Laminating Adhesives Market Size, Share & Industry Analysis, By Resin Type (Polyurethane, Acrylic, and Others), By Technology (Solvent-Based, Solvent-Less, Water-Based, and Others), By End-Use Industry (Packaging, Industrial, and Transportation), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

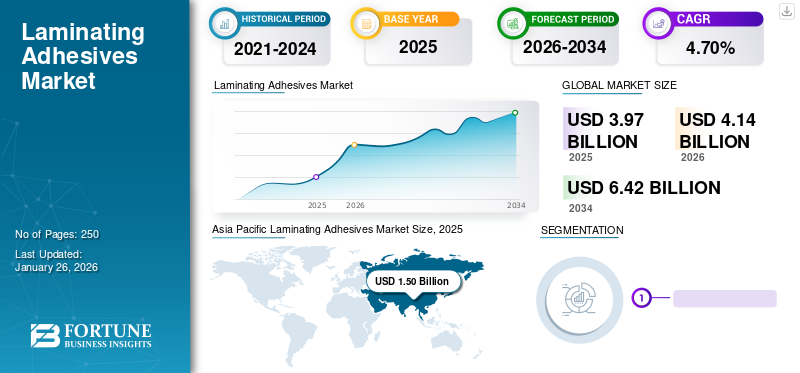

The global laminating adhesives market size was valued at USD 3.97 billion in 2025. The market is projected to grow from USD 4.14 billion in 2026 to USD 6.42 billion by 2034, exhibiting a CAGR of 4.70% during the forecast period. Asia Pacific dominated the laminating adhesives market with a market share of 38% in 2025. Moreover, the laminating adhesives market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 954.23 million by 2032, driven by the rising demand for flexible packaging and increased adoption in the automotive and electronics industries.

Laminating adhesives is an essential component to produce films with advanced functions by laminating multiple films, which are bonded together to form a top layer. These include plastic film, aluminum foil, paper, and others. The laminating mechanisms are cured using heat or a combination of heat and pressure, similar to hot melt adhesives. These adhesives can bond well, withstand high temperatures, and shield from low-risk environmental factors. The adhesives’ properties are always apparent and are used to laminate paper or films that need to be read while protecting them from water and tearing.

Laminating adhesives can bond certain surfaces due to their varied compositions. Some products stick to paper, metal, glass, and masonry, while others stick to textiles, wood, and porous surfaces. The adhesives can also join two different materials such as rubber and metal. A laminating adhesive may or may not contain solvents. They can be made resistant to chemicals, UV rays, and humidity and withstand temperatures up to 450°F. Besides, these can also be developed for use in high-voltage applications and with electrical goods.

The spread of COVID-19 led to a reduced demand for laminating adhesives owing to the shutdown of operations by various end-use industries. These included food & beverage, electronics, pharmaceuticals, and other sectors. It forced manufacturers to reduce production. Also, limitation on the movement and trade disrupted the supply chains involved in the market. Market trends, such as breaks in cash flow, transfer in resource allocation, the essential for social distance, and others will bring about change on every stage.

Download Free sample to learn more about this report.

LAMINATING ADHESIVES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.97 billion

- 2026 Market Size: USD 4.14 billion

- 2034 Forecast Market Size: USD 6.42 billion

- CAGR: 4.70% from 2026–2034

- Asia Pacific dominated the laminating adhesives market with a 38.0% share in 2025.

- The polyurethane segment is projected to hold the largest market share of 39.37% in 2026.

- The solvent-based technology segment is projected to hold a 41.3% share in 2026.

Asia Pacific

Asia Pacific held 38.0% share in 2025, valued at USD 1.50 billion.

Europe

Europe market valued at USD 1.17 billion in 2025.

North America

North America market valued at USD 1.01 billion in 2025.

U.S.

U.S. Market valued at USD 0.72 billion by 2026.

Japan

Japan Market valued at USD 0.26 billion by 2026.

Read More

Laminating Adhesives Market Trends

Rising Adoption of Solvent Free and Water Based Adhesives to Propel Industry Expansion

As environmental awareness has grown, solvent-free adhesives have become more common in the flexible packaging industry. It eliminates the erosion of organic solvent on printing ink caused by residual solvents in packaging products. Solvent-free adhesives are a future development trend that will be multifunctional and able to work with various materials in various industries. Waterborne adhesives are eco-accommodating and less harmful to on-site laborers. Water is a much cheaper solvent than organic solvent. Besides, waterborne adhesives are safer and less expensive than similar solvent-based adhesives. These are some of the primary reasons for driving the global laminating adhesives market growth. Asia Pacific witnessed a laminating adhesives market growth from USD 1.37 billion in 2023 to USD 1.43 billion in 2024.

Download Free sample to learn more about this report.

Laminating Adhesives Market Growth Factors

Growing Demand for Flexible Packaging in the Food & Beverage Industry to Propel Industry Expansion

Surge in the population in the urban areas has increased the demand for flexible packaging which is bringing innovative trends of smarter and safer packaging in the food & beverages industry. The necessity for laminating adhesives has risen recently from general-purpose economic packages to high-performance applications such as direct usage microwavable packaging. This calls for the manufacturer to integrate laminating coating with energy-efficient and eco-friendly structures that can be used under dry food packaging (snack food, soup pouches, coffee, pasta, and others), fresh food packaging (meat, cheese, and fish packaging), fruit juices stand-up pouch, confectionery and ice cream packaging, portion lidding, glass lidding (dairy products, dry food), and ready meal packaging. Thus, the flexible packaging sector is expected to increase the global market size significantly.

Advances in Technology Lead to Development of Eco-Friendlier and More Sustainable Laminating Adhesives

Advances in technology have revolutionized the production of laminating adhesives, making them eco-friendlier and more sustainable. With the increasing awareness of environmental issues, manufacturers have started developing adhesives that have minimal impact on the environment, while still providing the same level of performance as traditional adhesives.

New eco-friendly laminating adhesives are being made using plant-based or recycled materials that are non-toxic and biodegradable. Additionally, some manufacturers are now using renewable energy sources to power their production processes, thereby reducing their carbon footprint. These sustainable laminating adhesives are not only better for the environment, but they also offer other benefits, such as improved safety for workers and reduced waste. As more businesses adopt sustainable practices, the demand for eco-friendly laminating adhesives is expected to grow, leading to even more advancements in this area.

RESTRAINING FACTORS

Strict Rules and Regulations by Governments on the Disposal of Plastics to Restrain Market Growth

Governments all over the globe have been imposing programs and recycling processes for the release of dangerous chemicals from the recycling shops. This has raised a concern in the way plastics are discarded in the form of bags and holders which pollutes the aqueducts leading to clogging and hence, making a harder impact on marine brutes. Each time, large quantities of plastic is dumped in the oceans, it impacts the food chains of the marine ecosystems. Due to this, global authorities along with municipal authorities have imposed strict rules and regulations which hampers the demand for laminating bonds.

Laminating Adhesives Market Segmentation Analysis

By Resin Type Analysis

Polyurethane Segment to Hold the Largest Share Owing to the Strong Bonding Hold and Wide Performance Profile

Based on resin type, the market is segmented into polyurethane, acrylic, and others. The polyurethane segment is anticipated to hold a dominant market share of 39.37% in 2026. owing to their characteristics over the other resin types in the market. These adhesives have excellent adhesion to a wide range of substrates with numerous properties. These include non-flammability, enhancement of cure time, and formulation changes that can vary pot life. In addition, good flexibility can be achieved in the cured product. These adhesives remain bonded through a wide range of operating temperatures.

By Technology Analysis

Solvent-Based Segment to Dominate with the Growing Product Use in the Packaging Industry

Based on technology, the market is segmented into solvent-based, solvent-less, water-based, and others, contributing market share anticipated to hold 41.3% globally in 2026. Solvent-borne adhesive is the most widely used technology for flexible packaging laminating adhesives. It offers urethane technology with a long history of product development. Also, it provides good adhesion and performance to meet requirements from general to high-performance food packaging with good adhesion, product resistance, and heat resistance. This is the major driving factor for the growth of solvent-based adhesives.

In the past, general-purpose applications have been served by waterborne acrylic adhesives. For converters, waterborne adhesive typically costs less than solvent-borne adhesive. An emulsion polymer known as waterborne acrylic is produced by water's free radical polymerization of acrylic monomers. The lamination can be immediately slit to the waterborne adhesive with the increased shear strength.

By End-Use Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Packaging Segment to Dominate Due to the Growing Consumer Demand

Based on end-use industry, the market is segmented into packaging, industrial, and transportation, with a share anticipated to hold 64.49% in 2026. The growth in the demand for retail packaging sector and supportive government policies, the packaging sector witnessed a rebound in 2024 and is expected to exhibit a strong growth rate during the forecast period. The adhesives coatings are marketed for multiple packaging applications, including flexible coverings for packaging various products such as vegetables, meat, cheese, condiments, and dairy. Non-food contact applications include medical instrument packaging, pharmaceutical blister packaging, and industrial applications. The industrial segment is expected to hold a 26.6% share in 2024.

The laminating elastic adhesive for industrial use is produced by an extraordinary synthetic technique. It is utilized for clinging to metal, wood, furniture, formica board, design board, high-pressure cover, compressed wood, softwood, cowhide, bassage board, counterfeit calfskin, foam, concrete, elastic, plastics, and different materials. The laminating technology is growing and will create a new set of regimens in bringing safer norms to achieve hygiene solutions in the food and consumer goods sector. All these factors will help to generate the demand for laminating adhesives across various industries.

REGIONAL LAMINATING ADHESIVES MARKET ANALYSIS

Asia Pacific Laminating Adhesives Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The market in Asia Pacific reached USD 1.5 billion in 2025, representing 38.00% of total market revenue, and is projected to reach USD 1.57 billion in 2026. The market growth is fueled by the expanding regional industry, which positively impacts various sectors within the area. The packaging industry in China has been the driving force behind the country's dominance in the Asia Pacific region in 2023 and has witnessed significant growth and development of the sector in the region. The Japan market is valued at USD 0.26 billion by 2026, the China market is valued at USD 0.72 billion by 2026, and the India market is valued at USD 0.29 billion by 2026.

- In China, the transportation segment is estimated to hold a 9.1% market share in 2024.

To know how our report can help streamline your business, Speak to Analyst

North America

The North America market was valued at USD 1.01 billion in 2025, capturing 25.00% of global revenue, and is estimated to reach USD 1.05 billion in 2026. North America’s growing packaging industry will boost the growth of the market in this region. The shift into consumer behavior, market awareness, and demand for packaged food & beverages are driving growth in North America, impacting several end-use industries. The U.S. market is valued at USD 0.72 billion by 2026.

Europe

In 2025, Europe held 29.00% of the global market, reaching a valuation of USD 1.17 billion, and is projected to grow to USD 1.22 billion in 2026. The automotive industry in Germany, which is the largest in Europe, is currently driving market growth in the region. The rapid adoption of electric vehicles is a response to the increasing levels of CO2 emissions. Furthermore, major industrial manufacturers in the area are expected to raise their consumption of products, leading to further growth in the sector. The UK market is valued at USD 0.24 billion by 2026, and the Germany market is valued at USD 0.4 billion by 2026.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 0.17 billion in 2025, accounting for 4.00% share, and is expected to reach USD 0.17 billion in 2026. Industrialization of Latin America has led to growth in the market, particularly in the use of laminated bonds in Industrial and packaged food industries. This trend is expected to accelerate the growth of the market in the region. Meanwhile, Saudi Arabia is driving significant market growth in the Middle East and Africa due to increased consumption in the industrial sector. Furthermore, the rising economy within the region and improved lifestyles of consumers further surge the demand for finished consumer goods such as cosmetics, pharmaceuticals, and packaged food products.

Middle East & Africa market

In 2025, the Middle East & Africa market stood at USD 0.13 billion, representing 3.00% of global demand, and is projected to grow to USD 0.13 billion in 2026.

List of Key Companies in Laminating Adhesives Market

Joint Ventures and Facility Extension are the Prime Strategic Initiatives Implemented by Leading Companies

The foremost market players, including DuPont, H.B. Fuller Company, Henkel AG, 3M, and Dow are companies operating in the materials business.

DuPont has a strong presence in North America and manufactures laminating adhesives. The company is the largest manufacturer of specialty chemicals and advanced raw materials in the region. DuPont has a strong networks of distribution and offers a wide range of products. Other key players in the market have also has a strong regional presence, robust distribution channels, and diverse product offerings.

LIST OF KEY COMPANIES PROFILED:

- DuPont (U.S.)

- H.B. Fuller Company (U.S.)

- Henkel AG (Germany)

- 3M (U.S.)

- Dow (U.S.)

- Sika AG (Switzerland)

- Bostik (France)

- DIC Corporation (Japan)

- Pidilite Industries Limited (India)

- Flint Group (Luxembourg)

KEY INDUSTRY DEVELOPMENTS:

- June 2023- Henkel AG announced a groundbreaking ceremony for its new manufacturing adhesive-based business unit in Shandong Province, China. The new plant will be established at an approximate value of USD 126 million with the name of 'Kunpeng.' The facility would aim to meet the growing demand and Henkel's consumer base by optimizing the supply network in the Asia Pacific and international markets.

- May 2023- H.B. Fuller announced the acquisition of a stake of a U.K.-based venture, Beardow Adam, a family-owned business that commits to innovation and sustainable adhesives offerings. The acquisition aimed to provide a leading position in the H.B. Fuller market portfolio by expanding the customer base and technology to address the market demand.

- April 2023- Bostik, a subsidiary of Arkema Group and a leading producer of specialty adhesives for construction, industrial, and consumer markets, has launched a new series of solvent free adhesive lamination solutions in Asia. The company's HERBERTS series is sustainable, environment-friendly, specifically designed for food packaging solutions, and can be used for industrial and pharmaceutical markets.

- February 2022- Flint Group launched a sustainable UV LED dual cure ink, named EkoCure ANCORA, specifically designed for packaged food and product labeling. These dual inks and coatings are uniquely designed by using low-energy UV LEDs. It has optimized curing with enhanced adhesion to a wide range of substrates.

- November 2022- Sun Chemical, a member of the DIC Corporation group of companies, announced the acquisition of SAPICI, one of the leading manufacturers of high-performance PU for flexible packaging, coating, and industrial purposes. The acquisition aimed to provide DIC/Sun Chemical with a diversified polymer portfolio for various end-use industries.

REPORT COVERAGE

The market research report provides detailed market analysis and focuses on crucial aspects such as resin type, technology, end-use industry, and leading companies. It provides quantitative data regarding value, research methodology for market size estimation, and insights into market trends. It highlights vital industry developments and the competitive landscape. In addition to the above-mentioned factors, the report encompasses various factors contributing to the market growth in recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2026 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.70% from 2026 to 2034 |

|

Unit |

Value (USD Billion), Volume (Million Tons) |

|

Segmentation |

By Resin Type

|

|

By Technology

|

|

|

By End-Use Industry

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.97 billion in 2025 and is projected to reach USD 6.42 billion by 2034.

In 2025, the Asia Pacific market size was valued at USD 1.50 billion.

Registering a significant CAGR of 4.70%, the market will exhibit rapid growth during the forecast period of 2026-2034.

Based on technology, the solvent-based segment is expected to lead the market during the forecast period.

The rising polyurethane demand is a key factor driving industry expansion.

China held the highest market share in 2025.

DuPont, H.B. Fuller Company, Henkel AG, 3M, and Dow are the major players in the market.

The rising demand from the packaging industry in the end-use industry segment is expected to drive the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us