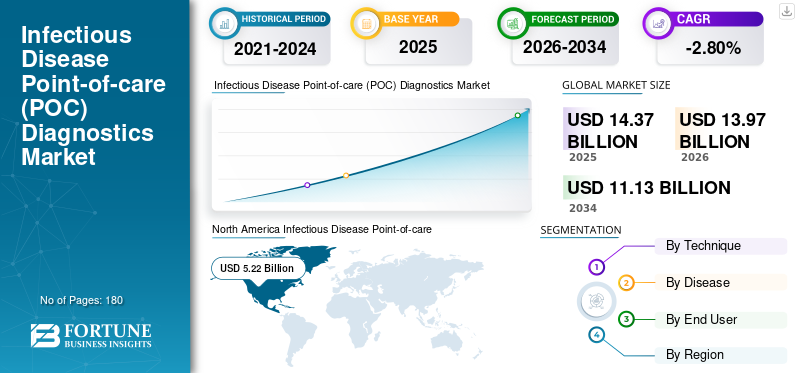

North America dominated the infectious disease point-of-care diagnostics market with a valuation of USD 5.22 billion in 2025 and USD 5.07 billion in 2026. The dominance of this region is attributable to the increasing adoption of advanced point-of-care diagnostics for the detection of various infectious diseases. Moreover, an increasing number of strategic partnerships amongst governmental organizations and players emphasizing the development of rapid diagnostic tests boosts the adoption of point-of-care diagnostics for various infectious diseases in the region. For instance, in February 2021, Thermo Fisher Scientific Inc. completed the acquisition of Mesa Biotech, Inc. The acquisition aimed to expand the POC molecular diagnostic portfolio of Thermo Fisher Scientific Inc. with the help of Accula System, an easy-to-use, POC PCR-based testing platform for infectious disease testing.

Infectious Disease Point-of-care (POC) Diagnostics Market Size, Share & COVID-19 Impact Analysis, By Technique (Lateral Flow Immunoassay, Agglutination Test and Others), By Disease (HIV, Hepatitis B Virus, Pneumonia/Streptococcus Associated Infections, RSV, Influenza, Clostridium Difficile Infections, Hepatitis C Virus, Methicillin-Resistant Staphylococcus Aureus, Tuberculosis, and Others), By Disease, COVID-19 Point-of-care (POC) Diagnostics, By End User (Hospital Bedside, Physicians Office Lab, Urgent Care & Retail Clinics and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

The global infectious disease point-of-care diagnostics market size was estimated at USD 14.37 billion in 2025. The market is expected to rise from USD 13.97 billion in 2026 to USD 11.13 billion by 2034, expanding at a CAGR of -2.80% from 2026 to 2034. North America dominated the infectious disease point-of-care diagnostics market with a market share of 36.30% in 2025. Moreover, the U.S. infectious disease point-of-care diagnostics market size is projected to grow significantly, reaching an estimated value of USD 4.05 billion by 2030, driven by increasing number of product approvals and launches for infectious disease diagnosis.

Infectious disease point-of-care (POC) diagnostics tests are important for diagnosing diseases and improving global health. Traditional diagnoses of infectious diseases resulted in inaccurate results and were time-consuming. This flaw led to the emergence of rapid, accurate, and portable point-of-care testing products in the market.

Point-of-care testing enables faster diagnosis of infectious diseases near the patient site providing quick results. Several researchers are now focused on developing multiplex point-of-care diagnostic technologies (MPOCTs). These MPOCT devices consist of hybridization papers, array settings, bead technology, or microfluidic systems that reduce the assay steps and provide diagnosis results in 15-30 minutes. The launch of new technology has transformed the accuracy, ease of use, and testing speed. Thus, technological advancements and growing opportunities for exploring ways to accelerate the development of the infectious disease point-of-care (poc) diagnostics are anticipated to leverage the market potential during the forecast timeframe.

Download Free sample to learn more about this report.

Global Infectious Disease Point-of-Care Diagnostics Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 14.37 billion

- 2026 Market Size: USD 13.97 billion

- 2034 Forecast Market Size: USD 11.13 billion

- CAGR: -2.8% from 2026–2034

Market Share:

- North America dominated the infectious disease point-of-care (POC) diagnostics market with a 36.30% share in 2025, driven by the increasing adoption of advanced POC diagnostic technologies, product approvals, and strategic partnerships for infectious disease testing.

- By technique, the lateral flow immunoassay segment is expected to retain its largest market share owing to its ease of use, rapid turnaround time, and widespread availability of test kits in decentralized healthcare settings.

Key Country Highlights:

- United States: Growth is driven by the rising number of product approvals and launches for infectious disease diagnostics, along with a growing inclination towards decentralized rapid testing.

- Europe: Strategic acquisitions and collaborations among key players to enhance infectious disease POC diagnostics portfolios are propelling market growth.

- China: Increasing prevalence of infectious diseases and investments in developing rapid diagnostic platforms are accelerating market adoption.

- Japan: Technological advancements in multiplex diagnostic platforms and emphasis on improving diagnostic speed and accuracy are driving demand.

COVID-19 IMPACT

Launch of POC Kits for COVID-19 Infection Improved Disease Diagnostics Management

The COVID-19 pandemic moderately affected the global market for Infectious disease point-of-care diagnostics as pharmaceutical companies and research institutes were focused on developing infectious disease POC diagnostics for COVID-19 diagnosis. The introduction of advanced products and quick turnaround time kits boosted the market growth in the forecast period. For instance, in July 2020, BD (Becton, Dickinson, and Company) announced that the U.S. Food and Drug Administration (FDA) granted Emergency Use Authorization (EUA) for rapid, point-of-care SARS-CoV-2 diagnostic test for use with its broadly available BD Veritor Plus System. However, demand and sales for diagnosis products related to infectious diseases such as MRSA (methicillin-resistant Staphylococcus aureus), HIV (Human Immunodeficiency Virus), and CDI (Clostridium difficile infection) declined due to disruptions in the supply chain and imposition of lockdown measures.

Moreover, a decline in the routine testing of diagnostic procedures for various infectious diseases other than COVID-19 was observed for a short-term period.

Infectious Disease Point-of-care Diagnostics Market TRENDS

Application of Nanotechnology for Infectious Disease Diagnosis has Attracted Huge Investments

Despite the tremendous efforts put into managing infectious diseases, the development of low-cost, accurate, and sensitive POC products is in massive demand. Nanotechnology has opened the doors for widespread applications in the healthcare industry. Researchers across the globe have emphasized the introduction of nanoparticle-based and nano-device-based POC platforms and tests. For instance, according to an article published in December 2022, a research team from the universities of Wurzburg and Erlangen in Bavaria, Germany, developed a novel and very sensitive rapid test based on specially designed magnetic nanoparticles. With the help of a mobile measuring device, the test takes only a few seconds to reliably detect antibodies against the SARS-CoV-2 coronavirus from a saliva sample. The unique property of nanoparticles, with the high surface area-to- volume ratio , makes them suitable for numerous applications.

Moreover, disease diagnosis can be done using a minimal volume of samples in kits prepared using nanotechnology to obtain real-time results of patients. Therefore, nanotechnology application provides reliable and rapid results for infectious disease diagnosis.

- North America witnessed a infectious disease point of care diagnostics market growth from USD 5.91 Billion in 2021 to USD 5.68 Billion in 2022.

Download Free sample to learn more about this report.

DRIVING FACTORS

Increasing Prevalence of Infectious Diseases to Foster Demand for Rapid Infectious Disease Point-of-care (POC) Diagnostics Kits

Globally, the increasing prevalence of HIV, Influenza, and RSV, has led to a surge in patient diagnosis rate. For instance, according to the WHO 2023 Factsheet, around 38.4 million people were living with HIV in 2021. Among them, 650,000 people died from HIV-related causes and 1.5 million people acquired HIV

Moreover, the WHO 2022 Factsheet shows that around 354 million people live with Hepatitis B or C worldwide. Thus, the growing infection rate of various diseases globally will increase the uptake of infectious disease point-of-care products for its diagnosis and subsequently aid the market growth during the forecast period.

Rising Inclination Toward Decentralized Health Care System to Aid Industry Growth

Owing to advantages such as quick turnaround time and the ability to make immediate treatment decisions, POC diagnosis has become a crucial part of patient-centric healthcare. There has been a preferential shift from centralized to decentralized point-of-care testing for infectious diseases, improving patient care. The growing demand for rapid tests has encouraged the market players to supply POC products to decentralized locations, thereby driving this market. For instance, in May 2022, miDiagnostics, a Belgium-based POC Diagnostics Company, launched a CE-IVD certified ultra-fast COVID-19 PCR test for decentralized testing. The restrictions during the pandemic, the requirement of routine testing, and the urgency for rapid test outcomes have driven the demand for rapid decentralized testing at locations such as airports, and large corporations. Thus, the adoption of rapid diagnostic testing in decentralized healthcare settings allows the ease of accessibility of infectious disease point-of-care diagnostics among less-trained personnel and eliminates the need to transport samples to the core labs. The factors mentioned above are anticipated to accelerate the infectious disease point-of-care diagnostics market growth.

RESTRAINING FACTORS

Lack of Accuracy Associated with Point-of-care Diagnostics Tests to Reduce Product Adoption

A major portion of the global population with infectious diseases such as HIV, malaria, and tuberculosis resides in developing countries. In low-middle income countries, lack of training among clinicians and poor product accessibility due to lower per capita expenditure has decreased POC kit adoption. Additionally, issues such as nonadherence to test procedures, operator incompetence, and use of uncontrolled reagents & equipment have led to an increased rate of errors in infectious disease POC tests. For instance, according to an article published by the American Association for Clinical Chemistry in April 2022, the two major challenges associated with POCT testing are test errors and quality control. Similarly, according to an article published in NCBI in 2022, in the U.K., 66 laboratories confirmed that there was no POCT training. These findings demonstrated a clear lack of POCT teaching and training, resulting in a shortage of required skills among biomedical scientists in the U.K. Thus, increasing accuracy errors due to several reasons, including a lack of skilled professionals, results in misinterpretation and is likely to hamper the market growth.

SEGMENTATION ANALYSIS

By Technique Analysis

Ease of Use and Availability of Lateral Flow Kits Fostered the Segment Growth

Based on technique, the market is segmented as lateral flow immunoassay, agglutination test, flow-through/Immuno-concentration assay, and molecular diagnostics.

The lateral flow immunoassay segment held a dominant infectious disease point-of-care (POC) diagnostics market share in 2022. This is owing to the availability of test kits and the benefit of faster diagnosis in decentralized settings. The segment’s growth has also been bolstered by an increase in product launches, spurred by the challenges posed by the COVID-19 outbreak.

The molecular diagnostics segment is likely to exhibit the highest CAGR over the forecast period. This is on account of the rising application of concepts such as ELISA and RT-PCR in infectious disease POC testing kits. Additionally, the rise in the number of product launches is likely to boost the segment sales. For instance, in May 2022, BD announced the U.S. launch of BD COR MX, a fully automated high-throughput infectious disease molecular diagnostics platform.

- The Lateral Flow Immunoassay segment is expected to hold a 31.2% share in 2026.

To know how our report can help streamline your business, Speak to Analyst

Furthermore, the flow-through test/immunoconcentration assay segment is poised for substantial growth with a noteworthy CAGR over the analysis period. This rise is driven by the growing introduction of advanced kits by an increasing number of industry participants in the global market. These kits are based on the flow-through technique. Furthermore, rising awareness regarding the efficacy of agglutination tests for the diagnosis of infectious diseases is expected to propel the agglutination test segment growth during the analysis period.

By Disease Analysis

Increasing Sales of POC Kits to Boost CDI Revenue Growth

Based on disease, the market is segmented into clostridium difficile infections (CDI), influenza, pneumonia/streptococcus-associated infections, hepatitis C virus, respiratory syncytial virus, tuberculosis, MRSA, HIV, hepatitis B virus, and others.

The global incidence rate of infectious diseases and rising under diagnosis burden has resulted in the rapid adoption of POC testing kits. CDI accounted for the highest market share in 2022 due to the huge sales volume of POC kits for CDI diagnosis. The increasing prevalence of CDI in developing countries is raising the demand for infectious disease POCT kits, contributing to market growth. For instance, according to an article published in March 2023 by the International Journal of Infectious Diseases, based on the 50 studies, the pooled prevalence of CDI in China was 11.4% in the past 5 years. In critical care units and hospitals, the clostridium difficile infections is emerged as the most prevalent infection, consequently spurring a substantial demand for POC CDI diagnosis kits.

The prominent cause of acute respiratory infection, influenza, has driven an increased adoption of infectious disease POC diagnostics products to facilitate timely disease management. Moreover, the surging research and development investments in advanced POC kits in emerging nations are likely to bolster the influenza segment growth. For instance, in November 2022, Virax Biolabs, a U.K.-based Biotechnology Company, announced the launch of the RSV-Influenza-COVID Triple Virus Antigen Rapid Test Kit in the European Union. The test kits are designed for use in point-of-care settings and at home, enabling individuals to identify infections associated with respiratory syncytial virus (RSV), influenza, and COVID-19. The results from these tests are typically available in 15 minutes. Likewise, increased sales of products for diagnosing other diseases, such as HIV, MRSA, and tuberculosis are also responsible for the growth of this segment.

By End User Analysis

Hospital Bedside Segment to Dominate Stoked by Rising Hospital Stays of Patients

In terms of end-user, the market is segmented into hospital bedside, physician's office labs, urgent care & retail clinics, home & self-testing, nursing homes, and others.

The hospital bedside segment is expected to account for a dominant market share during the forecast period. Its dominance is attributable to increased hospital stays of patients suffering from infectious diseases. This has led to a rise in the demand for infectious disease point-of-care diagnostics in hospital settings.

The urgent care & retail clinics are expected to grow at the highest CAGR during the forecast period due to the increasing number of stand-alone urgent care & clinics in developed and emerging countries. During the unprecedented times of COVID-19, other testing facilities, drive-through centers, and others have gained traction. For instance, according to a news article, published in January 2023, around 11,150 urgent care centers have emerged around the U.S. This is likely due to the need for rapid diagnosis of coronavirus infections.

Besides this, the home & self-testing segment is expected to register significant growth over the forecast period. This is owing to the rising preference shift of patients from hospital to home care diagnosis.

REGIONAL Analysis

North America Infectious Disease Point-of-care (POC) Diagnostics Market 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

Europe

Europe held the second-largest market share and this market is expected to grow at a significant CAGR over the forecast period. This is owing to the rising strategic alliances between key players. For instance, in February 2023, BIOSYNEX SA announced the acquisition of Chembio Diagnostics, Inc., intending to strengthen its POC testing portfolio. Also, in December 2021, F. Hoffmann-La Roche Ltd announced the acquisition of TIB Molbiol Group. The acquisition aimed to increase capabilities for rapidly developing assays for infectious diseases.

Asia Pacific

The market in Asia Pacific will exhibit the highest CAGR owing to the increased penetration of market players and higher adoption of POC diagnostics kits. In addition to this, market players in this region are making massive investments, which will fuel demand for advanced products. For instance, in June 2022, Cipla Limited signed an agreement to partially acquire Achira Labs Private Limited. The acquisition aimed to develop and commercialize point-of-care medical test kits in India, where Achira Labs Private Limited specializes in developing POC molecular assays and immunoassays across the clinical areas of infectious diseases.

Latin America and the Middle East & Africa

The market for Latin America and the Middle East & Africa infectious disease point-of-care diagnostics accounted for a lower market share compared to other three regions, due to a lack of awareness among the healthcare community and the benefits of point-of-care diagnosis.

KEY INDUSTRY PLAYERS

F. Hoffmann-La Roche Ltd, Cepheid Inc., and Abbott Laboratories to Lead the Market With Strong Product Portfolio

The market for infectious disease point-of-care diagnostics is semi-consolidated owing to the strong product portfolios and remarkable distribution network of major companies in developed and emerging countries. F. Hoffmann-La Roche AG, Cepheid Inc., and Abbott Laboratories lead the market, accounting for a dominant share in 2022. The launch of diagnostic products, coupled with strategic collaborations with the key industry players, is likely to foster the growth of the companies leading to higher market share. However, the potential opportunities provided by the market are enabling the entry of several domestic players in the forthcoming years. This will result in a slightly fragmented market by 2030. For example, in September 2021, LumiraDx, the U.K.-based announced the completion of the merger with CA Healthcare Acquisition Corp. (CHAC). The merger enabled LumiraDx to expand its portfolio and drive transformation in diagnostic testing with a pipeline of 30+ assays across common health conditions, including infectious diseases, cardiovascular diseases, diabetes, and coagulation disorders.

Other key players, such as bioMérieux, BD, Quidel Corporation, and Danaher Corporation, and others, have also entered the market competition with novel advanced infectious disease POC products.

LIST OF KEY COMPANIES PROFILED:

- F. Hoffmann-La Roche Ltd (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- BD (U.S.)

- bioMérieux SA (France)

- Cardinal Health, Inc. (U.S.)

- Cepheid (U.S.)

- Trinity Biotech (Ireland)

- Quidel Corporation (U.S.)

- Bio-Rad Laboratories Inc. (U.S)

KEY INDUSTRY DEVELOPMENTS:

- January 2023 - Cipla Inc. launched a point-of-care testing device, Cippoint. The device is CE IVD-approved and helps diagnose non-communicable and infectious diseases.

- February 2022 - Trinity Biotech received approval for its TrinScreen HIV, an HIV screening product, from the World Health Organization (WHO). It is a rapid test providing results in less than 12 minutes from a finger stick drop of blood.

- October 2021 – Hologic, Inc. announced the launch of the Aptima SARS-CoV-2/Flu Assay, a multiplex COVID-19/flu test, in North America and Europe to detect three respiratory viruses SARS-CoV-2, influenza A, and influenza B.

- April 2021 – Chembio Diagnostics, Inc. announced the launch of the rapid point-of-care COVID-19 /Flu A&B test. The test provides results within 15 minutes.

- March 2021 – Roche announced the launch of Cobas SARS-CoV-2 Variant Set 1 Test. This test was developed to detect the COVID-19 variants found in the U.K., South Africa, and Brazil.

REPORT COVERAGE

The infectious disease point-of-care diagnostics market report provides a detailed analysis of the industry and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the market research report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of -2.8% from 2026-2034 |

|

Segmentation |

By Technique

|

|

By Disease

|

|

|

By End-User

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is valued at USD 13.97 billion in 2026, projected to reach USD 11.13 billion by 2034 at a CAGR of -2.80% during 2026–2034.

In 2025, North America stood at USD 5.22 billion.

The market will exhibit a CAGR of -2.8% during the forecast period (2026-2034).

The molecular diagnostics segment is expected to be the leading segment in this market during the forecast period.

The increasing prevalence of infectious diseases and the introduction of advanced POC products by market players are major factors driving the growth of the market.

F. Hoffmann-La Roche Ltd., Cepheid, and Abbott Laboratories are major players in the global market.

North America dominated the market share in 2022.

Increased burden of under-diagnosis of infectious disease and demand for POC products by emerging nations are expected to drive the adoption in the global market.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us