Real and Compound Chocolate Market Size, Share & Industry Analysis, By Category (Real Chocolate and Compound Chocolate), By Type (Milk Chocolate, Dark Chocolate, and White Chocolate), By Form (Chips, Slabs, Coatings, and Others), By Application (Confectionery, Bakery, Dairy and Frozen Desserts, Beverages, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

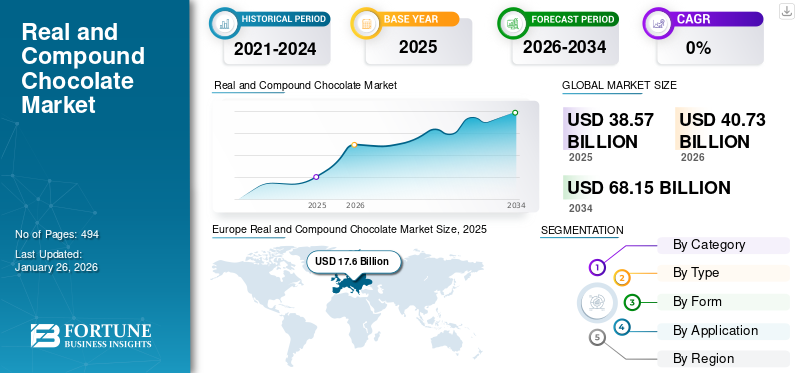

The global real and compound chocolate market size was valued at USD 38.57 billion in 2025. The market is projected to grow from USD 40.73 billion in 2026 to USD 68.15 billion by 2034, exhibiting a CAGR of 6.65% during the forecast period. Europe dominated the real and compound chocolate market with a market share of 45.63% in 2025.

Real and compound chocolates are made from cocoa mass and cocoa butter, with compound chocolate referring to products where cocoa butter and cocoa powder are replaced with vegetable oil. During the manufacturing process of both real and compound chocolates, nutritious seeds are roasted, enhancing their flavor. These chocolates have high heat resistance, bloom resistance, and other technical properties, making them suitable for consumption in warmer and colder countries. Additionally, they are widely used in different food products due to these properties. Market growth is associated with the increasing number of shoppers leaning toward indulgent confectionery products.

The demand for creative products and ingredients in premium product manufacturing globally has increased in recent years. This growth is attributed to the increasing disposable income of consumers, particularly in developing countries, supporting them to purchase indulgent chocolate confectioneries. As a result, global sales of real and compound chocolates have surged. Furthermore, key players such as Barry Callebaut AG, Puratos Group, and Mondelez International dominate the market.

Download Free sample to learn more about this report.

Global Real Compound Chocolate Market Key Takeaways:

Global Market Size

- 2025: USD 38.57 billion

- 2026: USD 40.73 billion

- 2034: USD 68.15 billion

- CAGR (2026–2034): 6.65%

Top Regional Markets

- Europe is the largest market at USD 17.6 billion, driven by strong demand for premium chocolate in 2025.

- Asia Pacific is the fastest-growing region with USD 8.05 billion and a CAGR of 7.93% in 2025.

- North America is supported by strong retail and bakery sector demand, reaching USD 6.80 billion in 2025.

- The Middle East & Africa is driven by rising consumption in GCC countries, estimated at USD 3.57 billion in 2025.

By Category

- Real compound chocolate accounted for 88% of the total market, reflecting strong preference for authentic formulations in 2024.

By Type

- Milk chocolate dominates with a 50% share in 2025.

- Dark chocolate is growing at a CAGR of 6.69%, driven by health-conscious consumer demand in 2025.

By Application

- Confectionery holds the largest usage share at 46%, including bars, candies, and molded items in 2025.

- Bakery is the fastest-growing segment with a CAGR of 6.92%, covering cakes and cookies in 2025.

By Form

- Coatings lead with a 45% share in 2025.

- Chocolate chips are expanding at a CAGR of 6.25%, popular in home baking and snacks in 2025.

Market Dynamics

Real and Compound Chocolate Market Trends

Evolving Plant-based and Low-Sugar Chocolate Consumption to Promote Growth

The chocolate confectionery sector has traditionally been driven by indulgence, but in recent years, there has been a surge in demand for “better-for-you” options. The rise of flexitarianism has further fueled the demand for plant-based chocolates. Consumers’ expectations are changing as they are seeking products beyond dairy allergies and lactose intolerance. At the same time, millennials look for tasty yet "ethical" plant chocolates that are harmless to the planet and animals.

As consumers become increasingly concerned with fitness and health, these trends are having a strong impact on the chocolate confectionery industry. This shift is prompting companies and artisanal confectionery manufacturers to come up with vegan and low-sugar products. According to the Barry Callebaut global proprietary research report 2023, nearly 66% of consumers are showing interest in “less sugar” or “no-sugar” chocolate confectioneries globally.

Vegan chocolate variants manufactured by traditional iconic brands, boutiques, and independent producers are increasingly appearing on store shelves, creating a positive product image among consumers. Retailers are highly aware of the potential of this label, which has driven them to develop innovative products. For instance, in December 2023, Lindt, a global chocolate confectionery manufacturer, recently signed a strategic partnership agreement with ChoViva, a vegan chocolate brand, to launch a limited-edition vegan chocolate named “Soft & Creamy Hazelnut.”

Download Free sample to learn more about this report.

Market Drivers

Increased Demand for Premium and Innovative Confectioneries to Boost Compound and Real Chocolate Sales

Although the premium chocolate market has matured, the global demand remains steady. In the U.S., artisan and gourmet products are popular, with consumers focused on cocoa content and its use as an ingredient to improve flavor. Although there is growing concern regarding the health benefits of consuming chocolates, the demand for innovative and chocolate-based confections continues to be strong. Major factors influencing purchasing decisions in the chocolate confectionery market include the taste and texture of the products. Manufacturers are continuously innovating and launching new variations that combine sweet and savory flavors.

Technical Advantage and Cost-Effectiveness of Compound Chocolates to Drive Global Market

Compound chocolates are made using hard vegetable fats, namely coconut oil and palm kernel oil, and serve as a low-cost alternative to original chocolates made with cocoa butter. Moreover, cocoa butter has to be tempered to retain its coating and gloss, whereas vegetable oil used in compound chocolate does not require tempering. This makes compound chocolate more cost-effective and easier to work with. The use of innovative technologies such as the Internet of Things (IoT) and AI also supports the growth of chocolate manufacturing. The use of these novel technologies can help reduce production overheads.

Market Restraints

Fluctuations in Raw Material Prices to Restrain Market Growth

The compound and real chocolate market relies on the supply, quality, and cost of raw materials worldwide. The fluctuations in the price and supply of raw materials, such as cocoa, due to crop disease, climate, and labor unavailability can negatively impact the market. According to the International Cocoa Organization, the cocoa bean price in March 2025 has declined from its highest price. However, its range remained high compared to the past few years. In London, the average price of cocoa beans reached USD 8,100 per ton in March 2025. In March 2024, the cocoa bean price was recorded at approximately USD 10,500 per ton in London.

Several factors, such as El Niño, climate change, bean disease, and the low income of cocoa farmers, are the primary reasons behind the price rise. Failure to recover higher or shortfalls in the availability or quality of raw materials, such as cocoa butter, cocoa powder, sugar, and others, could adversely impact the market. The significant change in regulatory controls, legal systems, and customs in the regions also affects product supply and hampers the global real and compound chocolate market growth.

Market Opportunities

Beans-to-Bar Chocolate Production to Create an Opportunity for Industry Growth

A few years back, bean-to-bar chocolate production was limited to small-scale operations, where chocolate was produced from scratch by a small group or even a single individual. However, the growing belief in the superior quality of ingredients used in bean-to-bar chocolates is expected to encourage market players to invest in the trend to capitalize on potential profits.

The rapid rise in recognition of craft or artisan chocolate is influencing major chocolate companies such as Barry Callebaut and Blommer Chocolate Company, and smaller producers, to take control over the entire production and supply, boosting the growth of bean-to-bar trends. As a result, manufacturers are coming up with innovatively crafted chocolates to expand their portfolio and attract a large consumer base. For instance, in October 2022, Scharffen Berger, one of America's original craft chocolate makers, launched a new brand, Chocolate Provisions. The new brand was designed to reflect the fine quality of the chocolate and emphasize the farm-to-bar process.

Impact of COVID-19

The COVID-19 pandemic had a profound impact on the usage of cocoa in the food & beverage processing industry. During the pandemic, the application of such products in the foodservice declined as countries implemented lockdowns to reduce the spread of the disease. As per the Cocoa Association of Asia (CAA), cocoa grindings in the Asian market fell by almost 10% in the first half of 2020 compared to 2019. Moreover, the prices of cocoa fell in the early days of the pandemic due to supply chain bottlenecks and an increase in transportation costs. The collection of cocoa from smallholder farmers and the supply of these products to the exporters and cocoa processors declined during the period. This raw material supply shortage affected the production of chocolates, leading to lower production. For instance, Barry Callebaut AG, a foremost premium chocolate manufacturer, reported a slowdown in chocolate production during the first six months of FY 2020 due to the pandemic.

However, the rapid establishment and speedy expansion of online retail, e-commerce, and other distribution channels amidst the COVID-19 pandemic have unlocked new opportunities for manufacturers in the retail sector. These developments are anticipated to boost market growth in the forthcoming year.

Segmentation Analysis

By Category

Real Chocolate Segment Dominated Due to Its High Quality and Taste

Based on category, the market is segmented into real chocolate and compound chocolate. Real chocolate remains the leading segment in 2026 with a share of 88.14%, due to the growth prospects of specialty and high-quality chocolate products. The presence of cocoa butter gives real chocolate its creamy, mellow flavor and delicate taste. Additionally, cocoa extract is becoming the ingredient of choice for various applications, including ice cream, candy, non-alcoholic beverages, delicious baked goods, and nutritious beverages.

- In 2024, real compound chocolate accounted for 88% of the market, indicating consumer preference for authentic chocolate formulations over synthetic alternatives.

Palm oil, shea butter, salted nut oil, and other substitutes for cocoa butter are commonly used in the production of compound chocolate. The reasonable prices of these substitutes have prompted compound chocolate manufacturers to expand their production capacity. The increasing use of cocoa butter alternatives is expected to further support the compound chocolate segment growth.

By Type

Milk Chocolate Segment Holds Major Share Due to its Wide Consumption and Utilization in Confectionery Items

On the basis of type, the market is segmented into milk chocolate, dark chocolate, and white chocolate. The milk chocolate segment is dominating the global market with a market share 50.21% in 2026, driven by its wide consumption and incorporation into various chocolate-based confectionery items due to its versatile taste and texture. Milk chocolate is made with milk solids and usually contains only cocoa butter, which gives it a creamy texture and mouthfeel. Real and compound milk chocolate is increasingly used in the formulation of various beverages and confectionery products, such as cakes, shakes, croissants, and hot chocolate, which has contributed to the growth of the segment.

- Milk chocolate dominates in 2025 with a 50% market share due to its mild taste and wide applications.

- Dark chocolate is projected to grow at a CAGR of 6.69% from 2025 to 2032, supported by rising health awareness and demand for high-cocoa products.

The dark chocolate segment is projected to grow at the highest CAGR during the forecast period. Dark chocolate provides consumers with premium appeal, along with health, sensory benefits, and a rich texture. It is high in antioxidants, can help balance blood pressure levels, and provides a range of other benefits, making it highly consumers among health-conscious consumers.

To know how our report can help streamline your business, Speak to Analyst

By Form

Adaptability in Various Applications to Make Coatings a Leading Segment

By form, the market is segmented into chips, slabs, coatings, and others.

Coatings are the most widely used form of real and compound chocolate and are likely to lead during the forecast period. The use of different fats in compound chocolate coatings allows for a variety of textures, making it suitable for various applications, such as coatings for ice creams, frozen desserts, and baked goods. The compound coating does not require tempering, which is more suitable for different temperatures and applications. In addition, since there are not so many guidelines on ingredients, compound coatings can be easily enhanced or flavored, offering virtually unlimited options. Coatings accounted for 44.93% of the market share in 2026 as they are widely used in ice creams, cakes, and snacks.

Chips are also experiencing significant growth, especially in the artisanal baking industry, where they are commonly used in cookie recipes. In addition, most chocolate chip formulations are made with dark chocolate, which adds value by providing solid antioxidant potential. Chocolate chips segment is projected to grow at a CAGR of 6.25% as they are popular in cookies and home baking kits.

By Application

Confectionery Segment Dominates Market Owing to Its Unique Taste

Based on application, the global market is categorized into confectionary, bakery, dairy and frozen desserts, beverages, and others.

The confectionary segment holds the largest market share in the market. Chocolate confectionaries are popular among young and mature consumers owing to their unique taste and texture. These products are known for their rich flavor and are often associated with happiness, contributing to their global appeal. Confectionery applications held the largest share in 2026 at 46.53%, including bars, candies, and molded chocolate.

Bakery applications are expected to grow at the fastest CAGR of 6.92%, driven by their usage in cakes, cookies, and filled desserts. The bakery segment is anticipated to grow at the highest CAGR during the forecast period. Compound and real chocolates are traditionally used in the bakery industry to coat, fill, and enhance the color and texture of bakery products. This enables bakers to be more creative with product innovation and provides a sensory experience, offering promising growth opportunities in the sector.

Real and Compound Chocolate Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, South America, and Middle East & Africa.

Europe

Europe Real and Compound Chocolate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Europe represented USD 17.6 billion, accounting for 45.63% of the worldwide market, and is projected to grow to USD 18.51 billion in 2026. Europe is expected to hold the largest real and compound chocolate market share, owing to the large cocoa processing base and strong manufacturing industry present in the region. According to the International Cocoa Organization, the German chocolate industry processed 460 thousand tons of cocoa beans in 2023/24. Although the demand is high, European chocolate manufacturers often process cocoa beans locally or source semi-finished products from European processors, making competition fierce. Multinational companies, such as Barry Callebaut AG, Cargill Inc., Cémoi Group, and Olam International, play a significant role in supplying semi-finished cocoa products to the food, beverages, and confectionery industry across the region. The UK market is projected to reach USD 2.36 billion by 2026, while the Germany market is projected to reach USD 3.97 billion by 2026.

This dominance is supported by strong demand from the premium confectionery industry and chocolate culture across Western Europe.

- Germany is projected to hit USD 3.74 billion by 2025, supported by premium and innovative chocolate offerings.

- France will reach USD 2.42 billion by 2025, fueled by gourmet desserts and artisanal products.

- The U.K. market will total USD 2.25 billion by 2025, supported by demand in snacks and pastries.

To know how our report can help streamline your business, Speak to Analyst

North America

North America recorded a market size of USD 6.8 billion in 2025, capturing 17.62% of the global market share, and is projected to reach USD 7.11 billion in 2026. North America represents a huge customer base and is the second-largest market, owing to the high per capita consumption of chocolate-based products. The growing awareness regarding the benefits of healthy confectioneries among consumers has augmented market growth. The shift to at-home consumption is reshaping and accelerating change in consumer behavior. Chocolate remains a leading flavor in several treats, so manufacturers and brands are bringing cocoa into new formats and varieties, including compounds and cocoa nibs, to meet consumers’ demands. The need for "better-for-me" alternative products is anticipated to accelerate as health and well-being have become a top priority in the region. Furthermore, the demand for premium and seasonal confectioneries on various festivals and celebratory occasions also drives market growth.

- North America is the third-largest regional market, anticipated to hit USD 6.8 billion in 2025, led by the U.S. with robust demand in retail, seasonal offerings, and bakery chains.

The U.S. is the major market within the region, contributing significantly to this trend. According to the National Confectioners Association, manufacturers of chocolate, gum, candy, and mints employ nearly 58,000 people across the U.S., and the confectionery industry contributes more than USD 37 billion in retail sales to the U.S. economy each year. The increasing demand for bakery products due to the ongoing trend of “snacking,” especially among the youth population, is likely to enhance the use of real and compound chocolate in bakery food production. The U.S. market is projected to reach USD 3.59 billion by 2026, driven by retail, baking, and gifting demand.

Asia Pacific

The Asia Pacific market generated USD 8.05 billion in 2025, representing 20.86% of the global market landscape, and is expected to reach USD 8.59 billion in 2026. Asia Pacific holds the third-largest market share due to the growing millennial population in the region and their rising preference toward high-quality chocolate confectioneries, especially in emerging economies such as India and China. Furthermore, the growing trend of cocoa processing at the origin for flavor cocoa also contributes to the regions' growth. According to the Cocoa Association of Asia, cocoa processing/grinding in Asia has increased by 11% from 858,675 tons in FY2023 to 859,607 tons in FY2024. Asian countries such as China, India, Japan, and Australia are a few emerging markets for compound chocolate, as consumers are inclined toward premium confectioneries. Indonesia is one of the vital countries holding a higher share of Southeast Asian cocoa grinding. The three multinational giants Cargill Inc., Olam International, and Barry Callebaut AG are behind Indonesia's strong position in cocoa grinding.

These companies dominate the cocoa processing at their place of origin, making the semi-finished cocoa products market more competitive. Therefore, it is becoming increasingly important for Small and Medium-Sized Enterprises (SMEs) to provide value-added cocoa products made from specialty cocoa in the market, contributing to the increased compound and real chocolate demand in the region. The Japan market is projected to reach USD 1.91 billion by 2026, the China market is projected to reach USD 2.75 billion by 2026, and the India market is projected to reach USD 1.29 billion by 2026.

Asia Pacific is the second-largest market, projected to reach USD 8.05 billion in 2025, and is expected to grow at the fastest CAGR of 7.93% during the forecast period, driven by increasing urbanization, gifting culture, and youth-oriented snacking trends.

- China is expected to record USD 2.57 billion by 2025, driven by the trend of festival gifting and demand for Western dessert.

- India will hit USD 1.20 billion by 2025, boosted by a growing middle-class population and urban retail growth.

- Japan is projected at USD 1.79 billion by 2025, with demand for high-end and seasonal chocolates.

South America

In South America, the evolving taste preferences and rising demand of consumers for chocolate confectionery have boosted the market. Consumers are increasingly interested in the artisanal products that make up the taste and the product's origin. As a result, consumers have started to look for exclusive chocolate and sugar confectionery products that are less mainstream. The rising cocoa processing and grinding industry in the region is likely to push the industry's growth. According to the International Cocoa Organization, Brazil processed nearly 240 thousand tons of cocoa beans in 2023/24. In 2025, Latin America held 6.64% of the global market, reaching a valuation of USD 2.56 billion, and is projected to grow to USD 2.7 billion in 2026.

Middle East & Africa

Middle East & Africa accounted for USD 3.57 billion in 2025, representing 9.25% of the global market share, and is projected to reach USD 3.83 billion in 2026. Compared to traditional sweets, UAE consumers prefer to give away high-quality boxed chocolates, which come in different shapes and sizes and have exquisite packaging. This factor has further increased the influx of global premium chocolate brands, such as Mars Inc., into the country and positively aided in the region's market growth. Market players in the country are preparing premium and improved compound chocolate products from good-quality cocoa in order to meet the rising demand for premium chocolate indulgence. For instance, in May 2022, Barry Callebaut, a chocolate and cocoa giant, set up a direct distribution network in South Africa. The company would offer a wide range of compound products to artisans and chefs and multiple distributors through their brands such as Carma, Mona Lisa, and Cacao Berry.

Middle East & Africa is projected to be the fourth-largest market, valued at USD 3.57 billion in 2025, boosted by rising chocolate consumption in GCC countries.

- UAE will total USD 1.53 billion by 2025, led by imports, tourism-linked retail, and gifting culture.

Competitive Landscape

Key Market Players

Key Players Incorporate Sustainable Sourcing and New Product Development Strategies to Enhance Their Industry Presence

The global real and compound chocolate industry is highly developed, with several multinational companies occupying the majority. Barry Callebaut AG, Puratos Group, and Mondelez International dominate the market. The primary strategy adopted by these major market players focuses on continuous product innovations in areas such as health-conscious offerings, enhanced taste, and innovative packaging solutions. The global market share is concentrated with the presence of key industry players such as Barry Callebaut AG, Cargill Inc., Fuji Oil Group, Puratos Group, and Cémoi Group. Prominent players in the market are extensively focusing on two strategies: new product development and a heightened focus on sustainability. They are increasingly prioritizing the procurement of organic, traceable, and Fairtrade cocoa, aligning there with growing demand for ethical and environmentally responsible sourcing.

To know how our report can help streamline your business, Speak to Analyst

List of Key Real and Compound Chocolate Companies Profiled

- Barry Callebaut AG (Switzerland)

- Puratos Group (Belgium)

- Mondelez International (U.S.)

- Cargill Incorporated (U.S.)

- Nestlé S.A. (Switzerland)

- Fuji Oil Company Limited (Japan)

- The Hershey Company (U.S.)

- Mars Incorporated (U.S.)

- Olam International (Singapore)

- Cémoi Group (France)

Key Industry Developments

- April 2024 - Barry Callebaut planned to develop a fully scalable, sustainable, and profitable cocoa farming model for the industry. To support this initiative, the group established a company called FFI, which focuses on developing technology and R&D activities. The company is also collaborating with farmers to modernize and scale sustainable cocoa farming practices.

- March 2024 - Cargill India, a subsidiary of Cargill Inc., expanded its product portfolio by unveiling block chocolates, chocolate chips, and cocoa powder products under its NatureFresh Professional brand. The company developed these products for manufacturers from the food & bakery industry across India.

- June 2023 - Barry Callebaut expanded its dairy-free chocolate offering in the Mexican market with the introduction of the Callebaut NXT and SICAO Zero brands. These brands target consumers seeking specialty claims such as dairy-free, low-sugar, and environmentally-friendly chocolate options.

- April 2023 - The Hershey Company launched an income accelerator program for cocoa farming households in Côte d’Ivoire to improve the livelihoods of cocoa farmers. The initiative includes investments in digital payment methods to streamline the transfer of payments to the household.

- November 2022 - Barry Callebaut, a global leader in chocolate and confectionery ingredients manufacturing, invested nearly USD 52.36 million to build a new production facility in India at Neemrana, Delhi. Its new facility would cover about 20,000 sq. meter area, which includes state-of-the-art assembly lines for producing chocolate and compounds and an R&D laboratory.

Report Coverage

The real and compound chocolate market research report offers qualitative and quantitative insights into the chocolate and chocolate confectionery industry. It focuses on significant aspects such as competitive landscape, product type, and product application areas. Besides this, it offers insights into the various market trends and highlights vital industry developments. In addition to these mentioned factors, it encompasses several other factors that have contributed to the market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.65% from 2026 to 2034 |

|

Unit |

Value (USD Billion) and Volume (Million Tons) |

|

Segmentation |

By Category

By Type

By Form

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market stood at USD 38.57 billion in 2025 and is projected to reach USD 68.15 billion by 2034.

The market is expected to grow at a CAGR of 6.65% during the forecast period (2026-2034).

Based on category, the real chocolate segment is the leading segment in the market.

Increasing consumer inclination toward premium and innovative confectioneries is a key factor driving market growth.

Barry Callebaut AG, Cargill Inc., Fuji Oil Group, Puratos Group, and Cémoi Group are the key players in the market.

Europe is expected to hold the highest market share.

By type, the milk chocolate is the leading segment in the market.

Evolving plant-based and certified chocolate consumption is a key market trend.

- 2021-2034

- 2025

- 2021-2024

- 494

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us