Insulin Market Size, Share & Industry Analysis, By Type (Human Insulin and Insulin Analogs), By Product Type (Long-acting & Ultra-long-acting Insulin, Rapid-acting Insulin, Intermediate-acting Insulin, Combination, and Others), By Drug Type (Branded and Biosimilar), By Disease Type (Diabetes Type 1, Diabetes Type 2, and Others), By Age Group (Pediatrics and Adults), By Route of Administration (Subcutaneous, Inhaled, and Others) By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, and Online Pharmacies & Others), and Regional Forecast, 2026-2034

Insulin Market Size and Future Outlook

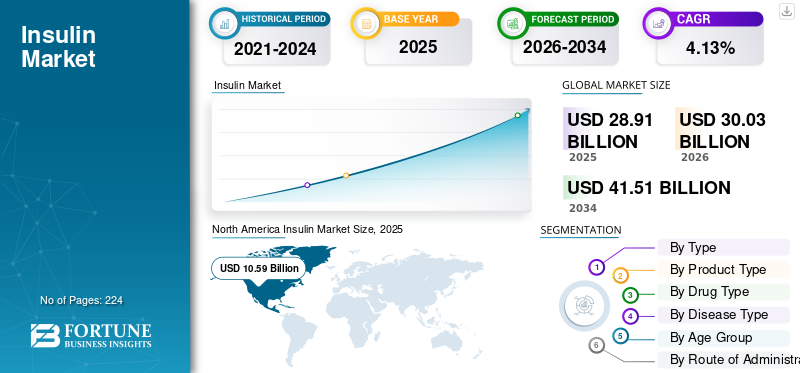

The insulin market size was valued at USD 28.91 billion in 2025. The market is projected to grow from USD 30.03 billion in 2026 to USD 41.51 billion by 2034, exhibiting a CAGR of 4.13% during the forecast period. North America dominated the insulin market with a market share of 36.63% in 2025.

The market includes insulin products used for the treatment and management of diabetes, mainly type 1 diabetes and insulin-requiring type 2 diabetes. The market growth is driven by rising global burden of diabetes, increasing diagnosis and treatment rates, greater use of long-acting and rapid-acting analog insulin, and the continued need for lifelong insulin therapy in type 1 diabetes. The market is also influenced by broader access to insulin in emerging countries, increasing uptake of biosimilar and affordable human insulin products.

Prominent firms operating in the market include Novo Nordisk, Eli Lilly and Company, and Sanofi, among others. These companies are strengthening their positions through broad insulin portfolios spanning basal, prandial, premixed, and biosimilar insulin products, along with a stronger focus on cost-competitive offerings and regional manufacturing expansion.

Download Free sample to learn more about this report.

Insulin Market Key Takeaways

- 2025 Market Size: USD 28.91 billion

- 2026 Market Size: USD 30.03 billion

- 2034 Forecast Market Size: USD 41.51 billion

- CAGR: 4.13% from 2026–2034

- North America dominated the market with a 36.63% share in 2025.

- Long-acting & ultra-long-acting insulin segment is expected to hold a 32.9% share in 2026.

- Retail pharmacies & drug stores segment is expected to hold a 55.7% share in 2026.

North America

The market reached USD 10.59 billion in 2025, driven by high insulin analog adoption and advanced delivery systems.

Asia Pacific

The market is projected to reach USD 7.28 billion by 2026, driven by rising diabetes prevalence and improving healthcare access.

Europe

The market is expected to grow at a 3.22% CAGR, supported by strong reimbursement systems and increasing biosimilar adoption.

U.S.

The market is projected to reach USD 10.06 billion by 2026, driven by a large diagnosed diabetes population.

Japan

The market is projected to reach USD 1.10 billion by 2026, supported by growing insulin adoption and diabetes management initiatives.

Read More

INSULIN MARKET TRENDS

Advancements in Insulin Delivery Technologies is a Remarkable Market Trend

Improvements in insulin delivery technologies are becoming a significant trend in the market, with diabetic patients and healthcare providers favoring options that enhance dosing precision, ease of use, and glucose management. The traditional use of vials and syringes is slowly being enhanced by prefilled pens, smart insulin pens, patch pumps, and automated insulin delivery systems, which can lessen the manual dosing workload. This trend is particularly significant for patients needing several daily insulin doses, as connected devices can aid in tracking doses, sending reminders, and enhancing treatment adherence. The combination of insulin pumps, continuous glucose monitoring systems, and dosing algorithms is broadening insulin delivery's function from basic administration to more tailored diabetes management. With advancements in these technologies, managing diabetes insulin therapy is becoming more straightforward for individuals with type 1 diabetes as well as those with insulin-dependent type 2 diabetes. This is anticipated to enhance the uptake of premium insulin delivery methods and boost the demand for insulin products that work with advanced delivery systems. These factors are supporting the overall insulin market growth.

- For instance, in February 2025, Tandem Diabetes Care announced that the U.S. FDA cleared its Control-IQ+ automated insulin delivery technology for adults with type 2 diabetes, expanding automated insulin delivery beyond its traditional type 1 diabetes base.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Prevalence of Diabetes is Propelling Market Growth

The increasing prevalence of diabetes significantly boosts the market, as a larger number of diagnosed patients directly heightens the demand for insulin treatment in type 1 diabetes and advanced type 2 diabetes. Individuals with type 1 diabetes need insulin for life, whereas numerous type 2 diabetes patients may later require basal, premixed, or mealtime insulin when oral medications and lifestyle changes become insufficient. With the increasing prevalence of diabetes in both developed and emerging nations, the need for human insulin, insulin analogs, biosimilars, and cost-effective tender-based products rises. The increasing count of undiagnosed patients generates future treatment needs as screening and diagnosis advance. This trend holds particular significance in densely populated nations such as China, India, the U.S., Brazil, and Mexico, where insulin-dependent type 2 diabetes significantly drives volume growth. Consequently, producers are enhancing insulin availability, increasing biosimilar supply, and boosting local production to cater to a growing diabetes population. All these factors cumulatively drive the overall market growth.

- For instance, in April 2025, the International Diabetes Federation (IDF) released new estimates from the IDF Diabetes Atlas 11th edition, stating that 589 million adults globally are living with diabetes, with 252 million adults unaware they have the condition, and the number of adults with diabetes projected to reach 853 million by 2050.

MARKET RESTRAINTS

High Cost of Insulin Therapy to Hamper Market Growth

The elevated expense of insulin therapy continues to be a significant barrier for the global market, as affordability directly influences treatment initiation, adherence, and the consistency of refills. Insulin is a long-term treatment for individuals with type 1 diabetes and is necessary for numerous patients with advanced type 2 diabetes, highlighting that even modest out-of-pocket expenses can turn into a constant financial strain. When patients postpone prescriptions, lower doses, or limit insulin due to expenses, the overall market penetration is hindered despite significant clinical demand. Elevated costs compel payers and governments to implement tougher reimbursement regulations, competitive bidding, and a preference for more affordable biosimilar or human insulin options. This may restrict revenue expansion for high-end branded analog insulin, particularly in price-sensitive regions. Therefore, the market encounters pricing challenges despite increasing patient demand, rendering affordability; one of the key obstacles to sustainable market growth.

- For example, in November 2025, a Yale-led study published in the Journal of General Internal Medicine found that one in four patients at Yale Diabetes Center rationed insulin due to cost in 2024, unchanged from 2017, while more than one-third reported rationing due to broader access barriers. This shows that insulin affordability remains a real restraint even after policy efforts to reduce patient costs.

MARKET OPPORTUNITIES

Increasing Awareness of Disease Management to Offer Market Growth Opportunities

Increasing awareness of disease management creates a strong market opportunity for the market, as better patient education improves diagnosis, treatment initiation, and long-term adherence to insulin therapy. Many people with diabetes delay insulin use due to fear of injections, poor understanding of disease progression, or limited knowledge of glucose control targets. As awareness programs expand, patients are more likely to understand when insulin is needed, how to use it safely, and how to avoid complications such as kidney disease, nerve damage, vision loss, and cardiovascular events. This supports demand for insulin analogs, biosimilar insulin, premixed insulin, and easier-to-use delivery formats. Awareness initiatives also help healthcare providers promote self-management, dose monitoring, lifestyle control, and regular follow-up. As a result, stronger disease-management awareness can convert underdiagnosed and undertreated patients into regular therapy users, creating growth opportunities across both developed and emerging markets. All these factors would drive the market growth in the coming years.

- For instance, in November 2025, the World Health Organization (WHO) used World Diabetes Day 2025 to highlight the theme “Diabetes across life stages,” emphasizing access to integrated care, supportive environments, and policies that promote diabetes self-management and overall well-being. This supports the opportunity for insulin and diabetes-care companies as better awareness and self-management practices can improve treatment adoption and continuity.

MARKET CHALLENGES

Competition from Alternative Diabetes Treatments a Prominent Challenge to Market Growth

Competition from other diabetes therapies poses a significant challenge for the market, particularly in type 2 diabetes, where there is a growing trend toward GLP-1 receptor agonists, dual GIP/GLP-1 therapies, and SGLT2 inhibitors prior to starting insulin. These treatments can enhance blood sugar management while providing advantages such as weight loss, lowering cardiovascular risks, or protecting the kidneys, making them appealing to doctors, insurers, and patients. Consequently, certain patients with type 2 diabetes might postpone starting insulin or need reduced insulin levels, limiting the growth opportunities for basal and premixed insulin products. This issue is more apparent in advanced markets, where reimbursement policies and clinical protocols promote wider utilization of GLP-1 and SGLT2 treatments. Insulin is still crucial for type 1 diabetes and advanced type 2 diabetes, but its significance in treating earlier stages of type 2 diabetes is encountering increased competition. Insulin manufacturers need to compete not just on pricing and accessibility, but also on ease of use, safety, and compatibility with advanced delivery technologies. All the factors cumulatively affect the market growth.

- For instance, in April 2025, Eli Lilly announced positive Phase 3 results for orforglipron, an oral GLP-1 receptor agonist for adults with type 2 diabetes, reporting significant A1C reduction and weight loss versus placebo.

Segmentation Analysis

By Type

Improved Clinical Performance and Convenience Supported Insulin Analog Segment Dominance

On the basis of type, the market is segmented into human insulin and insulin analogs.

The insulin analogs segment captured the largest insulin market share in 2025. The segment’s dominance is due to the fact that analog products are widely preferred for their improved action profiles, dosing flexibility, and stronger fit with modern diabetes management compared to conventional human insulin. Additionally, clinical guidelines increasingly support analog use in key patient group, further propelling the segment dominance. Moreover, the growing availability of biosimilar analogs is improving affordability, allowing analog insulin to expand in price-sensitive markets as well.

- For instance, in March 2026, Novo Nordisk announced that the U.S. FDA approved Awiqli (insulin icodec-abae), the first once-weekly basal insulin treatment for adults with type 2 diabetes.

The human insulin segment is anticipated to rise with a CAGR of 3.17% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Product Type

Strong Basal Insulin Use and Longer Duration Benefits Supported Long-acting & Ultra-long-acting Segment’s Leading Position

On the basis of product type, the market is segmented into long-acting & ultra-long-acting insulin, rapid-acting insulin, intermediate-acting insulin, combination, and others.

The long-acting & ultra-long-acting insulin segment accounted for the largest market share in 2025. This is due to basal insulin remains a core treatment option for both type 1 diabetes and insulin-requiring type 2 diabetes. Additionally, many type 2 diabetes patients start insulin therapy with basal insulin before moving to more complex basal-bolus regimens, which supports a larger treated patient base for this segment. Moreover, the availability of biosimilar basal insulin has also improved affordability and widened access in several markets. Furthermore, the segment is set to hold 32.9% share in 2026.

- For instance, in September 2024, Eli Lilly announced Phase 3 results for its once-weekly basal insulin efsitora alfa, showing A1C reduction comparable to daily basal insulin in adults with type 2 diabetes who were starting basal insulin or switching from daily basal insulin therapy.

The rapid acting insulin segment is growing at a CAGR of 4.26% over the forecast period.

By Drug Type

Strong Brand Equity, Prescriber Confidence, and Broad Product Access Supported Branded Segment Dominance

Based on drug type, the market is classified into branded and biosimilars.

The branded segment dominated the global market in 2025. The segment’s growth is driven by long-standing physician trust, broad reimbursement coverage, strong clinical familiarity, and established global supply networks. Additionally, branded insulin companies have maintained market strength through large-scale manufacturing, patient affordability programs, device-supported formats, and strong distribution across hospital and retail pharmacies.

- For instance, September 2025, Sanofi expanded its U.S. insulin affordability program by offering a 30-day supply of any Sanofi insulin for USD 35 to all patients with a valid prescription, regardless of insurance status.

The biosimilars segment is anticipated to rise with a CAGR of 5.88% over the forecast period.

By Disease Type

Large Patient Pool and Progressive Treatment Need Supported Type 2 Diabetes Segment Dominance

In terms of disease type, the market is segmented into diabetes type 1, diabetes type 2, and others.

The diabetes type 2 segment captured the highest share of the global market in 2025. The segment’s dominance can be attributed to the fact that type 2 diabetes accounts for the largest share of the global diabetes population and creates a broad insulin-treated patient base. This is mainly as many type 2 diabetes patients eventually require insulin when lifestyle changes, oral medicines, or non-insulin injectables are no longer sufficient to maintain glycemic control. Additionally, the growing burden of obesity, aging populations, sedentary lifestyles, and longer disease duration is increasing the number of patients progressing to insulin therapy. Furthermore, the segment is set to hold 71.9% share in 2026.

- For instance, according to the International Diabetes Federation, over 90% of people with diabetes have type 2 diabetes.

The others segment is anticipated to rise with a CAGR of 4.02% over the forecast period.

By Age Group

Larger Adult Diabetes Burden and Higher Insulin-Treatment Need Supports Segmental Growth

On the basis of age group, the market is divided into pediatrics and adults.

The adults segment captured the highest share of the global market in 2025. The segment’s growth is driven by the high demand from adult patients with type 1 diabetes and insulin-requiring type 2 diabetes. Additionally, older adults often have longer disease duration, multiple comorbidities, and higher need for basal or premixed insulin to maintain glycemic control. The adult segment also benefits from wider use of premium insulin analogs, prefilled pens, and connected insulin-management tools, specially in developed markets.

- For instance, in November 2025, Dexcom announced that Dexcom Smart Basal received U.S. FDA clearance as the first CGM-integrated basal insulin dosing optimizer for adults aged 18 and older with type 2 diabetes who use long-acting insulin.

The pediatrics segment is anticipated to rise with a CAGR of 3.66% over the forecast period.

By Rote of Administration

Established Injection Use and Broad Product Availability Supported Subcutaneous Segment Dominance

On the basis of route of administration, the market is segmented into subcutaneous, inhaled, and others.

The subcutaneous segment dominated the market as most commercially available insulin products are designed for injection under the skin through vials, cartridges, prefilled pens, and pump-compatible formulations. This is mainly due to subcutaneous administration supports routine outpatient diabetes management and is suitable for basal, rapid-acting, intermediate-acting, and premixed insulin products. Additionally, long-acting and rapid-acting analogs are commonly prescribed in pen-based subcutaneous formats, making this route more convenient and familiar for patients requiring daily insulin therapy. Moreover, the broad availability of subcutaneous biosimilar and branded insulin products also supports affordability and access across developed and emerging markets. Furthermore, the segment is set to hold 98.4% share in 2026.

- For instance, in July 2025, Biocon Biologics announced U.S. FDA approval of Kirsty (insulin aspart-xjhz), the first interchangeable rapid-acting insulin aspart biosimilar in the U.S. The company stated that Kirsty will be available as a single-patient-use prefilled pen for subcutaneous use and a multiple-dose vial for subcutaneous and intravenous use.

The inhaled segment is anticipated to rise with a CAGR of 7.81% over the forecast period.

By Distribution Channel

Retail Pharmacies & Drug Stores Segment Leads Due to Strong Prescription Refill Base and Broad Patient Access

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and online pharmacies & others.

In 2025, the retail pharmacies & drug stores segment held the leading position in the global market. Retail pharmacies provide easier access for repeat dispensing, insurance processing, affordability programs, and substitution of biosimilar or lower-cost insulin where permitted. Moreover, the wide presence of retail chains and independent pharmacies therefore makes this channel the most practical route for chronic insulin access. These factors have helped retail pharmacies & drug stores maintain the leading share in the market. Furthermore, the segment is set to hold 55.7% share in 2026.

- For instance, in October 2025, the State of California announced that CalRx insulin glargine pens would soon be available for purchase, with pharmacies able to buy the product for USD 45 per five-pack and consumers offered a suggested retail price of no more than USD 55 per five-pack.

In addition, online pharmacies & others segment is projected to withness 5.60% growth rate during the forecast period.

Insulin Market Regional Outlook

By geography, the market is divided into North America, Latin America, Asia Pacific, Europe, and the Middle East & Africa.

North America

North America Insulin Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market reached USD 10.37 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 10.59 billion. The regional growth is supported by a large diagnosed diabetes population, high use of insulin analogs, strong adoption of basal and rapid-acting insulin, and wider use of advanced delivery formats such as prefilled pens and automated insulin delivery systems.

U.S. Insulin Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 10.06 billion in 2026, accounting for roughly 33.5% of global market.

Europe

Europe market is anticipated to grow at 3.22% CAGR during the forecast period. Europe’s growth is driven by strong public reimbursement systems, high treatment adherence, and continued use of long-acting and rapid-acting insulin analogs. The region also has increasing biosimilar insulin adoption due to payer focus on cost containment and sustainable diabetes care budgets.

U.K. Insulin Market

The U.K. market in 2026 is estimated at around USD 1.71 billion, representing roughly 5.7% of global revenues.

Germany Insulin Market

Germany market is projected to reach approximately USD 1.90 billion in 2026, equivalent to around 6.3% of global sales.

Asia Pacific

The Asia Pacific market is expected to reach a valuation of USD 7.28 billion by 2026, making it the third largest region in the global industry. Asia Pacific is expected to be one of the fastest-growing regions due to its very large diabetes population, rising diagnosis rates, improving healthcare access, and expanding use of insulin in type 2 diabetes. Growth is also supported by local insulin manufacturing, increasing biosimilar availability, public procurement, and gradual movement from human insulin toward analog insulin in urban and insured populations.

Japan Insulin Market

The Japan market in 2026 is estimated at around USD 1.10 billion, accounting for roughly 3.6% of global revenues.

China Insulin Market

China’s market is projected to reach revenues of around USD 2.41 million in 2026, representing roughly 8.0% of global sales.

India Insulin Market

The India market in 2026 is estimated at around USD 1.10 billion, accounting for roughly 3.7% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa and Latin America regions are likely to witness a slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 2.01 billion by 2026. Prominent factors such as increasing diabetes prevalence, expanding public-sector insulin access, and rising use of basal insulin in type 2 diabetes are boosting the market growth in these regions.

In the Middle East & Africa region, the GCC market is projected to reach approximately USD 0.73 billion by 2026, representing about 2.4% of worldwide revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Insulin Portfolios and Affordable Biosimilar Expansion to Support Players’ Market Position

The insulin market reflects a moderately consolidated competitive landscape, consisting of major companies such as Novo Nordisk, Eli Lilly and Company, Sanofi, and Biocon Limited among others. The considerable market presence of these companies is owing to their broad insulin portfolios across basal, rapid-acting, premixed, human insulin, biosimilar/follow-on insulin, and niche inhaled insulin products. Furthermore, these players are focusing on long-acting analog innovation, affordability programs, biosimilar launches, regional manufacturing, and pharmacy-led access models to strengthen their competitive position.

- For instance, in October 2025, Biocon Biologics and Civica expanded their partnership and launched a private-label insulin glargine product to broaden diabetes treatment options across the U.S.

Additional key contributors include Gan & Lee Pharmaceuticals, Wockhardt Limited, Mannkind Corporation, and others. Emphasis on new product expansion, lower-cost insulin products and tender-based supply are key strategies undertaken by these players.

LIST OF KEY INSULIN COMPANIES PROFILED

- Novo Nordisk (Denmark)

- Eli Lilly and Company (U.S.)

- Sanofi (France)

- Biocon Limited (India)

- Gan & Lee Pharmaceuticals (China)

- Wockhardt Limited (India)

- Julphar Diabetes (UAE)

- MannKind Corporation (U.S.)

- Tonghua Dongbao Pharmaceutical Co., Ltd. (China)

- The United Laboratories International Holdings Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- March 2026: United Laboratories announced that China’s NMPA approved Insulin Degludec Injection submitted by its subsidiary Zhuhai United Bio-Pharmaceutical.

- January 2026: MannKind announced that the U.S. FDA approved an updated Afrezza label, adding clearer starting-dose guidance for patients switching from subcutaneous mealtime insulin or insulin pump bolus therapy to inhaled insulin.

- November 2025: Gan & Lee announced that Ondibta, its China-developed insulin glargine product, received a positive CHMP opinion.

- July 2025: Adocia announced that partner Tonghua Dongbao released positive topline Phase 3 results for BioChaperone Lispro (THDB0206) in adults with type 2 diabetes.

- April 2025: Fiocruz, Biomm, and Gan & Lee aligned guidelines for Brazil’s national production of insulin glargine through a Productive Development Partnership, aiming to reduce foreign dependence and expand local insulin supply.

REPORT COVERAGE

The insulin market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, pipeline analysis, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market outlook report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.13% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Product Type, Drug Type, Disease Type, Age Group, Route of Administration, Distribution Channel, and Region |

| By Type |

|

| By Product Type |

|

| By Drug Type |

|

| By Disease Type |

|

| By Age Group |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 28.91 billion in 2025 and is projected to reach USD 41.51 billion by 2034.

In 2025, North America’s market value stood at USD 10.59 billion.

The market is expected to exhibit a CAGR of 4.13% during the forecast period of 2026-2034.

By product type, the long-acting & ultra-long-acting insulin segment is expected to lead the market.

Increasing prevalence of diabetes and advancements in insulin delivery devices are primarily driving market expansion.

Novo Nordisk, Eli Lilly and Company, Sanofi, and Biocon Limited are some of the prominent players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 224

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us