Nuclear Waste Management Market Size, Share & Industry Analysis, By Waste Type (Low-Level Waste, Intermediate-Level Waste, and High-Level Waste), By Service (Collection & Handling, Interim Storage, Transportation & Logistics, Processing & Conditioning, and Final Disposal), By End User (Nuclear Power Utilities, Government/Defense, and Others), and Regional Forecast, 2025-2032

Nuclear Waste Management Market Size and Future Outlook

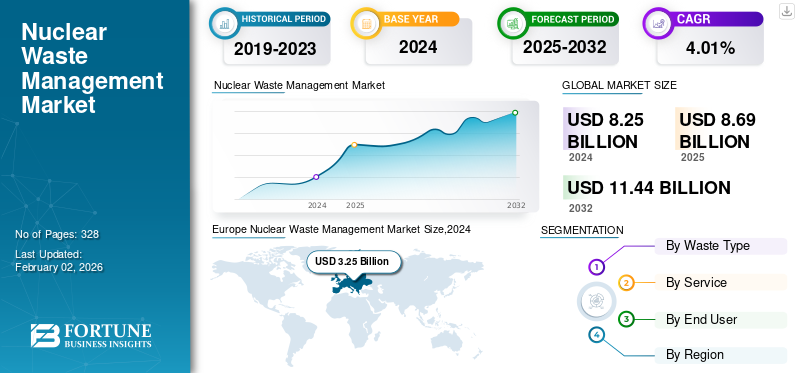

The global nuclear waste management market size was valued at USD 8.25 billion in 2024. It is projected to grow from USD 8.69 billion in 2025 to USD 11.44 billion by 2032, exhibiting a CAGR of 4.01% during the forecast period. Europe dominated the global nuclear waste management market with a market share of 39.39% in 2024.

Nuclear waste management refers to the systematic handling, treatment, storage, and disposal of radioactive materials generated from nuclear power generation, medical applications, research, and industrial activities. It involves multiple stages, including waste collection, segregation, conditioning, and secure containment to prevent environmental contamination and radiation exposure. The process ensures that all types of radioactive waste—low-level, intermediate-level, and high-level—are managed safely according to their radioactivity and longevity.

Several companies play a vital role in the global nuclear waste management industry, focusing on safe handling, treatment, storage, and long-term disposal of radioactive materials. Leading players include Orano Group, Veolia Environment S.A., Bechtel Corporation, Waste Control Specialists, and Perma-Fix Environmental Services. These companies are engaged in decommissioning nuclear plants, developing advanced waste treatment technologies & reactor types, and establishing secure disposal and storage solutions that comply with international safety standards. Orano Group, in particular, plays a significant role in this industry. The company is actively involved in every stage of the nuclear fuel cycle, including the collection, recycling, conditioning, and long-term storage of radioactive waste. Orano develops advanced technologies for reprocessing used nuclear fuel, reducing the volume and toxicity of high-level waste.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Nuclear Power Generation and Reactor Decommissioning to Drive Market Growth

The steady expansion of nuclear power generation and the increasing number of reactor decommissioning projects are key factors driving the growth of the nuclear waste management market. As of 2024, there are over 440 operational nuclear reactors worldwide and nearly 60 new reactors under construction, according to the International Atomic Energy Agency (IAEA). Each reactor generates high-level radioactive waste throughout its lifecycle—from fuel processing to spent fuel storage and eventual decommissioning. Moreover, around 200 reactors globally are either shut down or in various stages of decommissioning, particularly in countries such as the U.S., France, Japan, Germany, and the U.K. For instance, the U.S. Department of Energy (DOE) has allocated billions of dollars for decommissioning and site cleanup under its Environmental Management Program, reflecting the growing need for professional waste handling and disposal solutions. These decommissioning activities generate large quantities of low- and intermediate-level waste that must be treated, packaged, and stored in compliance with safety standards. As the global nuclear fleet ages, the volume of waste from both active operations and dismantled facilities is expected to increase significantly, propelling demand for advanced waste management systems and services.

Strict Government Regulations and Safety Standards to Propel Market Growth

Stringent regulations and international safety frameworks continue to drive the adoption of modern nuclear waste management practices. Organizations such as the IAEA and the OECD Nuclear Energy Agency (NEA) have established detailed safety standards for waste classification, transportation, treatment, and disposal. These global guidelines have prompted national governments to strengthen domestic policies and ensure long-term environmental protection. For example, the European Union’s Radioactive Waste and Spent Fuel Management Directive (2011/70/Euratom) requires member states to develop national programs for safe disposal and permanent storage of radioactive waste. Similarly, the U.S. Nuclear Regulatory Commission (NRC) enforces strict licensing and monitoring requirements for waste storage facilities, such as those in Nevada and New Mexico. The increasing focus on sustainability and public safety is pushing countries to invest in long-term geological repositories—such as Finland’s Onkalo facility, which is set to become the world’s first deep geological repository for spent nuclear fuel by the late 2020s. These regulations and initiatives ensure compliance while stimulating continuous technological innovation and investment across the nuclear waste management sector.

MARKET RESTRAINTS

Public Opposition and Regulatory Complexity to Constrain Market Growth

Public resistance and regulatory challenges continue to hinder the nuclear waste management market growth. Many communities oppose the establishment of storage or disposal sites due to safety concerns, potential radiation risks, and environmental impact fears. This opposition often results in political pressure, lengthy approval processes, and project cancellations. For instance, the Yucca Mountain repository project in the U.S.—once intended to serve as the country’s primary long-term storage site—was suspended after years of public and political controversy despite significant investment. Additionally, nuclear waste management regulations vary widely across countries, making international collaboration and standardization difficult. Meeting multiple compliance requirements and obtaining environmental clearances can delay projects and increase operational complexity. This combination of social resistance and fragmented regulatory frameworks remains one of the biggest obstacles to the timely and efficient development of nuclear waste management solutions globally.

MARKET OPPORTUNITIES

Development of Deep Geological Repositories to Offer Lucrative Opportunities for Market Players

The increasing focus on deep geological repositories (DGRs) presents a major opportunity for stakeholders in the nuclear waste management market. DGRs are engineered underground facilities designed to securely isolate high-level radioactive waste for thousands of years, protecting human health and the environment. Many nations are now advancing large-scale repository projects, driven by the need for permanent disposal solutions. For instance, Finland’s Onkalo repository, managed by Posiva Oy, is set to become the world’s first operational deep geological facility for spent nuclear fuel by the late 2020s. Similarly, Sweden, France, Canada, and the U.S. are progressing with their own repository development programs. The construction and operation of such repositories require extensive investment in design, excavation, safety assessment, and long-term monitoring technologies, creating new business opportunities for engineering firms, technology providers, and environmental consultants. As global regulatory frameworks increasingly favor permanent disposal over interim storage, the expansion of deep geological repositories represents one of the most promising growth avenues for the nuclear waste management industry.

MARKET CHALLENGES

Rising High Costs and Long Project Timelines to Hinder Market Growth

One of the most significant challenges in nuclear waste management is the extremely high cost and long duration associated with waste treatment, storage, and disposal projects. Developing secure facilities—especially for high-level waste—requires advanced engineering, geological assessment, and long-term monitoring systems that can last for thousands of years. For example, the construction of Finland’s Onkalo deep geological repository has taken more than two decades of planning and investment exceeding USD 3 billion, highlighting the financial and time-intensive nature of such projects. Similarly, decommissioning a single nuclear power plant can cost between USD 500 million and USD 1 billion, depending on the size and complexity of the facility. These high costs often strain government budgets and delay progress, particularly in developing countries with limited nuclear infrastructure. The long lead times for regulatory approvals, environmental impact assessments, and public consultations further slowdown project implementation, creating uncertainty for investors and operators in the market.

NUCLEAR WASTE MANAGEMENT MARKET TRENDS

Advancement in Waste Recycling and Reprocessing Technologies to Lead Market Growth

A major trend shaping the nuclear waste management industry is the growing adoption of advanced recycling and reprocessing technologies aimed at minimizing radioactive waste and enhancing resource efficiency. Traditional nuclear waste disposal methods primarily relied on long-term storage and containment, but emerging technologies now enable the extraction and reuse of valuable materials such as uranium and plutonium from spent fuel. Countries such as France, Japan, and Russia are leading in nuclear fuel reprocessing programs, with facilities such as Orano’s La Hague plant in France, which has reprocessed over 36,000 tonnes of spent fuel since its inception. These technologies significantly reduce the volume and toxicity of high-level waste that requires permanent disposal. Additionally, innovative concepts including partitioning and transmutation—which involve converting long-lived radioactive isotopes into shorter-lived ones—are gaining research attention in the European Union and the U.S. This trend not only supports sustainability but also aligns with global goals for circular resource use and reduced environmental impact in the nuclear energy sector.

Download Free sample to learn more about this report.

IMPACT OF TARIFF ON THE MARKET

The impact of tariffs on the nuclear waste management market is relatively indirect but still significant, particularly through their influence on equipment costs, material sourcing, and project economics. Nuclear waste management relies heavily on specialized machinery, containment systems, monitoring instruments, and advanced materials such as stainless steel, lead, and concrete—many of which are sourced globally. Tariffs on imported materials or components can increase the overall cost of building storage facilities, treatment plants, and decommissioning infrastructure. For instance, higher import duties on industrial equipment or construction materials can raise project expenses, potentially delaying investments or reducing profit margins for service providers. In addition, tariffs can disrupt international supply chains, especially in countries that depend on foreign suppliers for nuclear-grade materials or technology. This may lead to procurement delays and increased reliance on domestic manufacturing, which could affect quality or scalability. Conversely, in some regions, tariff protections may encourage local production of waste management equipment, fostering domestic industry growth. Overall, tariffs tend to create cost fluctuations and uncertainty in long-term nuclear waste management projects, influencing financial planning and cross-border collaboration in this highly regulated sector.

SEGMENTATION ANALYSIS

By Waste Type

High Generation of Lo-level Waste to Lead the Market Share

By Waste Type, the market is segmented into Low-Level Waste, Intermediate-Level Waste, and High-Level Waste. High-Level Waste commands the largest revenue share of 45.03% in 2024 in the market despite being the smallest by volume. HLW waste management is capital-intensive due to the need for heavy shielding, dry cask storage, centralized interim facilities, transport systems for spent fuel, and long-term geological disposal. Developed nuclear regions such as North America and Europe see HLW share exceeding, driven by large legacy inventories and multi-billion-dollar disposal initiatives (geological repository construction, dry cask expansion, and long-term storage liabilities). Asia-Pacific shows the fastest HLW growth, supported by a rapidly expanding reactor fleet and increasing spent-fuel accumulation. As geological disposal programs progress globally, HLW will continue to dominate market value, reflecting its long timelines and the high financial intensity of managing the most hazardous waste streams.

Intermediate-Level Waste is the second leading segment, accounting for 33.01% of global market revenues in 2025, driven by its higher treatment, conditioning, and engineered-storage requirements relative to LLW. ILW includes resins, reactor components, contaminated metals, and waste streams from decommissioning activities. Europe has the highest ILW revenue share (30–35%) due to extensive legacy decommissioning projects and sophisticated waste-conditioning infrastructure. North America and Asia-Pacific follow with balanced ILW spending linked to large operational fleets and ongoing upgrades to ILW packaging and storage facilities. Market growth for ILW is closely tied to the global wave of reactor retirements, as dismantling reactors generates large volumes of activation products and structural materials that fall into this category. As more reactors approach end-of-life, ILW processing demand remains steady to moderately rising.

By Service

Limited Availability of Deep Geological Repositories Boosted the Interim Storage Segment's Growth

Based on Service, the market is divided into collection & handling, interim storage, transportation & logistics, processing & conditioning, and final disposal. Interim storage holds a market share of 27.61%, emerging as one of the most crucial stages in nuclear waste management. It involves the temporary storage of waste, especially spent fuel and high-level waste, until a permanent disposal or reprocessing solution is available. Due to the limited availability of deep geological repositories worldwide, interim storage facilities are in high demand. These facilities are typically designed with robust containment and cooling systems to ensure radiation safety for decades. The growth of this segment is driven by the increasing volume of spent fuel awaiting final disposal, particularly in countries such as the U.S., France, Japan, and Russia, which rely heavily on dry cask or pool storage methods.

Final disposal is the second leading segment in the market, growing with a CAGR of 4.29%, though it accounts for the highest cost intensity per unit of waste managed. It involves the permanent isolation of nuclear waste, typically through deep geological repositories designed to contain radioactivity for thousands of years. While the volume of waste reaching this stage is relatively low, the complexity and expense of ensuring long-term containment make this segment strategically vital. Countries such as Finland, Sweden, and Canada are at the forefront of implementing permanent disposal solutions. The market share of this segment is expected to rise gradually as more nations move from interim storage toward final repository projects over the coming decades.

By End User

Significant Production Waste in Nuclear Power Facilities to Lead Market Growth

As per End User, the global Nuclear Waste Management market is broadly segmented into Nuclear Power Utilities, Government/Defense, and others. Nuclear power utilities hold the largest market share of 71.13% in 2024 in the global nuclear waste management industry. These entities are the primary generators of radioactive waste, as nuclear power plants produce significant volumes of low-, intermediate-, and high-level waste during electricity generation, maintenance, and decommissioning activities. The dominance of this segment is driven by the increasing number of aging nuclear reactors, ongoing operations of commercial power plants, and the expansion of nuclear capacity in countries such as China, India, and Russia. Utilities are heavily investing in waste minimization, on-site interim storage, and long-term disposal solutions to comply with national and international safety regulations. The growing focus on sustainable nuclear energy as a low-carbon alternative further amplifies the demand for efficient waste management practices within this segment.

The government and defense is the second leading segment in the market, growing at a CAGR of 3.07% in the forecast period. It is primarily linked to waste generated from military programs, nuclear research, and legacy cleanup projects. This category includes decommissioned weapons, reactor components from naval vessels, and materials from defense-related research facilities. Governments in countries such as the U.S., the U.K., and France allocate substantial budgets for managing defense-related nuclear waste and for restoring contaminated sites from past nuclear activities. The segment is expected to grow steadily due to the ongoing decommissioning of old defense facilities and increased funding for environmental remediation programs. Furthermore, government ownership of most national waste repositories and regulatory oversight ensures continued demand for safe handling and long-term containment of defense-related waste.

To know how our report can help streamline your business, Speak to Analyst

NUCLEAR WASTE MANAGEMENT MARKET REGIONAL OUTLOOK

The market has been studied regionally across five main regions: North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe is the most dominating region in the market, valued at USD 3.25 billion in 2024. Europe represents a substantial nuclear waste management market share, supported by its mature nuclear fleet, ongoing decommissioning programs, and technological advancements in conditioning and disposal. Countries such as France, the U.K., and Germany are major contributors, with established programs for intermediate- and high-level waste treatment. Finland’s Onkalo repository—the world’s first operational deep geological repository—demonstrates Europe’s leadership in final disposal solutions. Additionally, the region’s stringent environmental regulations and extensive experience in reprocessing (notably in France) further enhance its market value. High investment in research and collaboration across the European Union ensures that the region remains at the forefront of nuclear waste management innovation. Leading countries such as the U.K., Germany, and France hold a market value of USD 0.56 billion, USD 0.45 billion, and USD 0.75 billion, respectively, in 2025.

Europe Nuclear Waste Management Market Size,2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific region is the fastest-growing region, expected to expand at a CAGR of 5.09% during the forecast period. The Asia Pacific region is witnessing rapid growth in nuclear waste management activities due to expanding energy demand and nuclear power programs, particularly in China, India, South Korea, and Japan. China is the major driver, with dozens of reactors operational or under construction, resulting in a steady rise in spent fuel and radioactive waste. Japan continues to manage large volumes of waste from its existing reactors and the decommissioning of the Fukushima Daiichi plant. India’s closed fuel cycle approach and development of reprocessing and vitrification facilities contribute to growing regional demand. As more countries in the region invest in long-term waste storage and disposal infrastructure, Asia Pacific’s share in the global market continues to rise steadily. Leading countries such as China, India, and Japan represent USD 1.35 billion, USD 0.40 billion, and USD 0.48 billion in 2025.

North America

North America also holds a considerable position in the market, valued at USD 1.87 billion in 2025, driven by its extensive nuclear power generation capacity, defense cleanup programs, and advanced waste management infrastructure. The U.S. operates about 93–94 commercial reactors, producing significant volumes of spent fuel and operational waste that require safe handling and long-term storage. The U.S. Department of Energy’s Waste Isolation Pilot Plant (WIPP) serves as a key example of the region’s progress in geological disposal for defense-related waste. Canada’s Nuclear Waste Management Organization (NWMO) is also advancing a deep geological repository project for used nuclear fuel. The combination of large reactor fleets, mature regulatory frameworks, and high decommissioning activity sustains North America’s leadership in this industry. The U.S. holds a market value of USD 1.64 billion in 2025.

Latin America

Latin America accounts for a modest share of the global market, largely driven by nuclear programs in Brazil, Argentina, and Mexico. Brazil’s Angra nuclear power plant complex, which supplies about 3% of the country’s electricity, and Argentina’s Atucha plants are the primary sources of radioactive waste in the region. Most countries in Latin America focus on centralized interim storage and regulatory capacity building rather than deep geological disposal. Although the region’s overall nuclear capacity is limited, growing interest in clean energy diversification and international collaborations is gradually expanding investments in nuclear waste management systems.

Middle East & Africa

The Middle East and Africa currently represent the smallest share of the nuclear waste management market, but are emerging as future growth regions. The United Arab Emirates’ Barakah nuclear power plant, consisting of four operational reactors, marks a major milestone as the first commercial-scale nuclear project in the Arab world, generating new demand for waste storage and regulatory frameworks. In Africa, South Africa’s Koeberg plant continues to drive waste management activities, with additional projects under discussion in Egypt and Kenya. Although the market is still nascent, rising nuclear ambitions and increased international cooperation are expected to accelerate the establishment of robust waste management infrastructures in the coming decade. The region is likely to hold a market value of USD 0.28 billion in 2025, with the GCC countries alone accounting for about USD 0.13 billion.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players’ Extensive Range of Waste Management Solutions to Optimize Operational Efficiency

Orano Group plays a leading global role in nuclear waste management, specializing in the back end of the nuclear fuel cycle through its activities in used-fuel reprocessing, recycling, waste conditioning, and long-term storage solutions. The company operates major facilities such as the La Hague plant in France, which has a licensed capacity to process around 1,700 tonnes of used nuclear fuel per year, recovering about 96% of reusable materials (mainly uranium and plutonium) for recycling. Its Melox plant produces up to 195 tonnes of MOX fuel annually, significantly reducing the volume and radiotoxicity of final waste by roughly fivefold and tenfold, respectively, compared to direct disposal.

List of the Key Nuclear Waste Management Companies Profiled

- Orano Group (France)

- Veolia Environnement S.A. (France)

- Westinghouse Electric Company LLC (U.S.)

- EnergySolutions, LLC (U.S.)

- Bechtel Corporation (U.S.)

- AECOM (U.S.)

- BHI Energy (U.S.)

- Studsvik AB (Sweden)

- Centrus Energy Corp. (U.S.)

- Nuclear Waste Management Organization (Canada)

- Rosatom State Nuclear Energy Corporation (Russia)

- Svensk Kärnbränslehantering AB (Sweden)

- Nuclear Decommissioning Authority (U.K.)

- Cameco Corporation (Canada)

- Japan Nuclear Fuel Limited (Japan)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Rosatom’s Fuel Division, TVEL, and Kazakhstan’s National Nuclear Centre (NNC) signed a memorandum of intent to collaborate on radioactive waste management and decommissioning of nuclear and radiation-hazardous facilities. Under the agreement, Russian experts will support Kazakhstan in developing a national waste management strategy, training specialists, and sharing best practices for site reclamation, decommissioning, and radioactive waste disposal.

- In July 2025, Viam partnered with Swiss nuclear engineering firm Transmutex to enhance the reliability of ion source systems used to transform long-lived radioactive waste into shorter-lived isotopes. Using Viam’s AI and data platform, Transmutex can collect real-time sensor data, apply machine learning to detect faults, and reduce shutdown times—improving efficiency and stability in nuclear waste transmutation processes.

- In June 2025, the Nuclear Decommissioning Authority (NDA) launched a four-year partnership worth about USD 12 million to introduce autonomous technology for sorting and segregating radioactive waste at the former Oldbury nuclear site. The Auto-SAS project, developed in collaboration with Nuclear Restoration Services (NRS), Sellafield, and Nuclear Waste Services (NWS), will be jointly delivered by AtkinsRéalis and Createc under the partnership name ARCTEC, combining their expertise in robotics and automated nuclear systems.

- In September 2024, Constellation signed a 20-year power purchase agreement with Microsoft to supply carbon-free energy from the Crane Clean Energy Center (CCEC), marking the planned restart of Three Mile Island Unit 1, which was shut down five years ago for economic reasons. The revived plant will provide reliable, carbon-free power to support Microsoft’s data centers in the PJM region, advancing both companies’ clean energy goals and honoring former CEO Chris Crane’s legacy of safe and dependable nuclear operations.

- In January 2022, the U.K. government announced the formation of Nuclear Waste Services (NWS). This new organization unites Low Level Waste Repository Limited, Radioactive Waste Management Limited, and the Nuclear Decommissioning Authority’s Integrated Waste Management Program to streamline and strengthen the country’s nuclear waste management efforts.

REPORT COVERAGE

The report delivers a detailed insight into the market and focuses on key aspects, such as leading companies. Besides, it offers insights into the market trends & technologies and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors and challenges that have contributed to the growth and downfall of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 4.01% from 2025 to 2032 |

| Unit | Value (USD Billion) |

| Segmentation | By Waste Type, By Service, By End User, and By Region |

| Segmentation |

By Waste Type

|

|

By Service

|

|

|

By End User

|

|

|

By Region

Rest of Middle East & Africa (By End User) |

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was valued at USD 8.25 billion in 2024.

The market is likely to record a CAGR of 4.01% over the forecast period (2025-2032).

By end user, the Nuclear Power Utilities segment leads the market.

The European market size was valued at USD 3.25 billion in 2024.

Advancement in waste recycling and reprocessing technologies is the key factor driving the market’s growth.

Some of the key players in the market are Orano Group, Veolia Environment S.A., Bechtel Corporation, Waste Control Specialists, Perma-Fix Environmental Services, and others.

The global market size is expected to reach a valuation of USD 11.44 billion by 2032.

- 2019-2032

- 2024

- 2019-2023

- 328

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us