Lancet Market Size, Share & Industry Analysis by Type (Standard Lancet, Safety Lancet {Button-activated [Push/Top Button and Side Button] and Pressure/Contact-activated}, and Specialty Lancet), By Incision Type (Needle and Blade), By Age Group (Adults and Pediatric), By Gauge Size (22G and Below, 23G-28G, and Above 28G), By Application (Blood Glucose Monitoring, Hemoglobin Testing, Cholesterol Testing, and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

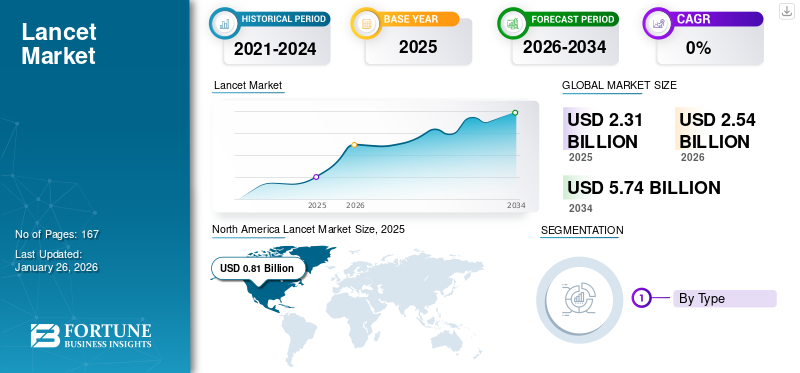

The global lancet market size was valued at USD 2.31 billion in 2025. The market is projected to grow from USD 2.54 billion in 2026 to USD 5.74 billion by 2034, exhibiting a CAGR of 10.72% during the forecast period. North America dominated the lancet market with a market share of 34.98% in 2025.

Lancets are small, sharp medical devices that are used to provide quick, minimally penetrating skin punctures, typically on the tip of the finger. They are most commonly used to draw up capillary blood specimens for blood sugar tests as well as other diagnostic examinations. They are either disposable or part of automated safety devices to minimize the risk of needle-stick injury. The growing awareness about the safety of sharp devices to avoid needle-stick injuries and the rising number of diagnostic and monitoring examinations are driving the demand for lancets globally, augmenting the market growth.

The global market is fragmented, with prominent companies being BD, HTL-STREFA (MTD Medical Technology and Devices), SARSTEDT AG & Co. KG, Cardinal Health, and others. These major players are increasingly implementing various growth strategies such as new product launches, acquisitions, and geographical expansions to capture a substantial market share.

Download Free sample to learn more about this report.

LANCET MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.31 Billion

- 2026 Market Size: USD 2.54 Billion

- 2034 Forecast Market Size: USD 5.74 Billion

- CAGR: 10.72% from 2026–2034

- North America dominated the lancet market with a 34.98% share in 2025.

- The Safety Lancet segment accounted for 51.55% of the market share in 2026.

- The Needle segment led the market with a 93.65% share in 2026.

North America

North America generated USD 0.81 billion in 2025 and is projected to reach USD 0.88 billion in 2026, driven by strong demand for advanced lancets.

Europe

Europe accounted for USD 0.78 billion in 2025 and is expected to reach USD 0.85 billion in 2026, supported by the presence of major industry players.

Asia Pacific

Asia Pacific reached USD 0.62 billion in 2025 and is forecast to grow to USD 0.70 billion in 2026 due to rising diabetes prevalence and healthcare awareness.

U.S.

The market is estimated to reach USD 0.82 billion in 2026

Japan

The market is expanding steadily, supported by increasing demand for blood glucose monitoring and advanced safety lancets.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Prevalence of Diabetes and Chronic Diseases to Drive the Market Growth

Over the past decades, the rising global cases of diabetes have tremendously boosted the product demand as they are used extensively to collect blood specimens to check the daily glucose levels of diabetic patients.

- For instance, the Institute for Health Metrics and Evaluation, in June 2023, revealed that over half a billion people globally are living with diabetes.

In addition, the growing adoption of home-based monitoring solutions as well as the need for convenient, less invasive blood sampling techniques are boosting the demand for advanced types of lancets such as safety lancets. Such a scenario is anticipated to drive the global lancet market growth during the forecast period.

MARKET RESTRAINTS

Cost Sensitivity of Safety Lancets to Restrict Market Expansion

Although routine blood sampling requires lancets, price variation among various types of lancets, such as safety lancets, is expected to challenge their adoption. Lancets that are safety-based, as an example, tend to be more costly than traditional ones, where cost becomes a vital factor, particularly in developing countries where the budget for healthcare is limited.

- For example, NHS data published in October 2020 highlighted that safety lancets typically cost around USD 4.87 to USD 5.06 per 100 units, compared to traditional lancets priced as low as USD 2.37 to USD 4.22 per 100 units.

Such price differences are pushing healthcare professionals to opt for cheaper options and are also deterring advanced product adoption among patients, which is expected to hamper the market growth.

MARKET OPPORTUNITIES

Increasing Need for Home Healthcare Monitoring to Create Lucrative Growth Opportunities

In recent years, the rising demand for home diagnosis has been generating lucrative opportunities for lancet providers to increase their product supply globally. Several patients managing their chronic conditions, especially diabetes, from home is surging the demand for convenient blood sampling devices such as lancets.

- For instance, as per data from the Indian Journal of Medical Specialties, in December 2023, a research study indicated that 35.0% of the 100 patients used a glucometer for self-monitoring of blood glucose levels at home.

As a result, lancets, especially safety lancets that minimize the risk of needle-stick injury occurrence, are gaining importance among patients who need routine blood tests without professional assistance. This is expected to create significant opportunities for manufacturers to increase product manufacturing capacity to meet growing demand, supporting the market expansion.

LANCET MARKET TRENDS

Technological Advancements and Sustainable Designs to Emerge as a Key Market Trend

The integration of ultra-fine gauge technology with ergonomic, user-friendly designs is significantly improving patient comfort and blood sampling accuracy. As a result, manufacturers are increasingly developing lancets with 21G-30G ultra-thin needles and spring-loaded mechanisms to enable nearly painless capillary blood collection.

These innovations are being fueled by stringent regulatory guidelines that encourage the use of safety-engineered sharps to minimize needle-stick injuries in healthcare settings. Additionally, the growing emphasis on sustainability has prompted design improvements such as reduced plastic consumption and the use of biodegradable materials, highlighting a broader shift toward environment-friendly products.

MARKET CHALLENGES

Limited Spending in Developing Regions to Challenge Market Growth

In developing countries, underdeveloped healthcare infrastructure and limited budgets for diagnostic devices are restricting access to high-end products such as lancets. Consequently, people in the affected areas are preferring cheap, sharp objects such as needles due to unaffordability, limited government spending on healthcare, and limited insurance cover.

- For instance, according to data from ScienceDirect in January 2024, the Bangladesh government only dedicates a fraction of 2.34% of the country's national GDP to public health, the lowest level among Asia Pacific countries.

Such restricted spending is limiting the uptake of advanced types of lancets and also limiting importation, further inhibiting access to such products among patients. Moreover, limited awareness about the benefits of the newer, safer, and more user-friendly lancets in these regions is also challenging the market growth of lancets in these regions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Safety Lancets Segment Led the Market in 2024 due to Increasing Adoption among Diabetic Patients

On the basis of the segmentation by type, the market is classified into standard lancets, safety lancets, and specialty lancets.

To know how our report can help streamline your business, Speak to Analyst

The Safety Lancet segment is projected to dominate the market with a share of 51.55% in 2026. The safety lancets segment dominated the global lancet market share in 2024. The growth is attributed to its proven safety and convenience. As a result, type 1 diabetes patients, who require daily monitoring of blood glucose, are using this product for blood drawing to place on the blood glucose meter. In response, the key players are launching advanced safety lancet products to the market, thereby increasing product penetration globally.

- For instance, in May 2021, Owen Mumford launched the Unistik Touch family of safety lancets to achieve a blood volume of 500 μl.

The standard lancet segment is projected to grow at a CAGR of 10.5% during the forecast period.

By Incision Type

Needle Segment to Dominate Due to Lesser Pain and Superior Safety Features

By incision type, the market is categorized into needle and blade.

In 2026, the Needle segment is projected to lead the market with a 93.65% share. the segment is anticipated to dominate with a 93.6% share. Patients are highly preferring needles due to their ease of use, superior safety features, and reduced pain during blood sampling. The demand for needles is increasing more prominently among patients who require frequent testing with less risk of needle-stick injury. This is expected to drive the segment’s growth during the forecast period.

- For instance, a study published by NCBI in April 2020 reported that needle-based lancets caused less pain compared to blade-based lancets during blood sample collection.

The blade segment is expected to grow at a CAGR of 10.0% over the forecast period.

By Age Group

Adults Segment to Dominate Due to Higher Testing Rate and Product Adoption

By age group, the market is categorized into adults and pediatrics.

The adult segment is expected to capture the largest share of the market, accounting for 72.92% in 2026. In 2025, the segment is anticipated to dominate with a 72.8% share. The segment’s growth is attributed to increasing cholesterol testing, HbA1c or glycated hemoglobin testing, and other testing among adults. This is fueling the utilization of lancets among this age group. Furthermore, the increasing blood glucose monitoring in type 2 diabetes adults is also anticipated to increase the utilization of lancets.

The pediatric segment is expected to grow at a CAGR of 10.1% over the forecast period.

By Gauge Size

23G-28G Segment to Dominate Due to Superior Comfort, Less Pain, and Significant Availability

Based on gauge size, the market is trifurcated into 22G and below, 23G-28G, and above 28G.

The 23G–28G segment is expected to hold the largest market share, accounting for 73.35% in 2026. In 2025, the segment is anticipated to dominate with a 73.3% share. The 23G-28G gauge range is thin enough to reduce discomfort compared to larger gauges such as 21G-22G. Moreover, most of the commercially available lancing devices are designed to work optimally with 23G-28G lancets, which further increases product demand and is expected to drive the segment’s growth.

The above 28G segment is expected to grow at a CAGR of 10.1% over the forecast period.

By Application

Blood Glucose Monitoring Segment to Dominate Due to Growing Diabetic Population

Based on application, the market is segmented into blood glucose monitoring, hemoglobin testing, cholesterol testing, and others.

The blood glucose monitoring segment accounted for the largest share of the market in 2024. In 2025, the segment is anticipated to dominate with a 56.3% share. The growth is attributed to the increasing number of individuals self-monitoring their blood glucose, thereby driving the purchase rate of lancets. Additionally, increasing diabetes prevalence globally is supporting the demand for lancets by pushing the need for self-monitoring of blood glucose.

- For instance, according to the International Diabetes Federation (IDF), as of July 2025, the global diabetic population is expected to reach around 783.0 million by 2045.

The hemoglobin testing segment is expected to grow at a CAGR of 10.8% over the forecast period.

By Distribution Channel

Retail Pharmacies Segment to Dominate Due to Direct Accessibility and Convenience

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies.

In 2024, the global market was dominated by retail pharmacies in terms of distribution channel. Most custom-fitted devices are prescribed and fitted at dental clinics. There is a surge in the number of retail pharmacies globally. This is making them the most convenient point of purchase for routine self-monitoring devices, such as lancets, due to widespread availability. In addition, these channels are selling lancets in combination with glucose meters, strips, or diabetes care kits to primary users, which is expected to fuel the segment’s growth. The segment is set to hold 51.9% share in 2025.

- For instance, in July 2025, CVS Pharmacy celebrated the grand opening of a new 13,000-square-foot store on Washington Avenue in Southwest Center City, Philadelphia, expanding to nearly 50 locations citywide with enhanced pharmacy, health, and wellness services.

In addition, the hospital pharmacies segment is projected to grow at a CAGR of 10.2% during the forecast period.

Lancet Market Regional Outlook

On the basis of geography, the market has been subdivided into North America, Latin America, Europe, Asia Pacific, and the Middle East & Africa.

North America

North America Lancet Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The market in North America reached USD 0.81 billion in 2025, representing 34.98% of total market revenue, and is projected to reach USD 0.88 billion in 2026. the region also accounted for a major share with a value of USD 0.88 billion. The growth is attributed to the strong demand for advanced products and reimbursement for chronic disease monitoring devices, including lancets. This is driving the key players to increase the supply of such products in the region. In 2026, the U.S. market is estimated to reach USD 0.82 billion.

- As of September 2025, Medicare Part B Preventive Services for Diabetes provides coverage of up to 300 lancets every three months for patients undergoing insulin therapy.

Europe

Europe contributed approximately USD 0.78 billion to the global market in 2025, accounting for 33.58% share, and is expected to reach USD 0.85 billion in 2026. Europe is projected to expand at a substantial rate in the coming years and is expected to record the second-highest growth rate of 10.2% during the forecast period, reaching a market value of USD 0.78 billion by 2025. The growth is largely attributed to the strong presence of key players in countries such as the U.K., Germany, and France, which contributes to the wide availability of lancets in the region. Based on these factors, the U.K., Germany, and France are projected to record market values of USD 0.07 billion, USD 0.19 billion, and USD 0.07 billion, respectively, by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 0.62 billion, representing 26.90% of global demand, and is projected to grow to USD 0.7 billion in 2026. The growth in the region is supported by increasing healthcare awareness and the rising prevalence of chronic diseases requiring regular blood glucose monitoring. Furthermore, India and China are expected to reach market values of USD 0.15 billion and USD 0.32 billion, respectively, by 2026.

Latin America

The Latin America market accounted for USD 0.07 billion in 2025, representing 3.03% of the global industry, and is expected to reach USD 0.07 billion in 2026. Latin America is projected to witness moderate growth during the forecast period. Growth in the region is primarily driven by increasing penetration and supply of lancets, along with rising awareness about safety and specialty lancets.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 0.03 billion in 2025, accounting for 1.50% share, and is expected to reach USD 0.04 billion in 2026. The Middle East & Africa region is also anticipated to experience moderate growth over the projection period. In this region, GCC countries are projected to reach a market value of USD 0.02 billion in 2025, supported by growing healthcare awareness and increasing adoption of safety lancets.

COMPETITIVE LANDSCAPE

Key Industry Players

Extensive Product Range and Growing Adoption of Customized Devices Strengthened the Leading Position of Key Players

The global lancet market is highly fragmented, with major players such as HTL-STREFA, BD, and Abbott holding a dominant share in 2024. These companies are focusing on strengthening their market hold by increasing product availability worldwide, launching innovative products, and signing strategic distribution agreements.

- In January 2025, BD announced additional investments in its U.S. manufacturing facilities to increase production capacity for critical medical devices, including syringes, needles, lancets, and IV catheters, in response to the rising needs of the healthcare system.

Moreover, these players are focusing on portfolio diversification to solidify their market position. Other major participants in the market include Cardinal Health, B. Braun SE, Terumo Medical Corporation, and SARSTEDT AG & Co. KG. These players are emphasizing product innovation and global expansion strategies to strengthen their brand reputation and market position.

LIST OF KEY LANCET COMPANIES PROFILED

- BD (U.S.)

- SARSTEDT AG & Co. KG (Germany)

- Greiner Bio-One International GmbH (Germany)

- HTL-STREFA (MTD Medical Technology and Devices) (Poland)

- Terumo Medical Corporation (Japan)

- Braun SE (Germany)

- Abbott (U.S.)

- Cardinal Health (U.S.)

- YPSOMED (Switzerland)

- Medline Industries, LP. (U.S.)

- Biosense Technologies Private Limited (India)

KEY INDUSTRY DEVELOPMENTS

- April 2025 – SteriLance Medical (Suzhou) Inc. showcased its product portfolio, including lancets, at CMEF Spring 2025.

- November 2024 – SteriLance Medical (Suzhou) Inc. announced its participation in MEDICA 2024 (Germany), presenting its innovative range of pressure/contact-activated safety lancets.

- August 2024 – HTL-STREFA, Inc, acquired Ypsomed’s pen needles and blood glucose monitoring systems. Integrating Ypsomed's pen needle and lancet operations into HTL-STREFA, Inc,’s European production and distribution network raised its total production capacity to over 2.5 billion pen needles and lancets.

- May 2021 – Owen Mumford launched the Unistik Touch series of pressure/contact-activated safety lancets, designed for blood collection of up to 500 μl.

- January 2019 – MediPurpose struck an agreement with Premier Inc. to include SurgiLance pressure/contact-activated safety lancets in its offerings.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.72% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Incision Type

By Age Group

By Gauge Size

By Application

By Distribution Channel

By Geography North America (By Type, Incision Type, Age Group, Gauge Size, Application, Distribution Channel, and Country)

Europe (By Type, Incision Type, Age Group, Gauge Size, Application, Distribution Channel, and Country/Sub-region)

Asia Pacific (By Type, Incision Type, Age Group, Gauge Size, Application, Distribution Channel, and Country/Sub-region)

Latin America (By Type, Incision Type, Age Group, Gauge Size, Application, Distribution Channel, and Country/Sub-region)

Middle East & Africa (By Type, Incision Type, Age Group, Gauge Size, Application, Distribution Channel, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.31 billion in 2025 and is projected to reach USD 5.74 billion by 2034.

In 2025, the North America market value stood at USD 0.81 billion.

The market is expected to exhibit a CAGR of 10.72% during the forecast period of 2026-2034.

In 2025, the safety lancets segment led the market by type.

The key factors driving the market are the increasing prevalence of diabetes and an increasing demand for home-based monitoring.

BD, SARSTEDT AG & Co. KG, HTL-STREFA, and Abbott are some of the prominent players in the market.

North America dominated the market in 2024.

Innovation of ultra-thin needles, increasing SMBG users, and new launches are favoring the product adoption globally.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us