Investment Casting Market Size, Share & Industry Analysis, By Process Type (Silica Sol Investment Casting and Sodium Silicate Investment Casting), By Material Type (Carbon Steel, Alloy Steel, Stainless Steel, Aluminum Alloys, Titanium Alloys, Superalloys, and Other Metals & Alloys), By End Use (Aerospace & Defense, Automotive, Industrial Machinery, Medical Devices, Energy & Power, Oil & Gas, and Others (Marine, Construction Equipment, and Agriculture)), and Regional Forecast, 2026 - 2034

Investment Casting Market Size and Future Outlook

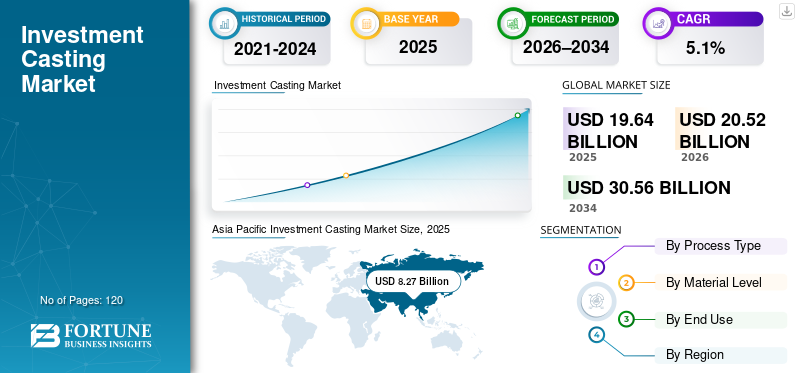

The global investment casting market size was valued at USD 19.64 billion in 2025. The market is projected to grow from USD 20.52 billion in 2026 to USD 30.56 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period. Asia Pacific dominated the investment casting market with a market share of 42.11% in 2025.

Investment casting is a precision metal manufacturing process in which molten metal is poured into a ceramic mold formed around a disposable wax pattern to produce complex, high-accuracy components with excellent surface finish, and it is experiencing steady, structurally driven growth as growing demand for high-precision metal components expands across aerospace & defense, industrial machinery, automotive, and energy end-use industries. The investment casting industry is increasingly adopting advanced casting technologies to achieve superior dimensional accuracy, complex geometries, and high-performance surface finishes while minimizing post-machining and material waste. Rising demand for corrosion-resistant, lightweight, and high-performance components is accelerating adoption of the investment casting process, particularly for turbine blades and other critical parts used in fuel-efficient aerospace engines, power generation systems, and medical devices. Ongoing technological advancements, including process optimization and selective use of 3D printing in tooling and pattern development, are further enhancing production efficiency and reducing lead times across the global market.

- For instance, during recent aerospace supply chain ramp-ups, leading investment casting suppliers such as Precision Castparts Corp., Doncasters Group, and Hitchiner Manufacturing expanded capacity and introduced advanced silica sol casting processes for turbine blades and structural components, reflecting OEM demand for higher throughput, metallurgical consistency, and qualification-ready investment casting solutions.

Precision Castparts Corp. (PCC), Impro Precision Industries Ltd., CIREX Group, and MetalTek International are among the key players holding a significant share of the investment casting market. Their competitive positioning is supported by broad portfolios spanning silica sol and sodium silicate casting, advanced alloy processing, in-house tooling, heat treatment, and precision finishing, along with the ability to deliver fully qualified, end-to-end casting solutions for aerospace, industrial, and energy applications.

Download Free sample to learn more about this report.

INVESTMENT CASTING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 19.64 Billion

- 2026 Market Size: USD 20.52 Billion

- 2034 Forecast Market Size: USD 30.56 Billion

- CAGR: 5.1% from 2026–2034

- Asia Pacific dominated the investment casting market with a 42.11% share in 2025.

- Silica sol investment casting held the largest market share among process types.

- Alloy steel accounted for the largest share of the market by material type.

Asia Pacific

Asia Pacific generated USD 8.27 billion in 2025, making it the largest and fastest-growing regional market.

North America

North America accounted for USD 5.17 billion in 2025, supported by strong aerospace, automotive, and industrial manufacturing demand.

Europe

Europe remains a key market, with Germany projected to reach USD 1.20 billion and the U.K. USD 0.72 billion by 2026.

U.S.

The investment casting market is projected to reach USD 4.37 billion by 2026.

Japan

The investment casting market is projected to reach USD 1.03 billion by 2026.

Read More

INVESTMENT CASTING MARKET TRENDS

Rising OEM Emphasis on Qualified Capacity and Multi-Alloy Flexibility is Reshaping Investment Casting Supplier Strategies

Investment casting demand is increasingly shaped by OEM requirements for qualified capacity, multi-alloy production flexibility, and shorter qualification lead times, particularly across aerospace, energy, and defense programs with longer production cycles. Rather than prioritizing pure volume expansion, leading foundries within the investment casting industry are investing in metallurgical flexibility, advanced shell systems, and alloy-specific process control to support frequent program changes and parallel production of stainless steels, superalloys, and titanium components, while maintaining high dimensional accuracy and consistent quality across the investment casting process.

- For instance, during recent aerospace engine program ramps, multiple Tier-1 investment casting suppliers expanded alloy-specific melting and shell qualification capabilities to support simultaneous production of nickel-based superalloys and titanium components under tightened OEM certification timelines.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Surge in Aerospace & Defense Casting Activity to Drive Market Growth

The market is experiencing accelerated investment casting market growth within aerospace & defense driving suppliers to expand capacity and invest in advanced metallurgy and digital foundry technologies. Production across aerospace castings rose sharply in 2024 with notable gains in turbine, engine, and structural components, prompting leading foundries to prioritize capacity additions and process upgrades to meet stringent OEM qualification cycles and escalating order backlogs. This trend reflects broader aerospace production momentum, where defense spending increases and commercial fleet renewals are boosting growing demand for high-precision, high-performance superalloy and high-temperature investment cast parts.

- For instance, Precision Castparts Corp. (PCC) and Doncasters Group have publicly indicated increased capital allocation toward aerospace-focused investment casting operations, including expanded turbine airfoil capacity and process upgrades, to support higher engine build rates and long-cycle defense programs across North America and Europe.

MARKET RESTRAINTS

Alloy-Specific Process Variability and Scrap Risk Limiting Standardization of Advanced Investment Casting Lines

Unlike high-volume metal forming processes, investment casting is highly sensitive to alloy chemistry, thermal behavior, and solidification dynamics, which limits the standardization of fully automated, high-throughput casting lines. Variations in superalloy composition, titanium reactivity, and ceramic shell behavior often require alloy-specific shell systems, melt controls, and post-cast handling, increasing scrap risk, and rework rates. For suppliers serving aerospace and energy OEMs, where yield losses directly impact program economics, this variability can delay the deployment of standardized automation and constrain rapid capacity scaling despite strong end-market demand.

MARKET OPPORTUNITIES

Defense Localization and ITAR-Driven Sourcing Creating New Demand for Certified Investment Casting Capacity

An emerging opportunity in the market is being created by defense localization policies and stricter ITAR and export-control requirements, which are reshaping supplier selection for military aerospace, naval, and land systems. Defense OEMs are increasingly prioritizing regionally certified investment casting suppliers with controlled melting, traceable material systems, and in-country production capabilities to reduce geopolitical and supply-chain risk. This shift is expanding demand for investment casting suppliers that can meet defense qualification standards, support low-to-medium volume programs, and deliver long lifecycle support for mission-critical components.

- For instance, Hitchiner Manufacturing and Zollern GmbH have expanded defense-qualified investment casting capabilities for aerospace and military programs, supporting turbine, structural, and high-temperature alloy components under tightened defense sourcing and certification requirements in North America and Europe.

MARKET CHALLENGES

Fragmented Aerospace, Defense, and Industrial Certification Requirements Increasing Process Customization and Qualification Burden

Investment casting suppliers face significant challenges arising from fragmented certification, qualification, and export compliance requirements across aerospace, defense, energy, and industrial end markets. Cast components often must be produced under program-specific standards such as NADCAP, AS9100, ITAR, customer-specific engine specifications, and regional defense regulations, requiring tailored process routes, documentation, and inspection protocols. This lack of harmonization limits standardization of casting processes, increases qualification lead times, and raises operating costs. For suppliers serving multiple OEMs and regions, frequent requalification and audit cycles can constrain capacity flexibility and discourage rapid deployment of new alloys or production technologies.

Segmentation Analysis

By Process Type

Silica Sol Investment Casting Segment Led as it is a Precision and Performance Backbone of High-Value End-Use Applications

By process type, the market is bifurcated into silica sol investment casting and sodium silicate investment casting.

Silica sol investment casting held the largest investment casting market share as it forms the technical backbone of high-precision and performance-critical applications within the market, particularly across aerospace & defense, medical devices, and advanced energy equipment. This process enables superior surface finish, tighter dimensional tolerances, and improved metallurgical integrity, making it essential for turbine blades, structural airframe components, and complex thin-wall geometries. As OEMs increasingly demand reduced post-machining, higher material efficiency, and consistent repeatability, silica sol casting is becoming a strategic priority for suppliers serving export-oriented and qualification-intensive programs where even marginal quality improvements translate into significant lifecycle and cost advantages.

- For instance, in 2024, Hitchiner Manufacturing highlighted continued investment in silica sol–based casting capabilities to support aerospace and defense programs requiring tight tolerance control and repeatable quality across long production cycles.

Sodium silicate investment casting plays a critical role in supporting cost-optimized, high-volume production across automotive, industrial machinery, energy, and general engineering applications and is growing at a CAGR of 5.0% over the forecast period. While offering lower tooling and processing costs compared to silica sol systems, sodium silicate casting remains well suited for larger components and less tolerance-sensitive geometries where economic efficiency is a primary consideration. The process continues to see strong adoption in emerging markets and decentralized manufacturing hubs, where foundries prioritize throughput, material flexibility, and competitive pricing to serve domestic and export industrial demand without the complexity of aerospace-grade qualification requirements.

To know how our report can help streamline your business, Speak to Analyst

By Material Type

Compatibility with High-Volume Production Requirements Led to Alloy Steel Segmental Dominance

By material type, the market is segmented into carbon steel, alloy steel, stainless steel, aluminum alloys, titanium alloys, superalloys, and other metals & alloys.

Alloy steel held the largest share of the investment casting market, driven by its widespread use across automotive, industrial machinery, energy, and general engineering applications. Alloy steels offer an optimal balance of strength, toughness, wear resistance, and cost efficiency, making them well suited for load-bearing components, power transmission parts, valves, pumps, and structural assemblies. Their broad applicability, ease of processing through both silica sol and sodium silicate investment casting routes, and compatibility with high-volume production requirements continue to reinforce alloy steel’s dominance in overall market consumption.

Titanium alloys are expected to register the highest growth rate in the investment casting market, expanding at a CAGR of 5.8% during the projected period, supported by rising adoption across aerospace & defense, medical devices, and advanced energy applications. Titanium investment castings offer an exceptional strength-to-weight ratio, corrosion resistance, and high-temperature performance, making them critical for aircraft structures, engine components, and implantable medical devices. Increasing focus on lightweighting, fuel efficiency, and lifecycle performance is driving OEMs to substitute traditional steel components with titanium alloys, particularly in qualification-intensive and export-oriented programs, accelerating capacity expansion and process investments among specialized investment casting suppliers.

By End Use

Extensive Use of Complex Thin-Wall Geometries Led to Aerospace & Defense Segmental Dominance

Based on end use, the market is segmented into aerospace & defense, automotive, industrial machinery, medical devices, energy & power, oil & gas, and others (marine, construction equipment, agriculture).

Aerospace & defense account for a highest share of market value despite lower production volumes, driven by the extensive use of superalloys, titanium, and complex thin-wall geometries in aircraft engines, airframes, and defense platforms. Aerospace investment casting programs are characterized by long qualification cycles, stringent certification requirements, and multi-year production runs, making suppliers’ metallurgical expertise, process repeatability, and quality assurance capabilities critical differentiators.

The energy & power segment is expected to register the highest growth rate in the investment casting market, expanding at a CAGR of 6.1% over the forecast period, supported by rising investments in power generation, renewable energy infrastructure, and gas turbine installations. Investment cast components are increasingly used in turbines, flow-control systems, and high-temperature equipment where corrosion resistance, thermal stability, and complex geometries are required. Growing demand for efficient power generation, grid modernization, and cleaner energy systems is accelerating adoption of high-performance investment castings, particularly in gas-fired, nuclear, and renewable energy projects, driving capacity expansion among casting suppliers focused on energy applications.

Automotive represents a major volume-driven end use for investment casting, supported by demand for precision components in powertrain systems, turbochargers, braking assemblies, and increasingly in electric vehicle platforms. Automotive investment casting is typically focused on cost efficiency, dimensional consistency, and scalability, with alloy steel, stainless steel, and aluminum alloys dominating material usage. High production volumes and platform standardization encourage continuous process optimization, particularly in sodium silicate and hybrid casting routes, to balance cost and performance requirements.

Others end use segment, including marine, construction equipment, and agricultural machinery, are characterized by region-specific demand and selective adoption of investment casting for durability-focused components.

Investment Casting Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Investment Casting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for over USD 5.17 billion revenue generated in 2025, supported by a highly developed aerospace, automotive, industrial machinery, and energy manufacturing base. Strong demand from aerospace & defense programs, coupled with sustained automotive and industrial equipment production, continues to underpin regional market strength. Tight labor availability, stringent certification requirements, and OEM quality standards are accelerating investments in process automation, advanced shell systems, and metallurgical controls. Ongoing capacity expansion, defense modernization programs, and long-cycle aerospace engine backlogs are driving steady demand for high-precision investment cast components across the U.S., Canada, and Mexico.

U.S. Investment Casting Market

U.S. to dominate the North American market with an estimated revenue of about USD 4.37 billion in 2026, supported by its large-scale, highly advanced aerospace, defense, automotive, and industrial manufacturing base. Strong demand from aircraft engines, defense platforms, industrial machinery, and energy systems continues to drive sustained consumption of high-precision investment cast components. The presence of globally qualified casting suppliers, deep OEM–supplier integration, and advanced metallurgical infrastructure supports continuous investment in silica sol casting, superalloy processing, heat treatment, and precision finishing capabilities.

Europe

The European market is supported by a highly developed and regulation-driven manufacturing base, particularly across aerospace, automotive, industrial machinery, and energy end uses. Strong demand from aircraft engine OEMs, automotive manufacturers, and industrial equipment producers, coupled with stringent quality, environmental, and certification standards, is driving continuous investment in advanced casting processes, energy-efficient melting systems, and precision finishing capabilities. Countries such as Germany, France, Italy, Spain, and the Netherlands lead adoption, supported by strong industrial clusters, skilled labor availability, and export-oriented production. Ongoing modernization of legacy foundries, increasing focus on sustainability compliance, and expansion of high-value precision casting applications continue to underpin steady market growth across Europe.

U.K. Investment Casting Market

The U.K. market in 2026 is estimated at around USD 0.72 billion, representing roughly 3.5% of global sales.

Germany Investment Casting Market

Germany’s market is projected to reach approximately USD 1.20 billion in 2026, equivalent to around 5.8% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing investment casting market, generating revenue of USD 8.27 billion in 2025 globally. Within the region, China and Japan are projected to reach approximately USD 4.05 billion and USD 1.03 billion, respectively by 2026. Market growth is driven by large-scale industrial manufacturing expansion, rising automotive and industrial machinery production, and increasing export-oriented casting activity. China, Japan, South Korea, and ASEAN countries are key contributors, supported by strong demand from automotive, industrial equipment, and energy end uses. The region is witnessing a structural shift from small-scale and manual foundry operations toward industrialized, higher-throughput, and quality-controlled investment casting facilities, particularly across China, India, and Southeast Asia.

China Investment Casting Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 4.05 billion, representing roughly 19.7% of global sales.

Japan Investment Casting Market

The Japan market in 2026 is estimated at around USD 1.03 billion, accounting for roughly 5.0% of the global sales.

India Investment Casting Market

The India market in 2026 is estimated at around USD 1.51 billion, accounting for roughly 7.4% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by energy infrastructure development, defense localization initiatives, and expanding industrial manufacturing activity, particularly across the GCC and North Africa. Government-backed investments in oil & gas, power generation, and industrial diversification are supporting demand for high-integrity cast components used in turbines, valves, pumps, and heavy equipment. The GCC benefits from high-capex, specification-driven projects requiring alloy and stainless-steel investment castings, while North Africa and Sub-Saharan Africa are witnessing gradual shifts from imported components toward localized and semi-industrialized casting supply. These dynamics continue to sustain demand for cost-optimized and performance-oriented investment casting across the region.

GCC Investment Casting Market

The GCC market is projected to reach around USD 0.48 billion in 2026, representing roughly 2.3% of the global sales.

South America

The South America market is supported by the region’s growing industrial manufacturing base, particularly in Brazil and Argentina, which serve as key hubs for automotive, industrial machinery, and energy-related production. Strong export demand for engineered components, coupled with compliance requirements for international quality and certification standards, is driving investments in controlled melting, shell-building, and precision finishing capabilities. While automation and process sophistication vary across the region, larger export-oriented foundries are increasingly modernizing facilities to improve yield consistency, dimensional accuracy, and cost efficiency.

Brazil Investment Casting Market

The Brazil market is projected to reach around USD 0.51 billion in 2026, representing roughly 2.5% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Qualification Depth, Alloy Breadth, and Program Longevity

The investment casting market is moderately consolidated, with competitive positioning shaped less by breadth of equipment portfolios and more by depth of metallurgical capability, qualification history, and long-term program participation. Leading players such as Precision Castparts Corp., Impro Precision Industries, CIREX Group, MetalTek International, and Hitchiner Manufacturing maintain strong market positions by supporting multiple alloys, complex geometries, and mission-critical applications across aerospace, defense, energy, and industrial end uses. Their competitive strength is reinforced by proprietary process knowledge, customer-specific qualification records, and the ability to sustain repeatable quality across long-cycle production programs.

Competitive differentiation is increasingly driven by a supplier’s ability to absorb program volatility, manage alloy-specific yield risk, and maintain parallel qualification pathways for multiple OEMs rather than by scale alone. As OEMs prioritize supply security and execution reliability, investment casting leaders are strengthening in-house testing, documentation control, and lifecycle support capabilities to protect incumbent positions and raise switching barriers for customers.

- For instance, Hitchiner Manufacturing and MetalTek International have continued to expand alloy-specific casting and testing capabilities to support long-duration aerospace and energy programs, reinforcing their role as qualified, high-reliability suppliers rather than volume-driven casting providers.

LIST OF KEY INVESTMENT CASTING COMPANIES PROFILED IN REPORT

- Precision Castparts Corp. (U.S.)

- Impro Precision Industries Ltd. (Hong Kong)

- CIREX Group (Turkey)

- MetalTek International (U.S.)

- Zollern GmbH & Co. KG (Germany)

- Milwaukee Precision Casting (U.S.)

- Dongying Giayoung Precision Metal Co., Ltd. (China)

- Proterial Metals, Ltd. (India)

- Doncasters Group (U.S.)

- Hitchiner Manufacturing (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Hitchiner Manufacturing opened a new 57,000-square-foot Shared Services Operations facility at its Elm Street Campus in Milford, NH, consolidating post-production capabilities and expanding its value stream for finished investment casting components to better support aerospace, automotive, and defense customers.

- July 2025: MetalTek International’s Wisconsin Investcast Division continued to advance its precision investment casting and additive manufacturing capabilities, producing large-scale castings (up to 2,000 lbs pour weight) and expanding alloy processing options for critical aerospace, energy, and industrial applications, supported by ISO 9001 and Nadcap certifications.

- March 2025: Impro Precision Industries reported increased aerospace and energy end-market revenue growth, with particular expansion in high-horsepower engine components and aerospace casting demand, as highlighted in its 2024 annual results and ongoing capacity investments in Mexico and China plants.

- April 2024: MetalTek’s Carondelet Division achieved certification to produce HY-80 steel castings, a high-strength, corrosion-resistant alloy widely used in naval defense applications, deepening its participation in high-compliance military and marine markets.

- January 2024: CIREX Group announced the expansion of its European investment casting operations with additional capacity for stainless steel and alloy steel castings, targeting increased demand from industrial machinery, energy, and precision engineering customers requiring high repeatability and export-grade quality.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Process Type, Material Type, End Use, and Region |

| By Process Type |

|

| By Material Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value is estimated at USD 20.52 billion in 2026 and is projected to reach USD 30.56 billion by 2034.

In 2025, the Asia Pacific’s market value stood at USD 8.27 billion.

The market is expected to exhibit a CAGR of 5.1% during the forecast period of 2026-2034.

By end use, the aerospace & defense is expected to lead the market.

Rising component complexity, tighter tolerance requirements, and increased automation across aerospace, energy, and industrial manufacturing are driving demand for high-precision investment castings.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us