Medium Voltage Switchgear Market Size, Share & Industry Analysis, By Product Type (Air-Insulated Switchgear, Gas-Insulated Switchgear and Solid/hybrid Insulated Switchgear) By Installation (Indoor and Outdoor), By Voltage Class (1 kV – 15 kV, 15 kV–27 kV, 27 kV–38 kV, and 38 kV–52 kV), By Switching Element (Vacuum Circuit Breaker, SF6 Circuit Breaker and Others), By End-User (Utilities, Industrial, Commercial & Institutional, Infrastructure and Renewables) and Regional Forecast, 2026-2034

Medium Voltage Switchgear Market Size and Future Outlook

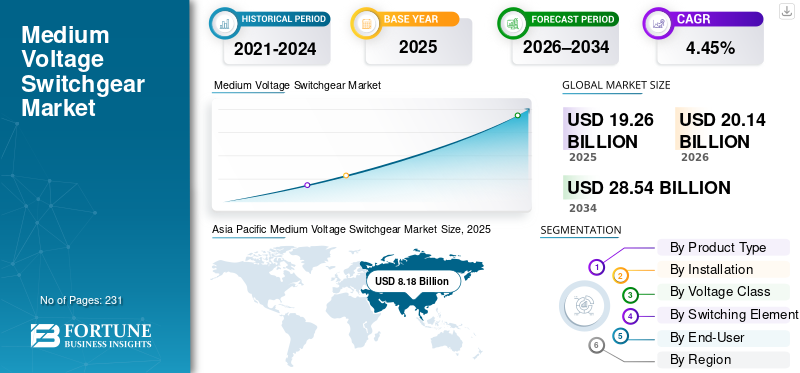

The global medium voltage switchgear market size was valued at USD 19.26 billion in 2025. The market is projected to grow from USD 20.14 billion in 2026 and is expected to reach USD 28.54 billion by 2034, exhibiting a CAGR of 4.45% during the forecast period. Asia Pacific dominated the medium voltage switchgear market with a market share of 42.47% in 2025.

Medium voltage (MV) switchgear refers to electrical equipment typically rated between 1 kV and 52 kV, used to control, protect and isolate power distribution circuits across utility, industrial, commercial and infrastructure applications. It is a core element of electrical distribution networks, ensuring operational safety, fault management and system reliability. Key performance parameters such as insulation medium (air, gas, or solid), arc-quenching technology, compactness, digital readiness and lifecycle durability, directly affect network uptime, safety and total cost of ownership.

Market growth is driven by grid modernization, rising electricity demand, renewable energy integration, and ongoing investments in urban and industrial infrastructure. Replacement of aging switchgear assets in developed markets, along with increasing adoption of compact, vacuum-based, and SF₆-free solutions, is accelerating demand. In parallel, the expansion of distributed energy resources, EV charging infrastructure, data centers and smart substations is boosting the need for intelligent, monitoring-enabled MV switchgear.

Leading players including ABB, Siemens, Schneider Electric, Eaton, Hitachi Energy, and Mitsubishi Electric are strengthening their positions through product innovation, digital protection integration, development of environmentally friendly insulation technologies, and localized manufacturing. Competitive strategies increasingly focus on sustainability compliance, space-efficient designs, predictive maintenance capabilities, and alignment with evolving grid standards, shaping the next phase of medium voltage switchgear deployment.

Download Free sample to learn more about this report.

Medium Voltage Switchgear Market Key Takeaways

- 2025 Market Size: USD 19.26 billion

- 2026 Market Size: USD 20.14 billion

- 2034 Forecast Market Size: USD 28.54 billion

- CAGR: 4.45% from 2026–2034

- Asia Pacific dominated the medium voltage switchgear market with a 42.47% share in 2025.

- The 1 kV–15 kV segment accounted for the largest market share of 54.69% in 2025.

- The renewables segment accounted for 7.77% during the forecast period.

North America

North America market valued at USD 3.77 billion in 2025.

Asia Pacific

Asia Pacific held 42.47% share in 2025, valued at USD 8.18 billion.

Europe

Europe market valued at USD 4.74 billion in 2025.

U.S.

The market in the U.S. was valued at USD 3.35 billion in 2025.

Japan

The market in Japan was valued at USD 1.04 billion in 2025.

Read More

Medium Voltage Switchgear Market Trends

Digital MV Switchgear and Condition Monitoring are Emerging Market Trends

Digital MV switchgear and condition monitoring are increasingly moving from premium offerings to mainstream specifications as utilities, data centers and process industries shift focus from upfront equipment cost toward lifecycle reliability and measurable downtime reduction. Tighter uptime requirements, higher outage penalties, and constrained maintenance windows are driving demand for switchgear capable of continuously monitoring parameters such as temperature rise, breaker operations and insulation or partial discharge activity, enabling condition-based rather than time-based maintenance. As a result, MV switchgear is evolving into an active, data-generating asset that improves fault visibility, enhances worker safety, and extends equipment life, making the operational ROI compelling even in cost-sensitive projects. OEM strategies reinforce this shift, as manufacturers increasingly embed sensors and digital-ready protection as standard features.

For instance, in March 2025, Schneider Electric launched its EcoStruxure Service Plan for medium-voltage switchgear, explicitly addressing customer demand for partial discharge monitoring and condition-based maintenance, underscoring the transition toward digital MV switchgear as a default rather than a premium option.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Smart Grid Expansion and Critical-Load Electrification are Lifting MV Switchgear Demand

Demand for MV switchgear is rising as utilities reinforce distribution networks and as high-uptime loads (especially data centers and critical infrastructure) add new capacity that requires dependable MV distribution and protection. Medium voltage switchgear market growth is driven by renewable interconnections and distribution automation programs, which increase the number of feeders, ring main units, and substation bays required per incremental MW added to the grid. In many markets, replacement of aging switchgear fleets is occurring in parallel with expansion, as utilities prioritize reliability and safety performance under higher load volatility. For instance, in March 2024, Schneider Electric announced a USD 140 million investment to expand U.S. manufacturing for custom electrical switchgear and medium-voltage power distribution products, explicitly linking the expansion to critical infrastructure and surging data center demand, a direct indicator of sustained order momentum.

Market Restraints

Long Lead Times And Capacity Bottlenecks Can Delay Project Commissioning And Revenue Conversion

Even with strong order pipelines, MV switchgear deliveries are often constrained by extended lead times, component availability and factory throughput, making procurement and project schedules harder to lock. For utilities and EPCs, this can translate into delayed substation energization, phased commissioning and higher working-capital exposure as projects wait on primary equipment. Specification rigidity (utility-approved vendor lists, strict type-test requirements, and site-specific configurations) can further limit substitution options when lead times spike. Manufacturers are responding with capacity additions that implicitly validate the constraint. For instance, in March 2024, Schneider expanded in the U.S. expansion aiming to increase output for switchgear and MV distribution products, while Eaton’s broader manufacturing investment program (with major completions across 2024–2025) similarly reflects the need to expand supply capacity to serve electrification-driven demand.

Market Opportunities

Digital MV switchgear and condition monitoring is creating a higher-value upgrade cycle.

A major opportunity is the shift from time-based maintenance toward condition-based asset management, as operators prioritize uptime, safety, and asset life extension, and need early warnings for thermal issues, insulation degradation, and partial discharge activity. Digitalization also expands the value pool beyond hardware into services, analytics, and lifecycle support, raising switching costs once platforms are standardized across a fleet. Importantly, adoption is broadening from only top-tier substations to routine distribution deployments as sensors and connectivity become more “built-in” rather than custom-engineered. OEM launches show this moving into packaged, repeatable offers rather than one-off premium projects. For instance, in March 2025, Schneider Electric launched its EcoStruxure Service Plan for MV switchgear with partial discharge monitoring positioned around demand for condition-based maintenance—supporting the narrative that monitoring is becoming standardized. In parallel, ecosystem moves such as ACTOM–Exertherm’s March 2025 predictive maintenance solution announcement reinforce growing mainstream demand for always-on monitoring around MV electrical assets.

Market Challenges

SF₆-Free Transition and Digital Integration Raise Qualification Complexity and Slow Fleet-Wide Standardization

While SF₆-free and digital-ready switchgear platforms are advancing, adoption at scale is gated by utility qualification cycles, specification changes and integration requirements (communications architecture, cybersecurity expectations, and interoperability across mixed-vendor fleets). For SF₆-free designs, buyers often require additional validation on footprint, thermal behavior, altitude performance, maintenance practices, and long-term serviceability, especially in the 24–52 kV class where installed-base conservatism is high. For digital switchgear, challenges include integrating monitoring outputs into existing SCADA/asset management workflows and ensuring consistent data quality across sites. OEM portfolio actions underscore both momentum and the execution challenge. Siemens expanded its sustainable and digital MV switchgear range (including F-gas-free “blue GIS” primary distribution products), but such transitions typically require multi-year re-standardization and tender requalification before fleet-wide rollouts accelerate.

Segmentation Analysis

By Product Type

Air-Insulated Switchgear Leads Due to its Cost-Effectiveness and Ease of Maintenance

Based on product type, the market is segmented into Air-Insulated Switchgear (AIS), Gas-Insulated Switchgear (GIS), and solid/hybrid insulated switchgear.

Air-insulated switchgear continues to account for the largest medium voltage switchgear market share, supported by its cost-effectiveness, ease of maintenance, and widespread deployment across utilities, industrial facilities, and infrastructure projects, particularly in regions with ample space availability. AIS remains the preferred solution in conventional substations, industrial plants and outdoor installations, especially across emerging markets where cost sensitivity remains high.

Solid and hybrid insulated switchgear forms a smaller but strategically important segment of the market. These solutions are gaining traction as alternatives to SF₆-based systems, supported by tightening environmental regulations and growing emphasis on sustainability. Solid and hybrid insulation technologies offer enhanced safety, lower environmental impact and reduced maintenance requirements, positioning them as a key growth area in next-generation MV switchgear deployments. The solid & hybrid insulated switchgear market is expected to grow at a CAGR of 5.60% during the forecast period.

By Installation

Indoor Installations Dominate as Utilities and Industries Prioritize Safety, Compactness and Environmental Protection

Based on installation, the market is segmented into indoor and outdoor.

Indoor MV switchgear accounts for the largest share of the global market, driven by its extensive use in commercial buildings, industrial facilities, substations, data centers and transportation infrastructure. Indoor installations offer superior protection against environmental factors, enhanced personnel safety and better integration with automation and digital monitoring systems. The increasing deployment of smart substations and compact electrical rooms further reinforces the dominance of the segment.

Outdoor MV switchgear continues to play a critical role in utility distribution networks, renewable energy installations and remote infrastructure projects. Outdoor systems are particularly prevalent in transmission and distribution substations, wind and solar farms, and mining operations, where exposure to harsh environmental conditions necessitates ruggedized designs. While outdoor installations hold a smaller share compared to indoor systems, steady demand persists due to ongoing grid expansion and rural electrification initiatives. The outdoor MV switchgear segment is expected to grow at a CAGR of 3.99% during the forecast period.

By Voltage Class

1 kV–15 kV and 15 kV–27 kV Classes Anchor Demand as Distribution Networks Expand

Based on voltage class, the market is segmented into 1 kV–15 kV, 15 kV–27 kV, 27 kV–38 kV, and 38 kV–52 kV.

The 1 kV–15 kV segment accounted for the 54.69% share in 2025, reflecting its extensive use in secondary distribution networks, industrial plants, commercial buildings and infrastructure applications. This voltage class is fundamental to last-mile power distribution and continues to benefit from urban expansion, electrification of buildings and industrial capacity additions.

Higher voltage classes (38 kV–52 kV) account for smaller but steadily growing shares, primarily driven by renewable energy integration, large industrial complexes, and transmission-linked substations. These segments benefit from investments in high-capacity distribution networks and interconnection points for wind and solar power projects. The 38 kV – 52 kV is projected to grow at a CAGR of 5.35% during the forecast period.

By Switching Element

Vacuum Circuit Breakers Dominate as SF₆ Faces Regulatory and Sustainability Pressures

Based on switching element, the market is segmented into Vacuum Circuit Breakers (VCB), SF₆ circuit breakers, and others.

Vacuum circuit breakers account for the largest share of the global market and remain the preferred switching technology across most applications. High operational reliability, long service life, low maintenance requirements and suitability for frequent switching operations support their dominance. VCBs are widely adopted across utilities, industrial plants and infrastructure projects, and their compatibility with environmentally friendly designs further strengthens their market position.

SF₆ circuit breakers continue to hold a meaningful share, particularly in compact GIS applications where high dielectric strength is required. However, their growth is increasingly constrained by environmental concerns and regulatory pressure related to greenhouse gas emissions. While SF₆-based systems remain relevant in specific high-performance and space-constrained applications, their share is expected to gradually decline over the long term. The SF₆ circuit breakers are projected to grow at a CAGR of 2.83% during the forecast period.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Utilities Leads Due to Continuous Investment in Distribution Network Expansion

Based on end-user, the market is segmented into utilities, industrial, commercial & institutional, infrastructure, and renewables.

Utilities represent the largest share of the global market, supported by continuous investment in distribution network expansion, replacement of aging switchgear fleets and the modernization of substations to improve reliability and reduce outage risk. Utility-driven demand is structurally high as MV switchgear is a core requirement across primary and secondary distribution substations, feeder automation systems and grid reinforcement projects. In addition, utilities are increasingly prioritizing digital-enabled switchgear, condition monitoring and fault isolation capabilities to improve grid resilience and reduce operational costs, further reinforcing the segment’s leadership.

Renewables is the fastest-growing segment, supported by accelerating deployment of solar and wind farms, grid-connected energy storage integration and the expansion of renewable evacuation and interconnection infrastructure. MV switchgear is essential at collector substations, step-up transformer interfaces and grid tie points, and demand rises as renewable penetration increases across both utility-scale and distributed installations. In addition, the shift toward more complex grid architectures, where renewables require enhanced protection, switching frequency and monitoring, further strengthens MV switchgear adoption in this segment. The renewables segment accounted for 7.77% during the forecast period of 2021-2034.

Medium Voltage Switchgear Market Regional Outlook

By geography, the Market has been studied geographically across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

Asia Pacific Medium Voltage Switchgear Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America was valued at USD 3.77 billion in 2025, accounting for approximately 19.60% of the market. The region is supported by grid hardening and modernization programs, replacement of aging distribution assets, rising renewable interconnections and sustained investment in commercial/industrial electrification (data centers, manufacturing expansions, and critical infrastructure). North America also shows strong momentum in vacuum-based switching and digital/condition-monitoring-enabled MV switchgear, driven by reliability expectations, outage mitigation priorities and utility automation roadmaps.

U.S. Medium Voltage Switchgear Market

The U.S. market was estimated at USD 3.35 billion in 2025 and will be at USD 3.49 billion in 2026, supported by utility distribution capex, undergrounding and storm resilience projects, expansion of large-load customers (especially data centers), and continued buildout of renewable and storage interconnections.

Europe

Europe was valued at USD 4.74 billion in 2025, contributing approximately 24.63% of global revenues. This growth is driven by distribution modernization, accelerated renewable integration, substation refurbishment cycles and increasing demand for compact, high-reliability switchgear in dense urban grids. Europe also demonstrates strong structural demand for SF₆-reduction pathways (where applicable), increased adoption of vacuum switching and higher penetration of gas-insulated and solid/hybrid technologies for space-constrained installations and sustainability-led procurement.

Germany Medium Voltage Switchgear Market

Germany was at USD 0.99 billion in 2025 and USD 1.05 billion in 2026, supported by grid reinforcement programs, renewable evacuation capacity and industrial reliability upgrades. Higher-spec installations in industrial clusters and utility automation initiatives strengthen the adoption.

U.K. Medium Voltage Switchgear Market

The U.K. market reached at USD 0.69 billion in 2025 and will be at USD 0.71 billion in 2026, driven by distribution upgrades, reinforcement for renewables integration, and sustained investment in transportation and energy infrastructure. Compact indoor and retrofit-heavy demand patterns continue to shape procurement.

Asia Pacific

Asia Pacific is the largest region in 2025, valued at USD 8.18 billion, accounting for approximately 42.47% of global MV switchgear revenues. The region benefits from the highest concentration of grid expansion, rapid urbanization, sustained industrial capacity additions, and accelerated deployment of renewable generation and interconnection infrastructure. Asia Pacific also leads in volume demand for MV switchgear across utilities, infrastructure megaprojects and industrial parks, while gradually upgrading toward higher-reliability and more compact configurations in major metropolitan grids.

China Medium Voltage Switchgear Market

China remains the dominant contributor in Asia Pacific, reached at USD 3.19 billion in 2025 and will be valued at USD 3.33 billion in 2026, supported by distribution expansion, substation densification in urban networks, and sustained renewable integration requirements. Demand is reinforced by large-scale utility procurement cycles and ongoing upgrades of distribution reliability and automation.

India Medium Voltage Switchgear Market

India’s market was at USD 1.68 billion in 2025 and would be at USD 1.80 billion in 2026, reflecting continued momentum in distribution buildout, industrial growth, infrastructure electrification and renewable evacuation capacity. The market is also shaped by expanding indoor installations for commercial/industrial load centers and increasing substation deployments for network strengthening.

Japan Medium Voltage Switchgear Market

Japan was valued at USD 1.04 billion in 2025 and will be at USD 1.08 billion in 2026, supported by replacement-driven demand, high reliability requirements, and upgrades in utility and industrial power distribution systems. Preference for higher-performance, compact, and safety-oriented specifications supports stable value growth.

Latin America

Latin America was valued at USD 1.14 billion in 2025, contributing approximately 5.91% of global revenues. Targeted distribution upgrades, renewable project additions and steady industrial/infrastructure investment support the growth. Demand is typically project and tender-driven, with utilities and large industrial users anchoring procurement volumes.

Brazil Medium Voltage Switchgear Market

Brazil was at USD 0.51 billion in 2025 and will reach at USD 0.53 billion in 2026, supported by distribution reinforcement, renewables integration and industrial demand across mining and processing sectors.

Middle East & Africa

The Middle East & Africa were valued at USD 1.42 billion in 2025, accounting for approximately 7.39% of global revenues. The growth is led by grid expansion, substation buildouts, infrastructure development and increasing renewable additions in select markets. The region’s demand mix remains strongly influenced by utility procurement cycles and large-scale infrastructure programs, with a meaningful share of outdoor deployments due to climate and network topology.

GCC Medium Voltage Switchgear Market

The GCC market was estimated at USD 0.71 billion in 2025 and will reach at USD 0.74 billion in 2026, supported by grid modernization, new substation capacity, industrial expansions and renewable energy buildout. Compact, high-reliability solutions are increasingly prioritized for dense urban developments and critical infrastructure corridors.

KEY INDUSTRY PLAYERS

SF₆-Free Portfolio Expansion and Regional Manufacturing Localization Aid in Enhancing Competition

The medium voltage switchgear market is moderately fragmented, with a mix of large electrification OEMs and regional specialists competing across insulation technology roadmaps (SF₆-free vs. conventional), switching platforms (VCB dominance), compactness (GIS/RMU), digital integration, and lifecycle service capability. Competition is increasingly shaped by utilities’ and large industrial customers’ push for regulatory-compliant, low-emission switchgear and higher operational reliability, which is accelerating the transition toward SF₆-free and compact MV solutions and elevating the strategic importance of localized manufacturing, assembly, and qualification near major grid modernization programs.

List of Key Medium Voltage Switchgear Companies Profiled

- ABB (Switzerland)

- Schneider Electric (France)

- Siemens (Germany)

- Eaton (U.S.)

- GE Vernova (U.S.)

- Mitsubishi Electric (Japan)

- Toshiba (Japan)

- Hyundai Electric (South Korea)

- CG Power and Industrial Solution (India)

- Bharat Heavy Electrical Limited (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: ABB expanded its SF₆-free medium voltage switchgear manufacturing capacity in Europe, citing rising utility demand ahead of upcoming regulatory restrictions on fluorinated gases. The expansion reinforces how OEMs are accelerating SF₆-free portfolio localization to support utility tender requirements and reduce lead times for distribution network upgrades.

- August 2025: Schneider Electric announced additional production and engineering investments at its Leeds (U.K.) facility to support growing demand for SF₆-free Ring Main Units (RMUs) under its AirSeT™ platform. The move highlights how suppliers are aligning manufacturing footprints with regional grid modernization programs and sustainability-driven procurement.

- April 2025: Eaton launched an upgraded digitally enabled MV switchgear lineup for utility and industrial customers, integrating advanced condition monitoring and predictive maintenance features. This reflects the increasing convergence of digitalization and MV switching equipment to improve asset uptime and reduce lifecycle costs.

- February 2025: Hitachi Energy announced new orders for compact MV switchgear solutions supporting renewable energy integration and grid reinforcement projects in the Middle East and Asia. The projects highlight continued demand for high-reliability, space-efficient switchgear in renewable evacuation and infrastructure-led grid expansion.

- November 2024: Lucy Electric expanded its RMU production and testing capabilities to support rising demand from distribution utilities in Europe and the Middle East. The expansion emphasizes the importance of regional manufacturing scale and utility qualification depth in the increasingly tender-driven MV switchgear market.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects, including leading companies, product processes, and Porter’s Five Forces analysis. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.45% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Product Type

|

|

By Installation

|

|

|

By Voltage Class

|

|

|

By Switching Element

|

|

|

By End-User

|

|

|

By Region

|

Frequently Asked Questions

According to a Fortune Business Insights study, the market size was USD 19.26 billion in 2025 and will reach USD 28.54 billion.

The market is likely to grow at a CAGR of 4.45% over the forecast period (2026-2034).

By end-user, the utilities segment is expected to lead the market.

The market size of the Asia Pacific stood at USD 8.18 billion in 2025.

Grid expansion and “critical-load” electrification is lifting the demand for medium-voltage switchgear.

Some of the top players in the market include ABB, Eaton, and Schneider Electric among others.

- 2021-2034

- 2025

- 2021-2024

- 231

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us