Intermodal Freight Transportation Market Size, Share & Industry Analysis, By Type (Rail Road Intermodal, Road Sea Intermodal, Rail Sea Intermodal, Air Road Intermodal, Air Sea Intermodal, and Multimodal (3+ modes combined)), By Solution Type (Fleet Management, Intermodal Terminals, Transportation & Warehousing Services, Freight Routing & Scheduling, and Others), By Operation (Domestic Intermodal and International Intermodal), By End User (Automotive & Mobility, Food & Beverage, Healthcare, Energy & Utilities, Construction & Infrastructure, and Others), and Regional Forecast, 2026-2034

INTERMODAL FREIGHT TRANSPORTATION MARKET SIZE AND FUTURE OUTLOOK

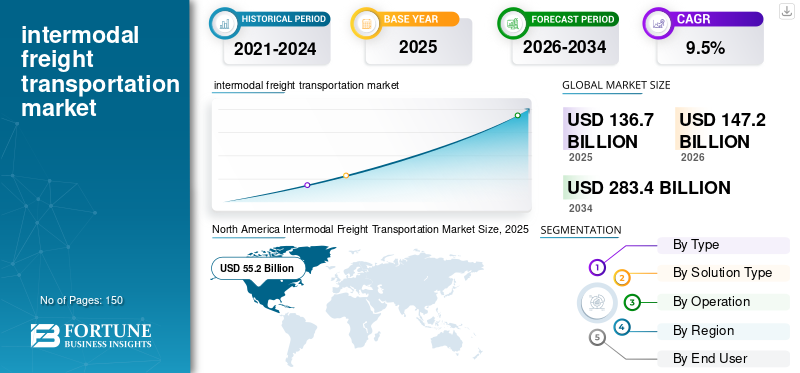

The global intermodal freight transportation market size was valued at USD 136.7 billion in 2025. The market is projected to grow from USD 147.2 billion in 2026 to USD 283.4 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period. North America dominated the global intermodal freight transportation market with a market share of 40.38% in 2025.

Intermodal freight transportation refers to the multiple modes of transportation, movement of goods using two or more modes of transport, typically road, rail, sea, and sometimes air, within a single, continuous shipping journey without handling the freight itself when modes are changed. Containers, trailers, and standardized loading units allow cargo to be efficiently transferred between trucks, trains, and ships, reducing manual handling, transit time, and risk of damage. This approach improves logistical efficiency, lowers costs, and increases demand for efficient supply chain reliability, making it the backbone of global trade flows.

There is a surge in the market due to several structural factors such as global trade expansion, nearshoring or reshoring activities, and increasing adoption of containerization across industries. Shippers are prioritizing cost-efficiency, sustainability, and reduced carbon emissions, areas where intermodal transport outperforms long-haul trucking due to lower fuel consumption per ton-mile and operational resilience. Congestion at ports and highways has also pushed companies toward rail truck combinations to diversify inland transport options. Additionally, digitalization, automated terminals, IoT-enabled tracking, and improved rail transportation infrastructure investments in the U.S., Europe, and Asia Pacific are making intermodal networks faster, more predictable, and more integrated, further accelerating market uptake.

Global shipping lines such as Maersk, CMA CGM, and COSCO, large rail operators such as Deutsche Bahn in Europe and Union Pacific and BNSF in the U.S., and integrated logistics providers such as FedEx, UPS, Kuehne + Nagel, and XPO Logistics. These companies dominate the market as they control extensive transportation assets ships, rail networks, trucking fleets, intermodal terminals, and container infrastructure, allowing them to offer seamless, end-to-end multimodal shipping solutions.

Download Free sample to learn more about this report.

INTERMODAL FREIGHT TRANSPORTATION MARKET TRENDS

Rapid Integration of Digital Technologies and Emphasis on Green Logistics to Amplify Market Growth

Technologies, including real-time tracking, IoT-enabled containers, AI-powered route optimization, and automated intermodal terminals, which together enhance visibility and improve cargo flow through enhancing operational efficiency. Another key development is the growing emphasis on green logistics, with shippers shifting freight from long-haul trucking to rail to reduce emissions, while operators invest in electric trucks, hybrid locomotives, and lower-carbon fuels. The market is also influenced by supply chain diversification and nearshoring, as companies move production closer to consumption markets, especially toward Mexico and Southeast Asia, thereby boosting demand for flexible cross-border and inland intermodal services.

Additionally, capacity expansion projects at ports, inland terminals, and rail corridors are strengthening intermodal connectivity and reducing congestion. Finally, the rise of e-commerce-driven freight, requiring fast and reliable multimodal networks, continues to increase demand for domestic intermodal solutions in the U.S., Europe, and Asia Pacific. Collectively, these modes of the intermodal freight transportation market trends highlight the shift toward smarter, greener, and more resilient intermodal logistics networks.

MARKET DYNAMICS

Market Drivers

Growing Need for Cost-Efficient and Sustainable Logistics Solutions to Drive Market

The surging need for cost-effective, sustainable, and efficient logistics solutions is driving the intermodal freight transportation market growth. As global supply chains become more complex and fuel prices continue to rise, companies are under pressure to lower transportation costs while maintaining reliability. Intermodal transport, especially rail combined with trucking, offers a more economical alternative to long-distance road freight as rail moves large volumes of cargo with significantly lower fuel consumption per ton mile. At the same time, businesses and governments are prioritizing sustainability, pushing shippers to reduce transit times, reduce carbon emissions, and comply with stricter environmental regulations. Rail-based intermodal transport can cut emissions by 60 to 75% compared to trucks alone, aligning with corporate ESG goals and national climate policies. This dual advantage of lower cost and lower environmental impact makes intermodal solutions increasingly attractive to manufacturers, retailers, and logistics providers seeking to build greener, more efficient supply chains.

According to the U.S. Department of Transportation (USDOT), rail is 3 to 4 times more fuel-efficient than trucking on a ton-mile basis, allowing one gallon of fuel to move one ton of freight over 470 miles a far lower operating cost for long-distance transport. From a sustainability perspective, the U.S. Environmental Protection Agency (EPA) reports that freight rail produces up to 75% fewer greenhouse gas emissions per ton-mile compared to road freight. These reductions are increasingly important as companies face rising fuel costs and stricter emission regulations.

Market Restraints

Infrastructure Limitation and Congestion at Ports, Rail Hubs, and Intermodal Terminals to Restrain Market Growth

Many facilities operate at or near maximum capacity, resulting in delays, longer dwell times, and reduced reliability for shippers. Aging rail lines, limited double-stack routes, and insufficient terminal automation further restrict the smooth movement of containers. In the U.S., for example, port congestion during peak seasons often leads to bottlenecks that cascade into rail networks, while shortages of drayage trucks and labor slow cargo transfers. These constraints reduce the efficiency of intermodal logistics operations and discourage some businesses from fully adopting multimodal logistics despite its cost and sustainability benefits.

Market Opportunities

Acceleration of Nearshoring and Supply Chain Diversification to Provide Ample Opportunities for the Intermodal Freight Transportation Market

As companies reconsider global sourcing strategies in response to trade tensions, rising manufacturing costs in China, and the need for more resilient supply chains, many are shifting production closer to end markets, particularly toward Mexico, Southeast Asia, and India. This geographic rebalancing increases demand for flexible, multimodal logistics networks capable of connecting new manufacturing hubs with major consumption regions.

In North America, for example, nearshoring to Mexico is driving higher volumes through cross-border rail and truck-rail intermodal corridors, especially via gateways such as Laredo and El Paso. At the same time, diversified sourcing across Asia is expanding ocean-rail intermodal flows into Europe and the U.S. As supply chains become more regionalized and multipolar, intermodal transport emerges as a critical enabler of efficiency, resilience, and cost optimization.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Road Sea Intermodal Segment to Lead Due to its Cost-efficiency

Based on type, the market is segmented into rail road intermodal, road sea intermodal, rail sea intermodal, air road intermodal, air sea intermodal, and multimodal (3+ modes combined).

The road sea intermodal segment is anticipated to dominate the market as it provides the most flexible and cost-effective solution for long-distance international freight combined with last-mile delivery. Ocean shipping remains the backbone of global trade, handling over the majority of worldwide merchandise volume. When paired with road transport, it enables seamless movement of containers from major ports to inland destinations. This combination offers unmatched scalability for high-volume cargo, competitive shipping rates, and broad accessibility through established port and highway networks. As global e-commerce, manufacturing, and consumer demand continue to rise, shippers increasingly rely on sea transport for cost efficiency and road transport for speed and reach.

The rail road intermodal segment is the fastest-growing segment in the market, driven by its strong balance of cost efficiency, environmental benefits, and inland connectivity. As shippers look for alternatives to long-haul trucking, which is increasingly affected by rising fuel costs, driver shortages, and capacity constraints, rail emerges as a more economical and sustainable solution for moving large volumes of freight over long distances.

By Solution Type

Transportation and Warehousing Services Lead Market Due to Their Central Role in Every Intermodal Freight Movement

Based on the solution type, the market is segmented into fleet management, intermodal terminals, transportation & warehousing services, freight routing & scheduling, and others.

Transportation & warehousing services hold the largest market share, primarily as they form the core operational layer of intermodal logistics. This segment includes container handling, storage, drayage, long-haul movement, cross-docking, and value-added warehousing. Since every intermodal shipment, regardless of mode, passes through transportation and warehousing processes, this segment naturally captures the highest revenue. The continuous rise of global trade, e-commerce growth, and increasing demand for integrated logistics services reinforces its dominance.

In contrast, fleet management is the fastest-growing segment, driven by rapid digitalization, increasing emphasis on operational efficiency, and the need for real-time visibility across multimodal assets. Technologies such as IoT-enabled tracking, predictive maintenance, telematics, and automated fleet scheduling are transforming how logistics companies manage trucks, railcars, containers, and chassis. As intermodal networks become more complex and shippers demand higher transparency and reliability, the adoption of advanced fleet management solutions is accelerating at a faster pace than traditional service-based segments.

By Operation

International Intermodal Dominance Driven by High-Volume, Long-Distance Freight Demand

By operation, the market is bifurcated into domestic intermodal and international intermodal.

International intermodal holds the largest market share as it supports the vast majority of global trade flows, connecting major manufacturing hub groups with consumption markets through integrated sea, rail road networks. The global merchandise trade moves by ocean, international intermodal is essential for transporting containers from ports to inland destinations across continents. Its large-scale infrastructure, including global shipping alliances, port terminals, cross-border rail corridors, and customs-integrated logistics systems, enables efficient long-distance movement of goods. The rapid expansion of export-driven economies in Asia, strong transpacific and Asia-Europe trade lanes, and increasing reliance on containerized freight further reinforce the dominance of international intermodal operations.

In contrast, domestic intermodal is the fastest-growing segment due to rising e-commerce demand, growing regional manufacturing, and ongoing investments in inland rail and terminal infrastructure. Countries such as the U.S., Canada, China, and European nations are increasingly shifting from long-haul trucking to rail road intermodal solutions to reduce costs, cut emissions, and overcome driver shortages. Domestic supply chains, especially in retail, FMCG, and automotive sectors, depend heavily on reliable inland logistics, and intermodal transport offers a scalable, fuel-efficient alternative. As companies prioritize nearshoring and regional distribution, domestic intermodal volumes are accelerating rapidly, making it the fastest-expanding component of the intermodal freight transportation market.

To know how our report can help streamline your business, Speak to Analyst

By End User

Food and Beverage Segment Dominates Market Due to Rising Need for Time-sensitive Transportation of Essential Goods

Based on end user, the market is categorized into automotive & mobility, food & beverage, healthcare, energy & utilities, construction & infrastructure, and others.

The food & beverage segment holds the largest market share, mainly as this sector requires constant, high-volume, and time-sensitive transportation to move perishable goods, packaged foods, beverages, and agricultural products across regions. The rising demand for refrigerated containers, expanding supermarket supply chains, and continuous restocking cycles make intermodal transport, especially sea road and rail road a cost-efficient and reliable solution. Its year-round shipment volumes and essential nature of goods ensure a consistently dominant share.

Meanwhile, automotive & mobility is the fastest-growing segment, driven by global production shifts, complex supply chains, and the industry’s increasing reliance on multimodal logistics for transporting vehicles, components, batteries, and EV-related materials. The growth of electric vehicle manufacturing, nearshoring of automotive production to Mexico and Eastern Europe, and the need for precise, just-in-time delivery are significantly boosting intermodal demand. Automotive supply chains benefit from intermodal’s efficiency, cost savings, and ability to handle high-volume, long-distance shipments, making it the fastest-growing end-use segment.

INTERMODAL FREIGHT TRANSPORTATION MARKET REGIONAL OUTLOOK

The market is analyzed across North America, Asia Pacific, Europe, and the Rest of the World.

North America

North America dominates the intermodal freight transportation market share due to its highly developed rail and road infrastructure, extensive network of intermodal terminals, and strong adoption of double-stack rail operations. The U.S. and Canada benefit from mature logistics ecosystems supported by major Class I railroads, advanced port facilities, and a high penetration of intermodal services across retail, automotive, FMCG, and e-commerce sectors. Cross-border trade under USMCA further boosts intermodal volumes, especially on key routes connecting the U.S., Canada, and Mexico. The region’s continuous investments in rail modernization, digital tracking systems, and sustainable freight initiatives solidify its position as the global leader.

North America Intermodal Freight Transportation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Moreover, the U.S. holds a dominant position in the intermodal freight transportation market due to its exceptionally advanced and expansive logistics infrastructure. The country has one of the most extensive rail networks in the world, operated by major Class I railroads such as BNSF, Union Pacific, CSX, and Norfolk Southern, which provide efficient long-distance, double-stack rail services crucial for intermodal growth.

Asia Pacific

Asia Pacific is anticipated to be the fastest-growing region, driven by rapid industrialization, expanding manufacturing bases, and increasing cross-border trade. Asian countries are witnessing major growth in containerized shipments and multimodal logistics development. The Belt and Road Initiative (BRI) is significantly enhancing rail connectivity between Asia and Europe, promoting long-distance intermodal transport. Rising exports, fast-growing e-commerce markets, and large-scale investments in ports, inland terminals, and smart logistics systems are accelerating intermodal adoption across the region. As supply chains diversify away from China, emerging economies in ASEAN are further boosting regional intermodal demand.

Europe

Europe holds a strong and steadily growing share due to its mature rail networks, stringent environmental regulations, and emphasis on shifting freight from road to rail to reduce carbon emissions. Countries such as Germany, France, the Netherlands, and Italy lead in intermodal integration, with well-established inland waterways, efficient cross-border rail corridors, and automated port operations. The EU’s Green Deal and investments in Trans-European Transport Network (TEN-T) corridors are further promoting modal shift, enhancing intermodal reliability and capacity. Europe’s harmonized logistics standards make it one of the most advanced intermodal markets globally.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and African countries, is experiencing gradual growth as countries begin investing in port expansions, rail upgrades, and multimodal logistics hubs. Latin America is strengthening intermodal connectivity to support agricultural exports and manufacturing supply chains. The Middle East is emerging as a strategic logistics gateway with major projects in UAE, Saudi Arabia, and Qatar, enhancing sea–road–rail integration. In Africa, growing trade corridors and international funding for rail modernization are slowly improving intermodal capacity. While still developing, the Rest of World region holds significant long-term potential as infrastructure and trade networks continue to expand.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Companies Focus on Integrating End-to-End Logistics Capabilities to Maintain Their Dominance

The intermodal freight transportation market is moderately fragmented, with a mix of global shipping lines, rail operators, logistics companies, and regional service providers competing across various segments. The market is structured around a few large, integrated key players that operate extensive multimodal networks, alongside numerous regional carriers and terminal operators that serve specific corridors.

Maersk stands out as one of the top market leaders, primarily due to its fully integrated end-to-end logistics capabilities. As one of the world’s largest container shipping companies, Maersk has expanded far beyond ocean freight into inland transportation, digital logistics, warehousing, and intermodal rail road services. Its vast global container fleet, ownership of major port terminals through APM Terminals, and strategic investments in supply chain technologies enable seamless connectivity from factory to destination. By offering comprehensive door-to-door intermodal solutions, Maersk leverages scale, efficiency, and digital visibility to maintain a strong leadership position in the global intermodal freight transportation market.

List of Key Intermodal Freight Transportation Companies Profiled

- A.P. Moller-Maersk (Denmark)

- CMA CGM Group (France)

- MSC (Mediterranean Shipping Company) (Switzerland)

- COSCO Shipping Lines (China)

- Deutsche Bahn (DB Cargo & DB Schenker) (Germany)

- Union Pacific Railroad (UP) (U.S.)

- BNSF Railway (U.S.)

- Kuehne + Nagel (Switzerland)

- UPS Supply Chain Solutions (U.S.)

- XPO Logistics (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, European property developer Verdion unveiled plans for a USD 1.17 billion intermodal freight hub in Denmark. The project, named iPort Zealand, will be developed on 250 hectares of privately owned land in Ringsted, located 60 km west of Copenhagen. The hub aims to leverage the upcoming Fehmarnbelt Tunnel, which will connect Denmark and Germany and significantly enhance regional freight connectivity.

- In November 2025, Schneider National, Inc., a leading multimodal transportation, intermodal, and logistics provider, unveiled Schneider Fast Track, a premium service tailored for shippers requiring fast, time-sensitive, and high-priority freight solutions.

- In September 2025, CLIP Intermodal expanded its partnership with Amazon, introducing new intermodal services connecting its Swarzędz terminal in Poland with the Setemar Can Tunis terminal in Barcelona, Spain.

- In September 2025, Ocean Network Express (ONE) announced the launch of a new reefer intermodal rail service connecting Hyderabad to Nhava Sheva, aimed at strengthening cold chain logistics and improving temperature-controlled cargo movement.

- In February 2025, Ocean Network Express (ONE) and LX Pantos officially completed their joint venture, launching Boxlinks LLC. The partnership combines the strengths of both companies to offer end-to-end domestic intermodal transportation services in the U.S., utilizing their established rail and trucking networks to ensure efficient and timely cargo delivery.

REPORT COVERAGE

The market report provides a detailed analysis and focuses on key aspects, such as leading market players, vehicle type, and leading applications of the product. Besides, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

|

|

By Solution Type

|

|

|

By Operation

|

|

|

By End User

|

|

| By Region |

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 136.7 billion in 2025 and is expected to reach USD 283.4 billion by 2034.

The market is set to register a CAGR of 9.5% during the forecast period of 2026-2034.

The transportation & warehousing services segment leads the market.

The market size in North America stood at USD 55.2 billion in 2025.

A.P. Moller-Maersk, CMA CGM Group, MSC (Mediterranean Shipping Company), COSCO Shipping Lines, and Deutsche Bahn (DB Cargo & DB Schenker) are some of the top players in the market.

The U.S. dominated the market in terms of revenue in 2025.

North America held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us