Protective Relay Market Size, Share & Industry Analysis, By Technology (Numerical/IED, Static and Electromechanical), By Voltage (Low Voltage, Medium Voltage, High/Extra-High Voltage), By Application (Feeder / Line, Transformer, Motor, Generator, Busbar, Capacitor Bank, and Others), By End-User (Utilities, Industrial and Commercial & Infrastructure) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

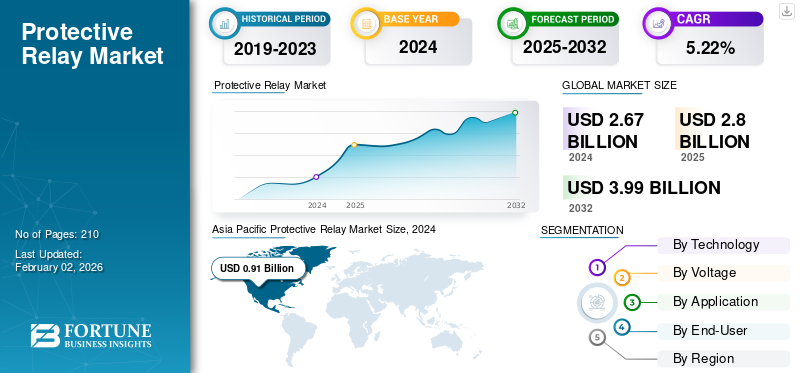

The global protective relay market size was valued at USD 2.67 billion in 2024. The market is projected to grow from USD 2.80 billion in 2025 to USD 3.99 billion by 2032, exhibiting a CAGR of 5.22% during the forecast period. Asia Pacific dominated the protective relay market with a market share of 34.08% in 2024.

The protective relays are intelligent electronic devices designed to detect abnormal conditions or faults in electric power systems, such as overcurrent, overvoltage, under frequency, or differential faults, and initiate the rapid isolation of the faulty part from the circuit breakers. The demand for protective relays is strongly influenced by rising investment in smart grid development, substation automation, and distribution network modernization, particularly in emerging economies. For instance, the U.S. Department of Energy GRIP Programme has allocated over USD 3.5 billion for grid resilience and automation initiatives. At the same time, China State Grid Corporation continues to invest more than USD 70 billion annually in smart grid and ultra-high voltage projects.

The protective relay market is transitioning from traditional standalone protection systems to integrated, networked, and intelligent protection architectures, aligning with the global trends towards digital grid transformation and predictive maintenance.

Leading players, including ABB, Siemens, Schneider Electric, Eaton, and others, are at the forefront of modernizing grid protection technologies. These companies are developing next-generation digital and IEC 61850-enabled protective relays, advanced fault detection algorithms, and cybersecure substation automation solutions. Their innovation is accelerating the global transition towards smarter, more resilient, and self-healing power networks.

Download Free sample to learn more about this report.

PROTECTIVE RELAY MARKET KEY TAKEAWAYS

- 2024 Market Size: USD 2.67 billion

- 2025 Market Size: USD 2.80 billion

- 2032 Forecast Market Size: USD 3.99 billion

- CAGR: 5.22% from 2024–2032

- Asia Pacific dominated the protective relay market with a market share of 34.08% in 2024.

- In 2025, the Numerical/IED segment is anticipated to dominate with 84.67% of the protective relay market share.

- The static technology segment is expected to be accounted for the fastest-growing segment in the market, with a 5.61% CAGR for the period of 2025-2032.

North America

During the forecast period, North America is projected to record a growth rate of 5.19% and reach a valuation of USD 0.66 billion by 2025.

Europe

Europe represents a mature yet steady market, supported by the modernization of aging grid assets, the integration of renewable energy sources.

Asia Pacific

The Asia Pacific held the demand for protective relays with the largest market share in 2023, valued at USD 0.87 billion, and also took the leading share in 2024 with USD 0.91 billion.

U.S.

The U.S. market is estimated to reach USD 0.56 billion in 2025.

Japan

Japan dominates the protective relay market due to its massive and ongoing transformation of its power grid infrastructure

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Investment in Smart Grid Modernization and Power Infrastructure Development Enhances Market Growth

The global demand for protective relays is strongly driven by increasing investments in power infrastructure expansion and smart grid modernization initiatives. Many utilities are upgrading their aging transmission and distribution (T&D) networks to improve efficiency, reliability, and response times to faults. The transition towards digital and automated power systems has accelerated the adoption of advanced protective relays that can perform multifunctional protection, real-time fault analysis, and remote monitoring.

Many existing transmission and distribution (T&D) systems, particularly in North America, Europe, and the Asia Pacific region, are nearing the end of their operational lifespans. This has spurred the development of large-scale programs to replace outdated protection and control systems with digital, intelligent, and automated equipment, including advanced protective relays capable of faster fault detection, real-time communication, and remote operations.

For instance, in 2025, American Electric Power (AEP) and its transmission affiliate, Transource Energy LLC, will invest approximately $1.7 billion in transmission system upgrades to enhance reliability and deliver more power to meet the increasing demand.

Rapid Integration of Renewable Energy Sources to Promote the Growth of Protective Relays

The accelerating global transition towards renewable and low-carbon energy systems has become one of the most significant catalysts for the protective relay market. Nations across all regions are aggressively expanding their renewable energy generation capacity – particularly solar, wind, and distributed energy resources (DERs)- to meet decarbonization targets under the Paris Agreement and various national Net Zero commitments. While transition supports sustainability goals, it introduces new operational complexities to power grids that were originally designed for centralized, unidirectional energy flow. Thus, utilities and system operators are investing heavily in advanced protective relays and adaptive protection schemes to ensure reliability, safety, and stability in increasingly dynamic grid environments.

For instance, in December 2024, the Department of Energy (DOE) grid deployment office reported that it had announced USD 14.5 billion in competitive funding and formula grants over the previous two years, aimed at advancing a more affordable, reliable, or resilient grid. This initiative emphasizes integrating new generation sources (such as renewable and storage) and upgrading grid infrastructure, including protection schemes.

MARKET RESTRAINTS

Cybersecurity Risks and Digitalization-related Vulnerabilities are Emerging as Market Restraints

The growing adoption of digital and intelligent protective relays, equipped with communication interfaces, remote monitoring capabilities, and real-time data exchange, has significantly enhanced the efficiency, responsiveness, and automation of modern power systems. However, this rapid digital transformation has also introduced new cybersecurity risks and system vulnerabilities, emerging as a notable restraint on market expansion.

As utilities, grid operators, and industrial users deploy more IoT-enabled relays, remote firmware updates, and cloud-based asset management systems, maintaining cyber resilience becomes increasingly complex. Many organizations still lack adequate network segmentation, encryption standards, and intrusion detection mechanisms, making them vulnerable to cyberattacks that could compromise the integrity of protective devices.

Protective relays are increasingly being integrated into smart grids, digital substations, and industrial automation systems, where they communicate through network protocols such as IEC 61850, DNP3, and Modbus TCP/IP. While these protocols enable seamless interoperability and real-time system coordination, they also expand the cyber-attack surface of critical energy infrastructure. A compromised relay could lead to false tripping, delayed protection, or even large-scale grid outages, posing a serious threat to reliability and safety.

MARKET OPPORTUNITIES

Regional Growth in Emerging Markets Provides Opportunities for Protective Relays

The emerging market, specifically in the Asia Pacific and Middle East & Africa regions, is scaling transmission and distribution (T&D) networks to absorb rapid demand growth and high additions of renewable energy. According to the International Energy Agency's (IEA) 2024 assessment, global grids are expected to expand by more than 20% in length by 2030 and double annual grid investment to USD 600 billion, with a significant share in emerging regions. Every kilometer of new line and each new/expanded substation requires a feeder, transformer, busbar, line distance, differential, and protection control schemes, directly expanding the addressable market for numerical protective relays and relay-centric services (settings, coordination, cyber-hardening, lifecycle, and O&M).

PROTECTIVE RELAY MARKET TRENDS

Growth of Digital Substations, Smart Grid Rollouts & IoT Connectivity are the Key Market Trends

The global shift toward digital substations and smart grid modernization is one of the most transformative trends driving the protective relay market growth. Utilities and transmission operators are increasingly adopting intelligent, communication-enabled protection and control systems that leverage real-time data, remote diagnostics, and Internet of Things (IoT) connectivity to enhance grid reliability, flexibility, and resilience.

Digital substations replace conventional copper wiring and hardwired analog systems with optical fiber communications, process bus, and digital instrumentation transformers. These relays enable faster fault detection, automated system reconfiguration, and remote monitoring, substantially improving operational efficiency and safety.

Moreover, smart grid expansion programs are directly influencing the adoption of IoT-integrated protective relays. These relays are capable of continuous condition monitoring, remote firmware updates, and predictive maintenance through cloud-based platforms and edge analytics. For example, in December 2024, the U.S. Department of Energy (DoE) announced a USD 14.5 billion investment in grid modernization projects under the Grid Resilience and Innovation Partnerships (GRIP) Program. A significant portion of these projects focuses on digital substation automation, adaptive protection, and communication-based fault isolation, highlighting the increasing role of connected protection systems.

Download Free sample to learn more about this report.

MARKET CHALLENGES

High Initial Investment and Cost Constraints are one of the major challenges in the Protective Relay Market

One of the major challenges in the protective relay market is the high upfront investment required for deploying modern digital protection systems. Protective relays have evolved from basic electromechanical devices to sophisticated, microprocessor-based systems that integrate communication, cybersecurity, and automation. This advancement has significantly improved reliability and operational control, but has also increased the initial purchase and installation cost.

The hardware itself is expensive. Digital and numerical relays are priced several times higher than traditional relays due to their processing capabilities, communication interfaces, and embedded diagnostic features. When combined with associated with auxiliary devices such as merging units, protocol converters, or redundant power supplies, the total material cost rises sharply.

Moreover, the installation and commissioning phase demands substantial capital and skilled labor. Implementing new protection systems often requires rewiring panels, upgrading switchgear, integrating SCADA or substation automation systems, and conducting extensive testing and configuration, all of which add to the total project expenditure. In addition, maintenance and lifecycle costs add financial pressure.

Segmentation Analysis

By Technology

Multi-functionality, Digital Integration, and Smart Grid Adoption Led Numerical/IED Segment

By technology, the market is classified into Numerical/IED, Static, and Electromechanical.

In 2025, the Numerical/IED segment is anticipated to dominate with 84.67% of the protective relay market share. Numerical or Intelligent Electronic devices (IEDs) dominate the market owing to their multifunctional capability, accuracy, and integration features. They offer high-speed digital processing, programmable logic, and communication interfaces that enable seamless integration with modern substation automation systems.

Moreover, the static technology segment is expected to be accounted for the fastest-growing segment in the market, with a 5.61% CAGR for the period of 2025-2032. The static relays use semiconductor components instead of mechanical contacts, offering faster and more reliable operation than electromechanical types, but without digital programmability. Moreover, they are less expensive than numerical relays and are ideal for cost-sensitive or small-scale systems.

By Voltage

Rising Widespread Application in Power Distribution Networks Led to Medium Voltage Segment Growth

By voltage, the market is tri-furcated into Low Voltage (<1 kV), Medium Voltage (1–36 kV), and High/Extra-High Voltage (>36 kV).

The medium voltage segment is likely to hold the highest share, approximately 50.58% in 2025, driven by its widespread application in power distribution networks, industrial facilities, and commercial infrastructure. Medium-voltage relays are extensively used in distribution substations, feeders, and switchgear systems to safeguard equipment from overloads, short circuits, and faults. Moreover, the continuous investments in smart grid technologies and renewable energy integration at the distribution level further reinforce the strong position of the medium voltage segment globally.

The low-voltage segment is expected to be the fastest-growing segment, with a 6.43% CAGR for the period of 2025-2032. This growth is primarily driven by the rising demand for reliable protection solutions in commercial, residential, and industrial low-voltage networks. Increasing urbanization, the expansion of building automation systems, and the proliferation of distributed energy resources (DERs), such as rooftop solar, EV charging stations, and Microgrids, are significantly boosting low-voltage relay installations.

By Application

Extensive Deployment of Protection Relays in Transmission Networks Leads to Feeder/Line Application Growth

In terms of application, the market is segmented into feeder/line, transformer, motor, generator, busbar, capacitor bank/reactive power, and others.

The feeder/line is anticipated to dominate the market, accounting for a 30.26% share in 2025. The feeder/line segment dominated the market due to the extensive deployment of protection relays in transmission and distribution networks, which safeguard lines and feeders against overloads, short circuits, and earth faults. Feeder protection relays are crucial for ensuring the selective isolation of faults and maintaining the continuity of supply chains across power grids.

Moreover, the transformer protection segment is projected to grow at a moderate CAGR of 5.54% from 2025 to 2032. The transformer protection segment represents the second-largest share, driven by continuous investments in grid expansion, substation modernization, and replacement of aging transformer fleets. Protective relays in this segment provide differential, overcurrent, and thermal protection, ensuring the stable operation of high-value transformer assets.

By End-User

To know how our report can help streamline your business, Speak to Analyst

Grid Reliability, Isolating Faults, and Automating Substations of Utilities Lead the Segmental Growth

In terms of end-users, the market is tri-furcated into utilities (T&D, IPPs), industrial, commercial & infrastructure.

The utilities (transmission & distribution, independent power producers) accounted for the largest share, 61.30%, in 2025. This dominance stems from the critical role of relays in ensuring grid reliability, isolating faults, and automating substations. Utilities worldwide are prioritizing grid modernization, renewable integration, and digital substation upgrades, which require numerical and communication-enabled relays.

The industrial segment accounted for the second-largest market and is growing at a CAGR of 4.82% during the period of 2025-2032. Industrial automation, process & safety regulations, and the need for uninterrupted power supply across various sectors, including oil & gas, metal & mining, manufacturing, chemicals, and data centers, drive this. Industries increasingly deploy intelligent motor, transformer, and feeder protection relays to prevent equipment failure and minimize downtime. The shift toward smart factories, the electrification of industrial assets, and predictive maintenance practices is accelerating the transition from static to numerical IED-based systems, especially in medium-voltage networks.

Protective Relay Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Protective Relay Market Size, 2024 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific held the demand for protective relays with the largest market share in 2023, valued at USD 0.87 billion, and also took the leading share in 2024 with USD 0.91 billion. The demand for protective relays in the Asia Pacific is increasing owing to massive investments in transmission and distribution (T&D) infrastructure, rapid industrialization, and growing electricity demand across countries such as China, India, Japan, and South Korea. The governments in the region are implementing large-scale programs to modernize power grids, expand renewable generation, and improve grid reliability, all of which require advanced protection systems. Moreover, the widespread deployment of numerical or IED relays in new substations and retrofit projects, along with domestic manufacturing initiatives, further supports the region's dominance.

In 2025, the China market is estimated to reach USD 0.35 billion. China dominates the protective relay market due to its massive and ongoing transformation of its power grid infrastructure, including the development of ultra-high voltage transmission, integration of renewable energy, smart substations, and the electrification of industrial and transportation sectors.

- For instance, in 2024, China's National Power Planner announced a comprehensive grid upgrade plan, in which long-distance transmission and distribution infrastructure will be enhanced, demand response capacity will be expanded, and the grid will be adapted to handle intermittent renewables. As part of this initiative, investments of more than USD 800 billion over the next six years for the transmission/distribution network were cited.

Other regions, such as North America and Europe, are expected to experience notable growth in the coming years.

North America

During the forecast period, North America is projected to record a growth rate of 5.19% and reach a valuation of USD 0.66 billion by 2025. North America holds a substantial share, driven by grid modernization, the retrofit of aging substation assets, and the strong adoption of IEC 61850–based digital substations by utilities and industrial users. The U.S. market is estimated to reach USD 0.56 billion in 2025, supported by initiatives for grid resilience, wildfire mitigation, and renewable integration, which encourage the replacement of legacy relays with IEDs and adaptive protection schemes.

Europe

Europe represents a mature yet steady market, supported by the modernization of aging grid assets, the integration of renewable energy sources, and interconnection projects across EU member states. Emphasis on cyber-secure substation automation and decarbonization targets is driving demand for digital protection relays in both transmission and distribution (T&D) and generation applications. Moreover, countries such as Germany, the UK, and France accounted for USD 0.18 billion, USD 0.13 billion, and USD 0.09 billion, respectively, in 2025.

Latin America

Over the forecast period, the Latin America and the Middle East & Africa regions are anticipated to present tremendous opportunities for the protective relay market, as countries such as Brazil, Mexico, and Chile are emerging as key adopters of protective relays. Transmission upgrades and the shift towards renewable energy sources in the countries support the growth in the Latin American region. The focus on reliable distribution networks and industrial automation is gradually increasing demand for modern protective relay solutions.

Middle East & Africa

The Middle East and Africa region also shows strong potential, led by grid expansion projects in GCC countries, offshore and onshore oil & gas infrastructure, and electrification programs across South Africa. Ongoing investments in smart cities and renewable power plants in Saudi Arabia, the UAE, Egypt, and South Africa are creating opportunities for relay manufacturers. The Middle East & Africa region accounted for USD 0.16 billion in 2025. The GCC countries accounted for USD 0.07 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Market Players Are Focusing on Technological Advancements and Strategic Developments

The global protective relay market is moderately consolidated, with several major players focusing on technological innovation, product reliability, and supporting grid modernization. Leading companies, such as ABB Ltd., Siemens AG, Schneider Electric, General Electric, and Mitsubishi Electric, dominated the market through their extensive product portfolios, global manufacturing capabilities, and long-term partnerships with utilities and industrial customers.

For instance, in September 2023, ABB signed a five-year agreement with the Belgian water utility Azulatis N.V. covering asset availability, performance, and lifecycle support. The ABB electrification service partners with utility, industrial, and commercial customers across all industries to manage their energy and electrification infrastructure as strategic operational assets in a safe, smart, and sustainable way.

LIST OF KEY PROTECTIVE RELAY MARKET PROFILED

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- General Electric (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Eaton Corporation (Ireland)

- Basler Electric Company (U.S.)

- Rockwell Automation Inc. (U.S.)

- Toshiba Energy System & Solution Corporation (Japan)

- Omron Corporation (Japan)

- Fuji Electric Co. Ltd (Japan)

- Littlefuse Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Siemens Smart Infrastructure launched a new series of coupling relays, featuring a housing made from 70% bio-based plastic derived from biomass waste.

- In June 2025, ABB expanded its Relion family with the REC 615, a unified medium-voltage protection and control relay for RMUs, Reclosers, and load-break switches. The devices consolidate protection, control, and power-quality analysis with one compact IED. They are designed to simplify grid-edge automation and reduce equipment footprint.

- In March 2025, Siemens AG, a German-based company, unveiled the Xcelerator and Gridscale X digital substation platform, which integrates advanced protective relays, automation, and secure communication systems. The showcase highlighted real-time interoperability between IEDs and control software, with cybersecurity compliance built in.

- In May 2024, General Electric, a U.S.-based company, collaborated with TECO Corporation to provide a STATCOM system and transfer solutions. TECO will oversee civil works and site operations. These STATCOM systems will be installed at substations connected via a 161 kV transmission line. This collaboration with TECO emphasizes a dedication to sustainable energy solutions that promote a positive global impact.

- In February 2024, ABB acquired SEAN Group, a leading provider of energized asset management and advisory services across industrial and commercial sectors. This strategic acquisition enhances ABB’s electrification services portfolio by integrating extensive expertise in predictive, preventive, and corrective maintenance, as well as electrical safety, renewables, and asset management advisory services.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 5.22% from 2025-2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Technology, Voltage, Application, End-User, and Region |

|

By Technology |

|

|

By Voltage |

|

|

By Application |

|

|

By End-User |

|

|

By Region |

Middle East & Africa (By Technology, By Voltage, By Application, By End-User, and by Country)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.67 billion in 2024 and is projected to reach USD 3.99 billion by 2032.

In 2024, the market value stood at USD 0.91 billion.

The market is expected to exhibit a CAGR of 5.22% during the forecast period of 2025-2032.

The Utilities segment led the market in terms of end-users.

Rising investment in smart grid modernization and power infrastructure development is enhancing the usage of relays are the major drivers for the market.

ABB Ltd, Siemens AG, Schneider Electric, General Electric, Mitsubishi Electric, and others are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us