Train Battery Market Size, Share & Industry Analysis by Battery Type (Lead-acid, Nickel-Cadmium (Ni-Cd), and Lithium-ion), By Application (Starter, Auxiliary, and Propulsion), By Rolling Stock Type (Locomotive (ICE, Electric, Hybrid), Multiple Units (DMU, EMU, Hybrid), Passenger Coaches & Freight Wagons, and Metros /Light Rail/Trams), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

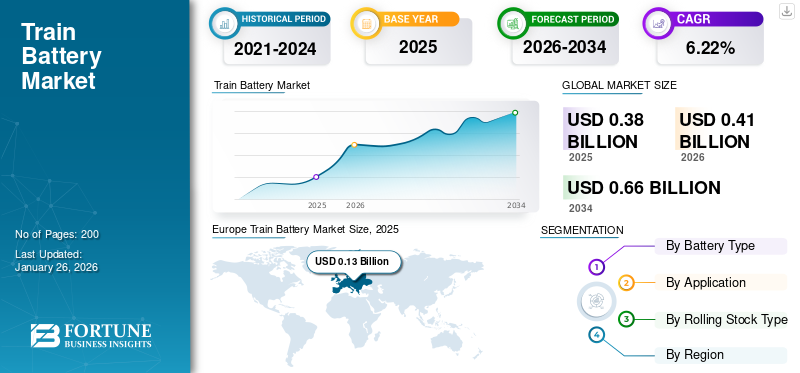

The global train battery market size was valued at USD 0.38 billion in 2025 and is projected to grow from USD 0.41 billion in 2026 to USD 0.66 billion by 2034, exhibiting a CAGR of 6.22% during the forecast period. Europe dominated the train battery market with a market share of 35.49% in 2025.

A train battery is an energy storage system installed on locomotives, multiple units, metros, or trams to supply auxiliary power for lighting, HVAC, signaling, door control, and, in some cases, traction support. These batteries, typically lead-acid, nickel-cadmium, or increasingly lithium-ion, ensure reliable operation during idling, low voltage, or emergency conditions. A key driving factor for adoption is the global shift toward cleaner, energy-efficient rail transport, with growing emphasis on hybrid and battery-powered trains to reduce carbon emissions, enhance sustainability, and comply with stricter environmental regulations.

The market encompasses several major players with Saft, EnerSys, GS Yuasa, and Exide Industries at the forefront. Broad product portfolios, continuous innovation in lithium-ion and lead-acid technologies, and strong geographic expansion across rail networks have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Train Battery Market Key Takeaways

- 2025 Market Size: USD 0.38 billion

- 2026 Market Size: USD 0.41 billion

- 2034 Forecast Market Size: USD 0.66 billion

- CAGR: 6.22% from 2026–2034

- Europe dominated the train battery market with a 35.49% share in 2025.

- Lead-acid batteries are projected to hold a 61.63% market share in 2026.

- Auxiliary applications are expected to account for 34.51% of the global market in 2026.

Europe

Europe was valued at USD 0.13 Billion in 2025 and is projected to reach USD 0.14 Billion in 2026.

Asia Pacific

Asia Pacific was valued at USD 0.14 Billion in 2025 and is projected to reach USD 0.15 Billion in 2026.

North America

North America was valued at USD 0.06 Billion in 2025 and is projected to reach USD 0.07 Billion in 2026.

U.S.

The U.S. is valued at USD 0.03 Billion in 2026.

Japan

Japan is valued at USD 0.03 Billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Rail Electrification and Modernization Programs to Propel the Market Growth

Governments worldwide are investing heavily in electrifying rail networks to cut carbon emissions and improve efficiency. Even on electrified routes, trains require reliable batteries for auxiliary loads such as lighting, HVAC, signaling, and emergency backup. Modernization initiatives also include upgrading older rolling stock with advanced energy storage systems, creating strong replacement demand. Countries such as India, China, and EU members are spearheading large-scale electrification projects, directly increasing the adoption of advanced battery technology. This dual push of expansion and retrofitting significantly accelerates train battery market growth globally.

- In March 2023, Siemens Mobility received an order from ÖBB for 27 additional Desiro ML electric trainsets, enhancing inner-Alpine regional services in Austria. These modern, low-floor trains improve comfort and capacity, reinforcing Siemens’ role in rail fleet modernization.

MARKET RESTRAINTS

Competition from Electrification and Hydrogen Could Restrain Market Expansion

In regions with extensive electrified rail networks, such as Europe and parts of Asia, trains primarily draw power from overhead catenary systems, reducing the need for large traction batteries. Simultaneously, hydrogen fuel cell technology is gaining momentum as a zero-emission alternative, especially for non-electrified routes where full electrification is costly. Several countries, including Germany and the U.K., are deploying hydrogen trains with longer ranges and faster refueling compared to battery-electric models. This dual competition limits investment and slows the adoption of battery-based solutions, constraining market expansion opportunities globally.

- In September 2025, Sierra Northern Railway unveiled the U.S.’s first hydrogen-powered switcher locomotive in West Sacramento, funded by USD 23.5 billion. The zero-emission train replaces diesel units, cutting fuel use and emissions while supporting California’s clean transportation transition.

MARKET OPPORTUNITIES

Advancements in Lithium-Ion and Solid-State Technologies to Create Lucrative Growth Opportunities

Lithium-ion batteries deliver higher energy density, longer life cycles, faster charging, and reduced maintenance compared to traditional lead-acid and nickel cadmium battery chemistries. This makes them highly suitable for modern rail applications, including hybrid and battery-electric multiple units. Solid-state batteries, still emerging, promise even greater safety, higher energy efficiency, and improved operational reliability, which could revolutionize traction and auxiliary power systems in advanced trains. As rail operators seek cost-effective, sustainable, and high-performance energy storage solutions, these next-generation train battery technologies open avenues for innovation, new product launches, and long-term growth, especially in electrification and non-electrified route operations.

- In December 2024, Škoda Group introduced its first battery-powered RegioPanter train featuring advanced lithium-titanium-oxide (LTO) batteries, enabling 80 km range off-wire. The batteries deliver faster acceleration, reliable performance, and support sustainable, zero-emission regional rail transportation in the Czech Republic.

TRAIN BATTERY MARKET TRENDS

Adoption of Battery-Powered and Hybrid Trains is one of the Significant Market Trends

The rising adoption of battery-powered and hybrid trains is a significant ongoing market trend. Countries such as Germany, the U.K., and Japan are introducing battery-electric multiple units (BEMUs) to serve non-electrified routes, reducing reliance on diesel and lowering emissions. Hybrid trains, combining catenary power with onboard batteries, provide cost-effective solutions for partially electrified networks. These developments align with global sustainability goals and also create strong demand for advanced lithium-ion batteries with higher capacity and faster charging. As rail operators modernize fleets for efficiency and compliance, the adoption of battery and hybrid trains continues to accelerate market growth.

- In April 2025, Hitachi Rail secured a major contract worth approximately USD 370 billion to build 45 “tri-mode” battery hybrid train cars for Grand Central, enhancing capacity, cutting emissions by around 30%, and supporting U.K. battery manufacturing in Newton Aycliffe.

MARKET CHALLENGES

Supply Chain and Raw Material Constraints to Challenge Market Growth

Advanced rail batteries rely heavily on lithium, cobalt, and nickel, materials concentrated in a few regions such as the Democratic Republic of Congo, Chile, and Indonesia. This geographic dependency exposes manufacturers to price volatility, export restrictions, and geopolitical risks, which disrupt stable supply. Additionally, rising global demand from the electric vehicle sector intensifies competition for these critical minerals, further tightening availability. Such uncertainties hinder long-term procurement planning for rail operators and increase production costs, making it difficult to scale the adoption of advanced battery technologies.

To address this issue, in March 2025, the European Union allocated EUR 1.8 billion (USD 1.94 billion) to strengthen the supply chain for battery raw materials, addressing the shortage of critical components such as lithium and cobalt. This initiative aims to bolster the EU's battery manufacturing sector and reduce dependence on external sources.

Download Free sample to learn more about this report.

Segmentation Analysis

By Battery Type

Widespread Use in Auxiliary Rail Applications Drives the Lead-acid Segmental Growth

On the basis of battery type, the market is classified into lead-acid, nickel-cadmium (Ni-Cd), and lithium-ion.

The lead-acid batteries segment is projected to dominate the market with a share of 61.63% in 2026.Their simple design, ease of maintenance, and established recycling infrastructure make them a preferred choice for operators with large fleets. Despite competition from lithium-ion, gel tubular lead acid battery, valve regulated lead acid battery, and regulated lead acid battery remain strong in legacy rolling stock and emerging markets where budget constraints dominate. Their ability to provide dependable emergency power and auxiliary support ensures steady demand, especially in regions with older train fleets.

- In September 2025, Germany introduced its first battery-powered train, the Giga Train, featuring advanced lead-acid batteries. This initiative supports Tesla’s sustainability goals and offers free rides, aiming to reduce CO₂ emissions by 50 tons annually.

By Application

Constant Demand across all Rolling Stock Types Fuels Auxiliary Segment Demand

In terms of application, the market is categorized into starter, auxiliary, and propulsion.

The auxiliary application segment is expected to lead the market, contributing 34.51%globally in 2026. In trains, batteries support critical systems such as lighting, HVAC, automatic doors, signaling, and emergency backup, independent of traction power supply. Increasing urbanization and metro expansion multiply auxiliary power requirements. Strict regulatory standards ensure that the trains are equipped with robust energy backup systems, making auxiliary use the most consistent and indispensable application segment. This constant demand across all rolling stock types fuels the continuous growth of battery adoption for auxiliary application globally.

- In September 2021, Wabtec unveiled its FLXdrive battery-electric locomotive in Pittsburgh. Equipped with an auxiliary battery system, it utilizes regenerative braking to recharge, enhancing energy efficiency. This innovation supports Wabtec's commitment to decarbonizing rail transport.

By Rolling Stock Type

Rising Urbanization and Commuter Transit Expansion Drive the Segment Growth

Based on rolling stock type, the market is segmented into locomotive, multiple units, passenger coaches & freight wagons, and metros /light rail/trams. The locomotive segment is further divided into ICE, electric, and hybrid. The multiple units are categorized into DMU, EMU, and hybrid.

Multiple units (EMUs and DMUs) represent the leading segment will account for 36.98% market share in 2026. With more cities investing in metro and suburban rail, multiple units require reliable auxiliary and emergency power systems for passenger services and safety. Electrification projects in Europe, Asia, and the Middle East further expand the deployment of EMUs. In contrast, hybrid multiple units with onboard batteries gain momentum on non-electrified routes. This trend makes multiple units a dominant rolling stock category, driving steady market growth.

- In July 2025, Alstom secured a USD 2.4 billion contract to deliver 316 M-9A electric multiple unit railcars to New York’s Long Island Rail Road and Metro-North Railroad. The order will modernize aging fleets with quieter, more reliable, and accessible trains, replacing 40-year-old models.

To know how our report can help streamline your business, Speak to Analyst

Train Battery Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Europe

Europe Train Battery Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

In 2025, Europe represented USD 0.13 billion, accounting for 35.49% of the worldwide market, and is projected to grow to USD 0.14 billion in 2026. Countries such as Germany, France, and the U.K. are leading in battery-electric train projects and hybrid rolling stock. EU’s Green Deal and decarbonization goals accelerate the demand for advanced battery systems. Additionally, Europe’s well-established metro and high-speed rail networks create consistent demand for auxiliary batteries. Strong local players such as Saft and Hoppecke, combined with government funding, further solidify Europe’s leadership in the global market. The UK market is projected to reach USD 0.04 Billion by 2026, while the Germany market is projected to reach USD 0.06 Billion by 2026.

- In July 2025, Turntide Technologies secured a USD 13.5 billion order to supply Hitachi Rail with Gen 2 LFP batteries for the U.K.’s first battery-powered intercity trains, boosting domestic production and safety.

Asia Pacific

The Asia Pacific market generated USD 0.14 billion in 2025, representing 35.94% of the global market landscape, and is expected to reach USD 0.15 billion in 2026. China leads with extensive high speed trains and urban rail networks, while India is rapidly expanding metro and suburban lines. Japan pioneers hybrid and battery-electric trains, showcasing advanced adoption. Growing passenger volumes and government policies promoting clean mobility accelerate the train battery demand. Local manufacturers such as GS Yuasa and Exide support regional supply. With large-scale projects and rising population mobility, the Asia Pacific is the strongest growth engine globally. The Japan market is projected to reach USD 0.03 Billion by 2026, the China market is projected to reach USD 0.07 Billion by 2026, and the India market is projected to reach USD 0.04 Billion by 2026.

- In December 2024, TKIL (formerly Thyssenkrupp Industries India) partnered with Hoppecke Batterie Systeme to develop advanced rail battery solutions in India. This collaboration aims to enhance energy efficiency and support the country's transition to sustainable rail transport.

North America

North America recorded a market size of USD 0.06 billion in 2025, capturing 17.07% of the global market share, and is projected to reach USD 0.07 billion in 2026. North America holds the third-largest share in the market due to slower rail electrification and limited adoption of commuter rail compared to Europe and Asia. Freight rail dominates the region, which relies heavily on diesel locomotives, reducing large-scale battery demand. However, urban transit projects in cities such as New York and Toronto generate auxiliary battery requirements. Growing focus on sustainable transport and pilot programs for hybrid trains offer some opportunities. However, the overall progress remains gradual, keeping North America behind other leading global markets.

The U.S. dominates the North America market owing to its large rail infrastructure and ongoing urban transit expansion. While freight remains diesel-driven, metropolitan areas such as New York, Washington, and California are investing in modern commuter and metro rail, creating auxiliary train battery demand. Federal funding for clean transport and pilot projects for hybrid trains strengthens opportunities. U.S.-based manufacturers such as EnerSys also support domestic supply. Despite slower adoption of full battery-electric trains, auxiliary needs and modernization programs keep the U.S. ahead regionally. The U.S. market is projected to reach USD 0.03 Billion by 2026.

- In June 2025, Siemens Mobility introduced the Charger B+AC, North America’s first battery-electric passenger locomotive. Built in the U.S., it runs 100 miles on battery, supports dual charging methods, and was selected by New York’s MTA and Metro-North Railroad.

Rest of the World

The rest of the world regional segment holds the smallest share in the market due to limited railway infrastructure and slower adoption of electrification. Many countries in Africa, Latin America, and parts of the Middle East heavily rely on diesel locomotives with minimal investment in metro or high-speed rail. The market in Rest of the World reached USD 0.04 billion in 2025, representing 11.50% of total market revenue, and is projected to reach USD 0.05 billion in 2026. Economic constraints and competing infrastructure priorities further restrict large-scale battery adoption. However, gradual urban transit initiatives in Gulf nations and Latin America may provide niche opportunities. Overall, the demand remains limited, keeping this region the least significant contributor globally.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations with Rolling Stock Manufacturers Help Players Gain Competitive Edge

The competitive landscape of the global market is shaped by a mix of multinational leaders and regional specialists. Key train battery players include Saft (France), EnerSys (U.S.), GS Yuasa (Japan), and Exide Industries (India), each with strong portfolios across lead-acid, nickel-cadmium, and lithium-ion technologies. European companies such as Hoppecke and Swiss-based Leclanché focus on advanced lithium-ion solutions, especially for hybrid and battery-electric trains. Competition centers on innovation, safety certifications, lifecycle cost optimization, and geographic expansion. Strategic collaborations with rolling stock manufacturers, government-backed electrification programs, and investments in next-generation chemistries such as solid-state batteries further intensify rivalry. Sustainability, recycling capabilities, and digitalized battery management systems are becoming key differentiators, shaping the long-term positioning of companies in this evolving market.

LIST OF KEY TRAIN BATTERY COMPANIES PROFILED

- Saft (TotalEnergies) (France)

- GS Yuasa (Japan)

- EnerSys (U.S.)

- Exide Industries (India)

- Hoppecke Carl Zoellner Sohn GmbH (Germany)

- Clarios (U.S.)

- East Penn Manufacturing (U.S.)

- Hitachi Rail (Japan)

- ABB (Switzerland)

- Toshiba Corporation (Japan)

- Turntide Technologies (U.K.)

- Hunan Fengri Power Electrical Co., Ltd. (China)

- Power & Industrial Battery Systems Gmbh (Germany)

KEY INDUSTRY DEVELOPMENTS

- In May 2025, South Korea's SRT unveiled plans to equip its next-generation high-speed trains with the world's first onboard lithium battery fire suppression system. This system activates automatically when internal battery temperatures exceed 120°C, enhancing safety during high-speed operations.

- In October 2024, Hitachi Rail partnered with Innovate UK, the University of Birmingham, DB ESG, and Turntide Technologies to develop a compact lithium iron phosphate (LFP) battery pack for regional trains. This initiative aims to enhance energy density and optimize low-floor train designs.

- In September 2024, Hitachi Rail, DB ESG, Innovate UK, and the University of Birmingham launched a GBP 1.4 billion (USD 1.75 billion) project to develop compact, high-density LFP train batteries, targeting 40% size reduction and 22% higher efficiency for commuter trains.

- In September 2024, Saft (a TotalEnergies subsidiary) began delivering innovative lithium-titanate-oxide (LTO) traction batteries to Siemens Mobility for its Mireo Plus H hydrogen trains. These batteries, forming a hybrid system with fuel cells, boost acceleration and braking efficiency while offering enhanced safety and a lifecycle up to ten times longer.

- In September 2024, ABB launched its new Pro Series traction battery at InnoTrans in Berlin, designed for hybrid and fully electric trains. It offers high energy density, modular scalability, rapid charging (80% in just 10 minutes), and a long lifespan of over 20,000 cycles.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.22% from 2026-2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Battery Type · Lead-acid · Nickel-Cadmium (Ni-Cd) · Lithium-ion |

|

By Application · Starter · Auxiliary · Propulsion |

|

|

By Rolling Stock Type · Locomotive · Multiple Units · Passenger Coaches & Freight Wagons · Metros /Light Rail/Trams |

|

|

By Geography · North America (By Battery Type, Application, Rolling Stock Type, and Country) o U.S. o Canada o Mexico · Europe (By Battery Type, Application, Rolling Stock Type, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Battery Type, Application, Rolling Stock Type, and Country) o China o Japan o India o Rest of Asia Pacific · Rest of the World (By Battery Type, Application, Rolling Stock Type, and Country) o South America o The Middle East · Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 0.38 Billion in 2025 and is projected to reach USD 0.66 million by 2034.

In 2025, the Europe market value stood at USD 0.13 million.

The market is expected to exhibit a CAGR of 6.22% during the forecast period of 2026-2034.

The lead-acid batteries segment leads the market by battery type.

Key factors driving the market include rail electrification, rising metro projects, sustainability goals, technological advancements in lithium-ion batteries, modernization of rolling stock, and government initiatives promoting clean, energy-efficient rail transport solutions globally.

Top players in the market comprise Saft (France), EnerSys (U.S.), GS Yuasa (Japan), Exide Industries (India), and Hoppecke (Germany).

Europe dominated the train battery market with a market share of 35.49% in 2025.

Major factors favoring product adoption include rail electrification, demand for sustainable transport, metro expansion, advances in lithium-ion technology, stricter safety standards, and government policies promoting low-emission mobility solutions.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us