’s largest electric vehicle registration base. Moreover, China’s regulatory landscape also indicates promising growth opportunities for the lithium-ion battery market. In November 2024, the Chinese government passed its first energy law to achieve carbon neutrality by adopting renewable energy over traditional energy sources and storage systems. The aforementioned factors are expected to propel the demand for lithium-ion batteries in the country over the forecast period.

Asia Pacific Lithium-ion Battery Market Size, 2026 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Lithium-ion Battery Market Analysis

Rising Prominence of Renewable Energy Adoption in the Region Contributes to Market Growth

In 2025, North America represented USD 26.69 billion, accounting for 22.15% of the worldwide market, and is projected to grow to USD 35.7 billion in 2026. The North American lithium-ion battery market is growing with technological advancements and new policies to adopt renewable energy. Lithium-ion batteries pose a high potential for energy storage in off-grid renewable energy.

North America represents a strategically important lithium-ion battery market, supported by electric vehicle adoption, manufacturing localization, and rising investment in energy storage solutions. Governments continue encouraging domestic battery production to strengthen supply chains and reduce import dependency. Expanding gigafactory development and clean energy programs continue supporting long-term lithium-ion battery market growth across the region.

In November 2023, Our Next Energy (ONE) and GE Vernova announced a collaboration to advance battery energy storage solutions in the U.S. Moreover, the partnership will focus on integrating ONE’s lithium iron phosphate (LFP) cells in GE Vernova's Solar & Storage Solutions business projects nationwide. The growing focus of North American energy storage market players towards integrating lithium-ion batteries in their energy storage systems is expected to foster the demand for lithium-ion batteries over the forecast period in the region.

The U.S. Lithium-ion Battery Market:

Rising Adoption of Electric Vehicles Drives the Demand for Lithium-Ion Batteries in the U.S.

The U.S. market size is estimated to be USD 34.23 billion in 2026. The United States dominates the regional market size due to strong electric vehicle demand, expanding battery manufacturing, and rising investment in clean energy infrastructure. Automotive sector electrification continues to accelerate battery consumption across passenger and commercial mobility systems. Government incentives, domestic sourcing initiatives, and strategic partnerships continue to strengthen supply chains and production scalability.

The U.S. has been experiencing a significant surge in electric vehicle registrations. According to the International Energy Agency, the U.S. witnessed a 20% increase in electric car registrations in 2023 from 2022, with total electric car registrations of 1.4 million, which signifies the rapid growth in demand for lithium-ion batteries. Moreover, government initiatives such as clean vehicle tax credits also contribute to the growing demand for electric vehicles, which is expected to drive the demand for lithium-ion batteries in the country in the coming years.

Europe Lithium-ion Battery Market Analysis

Increasing Focus of Government Bodies on Greenhouse Gas Emissions in Europe has Supported The Market Growth.

The European market generated USD 23.97 billion in 2025, representing 17.88% of the global market landscape, and is expected to reach USD 29.37 billion in 2026. Several countries in the region, such as Germany, Argentina, France, and others, have set their target of having zero emissions of CO2 by 2050. This has boosted the usage of Li-ion batteries in the region.

Europe demonstrates strong lithium-ion battery market growth, supported by decarbonization goals, electric mobility expansion, and localized manufacturing strategies. Governments continue investing in battery production ecosystems to reduce supply chain concentration risks. Energy storage solutions and automotive sector electrification remain major growth catalysts, strengthening long-term market visibility across the regional battery industry.

In June 2021, the European Commission and the Battery European Partnership Association launched a public-private partnership to encourage research into smart battery technology in Europe, which is expected to positively impact the lithium-ion battery market in the upcoming years.

Germany Lithium-ion Battery Market:

Germany is projected to hit USD 7.14 billion, and France is likely to hold USD 2.75 billion in 2026. Germany maintains a leading position within Europe’s lithium-ion battery market due to strong automotive manufacturing capabilities and accelerating electric mobility adoption. Battery manufacturers continue strengthening partnerships with vehicle producers to improve procurement efficiency and local production capacity. Growing investment in battery recycling and technology innovations continues to support industrial competitiveness and market expansion.

United Kingdom Lithium-ion Battery Market:

The market value in the UK is expected to be USD 4.99 billion in 2026. The United Kingdom lithium-ion battery market benefits from increasing electric vehicle adoption, battery manufacturing investment, and clean energy policies. Energy storage solutions continue expanding across commercial and grid applications to improve electricity resilience. Strategic investment in localized battery production and recycling ecosystems remains important for strengthening long-term supply chain competitiveness.

On the other hand,

Latin America Lithium-ion Battery Market:

Growing Focus of Key Market Players on Innovations in the Battery System in the Region Leads to Market Growth

The market in Latin America reached USD 2.35 billion in 2025, representing 1.75% of total market revenue, and is projected to reach USD 2.72 billion in 2026. The battery system market players in Latin America are mainly focused on integrating lithium-ion batteries to support the adoption of renewable energy. In July 2023, AES Andes announced the development of the largest battery storage project in Antofagasta, Chile. The project is equipped with five-hour duration lithium batteries with a capacity of 560 MWh, which is co-located with 180MW of Solar PV Capacity. More such projects will increase the demand for lithium-ion batteries over the forecast period.

Middle East & Africa Lithium-ion Battery Market:

Countries' Increasing Interest in Renewable Energy is Expected to Offer Considerable Opportunities for Market Growth

The Middle East & Africa market was valued at USD 2.84 billion in 2025, accounting for 2.12% of global revenue. It is projected to reach USD 3.14 billion in 2026 and is expected to grow significantly as many countries in the region undergo large-scale construction activities and rapid urban development. This, in turn, leads to the growing need for industrial and construction power tools that use Li-ion batteries. Key nations actively operating in the region are South Africa and the Gulf Cooperation Council (GCC) countries. The GCC market size is estimated to be USD 1.30 billion in 2026.

Competitive Landscape

Market Players are Mainly Focused on Increasing Production Capacity to Sustain the Competition

This market is highly competitive, with many players operating in multiple regions. Moreover, market players are expanding activities through production innovation and the enhancement of production capacity. For instance, in January 2025, Neuron Energy launched a lithium-ion battery manufacturing facility covering an area of 5 acres located in Pune, India. Furthermore, prominent manufacturers such as Saft Group S.A., BYD Company, LG Chem, and A123 Systems have well-established supply chains and distribution networks that help these major players hold a noticeable position in the market.

List of Key Company Profiles:

- BYD Company (China)

- LG Chem (South Korea)

- Contemporary Amperex Technology Co. Ltd (CATL) (China)

- Samsung SDI (South Korea)

- Panasonic Corporation (Japan)

- BAK Power (China)

- Clarios (Germany)

- Toshiba Corporation (Japan)

- Hitachi (Japan)

- Automotive Energy Supply Corporation (Japan)

- A123 System (U.S.)

- Saft Group S.A. (France)

KEY INDUSTRY DEVELOPMENTS:

- In January 2025, International Battery Company (IBC) announced plans to commence lithium-ion battery production in Bengaluru, India, by the end of 2025. The company aims to export 20% of its production.

- In January 2025, Urja Mobility and Eastman announced a strategic partnership to develop and deploy lithium battery technologies in India's electric vehicle industry.

- February 2024 – Panasonic Energy Co., Ltd., a Panasonic Group Company, announced an agreement with H&T Recharge for the supply of lithium-ion battery cans in North America to increase its production of safe EV batteries.

- November 2023 – Toshiba Corporation announced the development of a new lithium-ion battery using a cobalt-free 5V-class high-potential cathode material. This battery can operate in various applications, from power tools to electric vehicles.

- June 2023 – Samsung SDI announced that the company has become the first lithium battery maker to accept carbon footprint labels from Carbon Trust. Carbon footprint measures greenhouse gas GHG emissions throughout a product's life cycle from production, raw materials, and distribution to disposal.

Investment Analysis and Opportunities

Investment in this market acts as an opportunity for the lithium-ion battery sector by fueling research & development for better battery technology and expanding production capacity to meet growing demand from EVs, energy storage, and other applications. This is expected to eventually lead to lower costs and increased accessibility, further accelerating market growth.

- In May 2024, Maxvolt secured an investment of USD 1.5 million to expand its lithium-ion battery production and research & development. Moreover, the company also announced that this investment will foster its sustainable energy solutions and strengthen its market reach by introducing lithium-ion batteries in the near future.

- In May 2024, Exide Industries announced an investment of USD 116.63 million in lithium-ion cell manufacturing projects in India. The project's first phase, with a capacity of 6GWh, is expected to be completed by 2025.

REPORT COVERAGE

The global lithium-ion battery market report delivers a detailed insight into the market and focuses on key aspects such as leading companies in the lithium-ion market. Besides, the report offers insights into the market trends & technology and highlights key industry developments. In addition to the factors above, the report encompasses several factors and challenges that contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.85% from 2026 to 2034 |

| Unit | Value (USD Billion) and Volume (kWh) |

| Segmentation |

By Type

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 134.08 billion in 2025.

The market will likely grow at a CAGR of 22.85% over the forecast period.

The market size of Asia Pacific stood at USD 26.69 billion in 2025.

Rising efforts to reduce the effects of high carbon emissions are the key factors driving market growth.

Some of the top players in the market are LG Chem, BYD Company, Samsung SDI, and others.

The global market size is expected to reach USD 865.33 billion by 2034.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us