Mining Waste Management Market Size, Share & Industry Analysis, By Source (Surface Mining and Underground Mining), By Waste Type (Solid Waste {Waste Rock, Tailings, Others} and Liquid Waste), By Commodity (Mineral Fuels, Iron, Ferro Alloys, Industrial Minerals, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

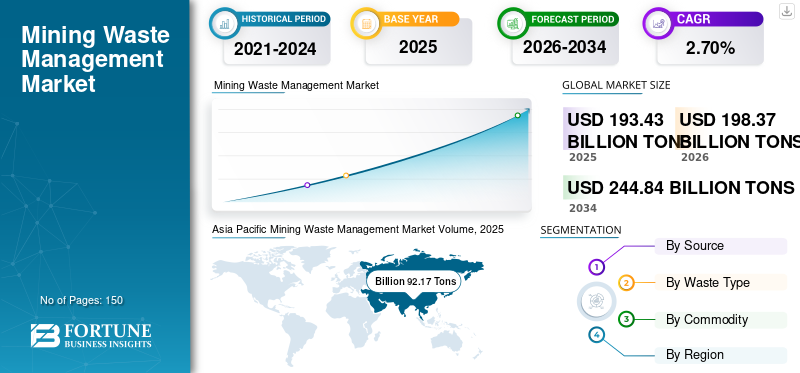

The global mining waste management market size was 193.43 billion tons in 2025 and is projected to grow from 198.37 billion tons in 2026 to 244.84 billion tons by 2034 at a CAGR of 2.70% during the forecast period (2026-2034). Asia Pacific dominated the mining waste management market with a market share of 47.60% in 2025. Moreover, the mining waste management market size in the U.S. is projected to grow significantly, reaching an estimated volume of 231.76 billion tons by 2032, driven by high mineral fuel mining exploration activities.

Mining waste consists of overburden, slurry, tailings, rock, and other discards. The amount of mining waste differs across countries and depends on the respective geographical structure, economic value of the ore, & metal and minerals demand in the market. Lower-grade ores are producing large quantities of mining waste, as compared to the higher grades. With increased mineral consumption globally, mining production has increased, and consecutively, high amounts of mining waste are produced. Due to the increasing problem of surface water pollution backed by strict environmental regulations, waste management in mines has gained significant importance.

The COVID-19 outbreak has resulted in an unprecedented economic and operational impact on the global mining industry. However, the mining industry partially resumed its operations, and the overall economic impact is slightly less than other manufacturing industries. Each region reacted differently in response to the COVID-19 outbreak. Many governments across developed and developing economies imposed partial or complete lockdown to avoid the spread of coronavirus.

The sudden lockdown led to supply chain disruption across the ecosystem. Some examples include Rio Tinto’s Oyu Tolgoi copper mine in Mongolia, Anglo American’s Quellaveco in Peru, the San Cristobal silver zinc-lead mine in Bolivia, and the Ambatovy nickel mine in Madagascar owned by Japan’s Sumitomo Corp. However, few of the countries such as Columbia and Chile excused mining sites from quarantine to limit the entire economy's major impact. The decrease in demand and prices of many minerals put a heavy toll on national economies such as Chile & Peru. Also, due to disruption in operation, especially in highly mining concentrated countries, affected the whole value chain and led to an increase in prices on account of shorter supply.

Download Free sample to learn more about this report.

GLOBAL MINING WASTE MANAGEMENT MARKET OVERVIEW

Market Size & Forecast:

- 2025 Market Size: 193.43 billion

- 2026 Market Size: 198.37 billion

- 2034 Forecast Market Size: 244.84 billion

- CAGR: 2.70% from 2026–2034

Market Share:

- Asia Pacific dominated the market in 2025 with a 47.60% share, reaching 92.17 billion tons.

- By source, surface mining was the largest segment due to its high waste generation.

- By waste type, solid waste led the market, with waste rock and tailings as key contributors.

- By commodity, mineral fuels held the major share at 83.7% in 2023, driven by coal, uranium, and petroleum mining.

Key Country Highlights:

- China: Accounted for over 24% of global mining production; major contributor in Asia Pacific.

- United States: Second-largest mining nation (12% global share); high mineral fuel mining supports growth.

- Russia: Major mining waste generator in Europe; top gold and coal producer in the region.

- Brazil: Second-largest iron ore producer; significant contributor to Latin American mining waste.

- South Africa: Rich in coal, gold, and platinum; key driver of waste management services in MENA.

Mining Waste Management Market Trends

Continued Interest in Mining Waste Co-disposal is a Prominent Trend

In the co-disposal technique, waste rock and fine tailings are combined and disposed systematically. The main aim behind this co-mixing is to improve the physical and chemical stability of the mining waste. Different co-disposal methods have been designed based on the degree of mixing and placement methods. Co-disposal possesses certain advantages over conventional or separate disposal methods. Tailing dams need not be constructed, which, in turn, saves space and minimizes maintenance costs. Also, co-disposal simplifies water consumption and wastewater management. Collectively, co-disposal techniques have a lower environmental impact. Asia Pacific witnessed a mining waste management market growth from USD 82.90 billion in 2022 to USD 86.00 billion in 2023.

Download Free sample to learn more about this report.

Mining Waste Management Market Growth Factors

Stringent Government Regulations on Mining Operations to Aid Growth

The government authorities such as the Environment Protection Agency (EPA) across each region, imposed strict regulations on mining operations and mining waste disposal. For instance, in the United States, the federal laws that regulate mining operations are National Environmental Policy Act (NEPA), Clean Air Act (CAA), Resource Conservation and Recovery Act (RCRA), Toxic Substances Control Acts (TSCA), Clean Water Act (CWA), and Comprehensive Environmental Response, and Compensation & Liability Act (CERCLA). These regulations force the mining operators to adopt safe and sustainable mining waste solutions.

Violation of non-fulfillment of such regulations leads to civil penalties. Similarly, the National Environmental Management Act 1998 (NEMA) is the framework of legislation regulating the environment in South Africa. It is framed along with environmental laws such as the National Water Act 36, National Environmental Management: Waste Act, etc. These regulations force mining operators to adopt safe and sustainable mining waste solutions. Violation of non-fulfillment of such regulations leads to civil penalties. Therefore, strict mining regulations are fueling the growth of the market.

Rising Environmental Concerns to Drive the Market Growth

Rising environmental concerns are driving the market as companies are now more conscious of their environmental impact and are taking steps to ensure sustainable and responsible mining practices. Proper waste management is crucial in preventing pollution and reducing the negative impact on ecosystems and communities surrounding mining sites. Therefore, companies in the industry are adopting a more proactive approach for dealing with this issue.

Environmental sustainability is a major driving force behind the mining waste management market growth. As people become increasingly aware of the impact of mining activities on the environment, there is a growing demand for sustainable and responsible mining practices. Mining waste management plays a crucial role in achieving this, as it helps to reduce the environmental impact of mining by properly managing the waste generated during the process. By implementing effective waste management strategies, mining companies can reduce their environmental footprint and improve their social license by demonstrating their commitment to sustainability.

RESTRAINING FACTORS

High Operating Cost to Hinder Mining Waste Management Market Growth

Disposing mining waste is a critical task and requires higher investment. It also consumes a considerable amount of power and energy. Handling hazardous mine waste, especially acid waste drainage, requires efficient operating equipment. Also, hazardous mine waste possesses a significant impact on human health. Therefore, to handle such waste material, highly skilled manpower and safety equipment are required. This increases the overall operating cost. However, with the adoption of smart mining waste technologies, the impact of this restraint is projected to become low during the forecast period.

Mining Waste Management Market Segmentation Analysis

By Source Analysis

Surface Mining Segment to Remain the Largest Source

Based on source, the market is divided into surface mining and underground mining segments.

Among these, in 2026, the surface mining segment will account for the largest share in the market, of 72.27%. This segment is further subdivided into open-pit, mountaintop removal, and strip mining. As compared to underground mines, surface mines produce large amounts of waste.

- For instance, waste rock production in the underground mines is typically 10% to 20% of the ore quantity. In contrast, waste rock production in open-pit mines is typically 2 to 10 times the ore quantity.

When ore deposits are critical to tapping from the surface, an underground mining technique is used. Due to higher operating costs, the underground mines are carefully operated to generate less amount of waste. The ore extraction capacity of the underground mines is generally less than the surface mines. Thus, underground mines generate fewer wastes as compared to open or surface mining.

By Waste Type Analysis

Solid Waste Segment to Dominate

Based on waste type, the market for mining waste management is segmented into solid waste and liquid waste.

Among these waste types, the solid waste segment holds the largest share of 94.92% in the market in 2026. This segment is further divided into waste rock, tailings, and others. The waste rock sub-segment held the largest share, followed by tailings. The quantity of waste rock generated depends upon the mine geometry, mining method, composition, & stripping ratio of mines.

- For instance, the stripping ratio of 3:1 means that thrice the quantity of waste rock needs to be mined to obtain one quantity of ore. The stripping ratio varies as per the different mineral commodities.

Tailings are fine sand remains that are found post valuable mineral separation. The amount of tailing is dependent upon the grades of the ore. Liquid mine waste is contaminated with harmful elements. The water released through different mining processes is acidic and can easily pollute the surface water. Therefore, mining wastewater is carefully monitored and treated before it is released into the environment.

By Commodity Analysis

To know how our report can help streamline your business, Speak to Analyst

Mineral Fuels Segment held Major Share

Based on commodity, the market is categorized into mineral fuels, iron, ferro alloys, industrial minerals, and others.

Among these, the mineral fuels segment accounts for the 81.33% of the market share in 2026. Mineral fuel waste consists of the waste generated during coal mining, lignite, uranium, natural gas, and other petroleum products. Mineral fuels became paramount to suffice the daily energy needs. With rapid industrialization, the demand for mineral fuels is increasing. Therefore, mineral fuel is highly mined, and new sites are explored to meet the rising demand. Due to the high stripping ratio, the waste generated during mineral fuel mining is more.

The others segment includes mining waste generated during the extraction of precious metal and non-ferrous metal. Owing to the higher demand for precious metals such as gold, silver, rhodium, palladium, platinum, and non-ferrous metals such as bauxite, copper, aluminum, zinc, lead, and rare earth metals. The production of these metals and minerals is increasing at a higher rate. Thus, the others segment is expected to grow at a higher CAGR.

REGIONAL INSIGHTS

Based on region, the global market is categorized into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Mining Waste Management Market Volume, 2025 (Billion Tons)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific market accounted for USD 92.17 Bn Tons in 2025, representing 47.60% of the global industry, and is expected to reach USD 92.27 Bn Tons in 2026. Due to high-capacity mines, the region is expected to exhibit a CAGR of 3.5% during the forecast period. China held the major share in the Asia Pacific owing to the presence of large capacity mines. China is the leading mining nation globally and accounts for over 24% share in the global mining production. In Asia Pacific, Australia is the second-largest individual contributor of mining waste. It ranked fourth among the top mining countries globally and accounted for around a 7% share globally. The Japan market is projected to reach USD 15.48 billion by 2026, the China market is projected to reach USD 53.41 billion by 2026, and the India market is projected to reach USD 11.5 billion by 2026.

Europe

In 2025, Europe generated USD 32.16 Bn Tons, contributing 16.60% to global market revenue, and is projected to grow to USD 32.53 Bn Tons in 2026. Owing to the strict mining regulations, it is a well-established market for mining waste management. In Europe, Russia is the major mining waste generating country, followed by Germany. In the global mining production, the country held the third position, contributing around 9% share. Also, it is the third-largest gold producer in the world. 83% of total European gold is sourced from Russia. Russian coal mines contribute around 14% to global coal production. Therefore, it is expected to maintain its dominance in the market during the forecast period. The UK market is projected to reach USD 17.04 billion by 2026, while the Germany market is projected to reach USD 2.24 billion by 2026.

North America

North America maintained a strong presence in the global market, reaching USD 26.44 Bn Tons in 2025, accounting for 13.70% share, and is expected to reach USD 26.99 Bn Tons in 2026. In North America, the U.S. is a leading mining waste-generating country. Also, the country's high mineral fuel mining exploration activities are fueling the demand for mining waste management systems. The U.S. is the second-largest mining nation in the world and accounts for around 12% share. Canada ranks among the top ten mining production countries globally, which, in turn, represents potential growth opportunities for the market.

Rest of The World

Latin America contributed 7.50% to the global market in 2025, with a valuation of USD 14.43 Bn Tons, and is projected to reach USD 14.85 Bn Tons in 2026. In Latin America, Chile, Peru, Brazil, and Mexico are the key countries driving the growth of the mining and waste management industry. Peru has the world’s largest silver reserves, while Mexico ranks sixth. These two countries, together with Chile, Bolivia, and Argentina, hold around half the worldwide silver production in 2023. Mexico, Peru, & Brazil ranks amongst the leading gold-producing economies. Chile ranks top in copper production. In bauxite production, Brazil ranks amongst the top five. Brazil was the second-largest iron ore mine producer, with half a billion tons produced. Such things represent the potential of mining waste management in these countries. With an increase in production, demand for waste management services is expected to increase in the region.

- The U.S. market is projected to reach USD 22.07 billion by 2026.

The main contributions to the supply of mineral commodities were crude petroleum & condensate (32.4 %), helium (31.1%), phosphate rock (20.3%), natural gas (21.5%), ammonia (12.2%), aluminum (primary) (about 11%), gypsum (9.9%), potash (7.2%), cement (7.1%), petroleum refinery product (3.8%), chromite (2.6%), and crude steel (2.3%) in the MENA region. Iran & Saudi Arabia are the main producers of bauxite; Iran, Oman were the only manufacturers of chromite; Egypt, Saudi Arabia, Iran are leading gold producers in the region. The mining sector has been a key element of the South African economy. Gold, diamonds, platinum & coal are well-known among the minerals & metals. South Africa also has chrome, vanadium, titanium & other essential minerals.

In 2025, Middle East & Africa represented USD 28.24 Bn Tons, accounting for 14.60% of the worldwide market, and is projected to grow to USD 28.24 Bn Tons in 2026.

List of Key Companies in Mining Waste Management Market

Leading Companies Focus on Acquisition and Expansion Strategies to Garner Market Growth

Acquisition of smaller enterprises and expansion are important strategies used by the leading companies to maintain their positions in the market. For instance, in July 2020, EnviroServ announced a new microencapsulation plant commission to manage high moisture waste to comply with new legislation.

The introduction of new legislation since August 2019 for the prohibition on disposal of high moisture content waste in landfills has led EnviroServe to develop various options to treat the waste into immobile solids. One such methodology developed by the company is microencapsulation. The process starts with obtaining a waste sample from a customer, analyzed in EnviroServ's in-house laboratory. A novel method for treating the moisture content in the waste by converting the waste into an immobile solid that complies with legislation has been developed. To commercialize this process, the company commissioned its new plant with a capacity of treating 1000 m3 of waste per day.

LIST OF KEY COMPANIES PROFILED:

- Enviro-Serve Inc. (South Africa)

- Hatch Ltd. (Canada)

- Veolia Environnement S.A. (France)

- Tetronics International (UK)

- Golder Associates Inc. (Canada)

- John Wood Group PLC (UK)

- Ramboll Group (Denmark)

- Tetra Tech, Inc. (USA)

- Ausenco (Australia)

- Seche Environnement Company (France)

- Cleanway Environmental Services (Australia)

- Aevitas (Canada)

KEY INDUSTRY DEVELOPMENTS:

- September 2022 – SUEZ and their partner companies, such as African Infrastructure Investment Managers (AIIM) and Royal Bafokeng Holdings (RBH), completed the acquisition of EnviroServ Inc. This acquisition would help SUEZ capture more market share in industrial and municipal waste treatment sectors.

- March 2019 – Seche Environnement Group acquired Interwaste Holdings Limited. With this acquisition, Seche Environnement Group entered the South African waste market. The expertise of both companies is aiming to support the southern African region in developing its circular economy.

- June 2018 – Cleanaway acquired Toxfree Solutions Limited and Daniel Health to become Australia’s largest environmental, industrial, and waste management company. Under this acquisition, both companies were aiming to develop more sustainable waste management in Australia.

REPORT COVERAGE

The global market research report provides both qualitative & quantitative insights into the mining waste management industry across the world. Quantitative insights include mining waste management market sizing in terms of volume (billion tons) across each segment, sub-segment, and region profiled in the study's scope. Also, it provides the market share analysis and growth rates of the segment, sub-segments, and key counties across each region. The qualitative insight covers an elaborative market analysis about the drivers, restraints, growth opportunities, and key trends related to the market. The competitive landscape section covers detailed company profiles of the key players operating in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

|

Study Period |

2021-2034 |

|

|

Base Year |

2025 |

|

|

Estimated Year |

2026 |

|

|

Forecast Period |

2026-2034 |

|

|

Historical Period |

2021-2024 |

|

|

Unit |

Value (USD Billion) |

|

|

Growth Rate |

CAGR of 2.70% from 2026 to 2034 |

|

|

Segmentation |

By Source

|

|

|

By Waste Type

|

||

|

By Commodity

|

||

|

By Geography

|

||

Frequently Asked Questions

Fortune Business Insights says that the global market size was 193.43 billion tons in 2025 and is projected to reach 244.84 billion tons by 2034.

Growing at a CAGR of 2.70%, the market will exhibit significant growth during the forecast period.

The surface mining segment is expected to be the leading source segment in this market.

The increasing initiatives by the leading companies and strict government regulations are the key factors driving the global market.

Asia Pacific held the highest market share in 2025.

Key players operating in the market are Enviro-Serve Inc., Hatch Ltd, Veolia Environnement S.A., Tetronics International, Golder Associates Inc., John Wood Group PLC, Ramboll Group, Tetra Tech, Inc., Ausenco, Seche Environnement Company, Cleanway Environmental Services, and Aevitas.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us