IVD Quality Control Market Size, Share & Industry Analysis, By Product & Services (Quality Control Products {Serum/Plasma-Based Controls, Whole Blood-Based Controls, Urine-Based Controls, and Others}, Quality Control Data Management Solutions, and Quality Assurance Services), By Technology (Clinical Chemistry, Immunoassay, Molecular Diagnostics, Microbiology, Hematology, and Others), By End-user (Hospitals, Independent/Commercial Laboratories, Academic & Research Institutes, and Others), and Regional Forecast, 2026-2034

IVD Quality Control Market Size and Future Outlook

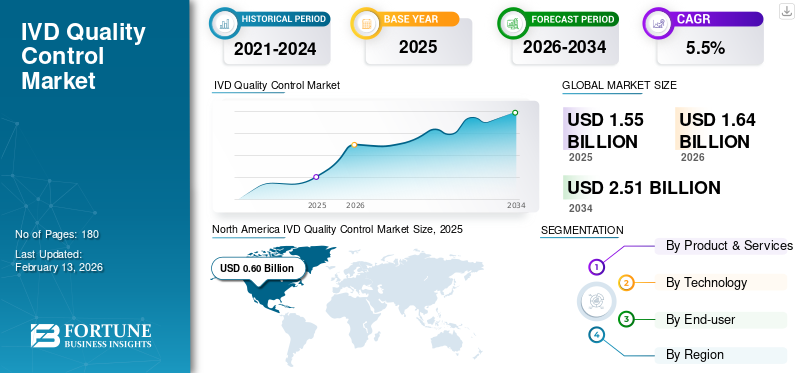

The global IVD quality control market size was valued at USD 1.55 billion in 2025. The market is projected to grow from USD 1.64 billion in 2026 to USD 2.51 billion by 2034, exhibiting a CAGR of 5.5% during the forecast period. North America dominated the global IVD quality control market with a market share of 38.71% in 2025.

IVD quality control includes the materials, software, and services used to verify that lab test systems are functioning correctly every day. It helps labs detect errors early and support compliance with accreditation and regulatory expectations. Market growth is attributed to labs running higher test volumes and using more automated analyzers. Moreover, the labs are seeking independent third-party controls to improve performance across instruments and sites.

Furthermore, Bio-Rad Laboratories, Inc., and Thermo Fisher Scientific, Inc., held the highest market share due to a diversified portfolio of control materials, data management solutions, and related QA/QC services.

Download Free sample to learn more about this report.

IVD Quality Control Market Key Takeaways

- 2025 Market Size: USD 1.55 billion

- 2026 Market Size: USD 1.64 billion

- 2034 Forecast Market Size: USD 2.51 billion

- CAGR: 5.5% from 2026–2034

- North America dominated the IVD quality control market with a 38.71% share in 2025.

- The quality control products segment accounted for the largest market share in 2025.

- The clinical chemistry segment is projected to hold a 37.80% share in 2026.

North America

North America generated USD 0.60 billion in 2025 and remained the leading regional market, driven by stringent regulatory requirements and high testing volumes.

Europe

Europe is expected to reach USD 0.39 billion by 2026, driven by the strong presence of key market players and advanced quality control adoption.

Asia Pacific

Asia Pacific is projected to reach USD 0.51 billion by 2026, supported by expanding laboratory networks and increasing QC standardization.

U.S.

The IVD quality control market is projected to reach USD 0.56 billion by 2026, supported by a large base of hospitals and independent laboratories.

Japan

The IVD quality control market is projected to generate USD 0.17 billion in revenue by 2026, driven by increasing adoption of advanced diagnostic testing and quality assurance practices.

Read More

IVD QUALITY CONTROL MARKET TRENDS

Shift Toward Connected QC and Peer Benchmarking to Emerge as a Key Trend

Currently, IVD quality control is moving toward connected technologies, such as “run controls and analysis in real time”. Labs are seeking faster root-cause analysis when quality control fails, particularly in high-throughput settings where repeat testing is expensive. The adoption of connected QC data platforms and peer comparison has enabled labs to detect issues instantly.

- For instance, in January 2025, Bio-Rad Laboratories, Inc.’s Unity Next Peer QC was a QC software platform focused on centralized reporting and peer access.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Regulatory Scrutiny and Standardization Needs to Fuel Market Expansion

In recent years, there has been increasing pressure on hospitals and labs to demonstrate high-quality control for every assay instrument and site. As these facilities consolidate and run multi-site networks, the demand for stricter quality control guidelines, tracking, and comparable performance reporting across locations is increasing significantly.

Additionally, there has been an increase in assay product launches, which is fueling demand for third-party controls, External Quality Assessment (EQA), and QC data management systems. Such a scenario is anticipated to drive the global IVD quality control market growth during the forecast period.

- For instance, in January 2021, LGC SeraCare launched AccuPlex SARS-CoV-2 in synthetic oral fluid, driving the demand for quality control for saliva and oral fluid diagnostics.

MARKET RESTRAINTS

Cost Sensitivity Among Smaller Labs and Workflow Burden to Restrict Market Growth

Despite the mandates, in QC, demand has been increasing, and smaller labs still try to control the cost per reportable result, thereby limiting QC frequency to the minimum allowed, especially in conditions of staffing shortages.

Moreover, the workflow burden caused by IT integration hurdles, manual QC practices, and slow upgrades is expected to limit the adoption of quality control solutions, hindering market growth.

MARKET OPPORTUNITIES

QC for Molecular/NGS Expansion and New Test Areas to Create Significant Growth Opportunities

In recent years, labs have expanded genetic testing, liquid biopsy workflows, and pharmacogenomics, driving the adoption of patient-like reference materials that cover multiple variants and are stable and reproducible. Additionally, the suppliers are actively launching new reference materials for specific panels.

Also, several players are expanding into newer biomarkers, which is creating growth opportunities for premium QC products and services.

- For instance, in August 2024, LGC Clinical Diagnostics launched Seraseq Carrier Screening DNA Mixa, a new reference material to support clinical laboratories in the validation, development, and routine assessment of NGS expanded carrier screening assays.

MARKET CHALLENGES

Variant Drift and Assay Complexity to Challenge Market Expansion

Currently, keeping QC materials relevant is quite challenging as assays change, especially in infectious disease and molecular testing, where targets evolve. Moreover, the vendors are responding with variant-focused panels. Still, continuous updating incurs high costs, posing a major challenge for material quality control.

Moreover, without strong informatics, harmonizing QC performance across instruments, sites, and reagent lots remains challenging, and labs are expected to face repeat testing and downtime due to quality control issues.

Segmentation Analysis

By Product & Services

Higher Routine Usage of Quality Control Materials Due to Increasing Testing Volume Boosts Segment Growth

Based on product & services, the market is segmented into quality control products, quality control data management solutions, and quality assurance services. The quality control products are further sub-segmented into serum/plasma-based controls, whole blood-based controls, urine-based controls, and others.

The quality control products segment accounted for the largest global IVD quality control market share in 2025. The liquid and lyophilized controls, calibrator verification materials, and molecular reference materials are routinely consumed in high volumes. They are required across essentially all labs and tests due to repeat purchases, driven by high testing volume, the number of analyzers, and the number of analytes per instrument. As a result, several companies are expanding the range of QC materials, which is anticipated to fuel the segment’s growth.

- For instance, in November 2022, Bio-Rad Laboratories, Inc. expanded its portfolio of independent quality controls, including InteliQ and Liquichek compact vials, for Abbott's Alinity ci-series clinical chemistry and immunoassay instruments.

Additionally, the quality control data management solutions segment is projected to grow at a CAGR of 6.8% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Higher Installed Base of Automated Analyzers to Drive Clinical Chemistry Segment’s Growth

By technology, the market is segmented into clinical chemistry, immunoassay, molecular diagnostics, microbiology, hematology, and others.

The clinical chemistry segment accounted for the largest market share in 2025. The segment’s growth is attributed to the high installed base of automated analyzers in hospitals and commercial labs, which is influencing labs to maintain multi-analyte QC across wide measurement ranges. Moreover, the segment is estimated to hold a 37.8% share in 2026.

Additionally, the immunoassay segment is anticipated to grow at a CAGR of 5.8% over the forecast period.

By End-user

Increasing Number of Hospitals Globally to Propel Segment’s Growth

On the basis of end-user, the market is segmented into hospitals, independent/commercial laboratories, academic & research institutes, and others.

In 2025, hospitals dominated the market as end-users. Hospitals operate at high test volumes across a wide range of assays, including clinical chemistry, immunoassays, hematology, coagulation, microbiology, and, increasingly, molecular diagnostics. This requires frequent QC runs, which are anticipated to drive the segment’s growth. Moreover, the increasing number of hospitals is expected to expand QC runs in the coming years. Furthermore, the segment is set to hold 53.9% share in 2026.

- For instance, the American Hospital Association (AHA) Fast Facts on Hospitals reported that there were 6,093 total U.S. hospitals as of early 2025.

In addition, the independent/commercial laboratories segment is projected to grow at a 5.6% CAGR over the forecast period.

IVD Quality Control Market Regional Outlook

Based on region, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America IVD Quality Control Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.57 billion, and is projected to grow to USD 0.60 billion by 2025. The growth is attributed to the large base of hospitals and independent/commercial laboratories that must comply with CLIA, CAP, and FDA requirements, which mandate routine internal QC.

- For instance, according to the Laboratory of Florida LLC., there are approximately 5,414 independent laboratories in the U.S. as of January 2026.

U.S. IVD Quality Control Market

In 2026, the U.S. is projected to reach USD 0.56 billion, accounting for approximately 34.1% of the global market.

Europe

Europe is projected to record a 5.5% growth rate during the projection period, the third-highest globally, reaching USD 0.39 billion by 2026. The growth is attributed to the significant presence of key players, which is driving higher penetration of higher-quality control products in the region.

U.K. IVD Quality Control Market

The U.K. market is anticipated to reach USD 0.07 billion by 2026, representing approximately 4.1% of global revenues.

Germany IVD Quality Control Market

Germany's market is estimated to reach a value of USD 0.11 billion by 2026, representing around 6.8% of global revenue.

Asia Pacific

By 2026, the Asia Pacific market value is projected to reach USD 0.51 billion, making it the second-largest market globally. The growth is attributed to increasing laboratory networks, standardization of QC guidelines, and key players entering the region with advanced portfolios.

Japan IVD Quality Control Market

Japan is projected to generate approximately USD 0.17 billion in revenue by 2026, representing nearly 10.6% of the global market.

China IVD Quality Control Market

China’s market is anticipated to reach around USD 0.18 billion by 2026, accounting for nearly 11.0% of global revenues.

India IVD Quality Control Market

India’s market is expected to reach approximately USD 0.06 billion by 2026, accounting for around 3.9% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are expected to showcase moderate growth, with the Latin America market predicted to reach USD 0.07 billion by 2026. Countries such as Brazil and Mexico are expanding private diagnostic networks and increasing the adoption of automated analyzers, which is expected to support growth in Latin America. Also, the government-led investments in hospitals, centralized laboratories, and healthcare quality programs are driving demand for standardized QC practices in the Middle East & Africa.

GCC IVD Quality Control Market

By 2026, the GCC market value is estimated to reach approximately USD 0.03 billion, representing around 3.2% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad QC Portfolios to Strengthen Market Position of Key Players

In 2025, Bio-Rad Laboratories, Inc. and Thermo Fisher Scientific, Inc. held the majority of the global market share. This share is attributed to their broad QC portfolios, global distribution networks, and long-standing relationships with hospitals and commercial laboratories.

Moreover, other prominent players are focusing on portfolio expansion through new product launches, especially in molecular diagnostics, and on strategic acquisitions to strengthen niche capabilities, which is expected to increase their market share in the coming years.

LIST OF KEY IVD QUALITY CONTROL COMPANIES PROFILED

- Thermo Fisher Scientific Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Abbott (U.S.)

- Siemens Healthcare GmbH (Germany)

- Randox Laboratories Ltd. (U.K.)

- Technopath Clinical Diagnostics (Ireland)

- LGC Limited (U.K.)

- QuidelOrtho Corporation (U.S.)

- Helena Laboratories (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Randox Laboratories Ltd. launched a new RIQAS EQA programme for pre-eclampsia testing, leading to the expansion of external quality assessment.

- October 2023: Technopath Clinical Diagnostics expanded availability of Multichem QC and IAMQC software in Australia.

- July 2023: LGC Group acquired Kova International, Inc., a manufacturer of in vitro urinalysis and toxicology quality control products for clinical laboratories to expand footprint in California and New York.

- August 2022: LGC Group extended its collaboration with Stanford Medicine to support genetic/metabolomic diagnostic testing.

- April 2021: LGC Group launched ACCURUN SARS-CoV-2 Antigen Reference Material Kit, a QC tool for antigen testing.

- January 2021: Antylia Scientific acquired ZeptoMetrix to strengthen the clinical diagnostics and QC portfolio.

REPORT COVERAGE

The report provides detailed analysis across all market segments, highlighting drivers, trends, opportunities, restraints, and potential challenges that shape the landscape. Moreover, the report provides key insights, including technological advancements, an overview of guidelines for the quality control of IVDs, and key industry developments. Moreover, the report offers insights into market share analysis and detailed company profiles.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.5% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product & Services, Technology, End-user, and Region |

|

By Product & Services |

· Quality Control Products o Serum/Plasma-Based Controls o Whole Blood-Based Controls o Urine-Based Controls o Others · Quality Control Data Management Solutions · Quality Assurance Services |

|

By Technology |

· Clinical Chemistry · Immunoassay · Molecular Diagnostics · Microbiology · Hematology · Others |

|

By End-user |

· Hospitals · Independent/Commercial Laboratories · Academic & Research Institutes · Others |

|

By Region |

· North America (By Product & Services, Technology, End-user, and Country) o U.S. (Product & Services) o Canada (Product & Services) · Europe (By Product & Services, Technology, End-user, and Country/Sub-region) o Germany (Product & Services) o U.K. (Product & Services) o France (Product & Services) o Spain (Product & Services) o Italy (Product & Services) o Scandinavia (Product & Services) o Rest of Europe (Product & Services) · Asia Pacific (By Product & Services, Technology, End-user, and Country/Sub-region) o China (Product & Services) o Japan (Product & Services) o India (Product & Services) o Australia (Product & Services) o Southeast Asia (Product & Services) o Rest of Asia Pacific (Product & Services) · Latin America (By Size, Procedure, End-user and Country/Sub-region) o Brazil (Product & Services) o Mexico (Product & Services) o Rest of Latin America (Product & Services) · Middle East & Africa (By Product & Services, Technology, End-user, and Country/Sub-region) o GCC (Product & Services) o South Africa (Product & Services) o Rest of the Middle East & Africa (Product & Services) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.55 billion in 2025 and is projected to reach USD 2.51 billion by 2034.

In 2025, the North America market value stood at USD 0.60 billion.

The market is expected to grow at a CAGR of 5.5% over the forecast period.

The diagnostic devices segment led the market by product.

The key factor driving the market is rising regulatory scrutiny and the need for standardization.

Bio-Rad Laboratories, Inc. and Thermo Fisher Scientific, Inc. are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us